Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.82 Billion |

| Market Size (2026) | USD 10.16 Billion |

| Market Size (2031) | USD 12.03 Billion |

| Growth Rate (2026 - 2031) | 3.46% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe E-Book Market Analysis by Mordor Intelligence

The Europe E-Book Market size is expected to grow from USD 9.82 billion in 2025 to USD 10.16 billion in 2026 and is forecast to reach USD 12.03 billion by 2031 at 3.46% CAGR over 2026-2031.

Growth remains moderate in mature Western European economies, yet new momentum is visible in Southern and Eastern Europe, where smartphone adoption and broader language digitisation are still expanding. Subscription platforms are reshaping revenue models, mobile reading is widening the addressable base among younger users, and sustainability goals are accelerating the print-to-digital shift. Meanwhile, regulatory initiatives such as the EU Digital Identity Wallet and harmonized VAT on e-books are lowering cross-border barriers, although piracy, audio-first competition, and new compliance demands continue to temper overall expansion.

Key Report Takeaways

- By content type, fiction led with 34.60% of the European e-book market share in 2025, while children’s literature is poised to expand at a 9.35% CAGR through 2031.

- By device type, smartphones captured 45.40% revenue share in 2025; dedicated e-readers are forecast to grow at an 7.72% CAGR by 2031.

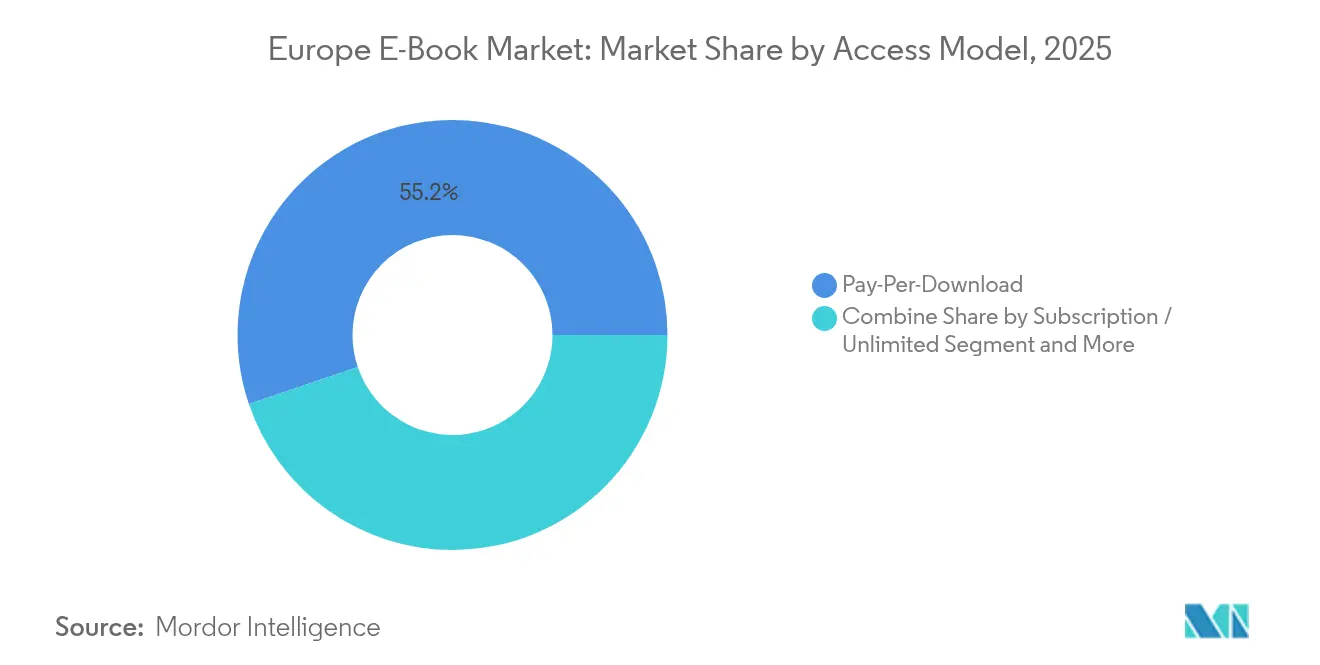

- By access model, pay-per-download accounted for 55.20% of the European e-book market size in 2025, whereas subscription services are advancing at an 10.85% CAGR between 2026-2031.

- By distribution channel, third-party e-retailers held a 61.10% share in 2025, with institutional and library portals registering the fastest 9.76% CAGR over the forecast period.

- By geography, the United Kingdom commanded 50.80% of the European e-book market share in 2025, while Italy is projected to be the fastest-growing country at 11.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe E-Book Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High smartphone & broadband penetration | 0.80% | Western Europe core, expanding to Eastern Europe | Short term (≤ 2 years) |

| EU VAT harmonisation removes fiscal barriers | 0.60% | All EU member states | Medium term (2-4 years) |

| Growth of subscription-based reading platforms | 0.40% | Nordic region leading, spreading EU-wide | Medium term (2-4 years) |

| Publisher digitisation of backlists in native European languages | 0.50% | Germany, France, Italy, Spain | Long term (≥ 4 years) |

| Sustainability goals pushing print-to-digital migration | 0.30% | EU-wide, strongest in Nordic & Western Europe | Long term (≥ 4 years) |

| Accessibility legislation expanding the addressable audience | 0.30% | All EU member states, early uptake in France & Scandinavia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Smartphone and Broadband Penetration Accelerating Mobile Reading in Western Europe

Mobile connectivity has transformed reading habits, with 46% of e-book consumption now taking place on smartphones in 2024.[1]European Commission, “Council Directive 2018/1713 on reduced VAT rates for e-books,” europa.eu Younger readers drive this shift through always-available devices and shorter attention cycles that align with digital formats. Publishers have responded by re-designing titles for smaller screens, ensuring typography and navigation meet mobile expectations. Advertised bundles pairing e-books with telecom plans are also widening reach among first-time digital readers. As 5G coverage deepens, in-app sampling and one-click purchasing further simplify the path from discovery to completed sale, reinforcing the European e-book market’s mobile-centric trajectory.

EU VAT Harmonisation Removing Fiscal Barriers to Digital Publishing

Equalised VAT treatment between print and digital books has eliminated a cost handicap that once constrained online price flexibility. French and German publishers now experiment with limited-time discounts and loyalty incentives previously restricted under fixed-price regulations. Subscription services benefit most, using the margin headroom to lower monthly fees while sustaining author royalties. Together with wider language catalogues, this fiscal shift lifted German e-book revenues by 5.2% in 2023 and set a precedent other markets quickly followed, supporting steady enlargement of the European e-book market.

Surge of Subscription-Based Reading Platforms Boosting Recurring Revenue Streams

Storytel booked SEK 3.489 billion (USD 336 million) in 2024 sales, proving that flat-rate reading resonates across borders. BookBeat’s 28% revenue jump and 70% international mix highlight the scalability of the model. Subscriptions give consumers low-risk discovery and promote deeper backlist monetization. Publishers exchange some control over pricing for stable cash flows and wider audience reach, especially among digital-native readers who treat content as a service.

Publisher Digitization of Backlists in Native European Languages

Projects such as France’s ReLIRE are converting out-of-print titles into digital editions, opening fresh revenue channels from dormant IP. Local-language backlists help regional platforms differentiate against English-heavy global catalogs. While upfront costs for scanning, formatting, and metadata are significant, long-tail revenues accumulate once titles join subscription or library platforms. These efforts also align with EU cultural preservation goals, adding public funding support for digitization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rampant e-book piracy & illegal file-sharing | –0.4% | EU-wide, acute in Eastern Europe | Short term (≤ 2 years) |

| Strong competition from audio-first formats | –0.3% | Nordic region, Germany, expanding south | Medium term (2-4 years) |

| Fixed book price laws limit discount flexibility | –0.2% | Germany, Austria, Switzerland, France | Long term (≥ 4 years) |

| Multi-layered regulatory compliance costs | –0.1% | All EU member states, heavier load on small houses | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Competition from Audio-First Formats such as Podcasts & Audiobooks

Rising audio engagement siphons discretionary time from e-book reading, with Nordic audiobook share estimated at 4-5% of the total book market. Major platforms lure authors with exclusive production budgets and voice-talent marketing, prompting e-book publishers to launch simultaneous text-audio releases. While multi-format strategies hedge risk, they also raise cost structures, adding pressure to maintain margin within the European e-book market.

Rampant E-Book Piracy and Illegal File-Sharing Networks Across EU

The European Union Intellectual Property Office notes widespread unauthorized distribution that erodes publisher margins, especially in high-value educational and professional segments. Eurojust’s 2024 study flags inconsistent national enforcement that pirates exploit.[2]European Union Intellectual Property Office, “The State of Online Piracy and Copyright Infringement in Europe,” euipo.europa.eu Rights holders intensify takedown requests and site blocking, but decentralized networks remain resilient, shaving points from the European e-book market’s potential CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Content Type: Fiction Dominates While Children’s Literature Surges

Fiction remained the revenue cornerstone in 2025, holding a 34.60% share of the European e-book market. Genre series release schedules and community marketing energise frequent purchases that sustain digital traction. The segment benefits from readers’ willingness to embrace auto-buy functions inside subscription apps, reinforcing volume. Children's literature, though still smaller, is the fastest climber at a 9.35% CAGR for 2026-2031, propelled by interactive enhancements that align with tablet use among families. Enhanced read-aloud features, embedded games and parental analytics differentiate digital from print, supporting premium pricing.

Educational shifts during pandemic lockdowns normalised screen-based reading for younger age groups and eased educator concerns about efficacy. Publishers pivoted by securing multimedia rights and collaborating with ed-tech partners to integrate curriculum alignment. The September 2024 appellate decision upholding restrictions on controlled digital lending clarified digital rights management boundaries, encouraging rights holders to increase children’s backlist conversions. Together, these factors expand the European e-book market size for youth titles and diversify revenue beyond traditionally dominant fiction lines.

Device Type: Smartphones Lead While E-Readers Show Surprising Resilience

Smartphones captured 45.40% of consumption devices in 2025, underpinned by widespread 4G/5G coverage and habit-forming quick reads during commutes. Publishers now design responsive layouts and compress download packages to meet data-cap sensitivities. Push notifications on reading milestones enhance engagement rates, directly influencing lifetime value within the European e-book market.

Dedicated e-readers, once considered niche, show renewed appeal with an 7.72% forecast CAGR as e-ink colour, front-lighting, and extended battery life address past limitations. Older readers, 53% of whom prefer e-readers for eye comfort, drive this resurgence. New EU cybersecurity requirements for digital products, effective November 2024, elevate the baseline resilience of devices. Compliance costs may squeeze smaller hardware makers yet reinforce consumer trust, supporting sustained hardware replacement cycles that indirectly fuel e-book sales.

Access Model: Subscription Services Challenging Pay-Per-Download Dominance

Pay-per-download held 55.20% of the European e-book market size in 2025, sustained by long-standing storefront habits and instant ownership appeal. Nevertheless, subscription services are scaling at 10.85% CAGR, signaling the appetite for flat-fee consumption models. Power users valuing breadth shift to subscriptions to manage cost, while casual readers remain attached to single-purchase flexibility.

Storytel’s availability in 26 European countries illustrates how unified subscription interfaces traverse language borders, helping smaller language markets achieve discovery parity. The EU Digital Services Act, which imposes new transparency and content responsibility rules, favors platforms with robust compliance infrastructure. Larger players leverage this barrier to scale, likely accelerating consolidation inside the European e-book market.

Distribution Channel: Institutional Portals Gaining on E-Retailers

Third-party e-retailers retained a 61.10% share in 2025 by blending frictionless checkout with recommendation engines and bundling options. Nonetheless, institutional and library portals are projected to grow at 9.76% CAGR as public libraries expand digital licences and universities replace print reserves with electronic access. Library-first acquisition models, such as simultaneous use or short-term loan, attract publishers by balancing exposure and revenue predictability.

The EU Digital Operational Resilience Act (DORA), effective January 2025, introduces stringent uptime and security obligations on any platform processing financial transactions, including e-book sales channels. Well-capitalised vendors can invest in compliance systems, positioning institutional portals as trusted nodes for high-volume academic transactions and boosting their share of the European e-book market.

Geography Analysis

The United Kingdom sustained its leadership with 50.80% of the European e-book market share in 2025, reflecting mature digital infrastructure, high e-reader penetration and the English language’s broad appeal. Local publishers leverage Amazon’s extensive Kindle ecosystem and diversified subscription products to reach urban professionals. Post-Brexit regulatory divergence introduces additional documentation for cross-border rights transfers, yet UK consumers continue to prioritise digital convenience. The EU Digital Identity Wallet, operational across member states, now offers frictionless authentication for EU users, potentially widening usability gaps for UK-centric platforms .

Italy is the fastest-expanding territory with an 11.35% forecast CAGR through 2031. The surge stems from aggressive digitisation of Italian-language backlists and rising smartphone penetration that lowers hardware entry barriers. Marketing collaborations between telcos and publishers bundle data plans with reading app credits, enhancing visibility among first-time e-book buyers. Cultural festivals increasingly feature digital author events, maintaining momentum as physical store footfall recovers.

Germany represents a pivotal, highly regulated battlefield. E-book revenue reached USD 523 million in 2023, accounting for 6.1% of the national book market. Fixed book pricing restricts deep discounting yet provides margin stability, compelling publishers to differentiate via exclusive early-access chapters and AI-generated reading aids. After a 5.2% sales uptick in 2023, growth hinges on converting occasional buyers around 3 million in number into heavier digital users. Consistent catalogue enrichment and VAT parity continue to strengthen prospects across the European e-book market.

Competitive Landscape

Competition is bifurcated between global technology platforms and regional specialists. Amazon’s Kindle remains dominant in the UK and Germany, complemented by seamless hardware-content integration. German consortium Tolino counters through alliances with local booksellers and publishers, providing an alternative ecosystem that secures market share among nationalistic consumers. Subscription-first firms such as Storytel and BookBeat differentiate with original productions, curated lists and family plans that reinforce loyalty. BookBeat’s 2023 expansion into 24 new European markets signals an escalating contest for continental scale.

Educational and professional niches present white-space opportunities. Specialist vendors build platforms that combine workflow tools with DRM-protected texts, aligning with institutional procurement policies. Blockchain pilots supported by the EU Markets in Crypto-assets Regulation (MiCA) explore transparent royalty tracking, though mainstream adoption remains nascent.

Artificial intelligence forms the next competitive front. Publishers invest in AI-driven discovery while safeguarding IP under new EU regulations. Ongoing litigation over training data will determine cost structures for machine-learning innovation. Firms that balance compliant AI with audience personalisation stand to capture greater share of the European e-book market.

Europe E-Book Industry Leaders

Amazon.com Inc.

Rakuten Kobo Inc.

Apple Inc. (Apple Books)

Alphabet Inc.

Tolino Media GmbH & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: French publishers filed a landmark copyright lawsuit against Meta over AI training practices

- February 2025: The EU Digital Operational Resilience Act (DORA) became effective, imposing strict infrastructure standards on e-book platforms

- December 2024: The General Product Safety Regulation came into force, expanding compliance obligations for digital content products

- November 2024: Regulation 2024/2847 introduced cybersecurity requirements for devices with digital elements, including e-readers

Europe E-Book Market Report Scope

An E-Book, or electronic book, is a text that is presented in digital format. This text remains non-editable, and the user needs an electronic device like a smartphone, tablet, or desktop to read this displayed text. These e-books can be accessed through multiple devices, most downloadable. From the author's perspective, e-books reduce production costs as they are not required to be printed. Portability and surging internet demand are favoring the e-books business.

The Europe e-books market is segmented by content type (professional, educational, general), device type (smartphone, tablet) and geography (Germany, United Kingdom, France, Spain, Russia, Italy, Netherlands, Poland, Rest of the Europe) The market sizes and forecasts are provided in terms of value (USD).

By Content Type

| Professional / Technical |

| Educational & Academic |

| Fiction |

| Non-Fiction |

| Childrens Literature |

| Comics & Graphic Novels |

| Other Genres |

By Device Type

| Smartphone |

| Tablet |

| Dedicated E-Reader |

| Laptop / Desktop |

| Other Devices |

By Access Model

| Subscription / Unlimited Reading |

| Pay-Per-Download |

| Free / Ad-Supported |

By Distribution Channel

| Direct Publisher Platforms |

| Third-Party E-Retailers |

| Institutional & Library Portals |

By Geography

| Germany |

| United Kingdom |

| France |

| Spain |

| Russia |

| Italy |

| Netherlands |

| Poland |

| Rest of Europe |

| By Content Type | Professional / Technical |

| Educational & Academic | |

| Fiction | |

| Non-Fiction | |

| Childrens Literature | |

| Comics & Graphic Novels | |

| Other Genres | |

| By Device Type | Smartphone |

| Tablet | |

| Dedicated E-Reader | |

| Laptop / Desktop | |

| Other Devices | |

| By Access Model | Subscription / Unlimited Reading |

| Pay-Per-Download | |

| Free / Ad-Supported | |

| By Distribution Channel | Direct Publisher Platforms |

| Third-Party E-Retailers | |

| Institutional & Library Portals | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Russia | |

| Italy | |

| Netherlands | |

| Poland | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size of the European e-book market?

The European e-book market size is USD 10.16 billion in 2026 and is projected to reach USD 12.03 billion by 2031.

Which country holds the largest share in Europe’s e-book sales?

The United Kingdom leads with 50.80% of the region’s e-book revenue in 2025.

How fast are subscription platforms growing compared with pay-per-download?

Subscription services are forecast to rise at an 10.85% CAGR between 2026-2031, while pay-per-download growth is much slower.

Which device category is growing the quickest for digital reading?

Dedicated e-readers are forecast to grow at an 7.72% CAGR thanks to advances in e-ink displays and eye-comfort features.

Why are subscription services gaining ground?

Flat-rate reading bundles lower price barriers for consumers and give publishers predictable recurring revenue, driving an 10.85% CAGR for the model.

Which country shows the strongest growth outlook?

Italy leads with an expected 11.35% CAGR, supported by government digitisation incentives and rapid youth adoption.

Page last updated on: