Middle East Manned Security Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

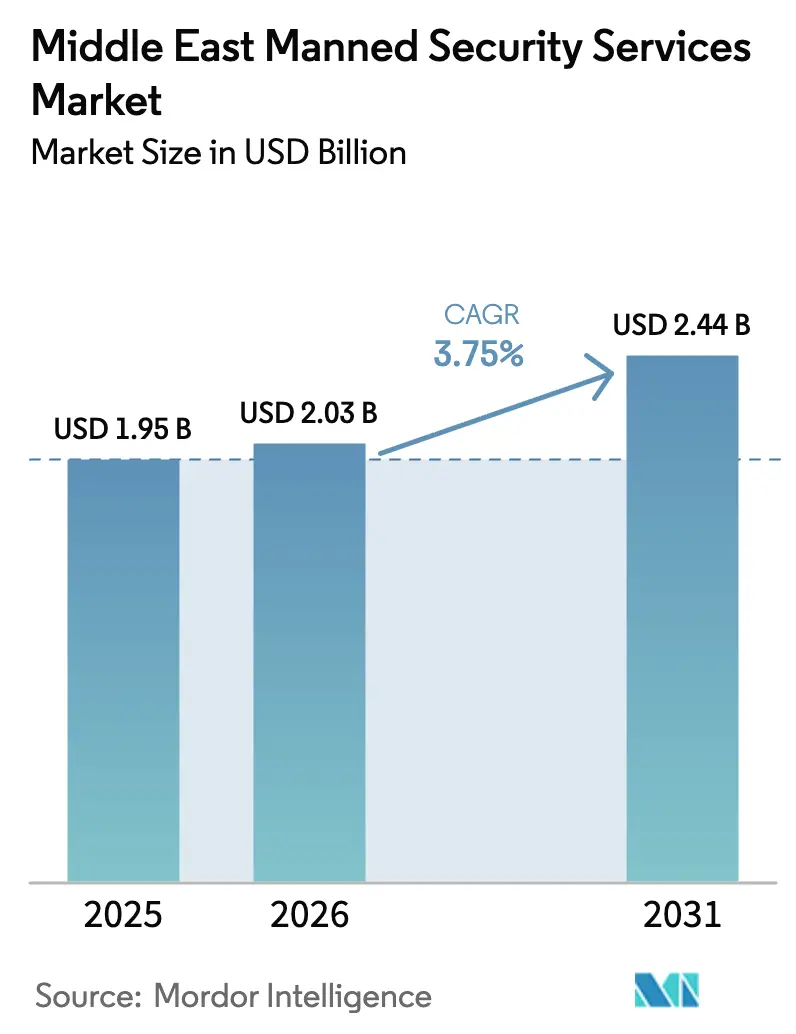

| Base Year Market Size (2025) | USD 1.95 Billion |

| Market Size (2026) | USD 2.03 Billion |

| Market Size (2031) | USD 2.44 Billion |

| Growth Rate (2026 - 2031) | 3.75% CAGR |

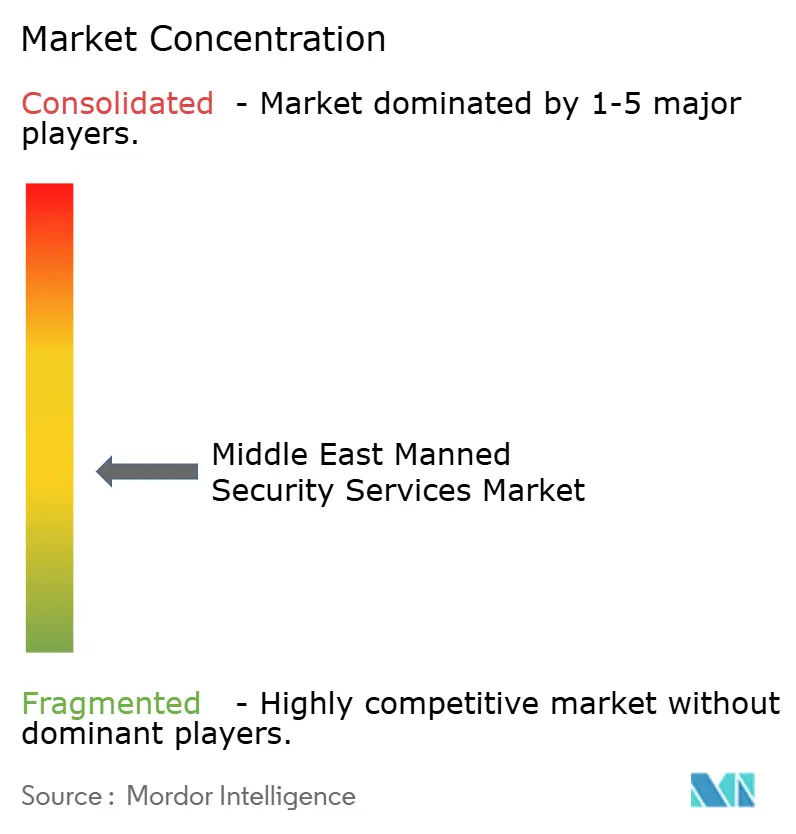

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Manned Security Services Market Analysis by Mordor Intelligence

The Middle East manned security services market size is projected to expand from USD 1.95 billion in 2025 and USD 2.03 billion in 2026 to USD 2.44 billion by 2031, registering a CAGR of 3.75% between 2026 to 2031. Ongoing diversification of Gulf economies toward tourism, logistics, and digital infrastructure is reshaping demand, moving the sector beyond its historical reliance on retail malls and office towers. Clients are shifting from pure headcount models to hybrid solutions that combine fewer on-site guards with AI-enabled monitoring, drone patrols, and K9 teams. Wage pressures, stricter licensing rules, and higher insurance premiums are nudging providers to favour long-term contracts that embed escalation clauses and to prioritize specialized roles that command price premiums. Competitive intensity is moderate, yet consolidation is gaining speed as larger operators acquire local firms to secure regional licenses and training capacity.

Key Report Takeaways

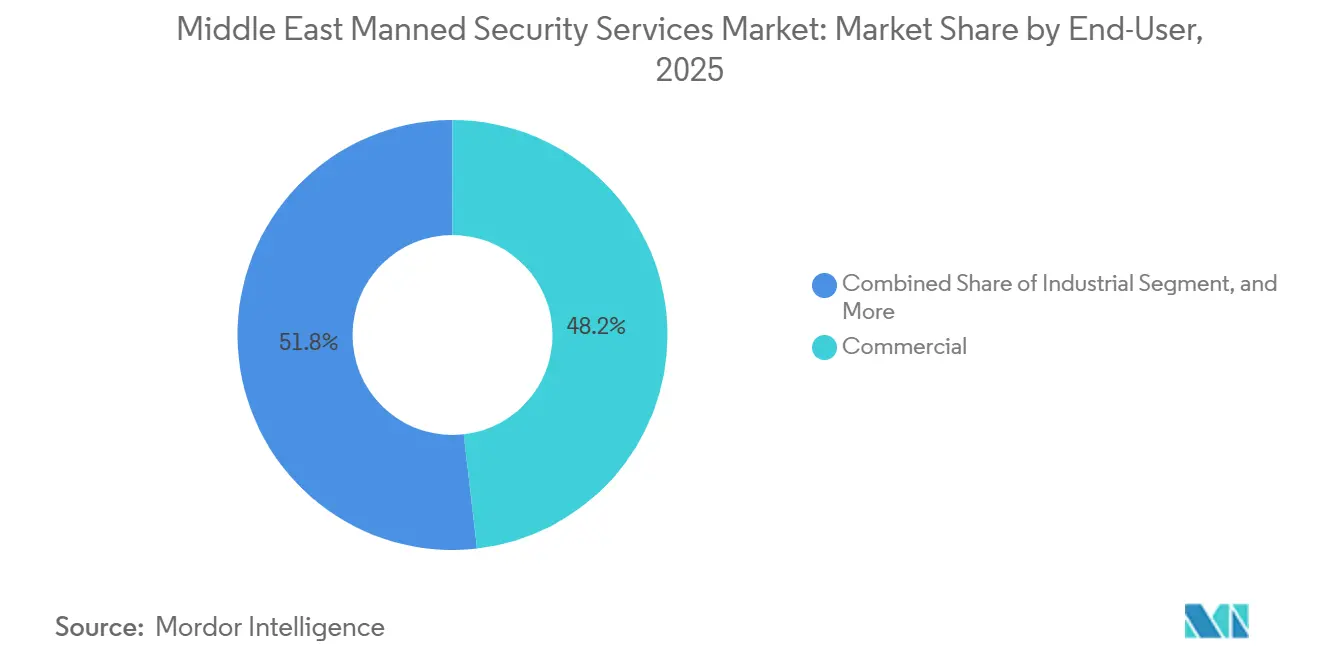

- By end-user, commercial properties led with 48.19% revenue share in 2025, while industrial facilities are advancing at a 4.29% CAGR through 2031.

- By service type, static guarding captured 42.53% of 2025 revenue; K9 and specialized protection record the fastest growth at 4.55% CAGR to 2031.

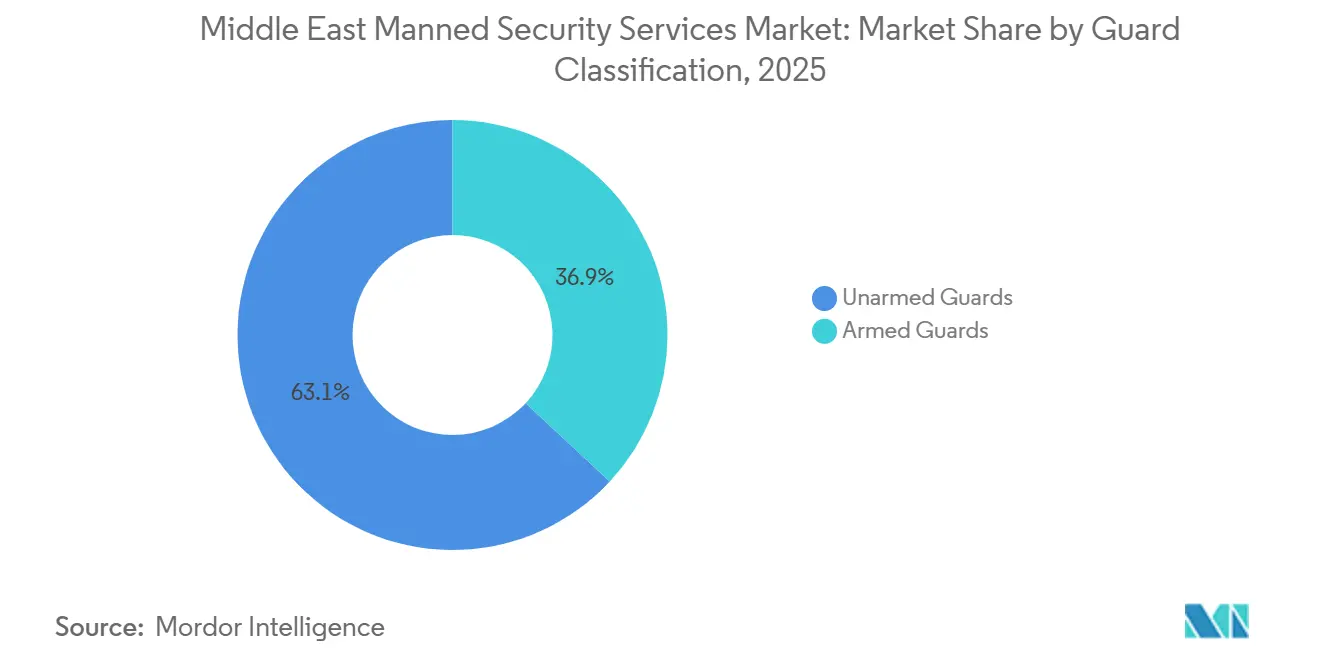

- By guard classification, unarmed personnel held 63.07% of 2025 bookings, but armed roles are rising at 4.34% CAGR through 2031.

- By contract duration, agreements longer than 12 months accounted for 72.73% of 2025 value, whereas short-term and event assignments are growing at 4.61% CAGR.

- By geography, the United Arab Emirates contributed 27.92% of 2025 sales; Saudi Arabia posts the highest CAGR at 4.58% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Manned Security Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mega-event proliferation and tourism expansion | +1.80% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Infrastructure and industrial project acceleration | +1.20% | Saudi Arabia, UAE, Oman | Long term (≥ 4 years) |

| Regulatory compliance mandates and licensing requirements | +0.50% | GCC-wide | Short term (≤ 2 years) |

| Vision 2030 diversification and private sector growth | +0.90% | Saudi Arabia, Bahrain, Kuwait | Long term (≥ 4 years) |

| Hybrid guard-technology adoption for cost optimization | +0.60% | UAE, Saudi Arabia | Medium term (2-4 years) |

| Rising female workforce participation and gender-specific security demand | +0.30% | Saudi Arabia, UAE | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Mega-Event Proliferation and Tourism Expansion

Saudi Arabia welcomed 109 million tourists in 2024 after easing visa rules, driving acute demand spikes such as 3,200 security jobs for the Saudi Arabian Grand Prix and 1,800 guards per Riyadh Season venue.[1]Saudi Tourism Authority, “Tourism Statistics 2024,” visitsaudi.com The UAE’s Expo 2020 legacy has converted pavilions into permanent conference sites that require year-round guarding, supported by 17.15 million overnight visitors to Dubai in 2024. Qatar continues to staff more than 5,000 guards across World Cup stadiums repurposed for concerts and sport. Event contracts carry 15-20% price premiums but expose providers to margin risk when bids are fixed months ahead. Luxury desert camps in Oman’s Wahiba Sands and Saudi Arabia’s Empty Quarter also require armed, wilderness-trained guards, adding a niche revenue stream.

Infrastructure And Industrial Project Acceleration

The Public Investment Fund’s USD 500 billion commitment to NEOM, Qiddiya, and Red Sea projects demands 12,000-15,000 guards for site access control and asset protection.[2]Saudi Public Investment Fund, “NEOM, Qiddiya, and Red Sea Projects,” pif.gov.sa In the UAE, Khalifa Industrial Zone expanded by 2.3 million m² in 2024, obliging 24/7-armed patrols under Federal Law No. 37 of 2006. Oman’s Duqm zone added 1,800 hectares of logistics parks subject to ISO 28000 security certification, generating new contracts for firms with documented guard-to-gate ratios. Industrial clients bundle manned security with AI video analytics, exemplified by Saudi Aramco’s Ras Tanura refinery, where breach response time fell from eight minutes to 90 seconds. Specialized security coordinators who liaise with contractors and authorities now earn USD 4,000-6,000 monthly, triple the wages of basic guards.

Regulatory Compliance Mandates and Licensing Requirements

Dubai’s Security Industry Regulatory Agency introduced biometric registration in 2024, disqualifying 4% of guards for visa or criminal violations.[3]SIRA, “Licensing and Training Requirements,” sira.ae Saudi Arabia lengthened mandatory training to 60 hours in 2025, adding modules on cybersecurity and first aid, which increased per-guard onboarding costs by USD 80-100. The UAE obliges a 1:50 supervisor-to-guard ratio and quarterly audits of equipment, favouring operators with robust compliance teams. Qatar requires annual psychological checks and weapon recertification for armed guards, costing QAR 1,500 (USD 412) per employee. New entrants in Dubai must post an AED 500,000 (USD 136,000) bond and show three years of operating history, effectively blocking startups.

Vision 2030 Diversification and Private Sector Growth

Saudi Vision 2030 aims to lift private-sector GDP share to 10% by 2030, a target adding thousands of security roles in entertainment, logistics, and hospitality. The General Entertainment Authority licensed 5,200 events in 2024, each requiring Interior-approved guard plans using ratios of 1:150 for concerts and 1:100 for sports. Mall space in the kingdom grew by 1.2 million m² in 2024-2025, prompting new posts at entrances and cash rooms. UAE non-oil GDP expanded 6.2% in 2024, with Jebel Ali and Dubai South logistics hubs employing 8,000 guards for cargo screening and driver verification. Rising female labour force participation in Saudi Arabia, now 35.6%, lifts demand for female guards at women-only venues, a segment expanding 7-9% annually.

Labor Cost Inflation and Wage Pressures

The UAE raised minimum guard wages from AED 1,200 (USD 327) to AED 1,500 (USD 408) in 2024, eroding margins on labour-intensive contracts. Saudi Arabia’s Nitaqat rule requires 15% Saudi nationals in private security by 2026, lifting payrolls to USD 2,000-2,500 for local hires versus USD 800-1,200 for expatriates. Qatar’s abolition of the kafala system in 2024 raised turnover to 18-22% and forced 10-12% wage increases. Visa caps in the UAE created a 3,000-4,000-guard shortfall in 2025, pushing overtime costs upward. Insurance premiums for armed roles climbed 15-18% after two false-alarm shootings in Saudi Arabia, squeezing EBITDA margins of UAE mid-tier firms to 8-10% in 2024 from 12-14% two years earlier.

Technology Substitution and Automation Threats

AI video analytics cut static-guard requirements by 12-15% at Dubai commercial towers in 2024-2025. Drone patrols at Saudi solar farms now cover 50-70 km per shift, reducing guard headcount by 20-25%. A single Abu Dhabi command hub oversees 120 sites, replacing 180 on-site guards with 40 remote operators and 60 rapid-response staff. Biometric systems at UAE government buildings removed 30% of lobby-guard posts in 2024. Hybrid tenders, such as the 2025 contract for King Salman Park that allocates 60% to electronics and 40% to patrols, illustrate the pivot away from headcount. Yet K9 teams remain irreplaceable, delivering higher detection accuracy than sensors, with one dog-handler pair costing USD 80,000-100,000 annually. Minimum guard-to-perimeter ratios for critical infrastructure in the UAE curb automation’s reach and sustain 4,000-5,000 jobs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Industrial Momentum Builds on Diversification

Industrial clients accounted for 4.29% CAGR growth between 2026-2031, outpacing the stable commercial base that held 48.19% of the Middle East manned security services market share in 2025. Petrochemical expansions at Ras Tanura and aluminium smelters in Khalifa Industrial Zone Abu Dhabi are contracting armed perimeter teams under Federal Law No. 37 of 2006. Residential sub-segments trimmed lobby posts by 30% after adopting AI analytics yet offset cuts with mobile patrols that preserve visibility.

Government ministries and universities continue to favour unarmed roles but are adding female guards for women-only spaces, creating 1,200 positions in 2024. Healthcare facilities in the UAE hired 800 extra guards in 2024-2025 to manage visitor flows and drug-theft risk. Retail chains renegotiate annually, pressing fees downward, whereas industrial firms sign 3-5-year deals with inflation clauses that bolster the Middle East manned security services market size resilience.

By Service Type: Specialized Roles Capture Premiums

Static guarding retained 42.53% revenue in 2025, yet K9 and specialized protection services are expanding at 4.55% CAGR through 2031. Dubai International Airport added 60 K9 teams in 2024, each pairing priced at USD 80,000-100,000. Mobile patrols are losing share to remote monitoring, as centralized hubs cut redundant posts. Executive protection is booming: 1,200 close-protection officers were hired by Saudi corporate leaders at USD 6,000-10,000 monthly.

Event security surged during Riyadh Season 2024-2025, absorbing 1,800 guards per venue. Cash-in-transit contracts now bundle two-guard escorts for ATM replenishment after robbery attempts spiked in the UAE. Annual veterinary checks for K9 units add AED 15,000-20,000 (USD 4,100-5,450) to compliance costs but reinforce entry barriers.

By Guard Classification: Armed Demand Gains Ground

Unarmed personnel represented 63.07% of 2025 bookings, yet armed roles are projected to post a 4.34% CAGR by 2031. The Saudi Interior Ministry issued 4,200 new permits in 2024, signalling a structural pivot toward lethal deterrence at petrochemical plants and logistics hubs. In the UAE, only critical infrastructure, government, and hazardous-materials sites may deploy armed guards, sustaining 5,000-6,000 posts under Federal Law No. 37 of 2006.

Wage premiums of 35-40% over unarmed roles reflect weapons training and psychological screening. Insurance costs rose 15-18% in 2024-2025, squeezing smaller firms. Hybrid contracts pair unarmed static guards with armed rapid-response teams, optimizing deterrence while controlling premiums.

By Contract Duration: Event Surge Alters Mix

Long-term agreements exceeding 12 months captured 72.73% of bookings in 2025, anchoring predictable revenue for providers. Inflation-linked clauses shield margins from wage escalation, unlike event contracts that are fixed price. The 2024 Saudi Arabian Grand Prix required 3,200 guards over four days at 15-20% rate premiums.

Government and industrial buyers prefer 3-5-year terms for continuity, while retail and hospitality clients renew annually to leverage competitive bids. Event deployments face 25-30% no-show risk, prompting overstaffing buffers that erode margins. UAE labour law mandates equal minimum wages for event and permanent staff, limiting the flexibility of short-term hiring.

Geography Analysis

The United Arab Emirates contributed 27.92% of 2025 revenue, yet Saudi Arabia shows the fastest expansion at a 4.58% CAGR through 2031, propelled by giga-projects that elevate the Middle East manned security services market size for site and venue protection. The UAE market is mature and increasingly tech-driven, with commercial towers cutting static headcount by 12-15% in 2024-2025 while investing in remote monitoring and K9 teams. Qatar sustains over 5,000 posts across stadiums and the Doha Metro, though growth is moderating as construction slows.

Saudi Arabia’s Public Investment Fund pipeline alone necessitates 12,000-15,000 guards for NEOM, Qiddiya, and Red Sea resorts, underpinning robust demand for armed and specialized roles. The General Entertainment Authority’s 5,200 licensed events in 2024 absorbed 8,000-10,000 guards, underscoring the kingdom’s shift toward experiential sectors. Regulatory divergence complicates regional operations: Dubai’s SIRA enforces biometric registration and 48-hour basic training, Saudi Arabia mandates 60 hours, and Qatar imposes annual psychological assessments for armed staff.

Oman’s Duqm industrial corridor added 1,800 hectares of logistics parks in 2025, creating 600-800 new guard posts under ISO 28000 certification. Kuwait and Bahrain together account for 12-15% of regional turnover, constrained by slower diversification and tighter fiscal policy but still adopting hybrid guard-technology models. Region-wide, providers offering compliance expertise and multilingual staff gain an edge as clients expand across borders with varying rules.

Competitive Landscape

The Middle East manned security services market remains moderately concentrated: multinational giants G4S, Securitas, and Transguard Group hold roughly 38% combined share, while hundreds of local firms cover niche verticals. Transguard Group employs 17,000 guards and packages security with cleaning and technical services, locking in multi-year government and commercial contracts. G4S leverages global standards and centralized command centers yet faces price pressure in retail and residential segments where local companies undercut wages by 10-15%.

K9 detection, executive protection, and event security command 25-40% premiums, but fewer than 20 regional providers own training and insurance capacity to compete. Early adopters of AI analytics and drone patrols cut guard numbers by 12-20%, a capability that smaller rivals struggle to finance due to USD 200,000-500,000 upfront hardware and software costs. Mobile-app disruptors now match guards to events within hours, challenging incumbents that need 48-72 hours to mobilize.

Saudi localization quotas reward firms meeting 15% Saudi staffing, forcing multinationals to pay 60-80% wage premiums to attract local citizens. Dubai’s SIRA demands AED 500,000 bonds and three years of operating history, impeding new entrants and encouraging consolidation. Partnerships with surveillance vendors allow operators to pitch hybrid guard-technology bundles that trim client costs by 15-25% while preserving margins.

Middle East Manned Security Services Industry Leaders

Hemaya Security Services Co.

Transguard Group LLC

G4S plc

Spark Security Services LLC

Vanguards Safety and Security Services Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Teledyne FLIR Defense secured a USD 7.8 million deal with METCO to supply long-range vehicle surveillance systems to a Saudi military customer.

- March 2025: Tawazun Council placed a USD 354 million order for offshore patrol vessels from Al-Seer Marine and Damen, bolstering maritime security capacity.

- March 2025: Canadian Medical Center Co. landed a SAR 22.8 million contract to staff National Guard hospitals, underscoring ongoing investment in critical-infrastructure.

- February 2025: UAE announced USD 6.45 billion in defense awards at IDEX, creating downstream demand for integrated guarding services.

Middle East Manned Security Services Market Report Scope

The Middle East Manned Security Services Market Report is Segmented by End-User (Commercial, Industrial, Residential, Government and Institutional), Service Type (Static Guarding, Mobile Patrols, K9 and Specialised Protection, Executive Protection), Guard Classification (Armed Guards, Unarmed Guards), Contract Duration (Long-Term exceeding 12 Months, Short-Term and Event-Based), and Geography (United Arab Emirates, Saudi Arabia, Qatar, Oman, Kuwait, Bahrain, Rest of Middle East). The Market Forecasts are Provided in Terms of Value (USD).

| Commercial |

| Industrial |

| Government and Institutional |

| Residential |

| Static Guarding |

| Mobile Patrol |

| Event / Crowd-Control Security |

| Cash-in-Transit (CIT) and Valuables Logistics |

| K9 and Specialised Protection |

| Unarmed Guards |

| Armed Guards |

| Long-Term (More than 12 Months) |

| Short-Term / Event-Based |

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Kuwait |

| Oman |

| Bahrain |

| Jordan |

| Egypt |

| Rest of Middle East |

| By End-User | Commercial |

| Industrial | |

| Government and Institutional | |

| Residential | |

| By Service Type | Static Guarding |

| Mobile Patrol | |

| Event / Crowd-Control Security | |

| Cash-in-Transit (CIT) and Valuables Logistics | |

| K9 and Specialised Protection | |

| By Guard Classification | Unarmed Guards |

| Armed Guards | |

| By Contract Duration | Long-Term (More than 12 Months) |

| Short-Term / Event-Based | |

| By Country | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Jordan | |

| Egypt | |

| Rest of Middle East |

Key Questions Answered in the Report

How large is the Middle East manned security services market today?

The Middle East manned security services market size stands at USD 2.03 billion in 2026 and is on track to reach USD 2.44 billion by 2031.

Which country is showing the fastest growth in private guarding demand?

Saudi Arabia is advancing at a 4.58% CAGR through 2031 due to Vision 2030 giga-projects and a surge in licensed entertainment events.

What drives the shift toward specialized services like K9 and executive protection?

Airports, critical infrastructure, and high-net-worth individuals demand higher detection accuracy and personal safety, allowing K9 and close-protection teams to command 25-40% pricing premiums.

How are wage hikes affecting security providers in the Gulf?

Minimum wage increases of up to 25% and localization quotas are compressing EBITDA margins to single digits, pushing firms to favor long-term contracts with escalation clauses.

Is technology replacing guards in the region?

AI analytics, drones, and biometric access have cut static headcount by about 15%, but regulations still impose minimum guard ratios at critical sites, sustaining thousands of roles.

What compliance hurdles face new entrants in Dubai?

Security firms must post an AED 500,000 bond, document three years of operations, and enroll all guards in biometric and 48-hour training programs before receiving a SIRA license.

Page last updated on: