Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

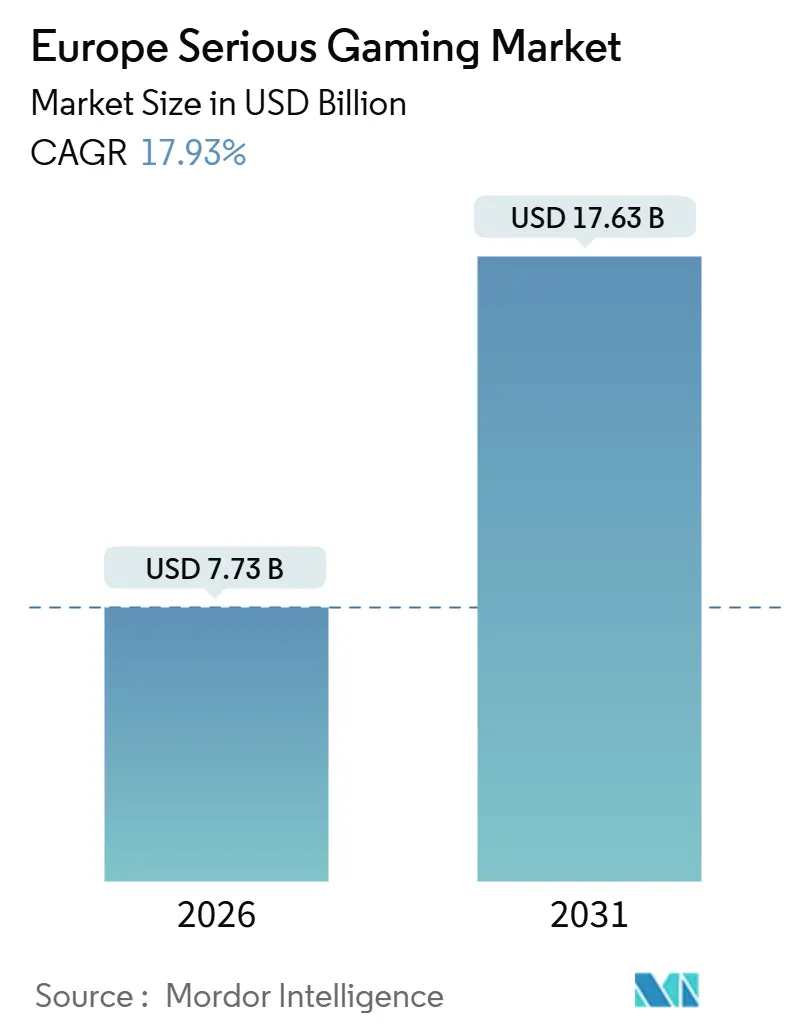

| Market Size (2026) | USD 7.73 Billion |

| Market Size (2031) | USD 17.63 Billion |

| Growth Rate (2026 - 2031) | 17.93% CAGR |

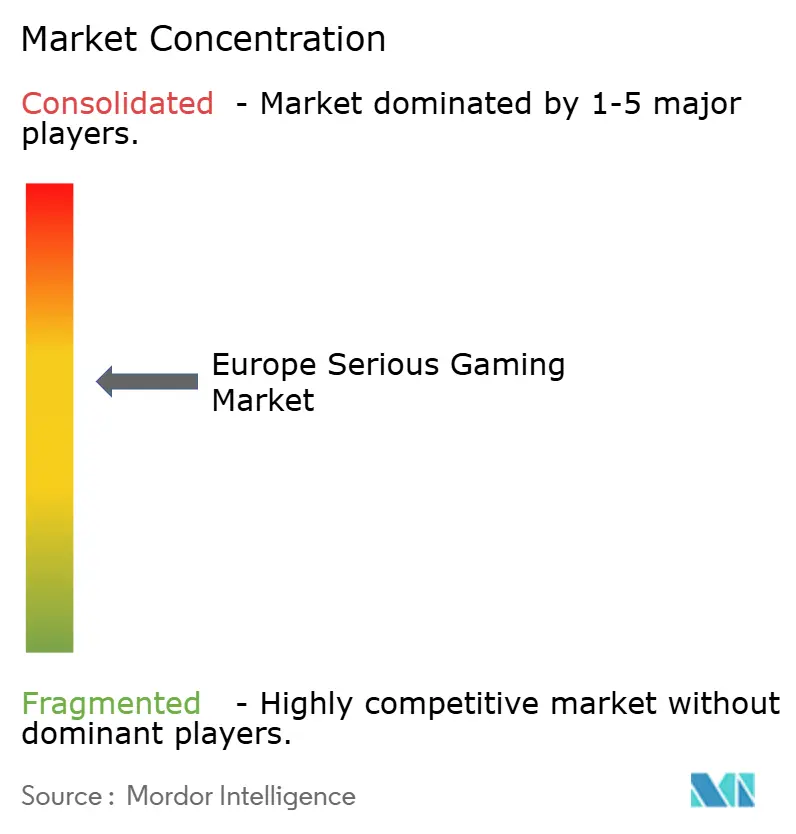

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Serious Gaming Market Analysis by Mordor Intelligence

The Europe serious gaming market size stood at USD 7.73 billion in 2026 and is projected to reach USD 17.63 billion by 2031, delivering a 17.93% CAGR over the forecast period. Digital skills policy funding, falling VR headset prices, and measurable learning outcome data are accelerating adoption across enterprises, healthcare networks, and public education systems. Corporate upskilling has taken center stage as manufacturers retrain technicians for electric-vehicle maintenance, while hospitals integrate simulation into clinician certification. GDPR compliance demands are reshaping platform architecture toward a privacy-by-design approach, yet the regulatory focus simultaneously deters monetization schemes that blur the line between training and entertainment. Competitive dynamics favor vendors that localize into the European Union’s 24 official languages, integrate with learning-management systems, and secure accreditation body endorsements, positioning them to capture larger slices of the Europe serious gaming market.

Key Report Takeaways

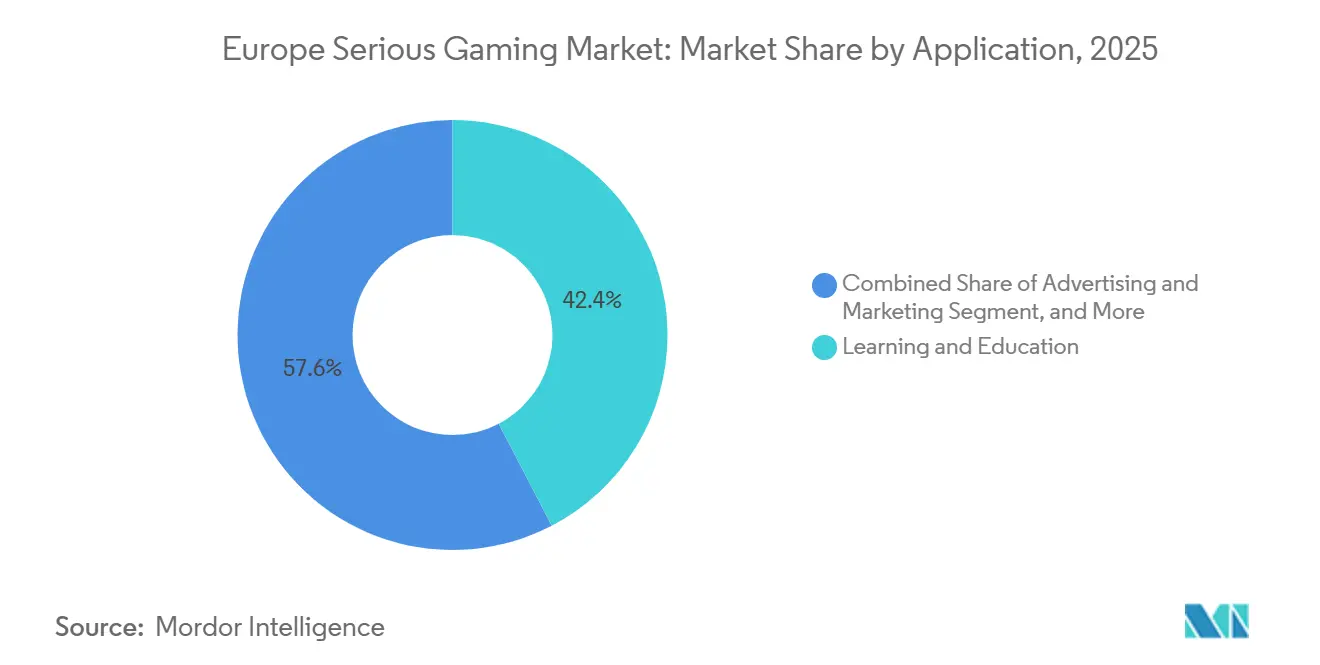

- By application, Learning and Education led the Europe serious gaming market with 42.36% of the market share in 2025, while Advertising and Marketing is forecast to expand at an 18.76% CAGR through 2031.

- By end-user industry, Education accounted for 34.21% of revenue in 2025, whereas Healthcare is advancing at a 19.32% CAGR to 2031.

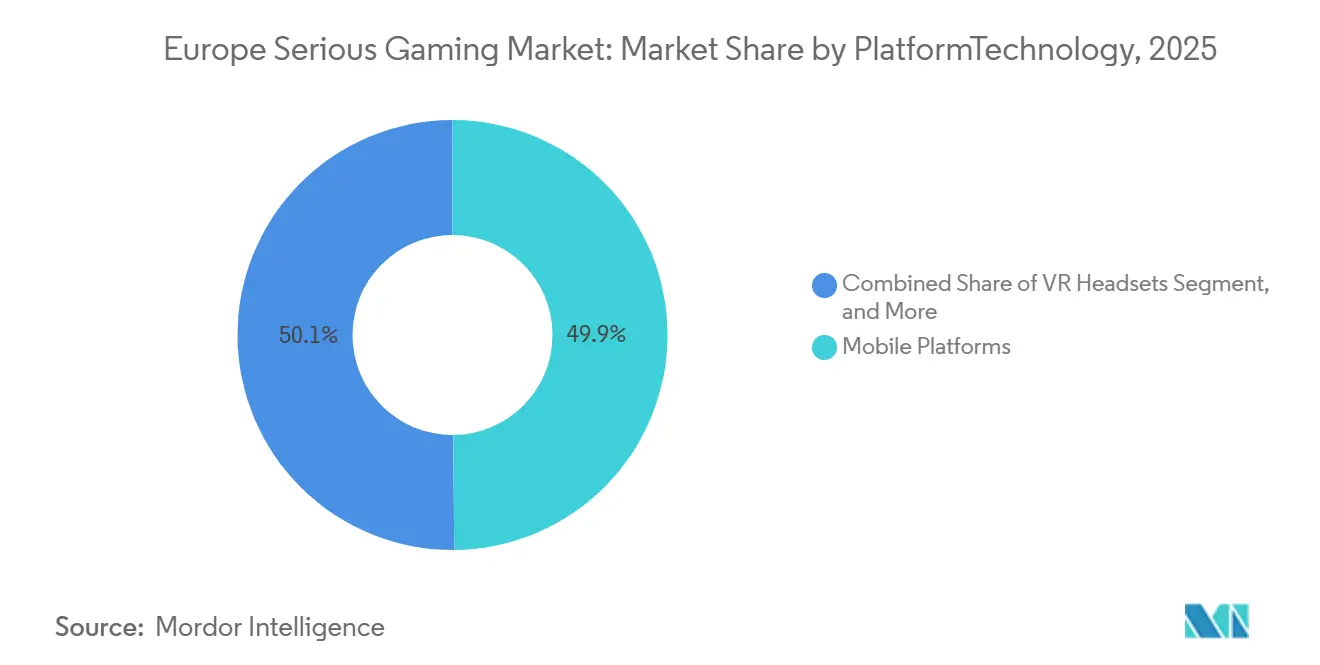

- By platform, mobile captured a 49.87% share in 2025, and VR headsets are set to grow at an 18.94% CAGR over the same horizon.

- By age group, children in K-12 held 38.62% of users in 2025, but adults aged 31-60 are expected to scale at an 18.69% CAGR.

- By country, the United Kingdom contributed 24.59% of 2025 revenue, and Germany is poised for a 19.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Serious Gaming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing usage of mobile-based educational games | +3.2% | United Kingdom, Germany, France | Short term (≤ 2 years) |

| Improved learning outcomes driving adoption among enterprises and educational institutions | +4.1% | Germany, United Kingdom, France, Netherlands | Medium term (2-4 years) |

| Proliferation of affordable VR and AR hardware | +3.8% | Germany, United Kingdom, Sweden, Netherlands | Medium term (2-4 years) |

| Government initiatives promoting digital skills and gamified learning | +3.5% | France, Germany, United Kingdom, Spain | Long term (≥ 4 years) |

| Integration of serious games with learning management systems for data analytics | +2.1% | United Kingdom, Germany, Netherlands, Sweden | Medium term (2-4 years) |

| Growing demand for gamified cybersecurity training in European SMEs | +1.2% | Germany, France, Netherlands, United Kingdom | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Usage of Mobile-Based Educational Games

Mobile platforms secured 49.87% of revenue in 2025, underscoring their affordability and ease of deployment for schools in budget-constrained regions. Smartphones sidestep IT procurement delays, allow for asynchronous learning, and enable fast localization through modular asset libraries. Multilingual titles such as the Joint Research Centre’s Happy Onlife reach pan-European audiences without recoding. Bring-your-own-device policies in secondary schools further expand mobile reach, although parental consent thresholds under GDPR vary from 13 to 16 across member states. Public funding in France’s Digital Decade roadmap, amounting to EUR 2.5 billion (USD 2.75 billion), specifically prioritizes mobile-first programs that serve rural learners.[1]French Government, “National Plan for Digital Inclusion,” gouvernement.fr

Improved Learning Outcomes Driving Adoption Among Enterprises and Educational Institutions

Return-on-investment evidence is converting pilots into budget-line staples. Play it Secure reported training completion four times faster and 30% fewer infringements after deployment in European firms.[2]Play it Secure, “Gamified Cybersecurity Training Results,” playitsecure.com NHS England’s Becoming Simulation Faculty Program embedded immersive modules that cut adverse events in high-acuity wards. OECD research has linked action games to improved spatial reasoning, providing policymakers with empirical evidence to support edtech grants. Germany’s broadband build-out is expected to connect 43,000 schools by 2025, creating device-ready classrooms where serious games can integrate smoothly.

Proliferation of Affordable VR and AR Hardware

Meta reduced the Quest 3S launch price to USD 299 in October 2024, slicing the entry cost for SMEs by 40%.[3]Meta, “Quest 3S Pricing,” meta.com Pico followed with the EUR 1,299 (USD 1,430) Pico 4 Enterprise, which bundles device-management tools and appeals to data-sensitive corporates. Public research grants, such as the EUR 80 million (USD 88 million) Virtual Human Twins initiative, bankroll clinical-simulation content that exploits these devices. Automotive OEMs deploy headsets to train technicians on high-voltage battery systems, eliminating the risk of physical inventory loss.

Government Initiatives Promoting Digital Skills and Gamified Learning

The Digital Europe Programme earmarked EUR 580 million (USD 638 million) for skills training, with EUR 1.3 billion (USD 1.43 billion) specifically for AI and cybersecurity between 2025 and 2027. National agendas amplify this push: France’s inclusion plan has trained 1.5 million citizens, the United Kingdom’s Digital Inclusion Action Plan channels donated devices into community centers, and Germany’s roadmap aims for 80% digital skills penetration by 2030. Funding criteria increasingly favor products aligned with European Qualifications Framework levels, steering procurement toward accredited serious-game vendors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack of standardized assessment tools to measure effectiveness | -1.8% | Germany, United Kingdom, France | Long term (≥ 4 years) |

| High development costs for high-fidelity content | -2.3% | Germany, United Kingdom, France, Sweden | Medium term (2-4 years) |

| Concerns over data privacy compliance in gamified platforms (GDPR) | -1.5% | European Union member states, United Kingdom | Short term (≤ 2 years) |

| Limited multilingual content hindering cross-border adoption | -1.1% | European Union member states, Switzerland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lack of Standardized Assessment Tools to Measure Effectiveness

Procurement teams struggle to benchmark vendors because there is no ISO-like metric that directly links gameplay to on-the-job competence. Proprietary dashboards track quiz scores yet seldom correlate with patient safety or production quality indicators. Switching providers can require recalibrating entire analytics frameworks, locking institutions into legacy platforms. The European Research Institute on Simulation received EUR 1 million (USD 1.1 million) in April 2025 to craft cardiac-training protocols, but its narrow scope underlines the broader gap.

Concerns Over Data Privacy Compliance in Gamified Platforms (GDPR)

The Children’s Code requires age-appropriate design, default geolocation to be off, and profiling to be disabled unless it is clearly beneficial. These safeguards restrict the behavioral telemetry that adaptive algorithms use to personalize difficulty. Fines totaling EUR 4.2 billion since 2018 underscore enforcement intensity, pushing smaller studios to allocate scarce capital toward legal audits rather than content innovation. The Digital Services Act’s ban on profiling-based ads to minors mandates reengineering of monetization loops built around loot boxes and dark patterns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Corporate Training Outpaces K-12 Adoption

Learning and Education dominated the Europe serious gaming market with 42.36% revenue in 2025. Corporate advertisers, however, are accelerating; their segment is projected to register an 18.76% CAGR as interactive storytelling sidesteps ad blockers. Simulation Training spans Healthcare, automotive, and aerospace, garnering recurring revenue from mandatory recertification cycles. Other applications, such as logistics and emergency response, rely on scenario-based drills that reduce the costs of live exercises.

Advertising and Marketing growth pivot on emotional engagement. Campaigns like “Lost in the World,” a Fortnite-based Alzheimer’s simulator, reached Gen Z users who ignore banner ads, validating sponsor investment. Simulation Training gains regulatory ballast, with NHS England’s procurement framework guaranteeing pipeline demand. Bundling analytics that feed compliance reports into learning-management systems bolsters enterprise traction across the Europe serious gaming market.

By End-User Industry: Healthcare Surges on Clinical-Simulation Mandates

Education retained the largest slice at 34.21% in 2025; however, Healthcare is on track for a 19.32% CAGR through 2031 as accreditation bodies integrate simulation into curricula. Automotive players are leveraging gamified modules to retrain staff on electric-vehicle powertrains. Retail adoption remains modest due to slim training budgets, but luxury brands test virtual showrooms. Government agencies conduct cybersecurity and emergency-response drills to protect critical infrastructure.

Healthcare momentum is illustrated by Vall d’Hebron Barcelona Hospital teaming with the Cleveland Clinic to pilot ultrasound simulators that eliminate patient risk. The Europe serious gaming market size for Healthcare alone is projected to rise sharply as trusts tap the NHS procurement system. Automotive gains scale through Valeo’s Tech Academy, which delivers certified modules across five countries, evidencing cross-border scalability once content aligns with industry standards.

By Platform/Technology: VR Headsets Gain as Prices Collapse

Mobile remained the volume leader with a 49.87% share in 2025, favored for its zero-install convenience and ready distribution. The VR sub-segment, however, is forecast for an 18.94% CAGR as headset prices fall below USD 300 and enterprise software ecosystems mature. PC and console products are well-suited for high-precision simulations, such as neurosurgery or flight operations. AR and MR devices stay niche pending cost reductions and broader app portfolios. Cloud or web-based delivery appeals to multinational firms seeking centralized version control.

Meta’s aggressive pricing, combined with on-premises deployment modes for GDPR-sensitive data, accelerates enterprise uptake. Pico’s multi-user licensing offsets higher sticker prices with fleet-management efficiencies. Cloud rendering minimizes local hardware demands, but latency constraints keep delicate surgical use cases tethered to powerful PCs. As vendors fold analytics into their stacks, platform choice increasingly hinges on integration ease rather than raw graphics performance, reshaping competitive positioning within the Europe serious gaming market.

By Age Group: Mid-Career Reskilling Drives Adult Segment

Children in K-12 commanded a 38.62% user share in 2025, consistent with compulsory digital literacy curricula. Adults aged 31-60 are forecast to post an 18.69% CAGR as employers finance reskilling in cybersecurity and electric-vehicle maintenance. Young adults in university or early career stages engage in capstone simulations through business and engineering programs. Seniors above 60 remain a niche market, limited by interface familiarity and vision constraints, although cognitive-health titles show promise.

Valeo’s Tech Academy targets technicians aged 30-55 who are trained on combustion engines and now require high-voltage certification. CyberALARM offers multilingual cybersecurity scenarios suited to SMEs, expanding adult uptake in the Netherlands, Germany, and France. Universities deploy Cesim’s business-strategy games to teach supply-chain optimization, thereby reinforcing young adult engagement. National digital-inclusion programs in France and Spain include senior-friendly modules that could unlock latent demand once usability hurdles fall.

Geography Analysis

The United Kingdom captured 24.59% of the 2025 revenue, anchored by early adoption of the National Health Service simulation and a robust edtech startup scene. Germany is projected to deliver a 19.21% CAGR through 2031, propelled by automotive retraining programs and federal broadband targets that create a ready digital infrastructure. France benefits from EUR 2.5 billion in Skills and Jobs investment, sustaining a developer cluster in Paris and Lyon.

Southern markets are gaining momentum through European Union structural funds, with Spain hosting healthcare-simulation pilots at Vall d’Hebron Barcelona Hospital and promoting public-health campaigns within commercial game engines. The Netherlands punches above its weight due to high English proficiency and a logistics-heavy economy that values scenario planning. Sweden leverages a deep pool of entertainment and gaming talent to export serious-game expertise across Europe.

The rest of Europe, including Belgium, Poland, and the remaining Nordic countries, taps into co-funded procurement schemes. Poland’s inclusion in Valeo’s Tech Academy highlights Eastern Europe’s dual role as both a development hub and an end-market. Italy focuses on virtual-surgery pilots to mitigate rural surgeon shortages. Regional diversity in language and policy underscores why localization and compliance fluency remain critical competitive levers across the Europe serious gaming market.

Regulatory Landscape

Regulation of serious gaming in Europe is shaped by digital-platform and consumer-protection rules that apply when games operate as hosting services, distribute user-generated content, or process learner data. The EU Digital Services Act (Regulation (EU) 2022/2065) raises requirements around transparency, platform accountability, and protections for minors. This reinforces a privacy-by-design approach and age-appropriate experiences for education and healthcare deployments. Co-regulation continues to matter for content and advertising suitability through PEGI, which is frequently used as the practical labeling mechanism across European markets.

In 2026, the European Commission signaled a preference for stakeholder engagement over new hard-law obligations when it announced it would not proceed with a legal requirement to keep video games playable after support ends, following a European Citizens Initiative. At the policy level, the EU Work Plan for Culture (2023-2026) highlights the video game sector and frames priorities around European values, safeguarding vulnerable groups (including minors) and supporting SME competitiveness. This, in turn, influences how public programs assess procurement, state-aid alignment, and responsible design expectations for serious game vendors.

Value Chain Analysis

The Europe serious gaming value chain spans (1) knowledge and content inputs (subject-matter experts from healthcare, education, and enterprise training, alongside academic partners), (2) technology layers (game engines, analytics, cloud hosting, identity and access, and device-management for mobile and VR fleets), and (3) solution development and integration (studios building modules, multilingual localization, and connectors into learning-management systems and compliance reporting). Collaborative ecosystems such as the RAGE Project have acted as an applied-gaming repository and community linking developers and researchers, supporting reuse of components and accelerating prototyping for workforce development use cases.

Distribution and deployment are primarily digital (enterprise LMS marketplaces, direct-to-institution procurement, and app stores for mobile-first programs), with a supporting services layer for hardware and media logistics where required. Companies that support gaming supply chains and fulfillment, such as Taurus Europe B.V. for gaming components and inventory management and Conectiv for gaming media manufacturing and fulfillment services (packaging, kitting, and point-of-sale materials), illustrate the operational backbone behind device-led rollouts and large institutional launches. Key bottlenecks remain high-fidelity content costs, GDPR-aligned data handling, and the effort of scaling across Europe through localization into the EU's 24 official languages.

Competitive Landscape

The market is moderately fragmented, with no firm exceeding 10% share. Ubisoft’s Serious Games Division leverages blockbuster intellectual property to secure healthcare and defense contracts, yet specialized boutiques such as SimforHealth capture niche depth. Tencent’s EUR 1.16 billion (USD 1.28 billion) stake in Ubisoft’s Vantage Studios underscores Asian interest in regulated European sectors. Meanwhile, Gamelearn scales corporate soft-skills titles using cloud delivery and pay-per-learner models, chipping away at perpetual-license incumbents.

Strategic themes include vertical integration into learning management systems, Eastern European expansion driven by European Union grants, and partnerships with accreditation bodies to integrate game hours into mandatory licensing. Valeo’s Tech Academy, certified by the Institute of the Motor Industry and Qualiopi, exemplifies how credential alignment accelerates multi-country rollouts. Vendors differentiate through adaptive algorithms, multiplayer collaboration modes, and privacy-by-design architectures that navigate GDPR scrutiny.

Language localization remains a significant cost barrier; only well-capitalized firms can translate into all 24 official languages of the European Union. Open-source connectors for Moodle erode switching costs, enabling institutions to pilot multiple vendors. Studios that cannot fund compliance audits face procurement headwinds, reinforcing the scale advantages of larger players while leaving white space for federated open-source platforms within the European serious gaming market.

Europe Serious Gaming Industry Leaders

Breakaway Games, Ltd.

Designing Digitally Inc.

Diginex Limited

MPS Interactive Systems Limited

Serious Games Solutions

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is concentrated in evidence-based serious games that map gameplay outputs to recognized competency frameworks and institutional assessment needs, reducing the procurement friction created by non-standardized effectiveness metrics. EU-funded research and education programs provide a visible pipeline for new content and evaluation methods. In July 2026, the European Commission (CORDIS) published a Results Pack highlighting 10 EU-funded projects using serious gaming across education, healthcare, and research, and Open Research Europe has published evaluations including the ERASMUS+-developed SG4NS serious game focused on emotional competence in nursing students. This creates room for vendors that can operationalize validated outcomes into dashboards compatible with learning-management systems and accreditation documentation.

Healthcare and care-pathway adherence represent another opportunity area, where serious games extend beyond training into patient support, including rehabilitation and cognitive training. This direction is reflected in 2026 academic literature on serious video games in healthcare. Cross-border, multi-country interventions also broaden addressable demand for localized content and teacher tooling, as shown by the EU-funded SEL4@ll program that commenced in January 2026 across Germany, Spain, Italy, and Finland for socio-emotional competencies in school students. Technical whitespace sits in privacy-preserving analytics for minors and sensitive health data, sensor-based motion control for rehabilitation scenarios, and co-creation toolchains that help institutions participate in content design while keeping measurable goals and user needs at the center.

Recent Industry Developments

- June 2026: Diginex announced an expanded end-to-end supply chain due diligence suite by integrating Risk-to-Remedy capabilities across its LUMEN risk assessment platform and APPRISE engagement tool, leveraging the expertise it added via The Remedy Project. The move strengthens audit-ready compliance workflows and positions the company to package training and operational decision support around evolving due-diligence requirements.

- December 2025: Ubisoft highlighted Europe as a major contributor to its net bookings during the period, coinciding with Tencent's EUR 1.16 billion equity investment tied to Ubisoft's Vantage Studios. The investment reinforced capital availability for large-scale content development and increased competitive pressure on smaller serious-game studios to differentiate via accreditation alignment and localization.

- October 2024: Meta reduced the Quest 3S launch price to USD 299, lowering the entry cost for VR-based training and simulation deployments. The price reset broadened the feasible buyer set for immersive serious games across SMEs and institutions, accelerating pilots that depend on scalable headset fleets and device-management readiness.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues generated in Europe from serious games that are designed mainly for learning, training, simulation, or behavior change, delivered through software across mobile, PC/console, and immersive platforms, and used by organizations and consumers.

Scope exclusions: We exclude pure entertainment games with no learning or training intent, and we also exclude general hardware sales unless bundled as part of a serious gaming deployment.

Segmentation Overview

- By Application

- Advertising and Marketing

- Simulation Training

- Learning and Education

- Other Applications

- By End-User Industry

- Healthcare

- Education

- Retail

- Media and Entertainment

- Automotive

- Government

- Other End-User Industries

- By Platform/Technology

- Mobile Platforms

- PC and Console

- VR Headsets

- AR/MR Devices

- Cloud/Web-Based

- By Age Group

- Children (K-12)

- Young Adults (18-30)

- Adults (31-60)

- Seniors (Above 60)

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Sweden

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the demand pool and the policy and funding environment that shapes adoption across Europe. We review public sources such as Eurostat ICT and education statistics, European Commission digital skills programs, OECD education indicators, and WHO and national health service publications where training and simulation needs are discussed. For software and content supply signals, we also use sources such as EPO patent search outputs, app store category descriptions and public rankings, and academic journals that report outcomes from serious game use in learning and clinical simulation.

After that, we use company filings, annual reports, investor presentations, developer websites, and trusted press to understand typical delivery models, pricing logic, and partnership patterns. Select paid subscriptions are used only for company financials and news intelligence, and for patent database screening when we need to validate product claims. The sources listed here are illustrative, and many other public and proprietary references were also reviewed to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work is used to confirm what "serious gaming spend" looks like in real buying situations, and to check how platforms like mobile, PC/console, VR headsets, AR/MR devices, and cloud delivery are actually being deployed. We speak with a mix of game studios, platform and tool providers, training and learning teams, and end-user stakeholders across major European countries, and then we re-check any conflicting inputs until the model assumptions align with how budgets are allocated.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 13% | |

| Mid tier: 52% | Functional/Unit leaders: 31% | |

| Smaller Players: 18% | Managers: 56% |

Market-Sizing & Forecasting

Sizing is built using top-down and bottom-up logic, where public spending and activity indicators are first used to reconstruct the addressable pool, and then the totals are checked against selective supplier and channel approximations. In practice, the top-down build starts from Europe-level digital learning and training intensity, simulation adoption in healthcare and safety training, and installed base signals for VR headsets and compatible devices, which are then converted into likely serious gaming usage and spend.

To keep the model grounded, we track a small set of inputs that can be explained and re-tested, such as enterprise training and education digitization rates, procurement cycles in government and healthcare, average project sizes for simulation and learning modules, platform mix shifts between mobile and immersive formats, and localization needs across languages that influence delivery cost. Forecasts are run using scenario analysis, because adoption is sensitive to budget confidence and policy support, and then the scenarios are reconciled with expert views on pipeline visibility and pricing progression. Where bottom-up checks have gaps, missing pieces are handled by using conservative ranges for average selling prices and conversion rates, and those ranges are narrowed only when interview feedback stays consistent across multiple buyer types.

Data Validation & Update Cycle

Model outputs are cross-checked against independent signals such as platform adoption trends, public program funding announcements, and the pace of deployments seen in healthcare and education. Outliers are investigated by revisiting assumptions like platform mix, currency timing, and whether a use case is counted as simulation training or general content. The numbers then move through a second analyst review before sign-off.

The report is refreshed annually, and interim updates are made when material events occur, such as major policy shifts, sudden device price changes, or step-changes in enterprise training budgets. Before delivery, we do a final pass to capture the latest public releases and to re-contact sources if new variances appear, so clients receive an up-to-date view.

Mordor Intelligence's Europe Serious Gaming Market Size Versus Other Published Estimates

Published market sizes for Europe serious gaming can look far apart, even when they describe the same general concept. The differences usually come from how each study defines what counts as a serious game, which years are treated as the base for modeling, and how fast pricing and adoption are assumed to move in training and simulation use cases.

The main gap comes from whether adjacent services and bundled hardware are counted inside the market, where Mordor Intelligence counts only serious gaming revenues tied to defined applications and platforms (mobile, PC/console, VR headsets, AR/MR devices, and cloud/web-based) and avoids folding in unrelated entertainment spend or broad device sales.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.73 B (2026) | |

| Regional Consultancy A | USD 10.00 B (2024) | Uses an earlier base year and a wider spend definition that can pull in adjacent digital training budgets and solution services, which lifts the headline value even before forecasting assumptions are applied. |

| Industry Publisher B | USD 4.73 B (2024) | Appears to apply a narrower product lens that is closer to a serious game software category and may undercount immersive deployments and multi-platform projects, which reduces the total compared with broader serious gaming scopes. |

The table shows that year selection and scope control explain most of the spread, and then growth assumptions do the rest. By keeping inputs tied to observable platform adoption and to practical buying use cases like learning, education, and simulation training, our sizing stays transparent and repeatable without relying on hidden multipliers.

Key Questions Answered in the Report

How fast is the Europe serious gaming market growing toward 2031?

The value is set to rise from USD 7.73 billion in 2026 to USD 17.63 billion by 2031, registering a 17.93% CAGR.

Which application is expanding the most rapidly?

Advertising and Marketing is forecast to post an 18.76% CAGR as brands substitute gamified storytelling for conventional ads.

Why are enterprises prioritizing VR headsets now?

Headset prices dropped below USD 300 in 2024, slashing capital expense and enabling high-fidelity training in smaller budgets.

What keeps some buyers from adopting serious games?

A lack of standardized assessment metrics and strict GDPR consent rules create procurement friction, especially in healthcare and education.

Which country will add the most new revenue by 2031?

Germany is projected for the fastest growth, at a 19.21% CAGR, as automotive OEMs use simulations for electric-vehicle workforce training.

Page last updated on: