Market Overview

| Study Period | 2020 - 2031 |

|---|---|

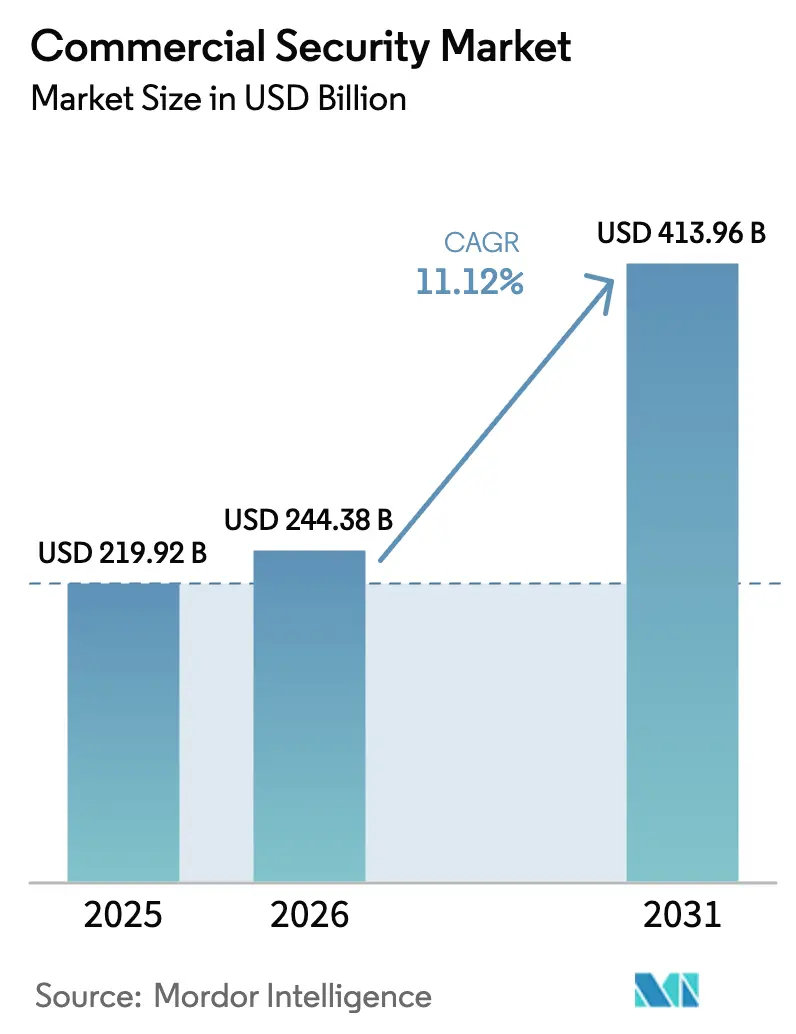

| Market Size (2026) | USD 244.38 Billion |

| Market Size (2031) | USD 413.96 Billion |

| Growth Rate (2026 - 2031) | 11.12% CAGR |

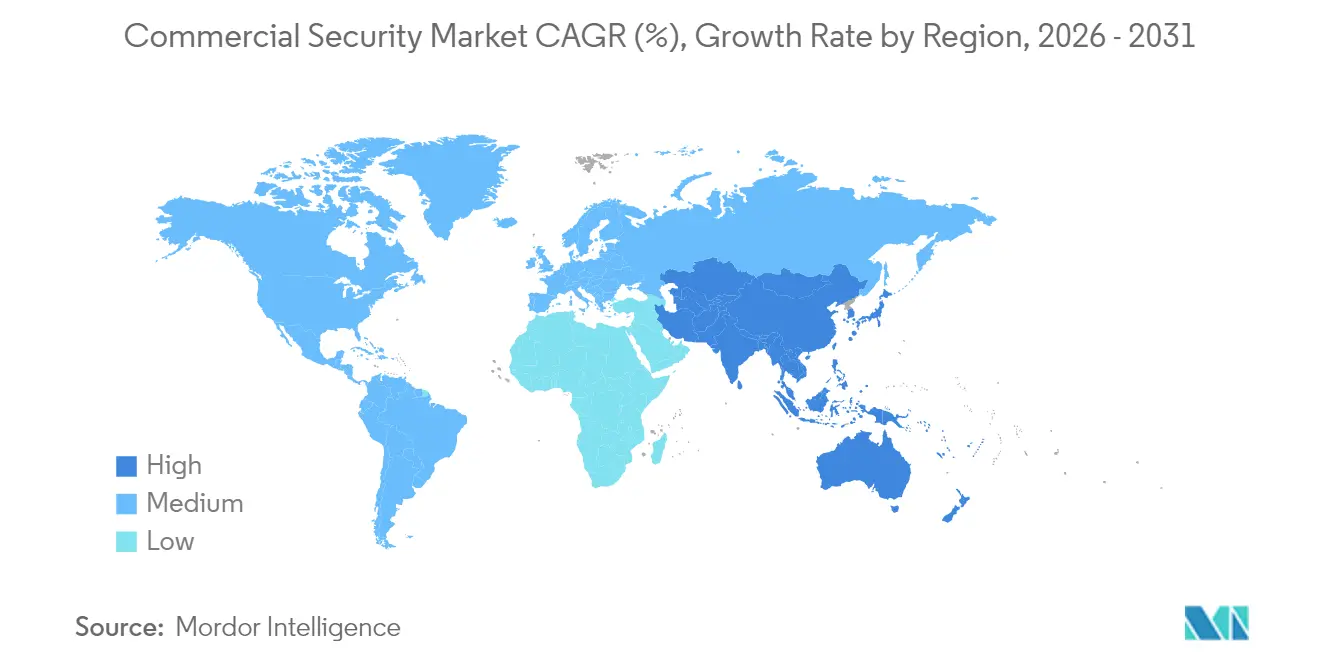

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Commercial Security Market Analysis by Mordor Intelligence

The Commercial security market size was valued at USD 219.92 billion in 2025 and estimated to grow from USD 244.38 billion in 2026 to reach USD 413.96 billion by 2031, at a CAGR of 11.12% during the forecast period (2026-2031). The step-up reflects how organisations now treat security installations as data-rich operational platforms, not isolated safety gear. Regulations such as Alyssa’s Law in the United States have forced the rapid adoption of multi-sensor solutions that fuse video, access, communication, and analytics. Enterprises are also converging physical and cyber safeguards inside operational-technology networks, driving demand for software-centric platforms that orchestrate both realms. Meanwhile, cloud-native video services are lowering ownership costs for multi-site retailers, and insurers have begun offering premium incentives when AI fire-detection tools are installed. These economic levers amplify purchasing momentum across every end-user segment.

Key Report Takeaways

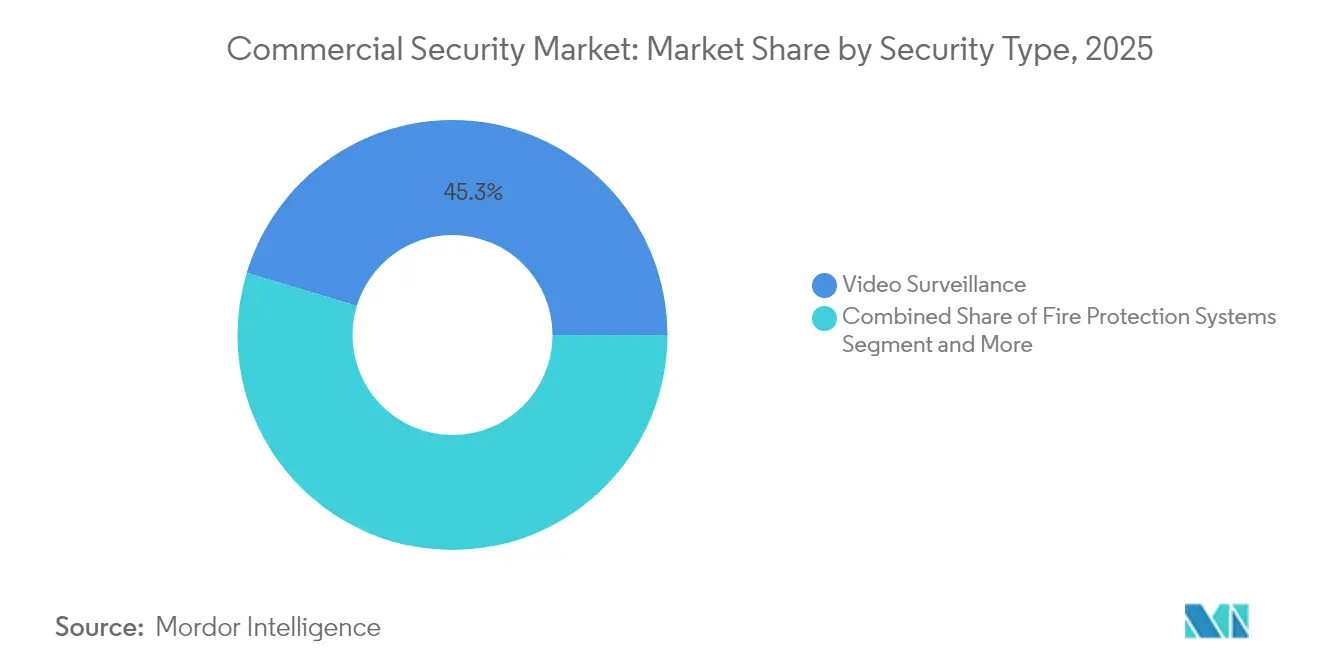

- By security type, video surveillance led with a 45.32% share of the Commercial security market in 2025, while access control is forecast to post the fastest 11.36% CAGR through 2031.

- By component, hardware held a 66.78% share of the Commercial security market size in 2025; services are projected to expand at an 11.75% CAGR during 2026-2031.

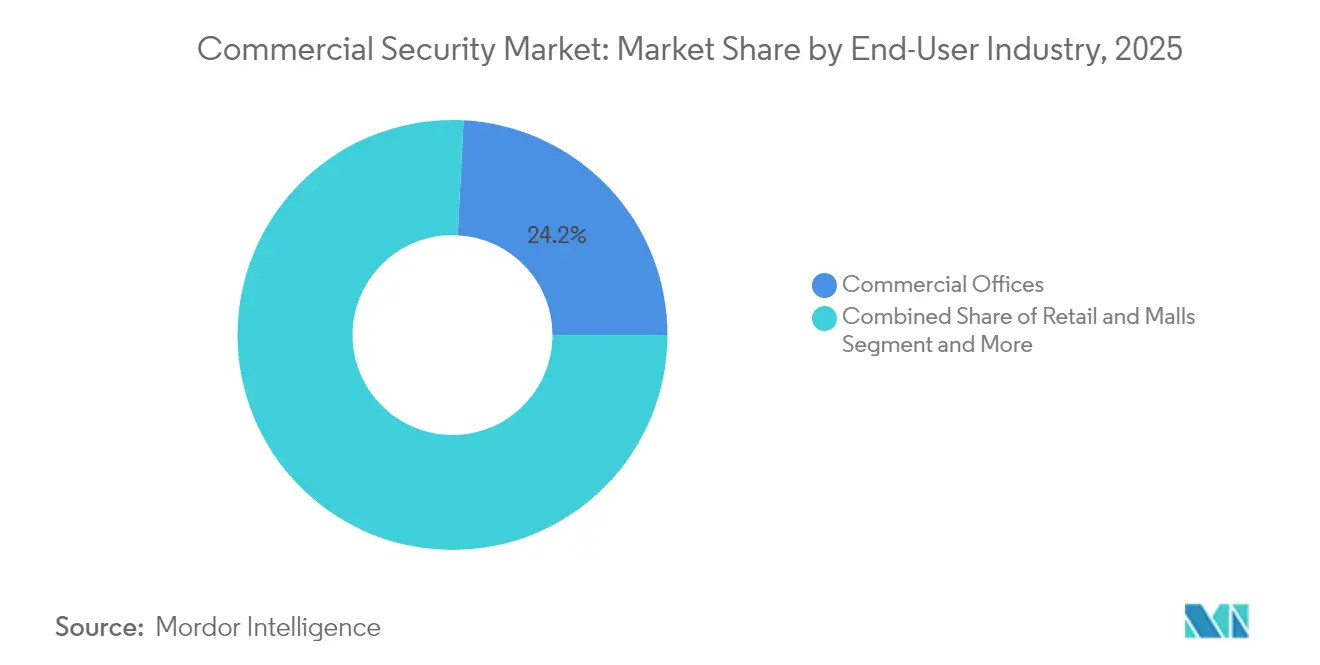

- By end-user industry, commercial offices captured 24.18% of the Commercial security market size in 2025, whereas healthcare facilities are expected to advance at a 11.47% CAGR to 2031.

- By organisation size, large enterprises commanded 71.34% of the Commercial security market share in 2025; SMEs are growing at the fastest rate, with a 11.96% CAGR.

- By geography, North America dominated the market with 33.78% revenue in 2025; however, the Asia Pacific is poised for an 11.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Commercial Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Workplace safety mandates driving multi-sensor platforms | +2.1% | North America & EU | Medium term (2-4 years) |

| Convergence of physical and cyber security within OT networks | +1.8% | Global | Long term (≥ 4 years) |

| Cloud-native video surveillance reducing TCO for multi-site retail chains | +1.5% | Global, early gains in North America & APAC | Short term (≤ 2 years) |

| Insurance premium discounts for AI-enabled fire detection systems | +1.2% | North America & EU | Medium term (2-4 years) |

| Rapid uptake of mobile-credential access control in co-working spaces | +1.4% | Global, urban centres | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Workplace Safety Mandates Driving Multi-Sensor Platforms

Legislative frameworks are compelling organizations to deploy comprehensive threat detection systems that extend beyond traditional perimeter security. The implementation of Alyssa's Law across multiple U.S. states requires educational institutions to install panic alert systems with direct law enforcement connectivity, creating demand for integrated platforms that combine access control, video surveillance, and emergency communication capabilities.[1]Security Magazine. "Notable Physical Security Trends of 2024." November 14, 2024. securitymagazine.com This regulatory push is driving the adoption of AI-powered security systems that can differentiate between routine activities and potential threats, with 56% of end-users now optimizing operations through their security systems rather than viewing them as purely protective measures. The convergence of safety mandates with technological capabilities is creating a multiplier effect, where compliance requirements become catalysts for broader modernization of security infrastructure. Organizations are discovering that multi-sensor platforms not only satisfy regulatory obligations but also provide operational intelligence that improves facility management and emergency response coordination. The economic impact extends beyond compliance costs, as integrated systems reduce the total cost of ownership through consolidated management interfaces and shared infrastructure components.

Convergence of Physical and Cyber Security within OT Networks

The integration of operational technology networks with physical security systems is creating new attack vectors that require unified defense strategies. Industrial facilities and critical infrastructure are increasingly adopting cyber-physical security convergence frameworks that treat physical access controls as cybersecurity endpoints, necessitating the use of quantum-safe cryptography and advanced authentication protocols. This convergence is particularly evident in healthcare facilities, where unified physical security platforms enable the quick identification and response to incidents while maintaining compliance with data protection regulations.[2]Campus Security Today. "How Hospitals are Using Modern Technology to Improve Security." October 1, 2024. campussecuritytoday.com The shift toward three-way security convergence, integrating physical security, OT security, and cybersecurity, is being driven by the recognition that siloed approaches create vulnerabilities that sophisticated threat actors can exploit. Organizations are implementing security frameworks that provide real-time correlation between physical access events and network activity, enabling proactive threat detection and response. The economic rationale for convergence extends beyond security benefits, as unified platforms reduce operational complexity and enable more efficient resource allocation across security functions.

Cloud-Native Video Surveillance Reducing TCO for Multi-Site Retail Chains

The migration to cloud-based video surveillance architectures is fundamentally altering the economics of multi-site security deployments. Retail chains are adopting cloud-native platforms that eliminate the need for on-premises storage infrastructure while providing advanced analytics capabilities that were previously accessible only to large enterprises. Genetec's Security Center SaaS platform, launched in 2024 with pricing starting at USD 149 per device annually, exemplifies this shift by offering enterprise-grade video management capabilities through a subscription model that reduces upfront capital requirements.[3]Genetec Inc. "Genetec Announces Availability of Security Center SaaS." April 1, 2024. genetec.com The total cost of ownership reduction stems from eliminated hardware refresh cycles, reduced IT staffing requirements, and the ability to scale storage capacity dynamically based on actual usage patterns. Cloud-native architectures also enable advanced AI-powered analytics that can identify patterns across multiple locations, providing retailers with insights into customer behavior and operational efficiency that extend beyond traditional security applications. The subscription-based model aligns security costs with business growth, making advanced surveillance capabilities accessible to smaller retailers while providing enterprise clients with predictable operational expenses.

Rapid Uptake of Mobile-Credential Access Control in Co-Working Spaces

The proliferation of flexible work arrangements is driving demand for access control systems that can accommodate dynamic occupancy patterns and temporary access requirements. Mobile credential technology has evolved beyond simple card replacement to encompass multi-layered authentication methods that provide enhanced security while improving user experience. The technology's adoption is particularly pronounced in co-working spaces, where operators must manage hundreds of users with varying access privileges and temporal requirements, creating operational complexity that traditional card-based systems cannot efficiently address. Mobile credentials enable real-time access management that can be modified remotely, reducing administrative overhead while providing detailed audit trails that support compliance requirements. The economic benefits extend beyond operational efficiency, as mobile systems eliminate the costs associated with physical card production, distribution, and replacement, while reducing the risk of credential sharing or loss. The integration of mobile credentials with broader facility management systems is creating new opportunities for space optimization and user experience enhancement, positioning access control as a value-added service rather than a security necessity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented building codes delaying retrofit projects | –1.3% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Data-residency regulations hindering cross-border video storage | –0.8% | EU & GCC | Medium term (2-4 years) |

| Component lead-time volatility for semiconductors and optics | –1.1% | Global | Short term (≤ 2 years) |

| Low end-user awareness of TCO benefits in MEA | –0.7% | Middle East & Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Building Codes Delaying Retrofit Projects

Post-disaster rebuilding in Los Angeles reveals permitting cycles that extend past one year for single-family homes, let alone commercial towers. Integrators must navigate diverse fire, accessibility, and cyber addenda, inflating design hours and eroding project IRR. This complexity deters owners from overhauling legacy estates, especially in developing regions where code enforcement varies across municipalities.

Data-Residency Regulations Hindering Cross-Border Video Storage

The UAE’s 2021 Data Protection Law and the EU AI Act classify biometric analytics as high-risk, requiring enterprises to store footage locally or demonstrate adequate safeguards. Retailers with pan-regional portals must fund hybrid clouds that silo EU data, raising the cost per retained hour of video. Compliance audits add operational overhead and constrain vendor selection.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Security Type: Access Control Systems Accelerate Despite Video Dominance

Video surveillance retained a 45.32% share of the Commercial security market in 2025 by leveraging AI analytics that transform cameras into predictive sensors. The segment benefits from cloud offloading of storage and real-time object recognition, which reduces false alarms and provides valuable insights into customer flow for retailers. Access control, however, is tracking the fastest 11.36% CAGR as smartphone-based credentials and IT security convergence spur refresh activity in offices and healthcare facilities. Mobile solutions deliver password-quality cryptography, while APIs let identity-management tools grant or revoke door rights instantly. Fire detection platforms hold steady demand on the back of code mandates, whereas perimeter-intrusion systems now integrate AI to filter wildlife motion. Integrated security management suites, which overlay analytics and policy engines across multiple device categories, represent a rapidly growing niche for enterprises seeking a single-pane-of-glass view.

Adoption momentum for mobile credentials is sharpest in co-working hubs where tenant turnover is high. Operators appreciate remote issuance, and occupants prefer device-free entry, which cuts badge inventory costs. Healthcare systems value audit trails that correlate patient-care events with staff movement, supporting compliance with life-safety protocols. Genetec’s six-year 28% CAGR in access control symbolises how software innovation is outrunning hardware turnover. Integration with cyber-defence tools also shortens incident-response times, illustrating why investors view access control as a software play within the broader Commercial security systems market.

By Component: Services Surge as Hardware Commoditises

Hardware still comprised 66.78% of the Commercial security market size in 2025, covering cameras, controllers, and sensors that anchor any deployment. Price competition and silicon shortages, however, are squeezing margins, pushing vendors to pivot toward services. Managed security, design consulting, multi-year maintenance contracts, and usage-based cloud storage are rising at an 11.75% CAGR as customers outsource complexity. Software analytics, powered by edge AI chips, extract behavioural patterns and anomaly alerts from raw feeds, creating upsell paths that do not depend on new metal.

The services uptrend dovetails with cybersecurity demands. Continuous vulnerability scans, firmware patches, and compliance reporting are now included in service-level agreements. Johnson Controls’ Metasys 14.0 demonstrates how analytics upgrades are delivered over the air, requiring ongoing subscriptions rather than one-off licences. For channel partners, recurring revenue smooths cash flow and raises customer lifetime value. Cloud storage also eliminates the headache of on-premises RAID refreshes, linking expenditure directly to retention policies and video analysis intensity.

By End-User Industry: Healthcare Facilities Drive Growth Despite Office Dominance

Commercial offices held 24.18% of the Commercial security market share in 2025 as corporate landlords integrated Physical Identity and Access Management suites that span multi-tower campuses. Tenants demand cohesive visitor vetting, package delivery tracking, and elevator dispatch, which central software consoles now manage. While offices retain scale, healthcare is charting an 11.47% CAGR because hospitals require 24/7 monitoring, staff-safety duress buttons, and seamless cross-wing access audits. Regulations governing patient data and narcotic storage further intensify security spending.

Hospitals are layering IoT sensors onto badge events to track equipment and monitor environmental parameters that influence infection control. The blend of life-safety and cybersecurity concerns makes integrated platforms indispensable. Retail venues harness cloud-based VMS to analyze shopper traffic and optimize staffing. Warehouses embed access readers on forklift charge bays to log operator licences, aligning with OSHA audits. Each use case pushes vendors to package sector-specific analytics modules, thereby raising the overall value proposition of the commercial security systems market.

By Organisation Size: SMEs Embrace Cloud-Based Solutions

Large enterprises still account for 71.34% of the Commercial security market size due to multi-site estates and compliance mandates. They rely on federated VMS clusters and central security operations centres for real-time situational awareness. Yet SMEs are the growth engine, expanding at 11.96% CAGR. Subscription pricing removes heavy capex hurdles, while plug-and-play devices ship with LTE fail-over, negating the need for dedicated IT staff. The ASSA ABLOY Centrios model, priced at USD 20 per month for 50 doors, resonates with micro-chains and professional services firms that lease rather than own property.

Cloud dashboards provide SME owners with instant insight into alarm status and visitor logs via mobile apps, democratizing features once reserved for Fortune 500 budgets. Integrated cyber-health checks flag weak passwords on routers, underscoring the trend toward convergence. As SME adoption scales, the Commercial security market benefits from a longer tail of customers, diversifying revenue and prompting vendors to widen channel programmes that cater to installers servicing local businesses.

Geography Analysis

North America retained 33.78% of global revenue in 2025, driven by stringent life-safety regulations and early adoption of AI. Regulatory momentum, such as Alyssa’s Law, continues to feed hardware refresh cycles, while cloud VMS adoption cuts recurring IT overhead. Supply-chain vulnerabilities, spotlighted by the Spruce Pine quartz mine disruption, underscore the strategic imperative for domestic sensor production.

The Asia Pacific is racing ahead with an 11.06% CAGR, driven by smart-city programs and a vast SME base that values cloud credentials. National AI policies in the UAE and Saudi Arabia (part of the broader Middle East) further stimulate AI-powered deployments compliant with data-sovereignty rules. Europe’s enforcement of the AI Act renders biometric systems high-risk, driving demand for local-edge processing to keep data onshore. GCC data-centre booms and strong infrastructure spending create fresh demand across the region.

South America is entering a stabilization phase as inflation eases and governments sharpen public-safety mandates. Mexico’s logistics corridors and Brazil’s retail modernization are accelerating upgrades from analog CCTV to hybrid cloud VMS, while privacy statutes such as Brazil’s LGPD are pushing vendors toward encrypted-edge architectures. In contrast, Africa’s growth is tied to infrastructure resilience, airports, utilities, and industrial parks are prioritising ruggedised sensors and solar-backed surveillance to counter grid volatility. Across both regions, donor-funded city surveillance initiatives and telecom-led cloud bundles are expanding access to enterprise-grade security, boosting baseline demand through 2030.

Competitive Landscape

Competition is moderate yet intensifying as platform economics overtake pure hardware sales. Honeywell’s USD 4.95 billion purchase of Carrier’s LenelS2, Onity, and Supra lines builds an end-to-end stack spanning cloud VMS, mobile credentials, and analytics, illustrating a pivot toward lifetime-value monetisation. Bosch’s decision to divest its security communications arm to Triton for USD 735 million suggests that scale alone no longer guarantees a strategic fit; software orchestration and recurring services revenue now dominate boardroom agendas.

White-space entrants such as Alarm.com and Suprema AI showcase pure-play AI differentiation, winning industry awards for autonomous deterrence and ATM-fraud prevention. Systems integrators are partnering with consultancies; the Convergint-Deloitte alliance bundles cyber-assessment with physical-device rollout, meeting the C-suite's appetite for a single, accountable partner. Patent activity around risk-scoring engines that weight physical and IT signals suggests the next battlefield will be algorithmic intellectual property rather than camera sensor count.

Vendor strategy centres on three pillars. First, acquire installed bases that can be migrated to cloud service plans. Second, embed AI analytics that extract cross-functional insights, elevating the platform from a cost centre to a productivity engine. Third, offer zero-trust-ready architectures to address board-level cyber liability exposure. Firms executing on all three capture premium margins even as device ASPs soften.

Commercial Security Industry Leaders

-

Honeywell International Inc.

-

Johnson Controls International plc

-

Carrier Global Corporation

-

Bosch Security and Safety Systems

-

Hangzhou Hikvision Digital Technology Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Honeywell closed the USD 4.95 billion purchase of Carrier’s Global Access Solutions arm, unifying LenelS2, Onity and Supra under one cloud platform.

- February 2022: Honeywell detailed a three-way split into Automation, Aerospace and Advanced Materials to sharpen operational focus on high-growth building-automation software.

- February 2025: Johnson Controls posted USD 5.4 billion Q1 sales and lifted FY25 EPS guidance, citing an USD 13.2 billion Building Solutions backlog.

- January 2025: Johnson Controls acquired Webeasy to deepen proprietary building-control IP.

- January 2025: Alarm.com rolled out AI Deterrence, an adaptive voice warning module that integrates with existing smart-home hubs.

- December 2024: Triton agreed to buy Bosch’s security communications unit for USD 735 million, aiming to scale the business as an independent integrator.

Global Commercial Security Market Report Scope

Commercial security refers to the protection systems that are commonly found in offices, apartment buildings, and other commercial establishments with an integrated set of components that work collectively. These security systems are different from home alarm systems because they monitor activities in large open spaces. Access control, video surveillance, and fire protection systems are widely used commercial security systems.

The global commercial security market is segmented By Security Type (Fire Protection System, Video Surveillance, Access Control System) and Geography (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa).

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Security Type

| Fire Protection Systems |

| Video Surveillance |

| Access Control Systems |

| Intrusion and Perimeter Detection |

| Integrated Security Management Platforms |

By Component

| Hardware (Cameras, Sensors, Panels) |

| Software/Analytics |

| Services (Design, Installation, AMC, Cloud Storage) |

By End-User Industry

| Commercial Offices |

| Retail and Malls |

| Hospitality and Leisure |

| Healthcare Facilities |

| Educational Campuses |

| Industrial and Warehousing |

| BFSI |

| Others |

By Organization Size

| SMEs |

| Large Enterprises |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Nordics | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia Pacific | |

| Middle East and Africa | Saudi Arabia |

| UAE | |

| Turkey | |

| South Africa | |

| Kenya | |

| Rest of Middle East and Africa |

| By Security Type | Fire Protection Systems | |

| Video Surveillance | ||

| Access Control Systems | ||

| Intrusion and Perimeter Detection | ||

| Integrated Security Management Platforms | ||

| By Component | Hardware (Cameras, Sensors, Panels) | |

| Software/Analytics | ||

| Services (Design, Installation, AMC, Cloud Storage) | ||

| By End-User Industry | Commercial Offices | |

| Retail and Malls | ||

| Hospitality and Leisure | ||

| Healthcare Facilities | ||

| Educational Campuses | ||

| Industrial and Warehousing | ||

| BFSI | ||

| Others | ||

| By Organization Size | SMEs | |

| Large Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| UAE | ||

| Turkey | ||

| South Africa | ||

| Kenya | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the Commercial security market?

The sector is valued at USD 244.38 billion in 2026 and is forecast to rise to USD 413.96 billion by 2031.

Which security technology is expanding fastest?

Mobile-credential access control is growing at an 11.36% CAGR, outpacing other security types due to flexible work models and IT-security convergence.

Which is the fastest growing region in Commercial Security Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Why are services gaining momentum versus hardware?

Services post an 11.75% CAGR because cloud storage, managed maintenance and analytics subscriptions provide predictable OPEX and solve skills gaps for users.

Which region offers the highest growth potential through 2031?

Asia Pacific leads with an 11.06% CAGR, supported by smart-city projects and a vast SME base that favours cloud-based deployments.

How are regulations affecting cross-border video surveillance?

Data-residency laws in the EU and GCC force enterprises to store footage locally or adopt hybrid clouds, raising compliance costs but also stimulating regional data-centre investment.

What strategic moves define competitive dynamics?

Large vendors are acquiring software-rich portfolios, shifting toward recurring-revenue cloud models, and partnering with cyber-consultancies to deliver integrated physical-and-IT protection.

Page last updated on: