Identity As A Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

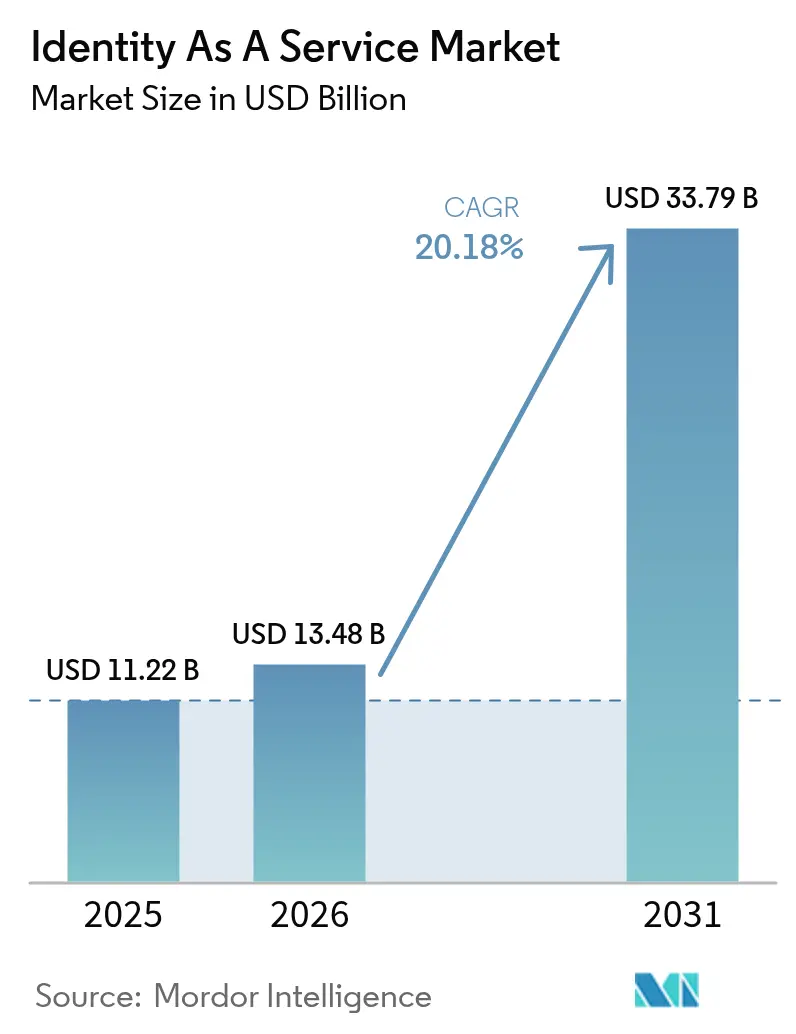

| Market Size (2026) | USD 13.48 Billion |

| Market Size (2031) | USD 33.79 Billion |

| Growth Rate (2026 - 2031) | 20.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Identity As A Service Market Analysis by Mordor Intelligence

The Identity-as-a-Service market size is expected to grow from USD 11.22 billion in 2025 to USD 13.48 billion in 2026 and is forecast to reach USD 33.79 billion by 2031 at 20.18% CAGR over 2026-2031. Heightened board-level focus on zero-trust architecture, rapid cloud migration, and the accelerating volume of machine identities underpin demand for subscription-based identity security platforms. Vendors that bundle passwordless authentication, machine-identity governance, and real-time risk scoring into a single control plane are capturing wallet share as enterprises consolidate point solutions. Government-backed national digital identity programs in Asia-Pacific and prescriptive zero-trust mandates in North America are further amplifying platform adoption, while horizontal acquisitions by hyperscalers and security-first software firms are redefining competitive boundaries.

Key Report Takeaways

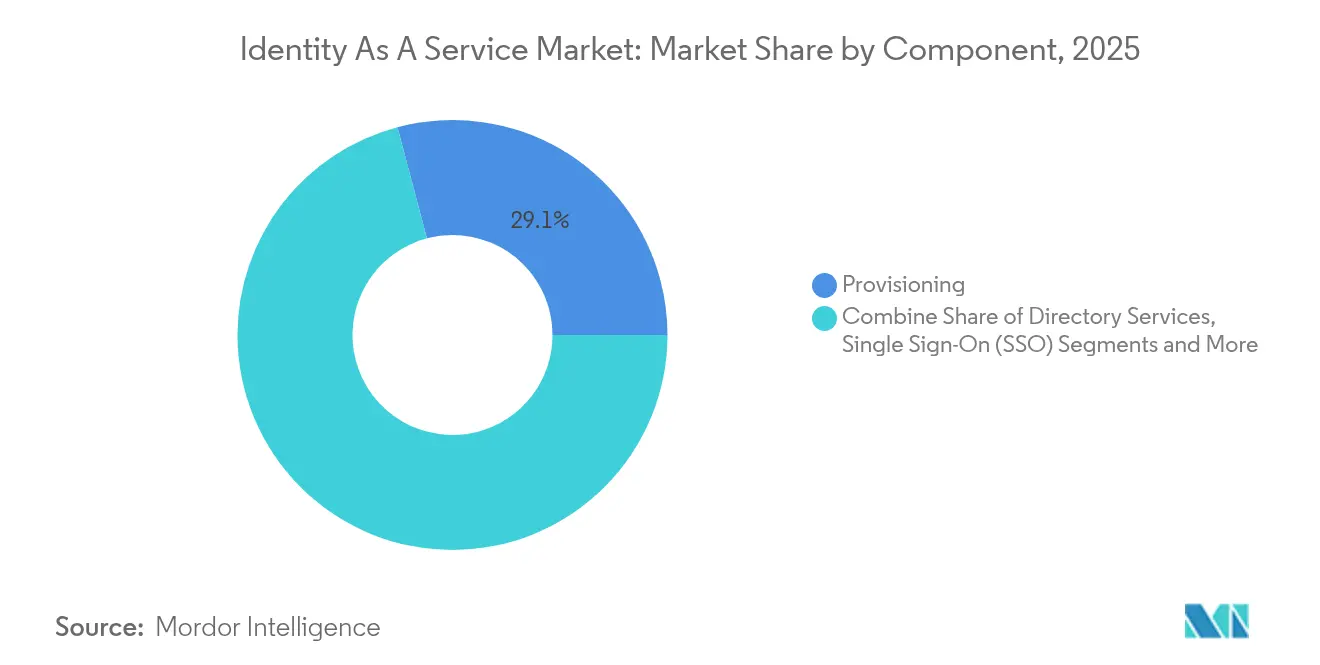

- By component, Provisioning held 29.12% of Identity-as-a-Service market share in 2025, whereas Multi-factor/Advanced Authentication is projected to advance at a 21.96% CAGR to 2031.

- By authentication type, single-factor methods retained 45.62% revenue share Identity-as-a-Service market size in 2025; Passwordless mechanisms, is set to outgrow at a 21.34% CAGR to 2031.

- By deployment mode, public cloud captured 62.55% share of the Identity-as-a-Service market size in 2025; hybrid cloud is forecast to expand at 21.78% CAGR through 2031.

- By user type, workforce identity comprised 56.42% share of the Identity-as-a-Service market size in 2025, while customer identity solutions are growing at 20.64% CAGR through 2031.

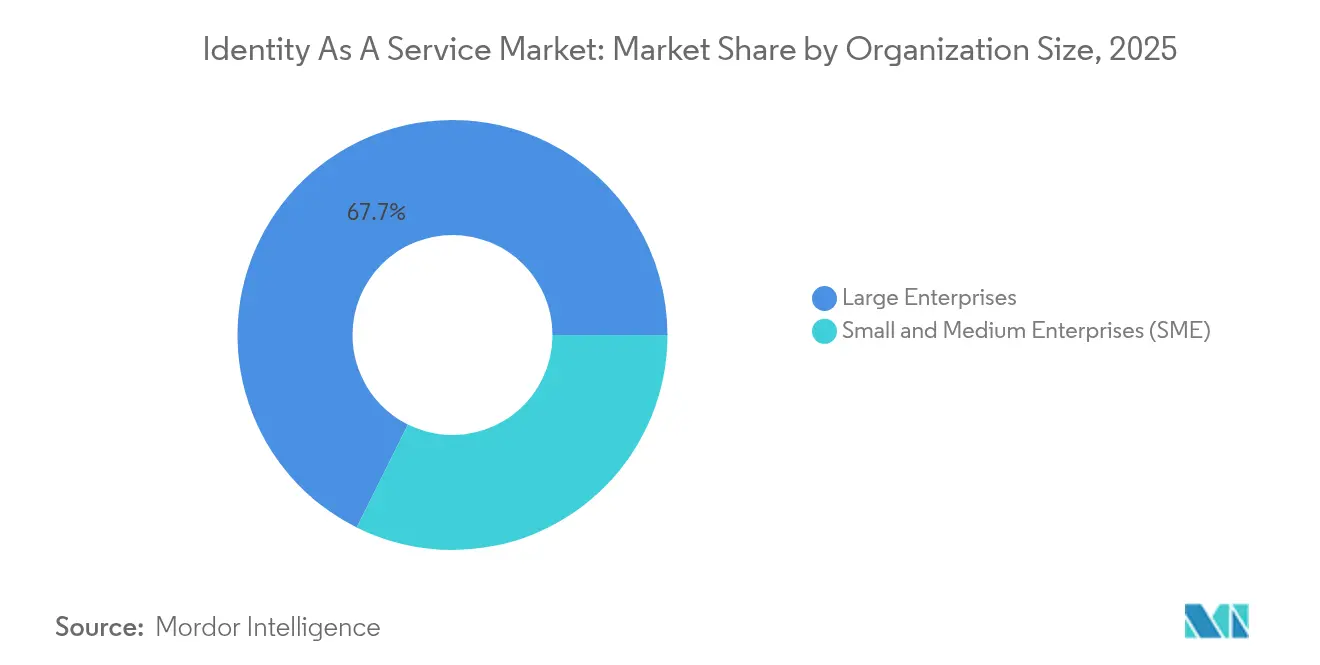

- By organization size, large enterprises accounted for 67.65% of the Identity-as-a-Service market size in 2025, while mall and mid-sized enterprises is poised for a 20.05% CAGR through 2031..

- By end-user vertical, the public sector accounted for 25.74% of the Identity-as-a-Service market size in 2025, while BFSI leads growth at a 20.26% CAGR to 2031.

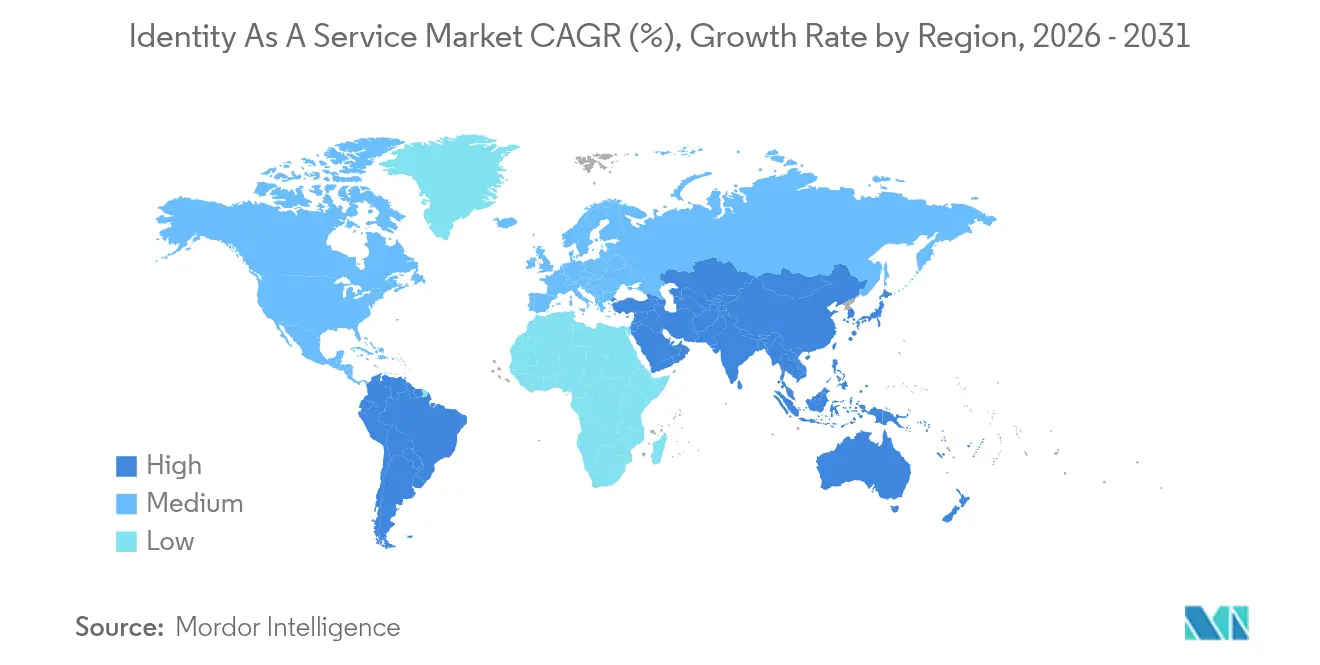

- By geography, North America dominated with 38.35% revenue share of the Identity-as-a-Service market in 2025; Asia-Pacific is poised for a 23.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Identity As A Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-native Zero-Trust Adoption in U.S.-Centric Highly Regulated Sectors | +4.2% | North America, EU financial services | Medium term (2-4 years) |

| Proliferation of API-based Micro-Services Accelerating CI/CD IDaaS Demand in Europe | +3.8% | Europe, North America tech hubs | Short term (≤ 2 years) |

| Asia's "Digital Public Goods" (eKYC, Aadhaar, Singpass) Triggering Country-wide Workforce IDaaS Roll-outs | +5.1% | Asia-Pacific, selective MEA adoption | Long term (≥ 4 years) |

| Passwordless FIDO2 Pilots Converting to Enterprise-wide Licences in Financial Services | +3.9% | Global, concentrated in BFSI | Medium term (2-4 years) |

| Vendor-bundled IAM Analytics Using Generative-AI for Real-time Risk Scoring | +2.7% | Global, early adoption in North America | Short term (≤ 2 years) |

| MandA-Driven Horizontal Suite-Building by Hyperscalers (Azure, AWS) Boosting Integrated IDaaS Uptake | +4.3% | Global, strongest in cloud-mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-native zero-trust adoption in regulated U.S. sectors

Executive Order 14028 requires U.S. federal agencies to implement zero-trust architectures, making identity verification the first line of defense. NIST’s draft practice guide codifies an interoperable blueprint that cuts deployment risk for private and public stakeholders.[1]National Institute of Standards and Technology, “Implementing a Zero Trust Architecture,” csrc.nist.govHospitals, insurers, and capital-markets firms are leveraging the guidance to shift from perimeter controls to continuous verification, turning Identity-as-a-Service market subscriptions into essential operating expenditure.

Proliferation of API-based micro-services requiring CI/CD identity controls

European adoption of micro-services has outpaced legacy IAM capabilities. The EU Digital Identity Regulation obliges Member States to issue cross-border digital wallets by 2026, creating uniform APIs for authentication. [2]European Commission, “European Digital Identity Regulation,” digital-strategy.ec.europa.euDevOps teams now require platforms that auto-provision tokens during each CI/CD run, positioning Identity-as-a-Service market providers that specialize in machine-identity governance for outsized growth.

Asia-Pacific digital public-goods programs (eKYC, Aadhaar, Singpass)

Regional governments are lowering verification costs by offering nationwide identity rails. Indonesia’s Digital Population Identity program and Singapore’s SingPass enable employers to bind workforce credentials to state-verified identities, widening the addressable Identity-as-a-Service market for multi-national corporations operating across ASEAN.

Enterprise-wide passwordless FIDO2 roll-outs in financial services

Banks moving from pilots to full production have documented 86% reductions in credential-stuffing incidents after deploying passkeys. Capital One has removed passwords from more than 1,000 internal applications, elevating passwordless authentication from innovation project to mainstream control.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Mainframe Entanglement Slowing IDaaS Migration in Tier-1 Banks | -2.8% | Global, concentrated in established financial markets | Long term (≥ 4 years) |

| Fragmented Data-Residency Statutes in the Middle East Inflating Compliance Costs | -1.9% | Middle East, selective impact on global providers | Medium term (2-4 years) |

| High Latency Concerns Among IIoT Users for Cloud-hosted Authentication | -1.4% | Global industrial sectors, edge computing environments | Short term (≤ 2 years) |

| Vendor-lock-in Fears around Proprietary SSO Protocol Extensions | -1.6% | Global, strongest in multi-vendor enterprise environments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy mainframe entanglement in Tier-1 banks

Tier-1 financial institutions face significant technical debt from mainframe systems that resist integration with modern IDaaS platforms, creating migration timelines that extend beyond typical enterprise deployment cycles. ING’s migration of 1.5 million COBOL lines illustrates the complexity of decoupling IAM logic trapped inside core banking systems softwaremining.com. Hybrid coexistence with mainframes prolongs testing cycles, tempering Identity-as-a-Service market acceleration among global banks.

Fragmented Middle-East data-residency statutes

Divergent localization mandates in the UAE and Saudi Arabia force providers to build redundant data zones, shrinking economies of scale and raising compliance cost per customer. The fragmented regulatory environment may slow market penetration until regional harmonization efforts mature or IDaaS providers develop specialized compliance capabilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Provisioning Dominates Amid Authentication Innovation

The provisioning segment generated 29.12% of Identity-as-a-Service market revenue in 2025, underlining the universal need for automated joiner-mover-leaver workflows across hybrid cloud estates. Directory services and single sign-on remain table stakes, yet adoption now concentrates on suites that orchestrate lifecycle controls for both human and machine principals.

Multi-factor and passwordless authentication services are forecast to grow 21.96% annually as regulatory guidance rewards phishing-resistant mechanisms. Vendors such as CyberArk are integrating biometric passkey orchestration following the USD 1.66 billion Venafi acquisition, signaling that unified suites will outpace isolated toolsets investors.

By Authentication Type: Passwordless Revolution Accelerates

Single-factor methods retained 45.62% revenue share in 2025, largely due to legacy workloads that cannot yet support modern protocols. Passwordless mechanisms, however, are set to outgrow the Identity-as-a-Service market at a 21.34% CAGR as FIDO2 certification becomes table stakes for regulated industries. The Federal Reserve Bank of Boston attributes USD 35 billion in 2024 fraud losses to synthetic identities, a statistic that spurs enterprises to prioritize continuous biometric and behavioral authentication.

Multi-factor tools serve as transitional safeguards, but board-level risk committees now favor passkeys that eliminate shared secrets entirely. This pivot reinforces a structural shift from occasional to continuous identity assurance.

By Deployment Mode: Hybrid Cloud Gains Momentum

Public cloud deployments commanded 62.55% of Identity-as-a-Service market size in 2025. Scalability and rapid time-to-value favor SaaS delivery, yet data sovereignty and latency-sensitive workloads fuel the hybrid cloud sub-segment, which is projected to climb 21.78% annually. Microsoft’s federated identity credentials for Entra illustrate industry intent to harmonize on-premises policies with cloud guardrails.

Edge computing in industrial settings requires authentication decisions within milliseconds, prompting enterprises to anchor policy engines in cloud while caching risk scores at the edge. Providers that deliver policy consistency across deployment modes are set to gain share.

By User Type: Consumer Identity Accelerates

Workforce identity comprised 56.42% of 2025 revenue, but customer identity solutions are growing at 20.64% CAGR. The surge reflects digital-commerce priorities frictionless onboarding and consent management where one failed login translates directly into lost revenue. Okta’s Customer Identity Cloud shows how providers are modularizing consumer workflows while reusing the same policy stack that protects employees.

Consumer identity platforms must handle significantly higher transaction volumes and more diverse authentication methods compared to workforce solutions, requiring specialized infrastructure and user experience design. The convergence of workforce and consumer identity requirements creates opportunities for unified platforms that can serve both use cases while maintaining appropriate security and compliance controls.

By Organization Size: SME Adoption Quickens

Large enterprises generated 67.65% of 2025 billings, anchored by complex hybrid estates and regulatory scrutiny. Small and mid-sized enterprises now expand 20.05% per year as subscription pricing removes the barrier of large-scale capital approvals. SailPoint’s USD 11.5 billion IPO valuation underscores the investment community’s conviction that midsized customers will migrate from rudimentary SSO to full lifecycle governance.

Turnkey, template-driven deployments resonate with resource-constrained IT teams, positioning cloud-native providers to capture lifetime value as SMEs scale operations. SME organizations increasingly require sophisticated identity management capabilities to support remote work, cloud application adoption, and regulatory compliance, creating sustained demand for simplified IDaaS solutions.

By End-User Vertical: BFSI Leads Growth Trajectory

The public sector represented 25.74% of 2025 consumption, propelled by sovereign digital-government initiatives. BFSI’s 20.26% CAGR outpaces every other industry as regulators direct financial institutions to adopt phishing-resistant credentials. 1Kosmos’ USD 194.5 million Blanket Purchase Agreement for the U.S. Login.gov program exemplifies how federal procurement influences private-sector buying criteria.

Healthcare, manufacturing, and energy customers follow, motivated by zero-trust mandates that harden industrial control systems and safeguard patient data. The vertical segmentation reflects industry-specific requirements for identity management, with regulated sectors driving premium solution adoption while commercial sectors focus on cost-effective scalability.

Geography Analysis

North America accounted for 38.35% of Identity-as-a-Service market revenue in 2025. Federal zero-trust edicts and early passwordless roll-outs among tier-one banks sustain spending momentum. Canada’s cloud-first program and Mexico’s cross-border trade platforms add incremental demand, all underpinned by mature hyperscaler infrastructure.

Asia-Pacific is the fastest-growing region at 23.02% CAGR. National digital ID frameworks, coupled with accelerated public-cloud adoption in Indonesia, India, and Vietnam, multiply workforce and citizen-access use cases. Enterprises leverage government-issued credentials to bind employees and contractors, compressing onboarding time and reducing KYC costs.

Europe exhibits steady expansion, catalyzed by the EU Digital Identity Regulation that obliges members to deploy interoperable wallets by 2026. Germany’s EUDI pilot and France’s health-data localization rules drive joint procurement models between ministries and enterprises. Providers able to guarantee regional data residency while integrating cross-border workflows will consolidate gains.

Competitive Landscape

The market is moderately fragmented. Okta posted USD 2.61 billion in fiscal-2025 revenue and leverages a 19,450-customer flywheel to cross-sell risk-based access controls investor.okta.com. CyberArk surpassed USD 1 billion in 2024 revenue following its Venafi purchase, positioning the firm as the only top-tier vendor with symmetrical control of human and machine identities investors.[4]SEC EDGAR, “CyberArk–Venafi Acquisition Filing,”

Private-equity roll-ups alter competitive dynamics: Thoma Bravo combined Ping Identity and ForgeRock into a portfolio nearing USD 800 million ARR, demonstrating the strategic premium placed on scale and wallet-share economics. SailPoint’s IPO brings fresh capital for horizontal expansion into adjacent data-access governance, while Saviynt’s 35% ARR growth highlights the appeal of AI-driven least-privilege analytics saviynt.com.

Strategically, leading vendors now differentiate through: 1) machine-identity lifecycle management baked into core platforms; 2) platformized generative-AI risk scoring; and 3) open standards for passkey orchestration to avoid locking customers into proprietary protocols.

Identity As A Service Industry Leaders

Ping Identity Corporation

OneLogin Inc.

IDaptive LLC

Microsoft Corporation

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: CyberArk launched an identity-security solution that secures AI agents at scale, aiming to monetize emerging machine-identity attack surfaces.

- April 2025: SailPoint released Machine Identity Discovery within its Identity Security Cloud, broadening addressable spend into certificate governance

- March 2025: IBM shifted Identity & Access Management revenue into its Automation segment, aligning go-to-market incentives around platform synergies.

- February 2025: SailPoint priced its 60-million-share IPO at USD 23 per share, valuing the firm at USD 11.5 billion and providing capital to fund inorganic growth.

Global Identity As A Service Market Report Scope

- Identity-as-a-Service (IDaaS) refers to a wide variety of cloud-based services for identity and access management (IAM), It is a technological function that maintains user identity and helps the organizations ensure that users are whom they claim to be and evidently restrict the cybercriminals and unauthorized users from accessing critical data as they rely on active and lightweight directory access protocol for IAM services.

- The reports cover the emerging trends in Identity as a Service Market segmented by component, deployment, organization size, end-user verticals across different regions studied.

| Provisioning |

| Directory Services |

| Single Sign-On (SSO) |

| Password Management |

| Advanced / Multi-factor Authentication |

| Access Governance and Compliance |

| Single-Factor (Password-based) |

| Multi-Factor (Token, OTP, Mobile Push) |

| Passwordless (Biometric, FIDO2) |

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Workforce Identity |

| Customer / Consumer Identity (CIAM) |

| Large Enterprise |

| Small and Medium Enterprise (SME) |

| BFSI |

| Telecom and IT |

| Public Sector and Government |

| Healthcare and Life-Sciences |

| Energy and Utilities |

| Manufacturing |

| Retail and E-commerce |

| Education |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Nordic Countries | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia Pacific | |

| Middle East and Africa | Middle East |

| Africa |

| By Component | Provisioning | |

| Directory Services | ||

| Single Sign-On (SSO) | ||

| Password Management | ||

| Advanced / Multi-factor Authentication | ||

| Access Governance and Compliance | ||

| By Authentication Type | Single-Factor (Password-based) | |

| Multi-Factor (Token, OTP, Mobile Push) | ||

| Passwordless (Biometric, FIDO2) | ||

| By Deployment Mode | Public Cloud | |

| Private Cloud | ||

| Hybrid Cloud | ||

| By User Type | Workforce Identity | |

| Customer / Consumer Identity (CIAM) | ||

| By Organization Size | Large Enterprise | |

| Small and Medium Enterprise (SME) | ||

| By End-User Vertical | BFSI | |

| Telecom and IT | ||

| Public Sector and Government | ||

| Healthcare and Life-Sciences | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Retail and E-commerce | ||

| Education | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordic Countries | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | |

| Africa | ||

Key Questions Answered in the Report

What is the current size of the Identity-as-a-Service market?

The market is valued at USD 13.48 billion in 2026 and is forecast to reach USD 33.79 billion by 2031 at a 20.18% CAGR over 2026-2031.

Which component generates the highest revenue?

Provisioning contributes 29.12% of 2025 revenue due to its critical role in automating user lifecycle management.

Which is the fastest growing region in Identity as a Service Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Why is passwordless authentication growing so quickly?

Regulatory mandates and the proven 86% reduction in credential-stuffing incidents make FIDO2 passkeys the preferred replacement for passwords.

Which region is expanding the fastest?

Asia-Pacific leads with a projected 23.02% CAGR through 2031, driven by national digital-identity programs and cloud adoption.

How fragmented is the vendor landscape?

A market concentration score of 6 indicates that while the top providers hold a majority share, room remains for niche specialists, particularly in machine-identity governance.

What deployment mode will dominate by 2031?

Hybrid cloud is forecast to grow fastest at 21.78% CAGR as firms balance data-sovereignty obligations with public-cloud scalability. Continue

Page last updated on: