Europe Integrated Circuits Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

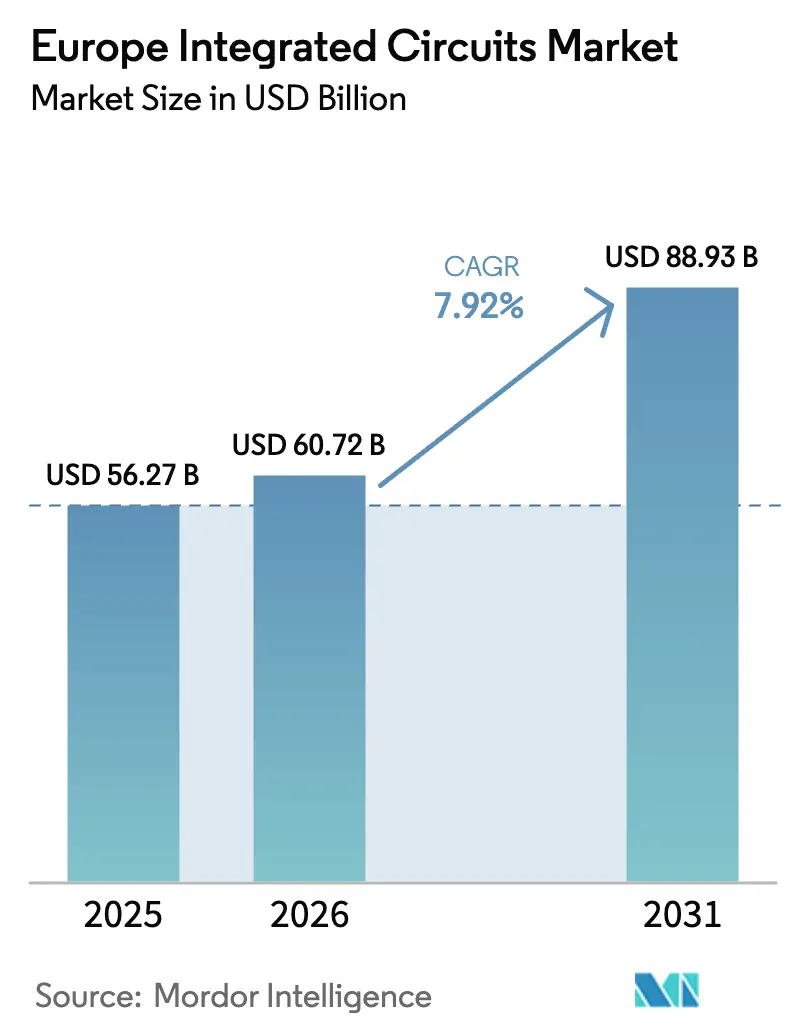

| Base Year Market Size (2025) | USD 56.27 Billion |

| Market Size (2026) | USD 60.72 Billion |

| Market Size (2031) | USD 88.93 Billion |

| Growth Rate (2026 - 2031) | 7.92% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Integrated Circuits Market Analysis by Mordor Intelligence

The European integrated circuits market size was valued at USD 56.27 billion in 2025 and estimated to grow from USD 60.72 billion in 2026 to reach USD 88.93 billion by 2031, at a CAGR of 7.92% during the forecast period (2026-2031). Momentum reflects the region’s concerted push for semiconductor sovereignty, a goal anchored by the EUR 43 billion (USD 50.62 billion) EU Chips Act and more than EUR 80 billion (USD 94.17 billion) in pledged private investments that have spread across front-end fabs, advanced packaging lines, and research nodes. Automotive electrification has been the single biggest catalyst, with German original-equipment manufacturers (OEMs) signing long-term silicon carbide and power device contracts to secure supply for next-generation electric vehicles. Memory devices are advancing fastest on the back of edge-AI rollouts in European factories, while analog components still hold the largest revenue slice thanks to their ubiquity in power management and sensor interfaces. Germany’s Dresden cluster anchors regional capacity expansions, yet Italy has emerged as the fastest climber after the approval of a EUR 1.3 billion (USD 1.53 billion) advanced packaging hub in Catania. Structural headwinds persist: sub-10 nm foundry capability remains scarce, fab electricity bills are tied to volatile energy markets, and a looming talent shortage threatens throughput as nearly two-fifths of the United Kingdom’s semiconductor workforce approaches retirement.[1]UK Government, “UK Semiconductor Workforce Study: Executive Summary,” gov.uk

Key Report Takeaways

- By IC type, analog devices led with 31.85% of the European integrated circuits market share in 2025, while memory ICs are on track for the fastest 9.08% CAGR to 2031.

- By technology node, >90 nm processes accounted for 45.08% revenue in 2025; <10 nm nodes are poised for a 15.62% CAGR through 2031.

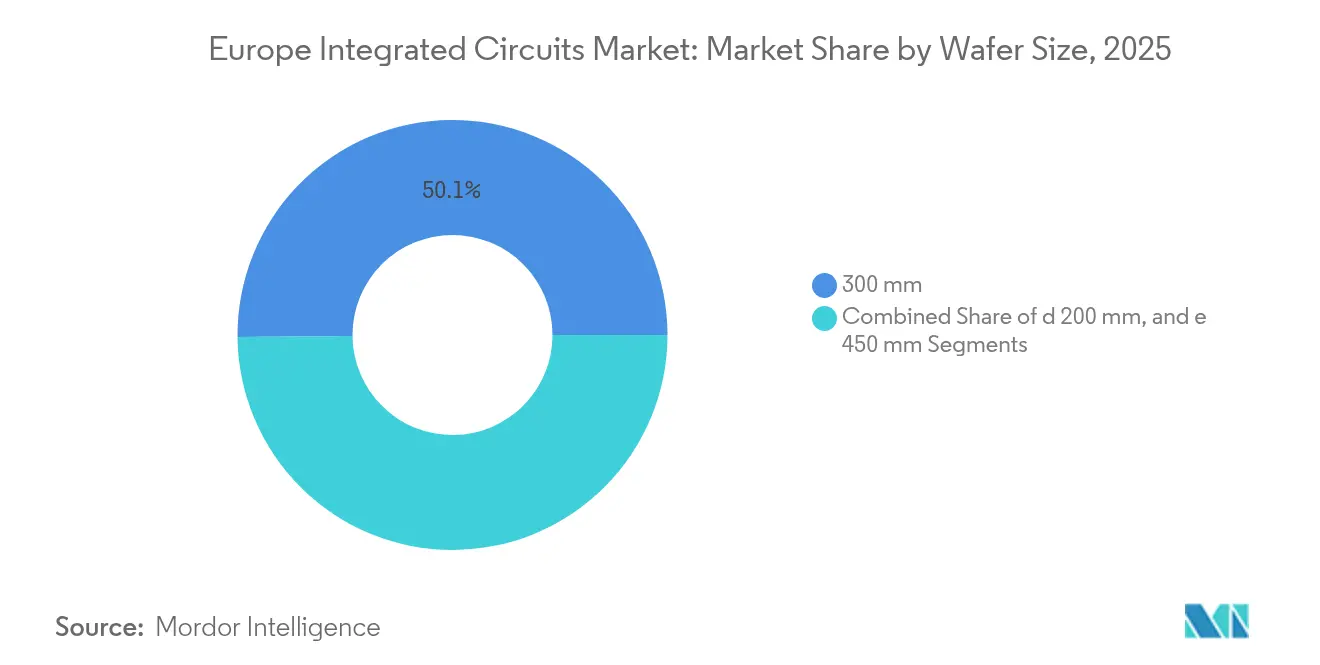

- By wafer size, 300 mm substrates captured 50.14% of the European integrated circuits market size in 2025; ≥450 mm wafers are forecast to expand at a 14.75% CAGR.

- By end-user, consumer electronics held 39.92% revenue share in 2025, whereas automotive applications are accelerating at a 13.12% CAGR.

- By country, Germany dominated with a 28.95% Europe integrated circuits market share in 2025; Italy is projected to post an 8.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe contributes to a system defined not by any single geography but by the interaction of many. The global integrated circuits market data by Mordor Intelligence represents that combined structure.

Europe Integrated Circuits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Chips Act–Driven Capacity Expansion Incentives | +2.1% | Germany, France, Italy, Netherlands | Medium term (2-4 years) |

| Automotive Electrification Surge Led by German OEMs | +1.8% | Germany, France, Italy, Nordic countries | Short term (≤ 2 years) |

| Edge-AI and IIoT Deployment Across European Factories | +1.4% | Germany, Netherlands, France, Nordic countries | Medium term (2-4 years) |

| Renewable-Energy Power Electronics Demand in Nordics | +0.9% | Nordic countries, Germany, Netherlands | Long term (≥ 4 years) |

| Space and Defense Autonomy Programs (ESA, EDF) | +0.7% | France, Germany, Italy, Spain | Long term (≥ 4 years) |

| Transition to 3D/Advanced Packaging in European R&D Hubs | +1.2% | Belgium, Netherlands, Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Chips Act – capacity expansion incentives

Public subsidies unlocked by the Act reshaped Europe’s cost structure for fabs, allowing Infineon to green-light a USD 5 billion Smart Power Fab in Dresden after securing EUR 1 billion (USD 1.18 billion) in state aid. The legislation’s three-pillar design integrates research networks with pilot-line funding, enabling start-ups and institutes to move prototypes into volume faster. An EU-level monitoring system now tracks inventory across the value chain, offering early warning on disruptions that plagued the region in 2021–2022. Together, these levers narrow cost differentials with Asian peers and support Europe's integrated circuits market expansion by balancing strategic autonomy with open trade.

Automotive electrification surge led by German OEMs

Electric vehicles require 3–5 times more semiconductors than combustion cars; Volkswagen, therefore, signed a multi-year power-device pact with onsemi, which is scaling end-to-end silicon-carbide output in the Czech Republic to serve European plants. Infineon’s AURIX and TRAVEO microcontroller lines pushed their global automotive MCU share to 29% in 2024, underscoring how embedded processing and high-voltage control dominate design wins. Zone-control architectures and over-the-air update features intensify the need for secure, high-bandwidth interfaces, driving broad-based demand across analog, logic, and memory categories within the European integrated circuits market.

Edge-AI and IIoT deployment across European factories

Industrial firms in Germany and the Netherlands installed AI-enabled vibration and temperature monitors that predict machine failure, relying on ultra-low-power mixed-signal chipsets such as Analog Devices’ Voyager4 sensor platform. The EU-funded PREVAIL consortium allocated EUR 156 million (USD 183.63 million) to accelerate on-device intelligence, pairing CEA-Leti and Fraunhofer with fabless start-ups to co-develop neuromorphic cores. Rising factory digitalization fuels persistent double-digit unit growth for industrial MCUs, connectivity ICs, and high-end memory, expanding the European integrated circuits market across mid-sized manufacturing economies.

Renewable-energy power electronics demand in Nordics

Massive offshore wind complexes like Ørsted’s 2.4 GW Hornsea 4 need fast-switching power modules to stabilize variable output. Hitachi Energy shipped Europe’s first enhanced STATCOM system using wide-band-gap semiconductors to the project, spotlighting gallium nitride and silicon-carbide devices as grid enablers. Meanwhile, Nordic data centers built with 100% renewable supply, such as Microsoft’s USD 3.2 billion Swedish campus, require high-efficiency power chains, reinforcing demand for advanced ICs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited <10 nm Foundry Capacity within Europe | -1.6% | Germany, Netherlands, France, Belgium | Medium term (2-4 years) |

| Energy Price Volatility Impacting Fab OPEX | -0.8% | Germany, Netherlands, France, Italy | Short term (≤ 2 years) |

| Semiconductor-Skilled Labour Shortage and Aging Workforce | -1.1% | Germany, UK, France, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited <10 nm foundry capacity within Europe

TSMC’s Dresden joint venture will focus on 28 nm and above nodes, leaving European handset and high-performance computing designers dependent on Asian fabs for advanced logic.[2]Taiwan Semiconductor Manufacturing Company Limited, “ESMC Breaks Ground on Dresden Fab,” pr.tsmc.com Sub-10 nm facilities demand USD 20 billion-plus outlays and top-tier EUV ecosystems that only a handful of companies can deploy. IMEC’s High-NA EUV pilot line will not reach commercial scale before 2028, prolonging the technology gap. The shortfall constrains Europe's integrated circuits market participation in AI accelerators, 5G radio silicon, and flagship mobile processors.

Semiconductor-skilled labour shortage and aging workforce

The United Kingdom reported that 39% of its semiconductor employees could retire within 15 years, while universities graduate insufficient process-engineering talent to compensate. SEMI projects a need for 1 million additional workers across Europe by 2030, a gap that threatens to cap fab utilisation and delay ramp-ups. Apprenticeships and cross-border mobility programs are in place, yet the lead time to cultivate niche expertise spans five to seven years, dampening the Europe integrated circuits market’s growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By IC Type: Memory Gains Momentum

Analog components held a commanding 31.85% revenue share in 2025, reflecting their ubiquity across power management and sensing circuits in vehicles and industrial automation. Memory devices, however, are scaling fastest at a 9.08% CAGR as edge-AI workloads and in-vehicle infotainment demand high-bandwidth, low-latency storage. This shift points toward heterogeneous architectures where processing-in-memory and neuromorphic arrays compress data-movement overhead. The European integrated circuits market size for memory chips dedicated to automotive advanced driver-assistance systems is projected to grow by double digits annually through 2030, fueled by infotainment upgrades and sensor fusion modules. Logic devices remain pivotal for functional safety, underpinning automotive microcontrollers and industrial PLCs. Infineon’s AURIX family illustrates Europe’s edge, pairing real-time control cores with cybersecurity blocks that comply with ISO 26262 functional-safety standards.

The memory surge dovetails with Europe’s strategic tilt toward decentralized computing: factory robots, smart-grid nodes, and autonomous shuttles all require on-board inference engines. Novel non-volatile memories that combine endurance with low energy draw are under joint development by CEA-Leti and STMicroelectronics, aligning with EU calls for sovereign edge-AI hardware. As such, the European integrated circuits market continues to rebalance toward data-centric architectures without eroding analog’s bedrock role.

By Technology Node: Legacy Dominates, Leading Edge Accelerates

Nodes above 90 nm commanded 45.08% of 2025 revenue, underscoring Europe’s alignment with “more-than-Moore” sectors like powertrain control and smart-grid metering, where high voltage tolerance and robust qualification outweigh sheer transistor density. Sub-10 nm chips attracted the steepest 15.62% CAGR outlook—yet from a modest base—driven by AI accelerators and premium handset SoCs. The 28–90 nm bracket delivers the cost-performance sweet spot for automotive radar processors and industrial controllers, sustaining high-volume output at legacy fabs. Europe's integrated circuits market size growth within the 10–28 nm tier will hinge on new Dresden capacity, which targets 28 nm FinFET lines optimised for automotive safety integrity.

imec’s monolithic CFET proof-of-concept, featuring stacked complementary transistors, signals Europe’s capacity to influence next-decade scaling paradigms. Nonetheless, commercial translation depends on further capital infusion and ecosystem alignment around high-NA EUV lithography.

By Wafer Size: 300 mm Standard, 450 mm on Horizon

300 mm lines generated 50.14% of 2025 revenue, positioning them as the economic backbone for Europe's integrated circuits market fabrication. Companies are eyeing ≥450 mm wafers, projected to swell at 14.75% CAGR, as a lever for lower die cost in power and mixed-signal applications. Infineon’s first 200 mm silicon-carbide product release represents an intermediate milestone towards larger-diameter wide-band-gap production. Smaller formats, especially 150 mm gallium-nitride lines in the United Kingdom, will persist for niche high-mix, low-volume runs that underpin quick-turn aerospace programs.

Adopting 450 mm substrates requires concurrent investments in lithography and metrology tools; ASML’s leadership in the Netherlands positions Europe favorably once demand justifies the transition. Cost gains from bigger wafers will flow into competitive pricing for automotive inverters and server power supplies, reinforcing the Europe integrated circuits market’s scale advantages.

By End-user Industry: Automotive Accelerates

Consumer electronics retained the largest 39.92% piece of 2025 revenue, covering smartphones, wearables, and smart-home nodes distributed across Western Europe. Yet automotive semiconductors are sprinting ahead with a 13.12% CAGR as EV penetration climbs toward the EU’s 2035 zero-emission mandate. Software-defined architectures featuring centralized domain controllers necessitate high-speed network switches and zonal gateways, boosting logical, analog, and memory chip demand in tandem. The European integrated circuits market size for automotive power modules is forecast to roughly double between 2025 and 2030 as silicon-carbide traction inverters scale in mainstream vehicle segments.

Industrial automation, propelled by IIoT retrofits, adds a steady growth layer, while data-center silicon in Nordic countries profits from abundant renewable energy. Aerospace and defense buyers drive margins through high-reliability gallium-nitride and radiation-hardened designs funded by European Space Agency satellite programs.

Geography Analysis

Germany’s Europe integrated circuits market leadership stemmed from a 28.95% revenue share in 2025, buoyed by automotive OEM proximity and large-scale fab investments such as TSMC’s EUR 10 billion (USD 11.77 billion) Dresden joint venture. Infineon’s Smart Power Fab—supported by EUR 1 billion (USD 1.18 billion) in EU Chips Act grants—expanded regional supply capacity for power devices and microcontrollers. Despite high industrial electricity costs, Germany leveraged a mature engineering talent base and tight OEM-supplier integration, reinforcing its hub status. Research outfits like Fraunhofer IIS accelerated the development of advanced in-car networking chips, sustaining technology spillovers into adjacent segments.

Italy emerged as the fastest-growing locale at an 8.34% CAGR outlook to 2031, catalysed by the European Commission’s EUR 1.3 billion (USD 1.53 billion) approval for Silicon Box’s chiplet-integration facility in Catania. The initiative unlocks leading-edge packaging services previously unavailable in Europe, positioning Italy as an anchor for heterogeneous integration across AI, data-center, and automotive workloads. STMicroelectronics further lifted local momentum by ramping 200 mm silicon-carbide wafer output for traction inverters, aligning with Italy’s sizeable automotive tier-1 supplier base.

France, the United Kingdom, and Nordic nations together account for a growing tranche of demand. France leveraged CEA-Leti’s R&D assets to push GaN-on-silicon RF devices into space platforms, while ST’s Tours site continued to supply high-reliability power modules to Airbus and Safran. The UK’s compound-semiconductor cluster in Newport harnessed GaN expertise for 5G macro-cell base stations, securing European competitive positioning even after Brexit. Nordic countries—especially Sweden and Denmark—captured power-electronics investments tied to offshore wind and renewable-powered data centers, enabling a virtuous cycle between green energy and semiconductor manufacturing needs.

The integrated circuits market is analyzed by Mordor Intelligence across multiple other geographies. This is complemented by country-specific insights for United States, South Korea, Taiwan, and China, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

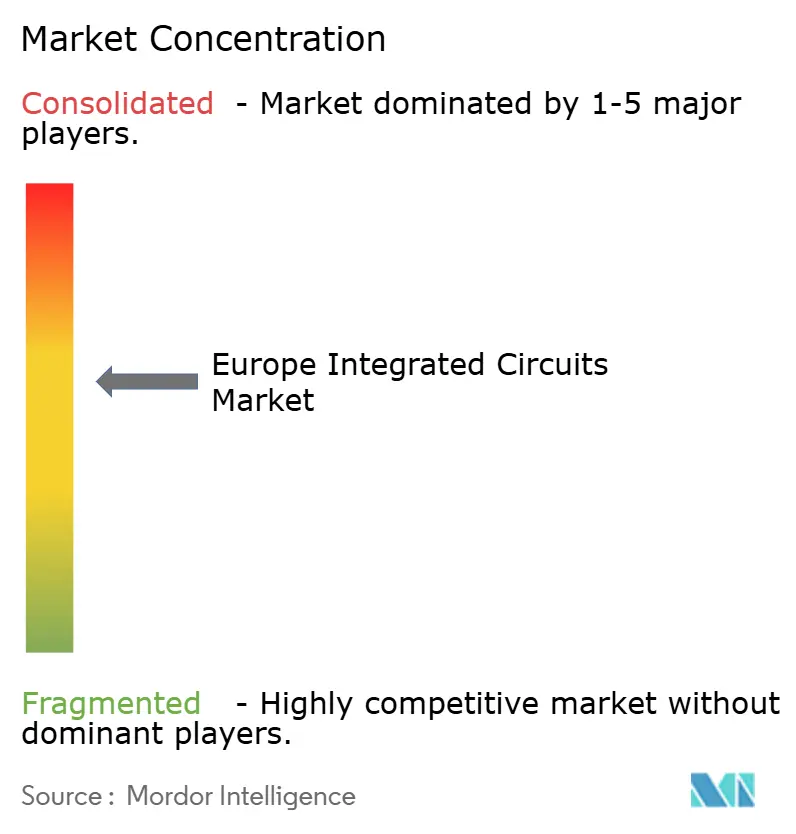

The European integrated circuits market is moderately concentrated: the top five suppliers held a majority of combined revenue in 2024, creating a competitive arena where regional champions and multinational foundries jostle for automotive and industrial sockets. Infineon, STMicroelectronics, and NXP strengthened their positions by leveraging EU Chips Act incentives to expand in-region wafer starts. Infineon’s USD 2.5 billion acquisition of Marvell’s Automotive Ethernet business provides system-level differentiation for software-defined vehicles, while ST deepened vertical integration with front-end SiC capacity expansions in Italy.

Global players such as ON Semiconductor and Texas Instruments continued building European distribution and assembly footprints, with ON Semiconductor completing a USD 115 million buyout of Qorvo’s SiC JFET assets to broaden its EliteSiC module range. Meanwhile, the ESMC consortium—comprising TSMC, Bosch, Infineon and NXP—began constructing Europe’s first FinFET-capable pure-play foundry, providing the region with partial autonomy at 28 nm geometries and generating 2,000 direct jobs. The rise of advanced packaging as a differentiation layer opened whitespace opportunities for upcoming firms such as Silicon Box and Black Semiconductor, the latter securing EUR 254.4 million (USD 299.45 million) to industrialise graphene-based interconnect solutions.

Sustainability commitments have become differentiators: GlobalFoundries pledged net-zero emissions by 2050 and greater use of carbon-neutral power at its Dresden line, responding to EU taxonomy regulations.[4]GlobalFoundries, “GlobalFoundries Commits to Net Zero Emissions,” gf.com Intellectual-property protection equally rose in prominence; Cadence’s purchase of Secure-IC bolsters on-chip security for European automotive customers migrating to over-the-air updates. This mosaic of IDMs, fab-light players and specialised packaging firms sets a dynamic stage for the European integrated circuits market through 2030.

Europe Integrated Circuits Industry Leaders

-

Intel Corporation

-

Texas Instruments Inc

-

Analog Devices Inc

-

Infineon Technologies AG

-

STMicroelectronics N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Infineon acquired Marvell’s Automotive Ethernet unit for USD 2.5 billion to enhance software-defined vehicle solutions.

- February 2025: Infineon received EUR 1 billion (USD 1.13 billion) EU Chips Act funding for its Dresden Smart Power Fab, part of a USD 5 billion project expected to add 1,000 jobs.

- February 2025: SkyWater Technology agreed to acquire Infineon’s Austin 200 mm fab, preserving nearly 1,000 roles and expanding foundational chip capacity.

- January 2025: NXP secured a EUR 1 billion European Investment Bank loan to ramp R&D across five EU nations.

Europe Integrated Circuits Market Report Scope

Integrated circuits (ICs) are compact electronic devices that integrate multiple components—such as transistors, resistors, capacitors, and diodes—onto a single piece of semiconductor material, typically silicon. This integration facilitates the creation of complex circuits capable of performing various functions within a small physical footprint.

For market estimation, the revenue generated from sales of various types of integrated circuits that are used in various industries, such as consumer electronics, automotive, IT & telecommunication, manufacturing, and automation, across Europe has been tracked.

The European integrated circuits market is segmented by type (analog IC, logic IC, memory, and micro [microprocessor, microcontrollers, and digital signal processors]) and end-user industry (consumer electronics, automotive, IT & telecommunications, and manufacturing and automation). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Analog IC | |

| Logic IC | |

| Memory | Micro (MPU) |

| Micro (MCU) | |

| Digital Signal Processors |

| <10 nm |

| 10 – 28 nm |

| 28 – 90 nm |

| >90 nm |

| ≤ 200 mm |

| 300 mm |

| ≥ 450 mm |

| Consumer Electronics |

| Automotive |

| IT and Telecommunications |

| Industrial and Factory Automation |

| Data Centers and Cloud |

| Aerospace and Defense |

| Healthcare Devices |

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Netherlands |

| Nordics (Sweden, Finland, Denmark, Norway) |

| Rest of Europe |

| By IC Type | Analog IC | |

| Logic IC | ||

| Memory | Micro (MPU) | |

| Micro (MCU) | ||

| Digital Signal Processors | ||

| By Technology Node | <10 nm | |

| 10 – 28 nm | ||

| 28 – 90 nm | ||

| >90 nm | ||

| By Wafer Size | ≤ 200 mm | |

| 300 mm | ||

| ≥ 450 mm | ||

| By End-user Industry | Consumer Electronics | |

| Automotive | ||

| IT and Telecommunications | ||

| Industrial and Factory Automation | ||

| Data Centers and Cloud | ||

| Aerospace and Defense | ||

| Healthcare Devices | ||

| By Country | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Nordics (Sweden, Finland, Denmark, Norway) | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current size of the European integrated circuits market?

The European integrated circuits market stood at USD 60.72 billion in 2026.

How fast will the European integrated circuits market grow through 2031?

Revenue is forecast to rise to USD 88.93 billion by 2031, representing a 7.92% CAGR during the forecast period (2026-2031).

Which segment is expanding fastest?

Automotive applications post the quickest growth, advancing at a 13.12% CAGR thanks to electric-vehicle semiconductor demand.

Why is Germany dominant in the European integrated circuits market?

Germany combines large automotive OEM demand with major fab investments, resulting in a 28.95% revenue share in 2025.

What is the main bottleneck for Europe’s semiconductor ambitions?

A shortage of sub-10 nm foundry capacity forces designers to rely on Asian fabs for advanced logic, limiting regional sovereignty prospects.

How is the talent gap being addressed?

Industry and governments are launching apprenticeships and cross-border training programs, yet SEMI estimates Europe still needs 1 million additional workers by 2030.

Page last updated on: