Africa Entertainment And Telecommunication Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

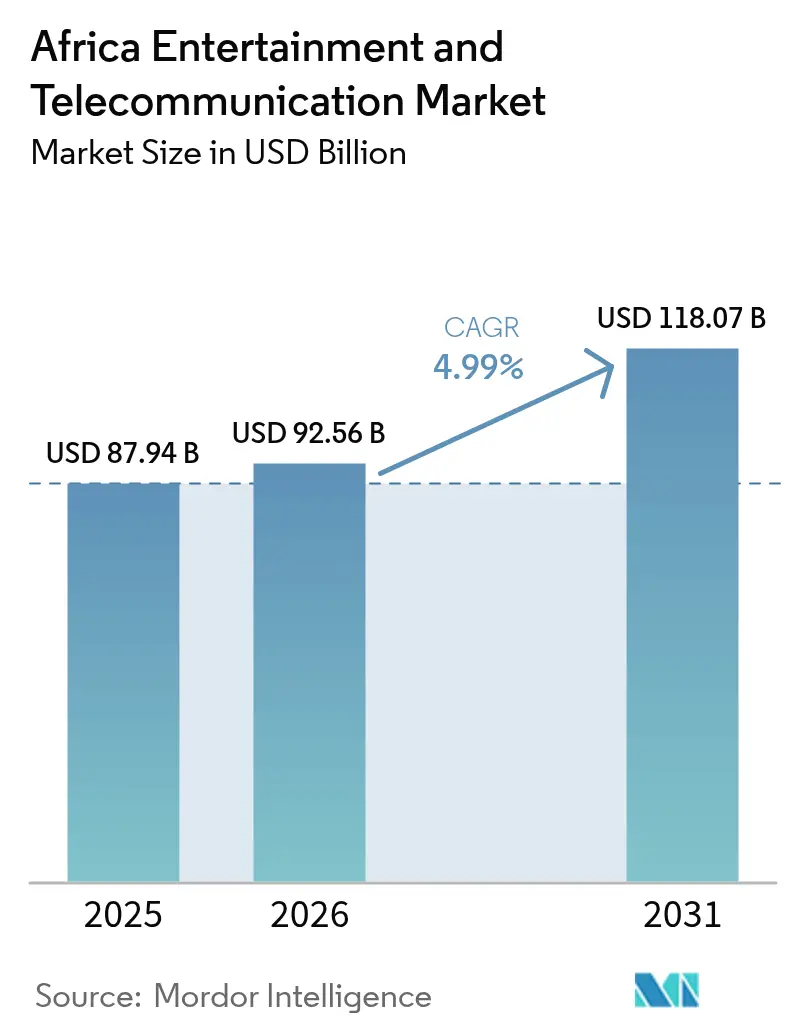

| Base Year Market Size (2025) | USD 87.94 Billion |

| Market Size (2026) | USD 92.56 Billion |

| Market Size (2031) | USD 118.07 Billion |

| Growth Rate (2026 - 2031) | 4.99% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Entertainment And Telecommunication Market Analysis by Mordor Intelligence

The Africa entertainment and telecommunication market size is expected to grow from USD 87.94 billion in 2025 to USD 92.56 billion in 2026 and is forecast to reach USD 118.07 billion by 2031 at 4.99% CAGR over 2026-2031. Robust mobile-first infrastructure, early 5G fixed-wireless access, and low-earth-orbit satellite rollouts collectively widen broadband availability while sidestepping legacy fixed-line constraints. Infrastructure-sharing mandates compress tower capital expenditure, freeing operator cash flow for spectrum acquisitions and network densification. Local-content quotas spur international streaming platforms to finance Nollywood and Afrobeats originals, accelerating data traffic and subscription uptake. Meanwhile, coastal hyperscale data centers reduce latency for cloud gaming and other edge workloads, stimulating premium-speed data bundle sales.

Key Report Takeaways

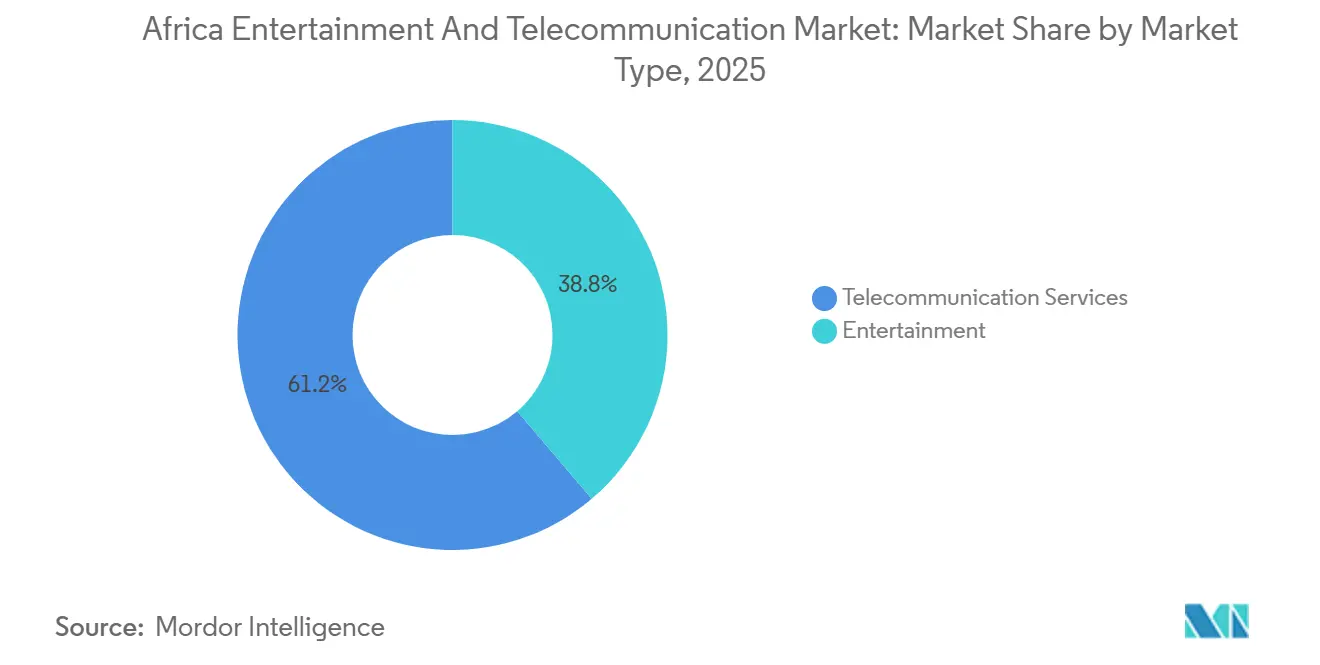

- Telecommunication services led with 61.22% revenue share in 2025, while entertainment is advancing at a 5.67% CAGR through 2031.

- By connectivity technology, 4G and LTE held 46.47% of the Africa entertainment and telecommunication market share in 2025, whereas 5G is the fastest growing layer at 5.45% CAGR to 2031.

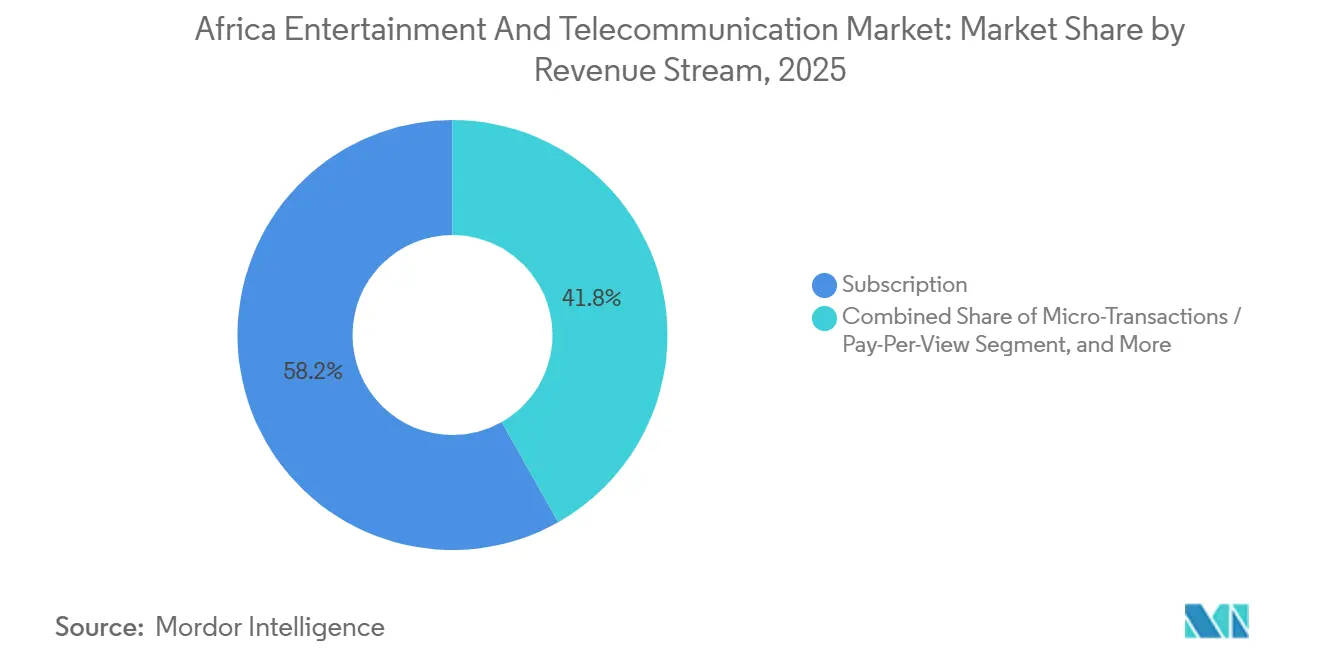

- By revenue stream, subscriptions contributed 58.19% of value in 2025, yet micro-transactions and pay-per-view are projected to expand at 5.94% CAGR between 2026-2031.

- By subscriber category, consumers represented 72.53% of the Africa entertainment and telecommunication market size in 2025, while enterprise accounts are poised for the quickest rise at 5.87% CAGR through 2031.

- By geography, South Africa commanded 26.72% revenue share in 2025, but Nigeria posts the strongest growth trajectory at 5.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Entertainment And Telecommunication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rollout of 5G fixed-wireless access in capital cities | +1.20% | South Africa, Nigeria, Kenya, Egypt, Morocco | Short term (≤ 2 years) |

| Mobile-money-bundled data plans among unbanked youth | +1.00% | East Africa (Kenya, Tanzania, Uganda), West Africa (Nigeria, Ghana) | Medium term (2-4 years) |

| Infrastructure-sharing mandates lowering tower capex | +0.80% | Pan-African, with early adoption in Nigeria, South Africa, Kenya | Medium term (2-4 years) |

| Local-content incentives boosting OTT subscriptions | +0.70% | Nigeria, South Africa, Kenya, Ghana | Medium term (2-4 years) |

| Coastal hyperscale data centers enabling cloud gaming | +0.50% | Nigeria (Lagos), Kenya (Nairobi), South Africa (Cape Town, Johannesburg) | Long term (≥ 4 years) |

| Expansion of low-earth-orbit satellite constellations for rural connectivity | +0.60% | Rural and peri-urban zones across Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Rollout of 5G Fixed-Wireless Access in Capital Cities

Capital deployments of 5G fixed-wireless access supply fiber-like speeds at roughly one-third of last-mile cost. Operators such as MTN South Africa and Safaricom Nairobi marketed unlimited home-broadband plans that undercut local fiber by about 30%.[1]Safaricom PLC, “Annual Report and Financial Statements 2025,” safaricom.co.ke National regulators obligate passive-infrastructure sharing, trimming site acquisition delays and smoothing fast-track rollouts. Because household fixed-line penetration lingers under 1% across most African economies, 5G emerges as the primary household pipe rather than a pure mobile upgrade. The model also pushes legacy internet service providers toward wholesale alignment, deepening operator dominance at the access layer.

Mobile-Money-Bundled Data Plans Among Unbanked Youth

Linking airtime and data purchases to mobile-wallet top-ups converts unbanked youths into digital subscribers without credit cards. Platforms such as M-Pesa, Telebirr, and MTN Mobile Money embed frictionless data-bundle menus inside payment apps, slashing acquisition costs and lifting ecosystem stickiness. Agent networks originally designed for cash-in and cash-out activities now double as connectivity storefronts across peri-urban markets. As mobile-money throughput nears the USD 700 billion mark annually, bundled data plans remain a prime lever for prepaid growth, especially where scratch-card distribution is expensive or insecure.

Infrastructure-Sharing Mandates Lowering Tower Capex

Nigeria, Kenya, and South Africa direct operators to co-locate equipment on common masts, reducing per-site capital outlay by roughly 25-30%. Higher tenancy ratios improve tower-company asset returns, luring infrastructure-fund capital and widening rural coverage economics. Lower diesel use at shared sites further trims operating costs and aligns with decarbonization pledges. Cost savings free cash for mid-band spectrum auctions and urban 5G densification, reinforcing a cycle in which lighter balance-sheet stress feeds broader network footprints.[2]GSMA, “Mobile Economy Sub-Saharan Africa 2025,” gsma.com

Local-Content Incentives Boosting OTT Subscriptions

Mandatory quotas require global streaming brands to dedicate 30% of catalog budgets to African productions, triggering a wave of Nollywood and local-language commissions. Regional platforms that already source predominantly domestic content gain licensing leverage, stretching marketing reach without equivalent budget escalation. Subscriber additions quicken where exclusive originals align with national culture and language, while tax rebates on domestic shoots attract foreign studios and upskill local crews. The uplift in creative-sector spending supports a broader digital-economy narrative that underpins steady data-traffic growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Under-sea cable fragility causing backbone outages | -0.90% | West Africa (Nigeria, Ghana, Senegal, Côte d'Ivoire), East Africa (Kenya, Tanzania) | Short term (≤ 2 years) |

| Currency devaluation compressing ARPU in key markets | -0.80% | Nigeria, Egypt, Ghana, Zambia | Medium term (2-4 years) |

| Nollywood and Afrobeats piracy on Telegram channels | -0.50% | Nigeria, South Africa, Kenya, Ghana | Medium term (2-4 years) |

| High 3.5 GHz spectrum fees delaying 5G in Francophone Africa | -0.40% | Francophone West and Central Africa (Senegal, Côte d'Ivoire, Cameroon, Gabon) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Under-Sea Cable Fragility Causing Backbone Outages

Submarine-fiber breaks exposed reliance on single routes when a 2024 failure sidelined 12 nations for three days. Mobile operators throttled video, enterprises lost cloud uptime, and local e-commerce shed over USD 100 million in potential transactions. Slow repair-ship mobilization underscores the need for mesh topologies and redundant landings, yet financing remains constrained. Until additional loops like Equiano and 2Africa fully land, corporate digital-transformation projects face elevated continuity risk.

Currency Devaluation Compressing ARPU in Key Markets

Sharp local-currency falls erode revenue once translated into U.S. dollars, even where nominal local pricing rises. Operators hold substantial U.S.-dollar liabilities for spectrum and equipment, so margin squeeze restrains reinvestment appetite. Frequent bundle repricing stresses subscriber loyalty and accelerates churn toward lower-priced competitors. Volatility also complicates long-range capital planning, nudging firms to hedge at higher cost or delay radio-access modernizations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Market Type: Entertainment Outpaces Legacy Voice Revenue

Entertainment added momentum to the Africa entertainment and telecommunication market size as telecommunication services still accounted for 61.22% of 2025 earnings. Voice revenue slipped to 18% of the telecommunication mix after over-the-top chat apps displaced domestic and international calling minutes. Data now underwrites 68% of operator turnover, mainly from video streaming, social networking, and nascent cloud use. Complementary services such as mobile money and IoT delivered 14% and grow double digits because enterprises demand connected devices for agriculture and logistics.

Subscription video-on-demand held 42% of entertainment receipts in 2025, buoyed by Showmax, Netflix, and IrokoTV, while digital music captured 22% thanks to Boomplay's surging user base. Video gaming secured 18% and gains extra lift from mobile esports, a format well suited to Africa's handset-first habits. E-publishing and digital advertising combined for the residual slice, but both still climb as smartphone adoption widens and print legacy channels migrate online. Collectively, entertainment’s superior 5.67% CAGR confirms a pivot toward content monetization inside the wider Africa entertainment and telecommunication market.

By Connectivity Technology: 5G Gains Despite 4G Dominance

4G and LTE owned 46.47% Africa entertainment and telecommunication market share in 2025, affirming their status as workhorse layers. Yet 5G advances at a 5.45% clip because fixed-wireless packages undercut home fiber while matching speed expectations. Legacy 2G and 3G footprints continue to recede as sub-USD 50 smartphones arrive, freeing spectrum for higher efficiency air interfaces. Satellite broadband’s 3% revenue share may seem minor, but Starlink-driven landmark pricing shifts the competitive calculus in underserved provinces.

By 2025, 29 nations counted at least one active 5G network, and operators tout installation costs roughly one-quarter of fiber deployments, lifting return profiles. Spectrum auctions, however, move at uneven cadence; Francophone reserve prices slow launches and cede mindshare to Anglophone peers. Long-run uptake hinges on smartphone affordability and the regulatory pace at which digital-dividend and 3.5 GHz bands clear for commercial use.

By Revenue Stream: Micro-Transactions Challenge Subscription Bundles

Subscriptions still ruled 58.19% of 2025 inflows, yet consumer behavior skews toward micro-spend as disposable income ebbs and inflation climbs. Daily and weekly prepaid packets align with irregular earnings cycles, unlike postpaid contracts that linger below 10% penetration outside South Africa and Kenya. Advertising-funded apps draw eyeballs but face ad-load tolerance ceilings, prompting content owners to test freemium ladders.

Showmax’s mobile-only tier demonstrates hybrid monetization, with single-title rentals capturing impulse demand while nurturing trialists into repeat payers. Mobile gaming micro-purchases average USD 1.50 but scale on a 120 million-gamer base, illustrating long-tail economics. Wholesale licensing remains niche, yet operators see margin upside in asset-light syndication, especially where regulatory ceilings cap direct pricing power.

By Subscriber Category: Enterprise Adoption Accelerates IoT Deployment

Consumers formed 72.53% of 2025 SIM and subscription lines, undergirded by rising smartphone penetration and 6.2 GB average monthly usage. Prepaid dominates because credit access is limited, making small bundle denominations critical. Enterprises, though smaller in headcount, expand faster and command higher average revenue per connection, pushing the Africa entertainment and telecommunication market size into higher-margin territory.

Small and medium enterprises integrate point-of-sale terminals with mobile wallets, emphasizing affordability, whereas large firms embrace dedicated fiber and private 5G for latency-sensitive industrial automation. IoT links touched 45 million units in 2025, with livestock tracking and fleet telematics leading the pack. Two-factor authentication messaging services also contribute meaningful enterprise revenue, highlighting a diversified corporate ARPU mix.

Geography Analysis

South Africa contributed 26.72% to 2025 turnover, buoyed by mature infrastructure and an 88% smartphone penetration rate. Nigeria, holding 28% share within West Africa, enjoys the highest forward growth at 5.81% CAGR, aligned to its 220 million population and early 5G exploits. Kenya delivered 9% of regional value, leveraging M-Pesa’s ecosystem to bundle connectivity and finance, while Egypt captured 8% but faces forex headwinds that dilute margins despite rapid fiber rollouts.

West Africa collectively generated 38% of the Africa entertainment and telecommunication market size in 2025, thanks to mobile-money prevalence and tower-sharing policies that slash rural build costs. East Africa supplied 22%, led by Kenya’s fintech nexus and Ethiopia’s market liberalization, which dents the former monopoly’s comfort zone. North Africa’s 15% share leans on comparatively stronger fixed-line bases, yet currency pressure tempers capex. Southern Africa, outside South Africa, grows more slowly as smaller economies wrestle with import-price inflation for radio equipment, although satellite broadband introductions in Zambia and Zimbabwe begin narrowing the digital divide.

Urban hubs host edge compute that lowers gaming and enterprise-cloud latency under 50 ms, fortifying premium-data bundle uptake. Rural advancement, meanwhile, pivots on Starlink and allied LEO networks delivering 100 Mbps links at USD 60 monthly, pressuring incumbents to hasten 4G densification before satellite mindshare solidifies.

Competitive Landscape

The top five operators MTN Group, Vodacom, Orange Middle East and Africa, Airtel Africa, and Safaricom command roughly 55% revenue, yielding a moderately concentrated structure. Tower-sharing accords with IHS Towers and American Tower cut rollout costs by near-30%, aiding profitability amid forex volatility. Strategic thrusts revolve around 5G fixed-wireless, mobile-wallet ecosystems, and edge nodes with hyperscalers; Vodacom-Microsoft Azure’s 35 ms latency milestone exemplifies such collaboration.[3]Vodacom Group, “Financial Results 2025,” vodacom.com

Disruptive entrants include Starlink and OneWeb, whose LEO constellations circumvent terrestrial backhaul gaps, and regional content specialists like IrokoTV that leverage local-content rules to win culturally attuned audiences cheaper than global giants. Smaller operators such as Rain focus on data-only propositions that skip voice overhead and emphasize unlimited models. Regulatory reforms such as mandatory infrastructure sharing and spectrum-auction redesign lower financial barriers for green-field aspirants and promote service-based competition rather than pure facilities play.

Patent filings around network slicing, edge orchestration, and fintech-telco convergence signal a shift from hardware-centric expansion to software-driven differentiation. Operators aim to fold cloud services, content, and payments into single-pane-of-glass super-apps, raising switching costs and insulating against over-the-top encroachment. The Africa entertainment and telecommunication market therefore evolves toward vertically integrated digital ecosystems anchored by mobile connectivity.

Africa Entertainment And Telecommunication Industry Leaders

Telkom SA SOC Ltd

Orange Africa & Middle-East

MTN Group

Maroc Telecom SA

Vodacom Group Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: MTN Group announced a USD 500 million program to add 3,000 5G sites across Nigeria, South Africa, and Ghana, targeting 60% population coverage before year-end 2026.

- December 2025: Vodacom Group acquired a 30% stake in Community Investment Ventures Holdings for USD 180 million, securing 1.2 million additional fiber connections.

- February 2025: Canal+ restructured its MultiChoice acquisition, creating an independent LicenceCo to meet South African media-ownership rules.

- November 2025: Safaricom PLC activated commercial 5G service in four Kenyan cities, pricing unlimited data at KES 2,999 (USD 23).

Africa Entertainment And Telecommunication Market Report Scope

The Africa Entertainment and Telecommunication Market Report is Segmented by Market Type (Telecommunication Services, Entertainment), Connectivity Technology (2G, 3G, 4G/LTE, 5G, Satellite Broadband), Revenue Stream (Subscription, Advertising-Funded, Micro-Transactions/Pay-Per-View, Licensing and Wholesale), Subscriber Category (Consumer, Enterprise), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Telecommunication Services | Voice (Fixed And Mobile) | |

| Data (Fixed And Mobile) | ||

| Other Telco Services (IoT, Messaging) | ||

| Entertainment | Digital Music | Download |

| Streaming | ||

| Video Games | ||

| Video-On-Demand | Svod | |

| Tvod | ||

| Download-To-Own | ||

| E-Publishing | ||

| Advertising | Newspaper | |

| Magazine | ||

| 2G |

| 3G |

| 4G / LTE |

| 5G |

| Satellite Broadband |

| Subscription |

| Advertising-Funded |

| Micro-Transactions / Pay-Per-View |

| Licensing And Wholesale |

| Consumer | |

| Enterprise | Sme |

| Large Enterprise |

| By Market Type | Telecommunication Services | Voice (Fixed And Mobile) | |

| Data (Fixed And Mobile) | |||

| Other Telco Services (IoT, Messaging) | |||

| Entertainment | Digital Music | Download | |

| Streaming | |||

| Video Games | |||

| Video-On-Demand | Svod | ||

| Tvod | |||

| Download-To-Own | |||

| E-Publishing | |||

| Advertising | Newspaper | ||

| Magazine | |||

| By Connectivity Technology | 2G | ||

| 3G | |||

| 4G / LTE | |||

| 5G | |||

| Satellite Broadband | |||

| By Revenue Stream | Subscription | ||

| Advertising-Funded | |||

| Micro-Transactions / Pay-Per-View | |||

| Licensing And Wholesale | |||

| By Subscriber Category | Consumer | ||

| Enterprise | Sme | ||

| Large Enterprise | |||

Key Questions Answered in the Report

How large will Africa’s entertainment and telecommunication market be by 2031?

The sector is projected to reach USD 118.07 billion by 2031.

Which connectivity technology is expanding the fastest across Africa?

5G is registering the quickest rise, advancing at a 5.45% CAGR through 2031 thanks to fixed-wireless access rollouts.

Which segment currently drives the most revenue?

Telecommunication services remain the primary contributor, accounting for 61.22% of 2025 market value.

Why is Nigeria growing faster than South Africa?

Nigeria combines population scale with rapid 5G deployment and mobile-money-bundled data plans, yielding a 5.81% CAGR that outpaces South Africa.

How are operators keeping network-build costs down?

Regulatory mandates for tower co-location reduce capital expenditure by up to 30%, freeing cash for wider 5G and rural coverage.

What business model is challenging traditional subscriptions?

Micro-transactions and pay-per-view options are expanding at a 5.94% CAGR, reflecting consumer demand for granular spending control.

Page last updated on: