Pipeline Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

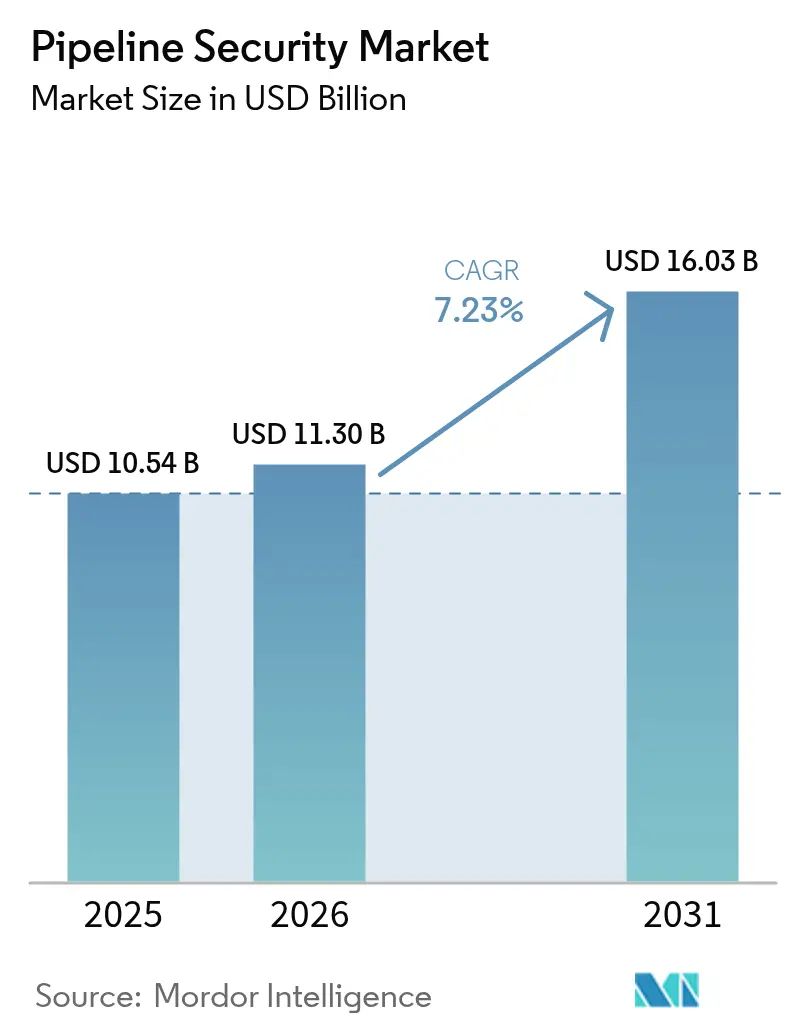

| Market Size (2026) | USD 11.3 Billion |

| Market Size (2031) | USD 16.03 Billion |

| Growth Rate (2026 - 2031) | 7.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

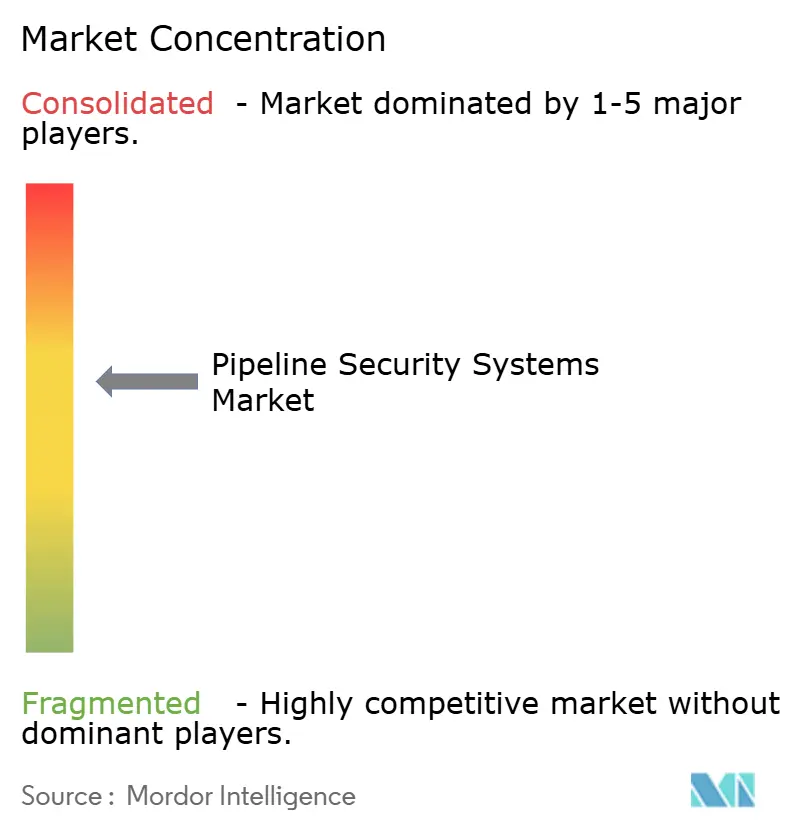

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pipeline Security Market Analysis by Mordor Intelligence

The pipeline security market size in 2026 is estimated at USD 11.3 billion, growing from 2025 value of USD 10.54 billion with 2031 projections showing USD 16.03 billion, growing at 7.23% CAGR over 2026-2031. Rising geopolitical tensions, tougher safety mandates, and the technical challenge of monitoring thousands of kilometers of mixed-product lines are sustaining capital outlays on both physical and cyber safeguards. A growing share of investment now targets integrated platforms that blend fiber-optic distributed acoustic sensing with OT-cybersecurity analytics, enabling faster threat identification and coordinated response. Operators are also racing to secure nascent hydrogen and CO₂ corridors, where embrittlement monitoring and leak-detection algorithms must be recalibrated for smaller-molecule gases. These trends collectively underpin a multi-year demand cycle that favors vendors able to converge sensor data, geospatial intelligence, and machine-learning insights into a single decision framework.

Key Report Takeaways

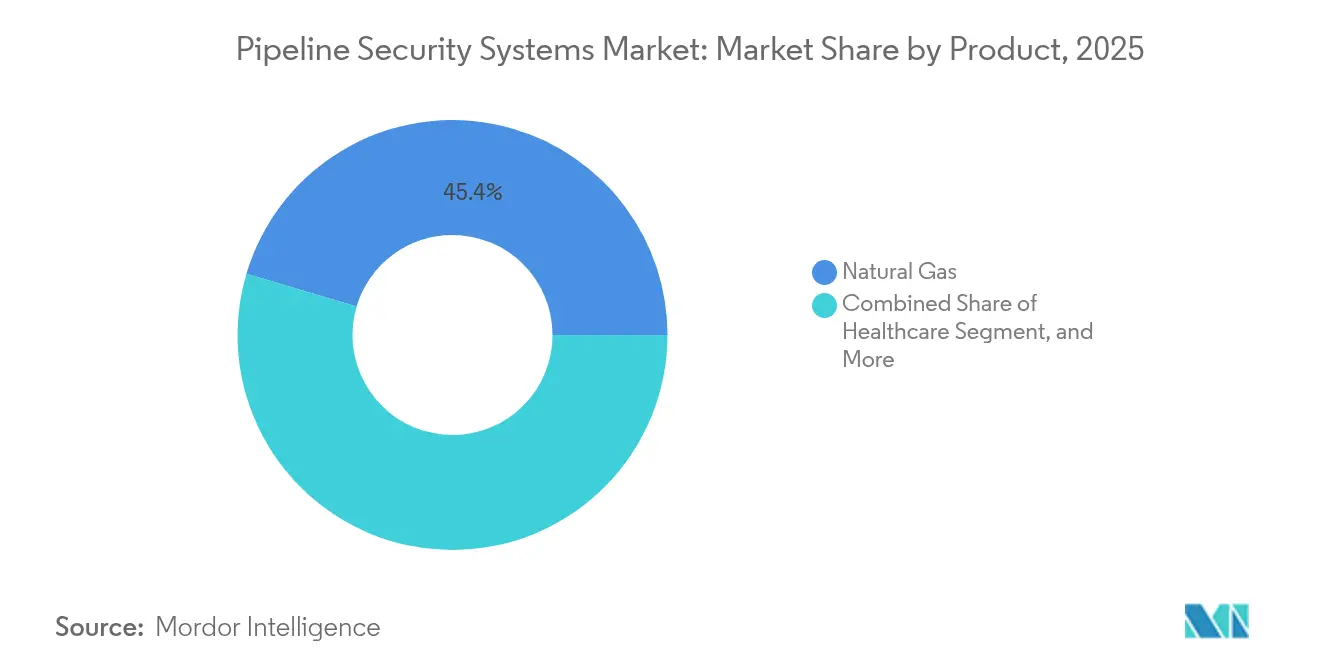

- By product, natural gas pipelines captured 45.40% of the 2025 pipeline security market share, while hydrogen and CO₂ lines are forecast to expand at an 8.17% CAGR through 2031.

- By technology and solution, supervisory control and data acquisition systems held 31.20% of 2025 revenue, whereas integrated end-to-end platforms are projected to grow at 8.74% CAGR.

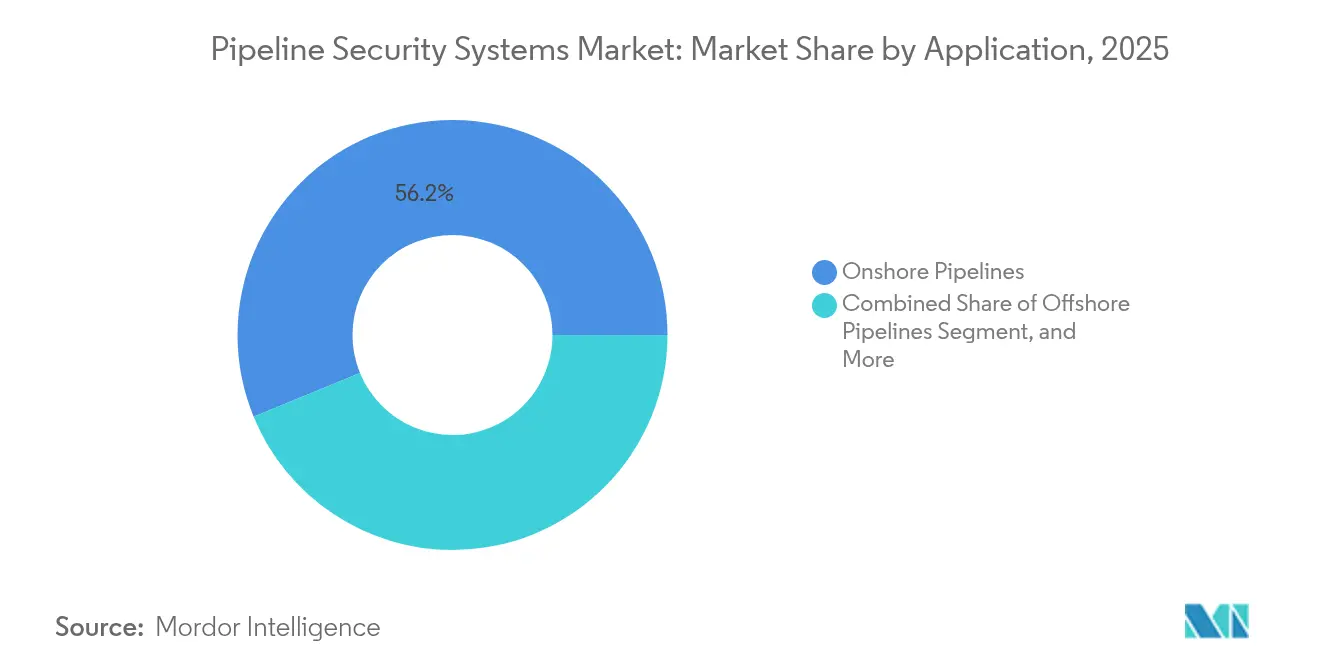

- By application, onshore corridors generated 56.20% of 2025 value, but offshore routes are expected to lead growth at 9.35% CAGR.

- By security type, physical security accounted for 50.30% of 2025 spending, yet OT-cybersecurity solutions will advance at an 7.72% CAGR to 2031.

- By geography North America retained 37.90% of 2025 revenue, while Asia-Pacific is positioned for the fastest regional expansion at 9.12% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pipeline Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Cross-Border Energy Trade Routes | +1.5% | Asia-Pacific, Middle East, Europe | Long term (≥ 4 years) |

| Stringent Environmental and Safety Regulations | +1.2% | North America and Europe, spreading to Asia-Pacific | Medium term (2-4 years) |

| Increasing Incidence of Sabotage and Terrorism Attacks | +1.0% | Global hot spots in South America, Middle East, Sub-Saharan Africa | Short term (≤ 2 years) |

| Growing Adoption of AI-Powered Leak Detection | +0.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Integration of Fiber-Optic Sensing | +0.7% | North America and Middle East | Medium term (2-4 years) |

| Proliferation of Remote, Unmanned Operations | +0.6% | North America, Australia, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Cross-Border Energy Trade Routes

Mega-projects such as the 5,600-kilometer Nigeria-Morocco line and Saudi Arabia’s 4,000-kilometer Jafurah network illustrate how multinational corridors heighten security complexity by spanning jurisdictions with divergent enforcement standards. Operators must coordinate incident response protocols, satellite surveillance, and fiber-optic intrusion detection across multiple legal frameworks, driving per-kilometer security budgets higher than domestic averages

Stringent Environmental and Safety Regulations

The U.S. Pipeline and Hazardous Materials Safety Administration’s 2024 rule requires leak-detection systems that spot 8% of maximum flow within 30 minutes, a threshold that effectively disqualifies legacy hydraulic models and pushes adoption of real-time acoustic sensing. Complementary EPA amendments extend risk-management audits to liquid pipelines near populated zones, adding third-party security reviews to compliance checklists. Similar pressure is mounting in Europe, where draft hydrogen network codes call for continuous embrittlement monitoring on repurposed lines

Increasing Incidence of Sabotage and Terrorism Attacks

The 2024 bombings of Colombia’s Caño Limón-Coveñas pipeline and renewed focus on the 2022 Nord Stream sabotage highlight the financial and reputational fallout of physical attacks. Operators now blend aerial drones, seabed acoustic arrays, and social-media threat mining to anticipate hostile activity, redirecting capital from reactive repairs toward predictive monitoring platforms

Growing Adoption of AI-Powered Leak Detection Solutions

Machine-learning models trained on distributed acoustic sensing data have achieved 97% detection accuracy with false-positive rates below 2%, materially outperforming rule-based systems. Vendors such as Honeywell embed these algorithms at edge gateways to cut latency and bandwidth costs, while government funding accelerates R&D for hydrogen-specific leak signatures. The payoff is faster isolation of leaks and lower clean-up liabilities, bolstering ROI on advanced sensing rollouts.[1]Honeywell, “Honeywell Forge Industrial AI Updates,” honeywell.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation and Maintenance Costs | -0.8% | Global, especially emerging markets | Short term (≤ 2 years) |

| Complex, Heterogeneous Legacy Infrastructure | -0.6% | North America, Europe, mature Asia-Pacific pipelines | Medium term (2-4 years) |

| Shortage of Qualified OT-Cybersecurity Professionals | -0.5% | Asia-Pacific and Middle East | Long term (≥ 4 years) |

| Limited Budget Allocation in Emerging Economies | -0.4% | Africa, South America, Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Maintenance Costs

Fiber-optic distributed acoustic sensing can exceed USD 10,000 per kilometer when installation, interrogator units, and SCADA integration are included, and annual software licenses add up to 20% of total life-cycle spending. Offshore pipelines bear even steeper costs: autonomous underwater vehicles, seabed arrays, and specialty corrosion sensors can push security budgets to 10% of total capex, challenging project economics for marginal fields

Complex, Heterogeneous Legacy Infrastructure

Older lines use multiple SCADA vintages, proprietary protocols, and disparate sensor fleets, creating data silos that complicate holistic threat monitoring. Integrating modern analytics platforms with 30-year-old Remote Terminal Units often requires protocol converters and staged cutovers, lengthening deployment time and elevating cybersecurity risk during transitions

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Hydrogen Networks Drive Diversification

Hydrogen and CO₂ pipelines are on track to expand at an 8.17% CAGR, the fastest pace among products, as governments underwrite green-hydrogen export corridors and carbon-capture value chain. This emerging network demands real-time strain sensing and embrittlement analytics that legacy natural-gas systems cannot deliver. Operators are piloting fiber-optic strain gauges to spot microfractures before rupture, a prerequisite for insurance underwriting in newbuild hydrogen corridors. In contrast, natural gas lines held a 45.40% share of the pipeline security market in 2025, sustained by LNG export buildouts in the United States, Qatar, and Australia.

Natural gas assets will continue to anchor revenue, but upside potential shifts toward hydrogen once demand visibility improves. Crude oil routes remain stable in security outlays owing to high spill liability, yet long-term growth is muted by electric-vehicle penetration. Hazardous-liquid and chemical pipelines funnel premium budgets into automated shutoff valves and multi-factor perimeter controls because any release can prompt class-action litigation within hours. Carbon dioxide networks for sequestration are at a formative stage, but forward-looking operators view the segment as a hedge against eventual emission-pricing regimes, keeping R&D pipelines active for CO₂-specific sensor suites

By Technology and Solution: Platforms Eclipse Point Products

Integrated end-to-end platforms are forecast to grow at 8.74% CAGR through 2031, reflecting operator preference for a single dashboard that unifies acoustic alerts, video feeds, GIS overlays, and cyber-threat telemetry. SCADA-only environments, though still 31.20% of 2025 revenue, are losing share as operators switch to edge-computing nodes that preprocess data locally, cutting latency and bandwidth commitments. Vulnerability disclosures affecting widely deployed SCADA vendors have hastened adoption of zero-trust architectures and micro-segmentation to isolate OT assets from enterprise IT.

Perimeter-security modules fencing, radar, and thermal cameras remain critical, but their market share slides as procurement officers bundle them into platform licenses instead of standalone buys. Computer-vision analytics now flag anomalous activity autonomously, freeing control-room staff for higher-order triage. Meanwhile, sensor innovation is shifting from hardware to firmware, with machine-learning edge nodes extracting leak-detection features directly from distributed acoustic sensing waveforms, improving accuracy while cutting false alarms by 30% compared to rule-based thresholds. These advances enlarge the addressable market among mid-tier operators once priced out of premium gear, broadening the revenue base for platform vendors

By Application: Offshore Complexity Commands Premium

Offshore corridors are projected to register a 9.35% CAGR through 2031 as deepwater fields in Guyana, Brazil, and Mozambique reach final investment decision. Water depths exceeding 2,000 meters and pressures above 10,000 psi necessitate autonomous underwater vehicle patrols and seabed acoustic arrays that add significant incremental cost yet deliver early-warning insights unreachable from the surface. Onshore lines, though accounting for 56.20% of 2025 revenue, experience lower per-kilometer spend because aerial drones and patrol vehicles mitigate many threats at modest outlay.

Gathering and distribution networks represent a fragmented long tail of smaller operators who often rely on basic pressure monitoring, yet tightening EPA and state regulations are nudging them toward battery-powered acoustic nodes and cloud-hosted analytics for first-time leak detection. Refined-products pipelines remain a security focal point after the 2021 Colonial ransomware incident, leading to mandated network segmentation and intrusion-detection deployments on OT networks. Subsea inspection cycles, once annual, now trend toward continuous monitoring via permanent sensor strings as insurers tighten coverage requirements, raising the recurring revenue streams for service providers

By Security Type: Cyber Threats Redefine Perimeters

Physical safeguards captured 50.30% of 2025 spending, yet OT-cybersecurity will deliver the fastest growth at 7.72% CAGR as attackers shift from physical sabotage to digital compromise. The Volt Typhoon campaign, which exploited unpatched edge routers to gain SCADA access, demonstrated how cyber breaches can prepare the ground for kinetic disruptions without breaching a fence. Operators now integrate network segmentation, multi-factor authentication, and continuous vulnerability scanning into core capex plans rather than IT afterthoughts.

Converged operations centers, staffed by teams cross-trained in both physical and cyber disciplines, are emerging as best practice, allowing a single incident-response playbook for multi-vector threats. Physical countermeasures are evolving toward mobility unmanned aerial vehicles, rapid-deployed command trailers, and AI-enabled video analytics that flag suspicious loitering while static fencing receives only maintenance capex. This functional convergence favors suppliers with deep software pedigree over hardware-only manufacturers, accelerating industry consolidation as platform vendors acquire perimeter specialists to round out offerings.

Geography Analysis

North America remained the single largest contributor with 37.90% of 2025 revenue, thanks to the United States’ 3 million-kilometer grid and Canada’s export corridors linking western basins to coastal terminals. Compliance spending accelerated after PHMSA’s 2024 leak-detection rule, prompting widespread retrofits of fiber-optic distributed acoustic sensing and linking of fault-isolation valves to real-time analytics. Meanwhile, cross-border projects moving Permian gas into Mexico face dual compliance audits from both U.S. and Mexican regulators, lifting consulting hours and driving platform upgrades that bridge language and protocol differences.

Asia-Pacific will outpace all regions at a 9.12% CAGR, fueled by 80% of global gas-pipeline kilometers now under construction across China, India, and Southeast Asia. China’s Central-Asia. corridor overlays new surveillance gear on legacy lines that lacked basic telemetry, while India’s city-gas push forces distributors to adopt low-cost acoustic sensors scalable to thousands of urban kilometers. Japan and South Korea add seismic monitoring layers around LNG import terminals, and Asia-Pacific members negotiate federated security clauses in the proposed Trans-Asia-PacificGas Pipeline, delaying tenders but raising future per-kilometer outlays.

Europe’s market is shaped by dual imperatives: decarbonization and resilience following disrupted Russian flows. Draft hydrogen rules require real-time embrittlement monitoring on repurposed gas lines, a specification not yet available at commercial scale. Elsewhere, the Middle East bankrolls dual-use networks capable of carrying natural gas today and hydrogen tomorrow, with Saudi Aramco’s Jafurah lines fitted with distributed acoustic sensing from inception. Africa’s split market pairs North-African adoption of European-grade systems against Sub-Saharan budget constraints, while South America’s growth centers on Vaca Muerta pipelines mandated to embed fiber-optic monitoring to meet environmental permits

Competitive Landscape

Large automation conglomerates Honeywell, Siemens, ABB, Schneider Electric, and Rockwell Automation dominate platform sales by bundling security modules with existing PLC and DCS installations, monetizing service contracts and software subscriptions rather than pure hardware volumes. Their advantage lies in global service networks and legacy-system interoperability, which reduce project risk for operators modernizing multi-vendor estates. Fiber-optic sensing specialists such as OptaSense, Senstar, and Future Fibre Technologies have carved high-margin niches in critical corridors where leak-related liabilities justify premium pricing.

Market boundaries are blurring as customers insist on converged dashboards capable of ingesting acoustic, thermal, satellite, and cyber telemetry. This requirement favors vendors with strong data-science benches and secure-by-design code bases, pressuring hardware-centric firms to acquire analytics capabilities or risk commoditization.

Mid-tier entrants focus on underserved segments: battery-powered acoustic nodes for gathering networks, satellite-based methane plume detection for Arctic pipelines, and blockchain-anchored audit logs for regulatory reporting. Patent filings in 2024 clustered around sensor-fusion algorithms and edge-processing of distributed acoustic sensing data, signaling an arms race to reduce bandwidth costs while raising detection fidelity. Regulatory initiatives such as CISA’s Secure-by-Design push reward vendors that ship products with encrypted firmware, signed updates, and open vulnerability-disclosure programs, reshaping procurement scorecards in favor of cyber-mature suppliers.[3] Cybersecurity and Infrastructure Security Agency, “Secure by Design Initiative,” cisa.gov

Pipeline Security Industry Leaders

Honeywell International Inc.

General Electric Company

ABB Ltd.

Rockwell Automation, Inc.

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The Economic Community of West African States opened tenders for the Nigeria-Morocco Gas Pipeline, stipulating satellite surveillance and fiber-optic intrusion detection along the full 5,600 kilometers.

- December 2024: Argentina approved Transportadora de Gas del Sur’s USD 500 million Vaca Muerta evacuation line, mandating fiber-optic distributed acoustic sensing on every kilometer.

- November 2024: Brazil and Argentina signed an MOU to co-develop gas export infrastructure capable of moving up to 30 million m³ per day by 2030, including harmonized security standards.

- October 2024: PHMSA finalized valve-installation and rupture-detection rules requiring 8%-within-30-minutes leak-detection performance on approximately 300,000 kilometers of U.S. transmission pipelines.

Global Pipeline Security Market Report Scope

The pipeline security systems protects land-based pipelines against illegal tapping, terririst actions, and sabotage. It detects threats and leakages and alert security and maintenance teams before the incident occurs.It enables remotely monitor the pipeline infrastructure and avoid hazardaous accidents. The scope of the study for pipeline security market is limited to the type of security systems offered by the vendors for different commodity pipelines globally. The after sales service are not considered for market estimation.

The Pipeline Security Market Report is Segmented by Product (Natural Gas, Crude Oil, Hazardous Liquid/Chemicals, Hydrogen and CO₂ Pipelines, Other Products), Technology and Solution (SCADA Systems, Perimeter Security, ICS Security, Video Surveillance, Pipeline Monitoring Sensors, Integrated Platforms), Application (Onshore, Offshore, Gathering Networks, Refined Products), Security Type (Physical, OT Cybersecurity, Converged), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

| Natural Gas |

| Crude Oil |

| Hazardous Liquid / Chemicals |

| Hydrogen and CO? Pipelines |

| Other Products |

| Supervisory Control and Data Acquisition (SCADA) Systems |

| Perimeter Security and Intruder Detection Systems |

| Industrial Control Systems Security |

| Video Surveillance and GIS Mapping |

| Pipeline Monitoring Sensors and Analytics |

| Integrated End-to-End Security Platforms |

| Onshore Pipelines |

| Offshore Pipelines |

| Gathering and Distribution Networks |

| Refined Products Pipelines |

| Physical Security |

| Operational Technology (OT) Cybersecurity |

| Physical-Cyber Converged Solutions |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Natural Gas | |

| Crude Oil | ||

| Hazardous Liquid / Chemicals | ||

| Hydrogen and CO? Pipelines | ||

| Other Products | ||

| By Technology and Solution | Supervisory Control and Data Acquisition (SCADA) Systems | |

| Perimeter Security and Intruder Detection Systems | ||

| Industrial Control Systems Security | ||

| Video Surveillance and GIS Mapping | ||

| Pipeline Monitoring Sensors and Analytics | ||

| Integrated End-to-End Security Platforms | ||

| By Application | Onshore Pipelines | |

| Offshore Pipelines | ||

| Gathering and Distribution Networks | ||

| Refined Products Pipelines | ||

| By Security Type | Physical Security | |

| Operational Technology (OT) Cybersecurity | ||

| Physical-Cyber Converged Solutions | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast CAGR for pipeline-security spending through 2031?

The pipeline security market is projected to grow at a 7.23% CAGR between 2026 and 2031.

Which product segment will grow fastest over the next five years?

Hydrogen and CO₂ networks lead with an expected 8.17% CAGR as decarbonization programs accelerate investment in new corridors.

Why is Asia-Pacific attracting the most new pipeline-security investment?

The region accounts for over 80% of global gas-pipeline kilometers now in development, prompting a 9.12% CAGR forecast for security solutions.

How are regulations influencing technology selection?

Standards such as PHMSA’s 8%-within-30-minutes leak-detection rule are pushing operators toward fiber-optic acoustic sensing and AI-enabled analytics.

Which vendors dominate integrated security platforms?

Honeywell, Siemens, ABB, Schneider Electric, and Rockwell Automation hold the largest installed bases, leveraging PLC and DCS footprints to upsell security modules.

What is driving demand for OT-cybersecurity solutions?

Campaigns like Volt Typhoon proved that cyber intrusions can pre-position for physical disruption, prompting operators to allocate growing budgets to network segmentation, multifactor authentication, and continuous vulnerability scanning.

Page last updated on: