GPU Immersion Cooling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

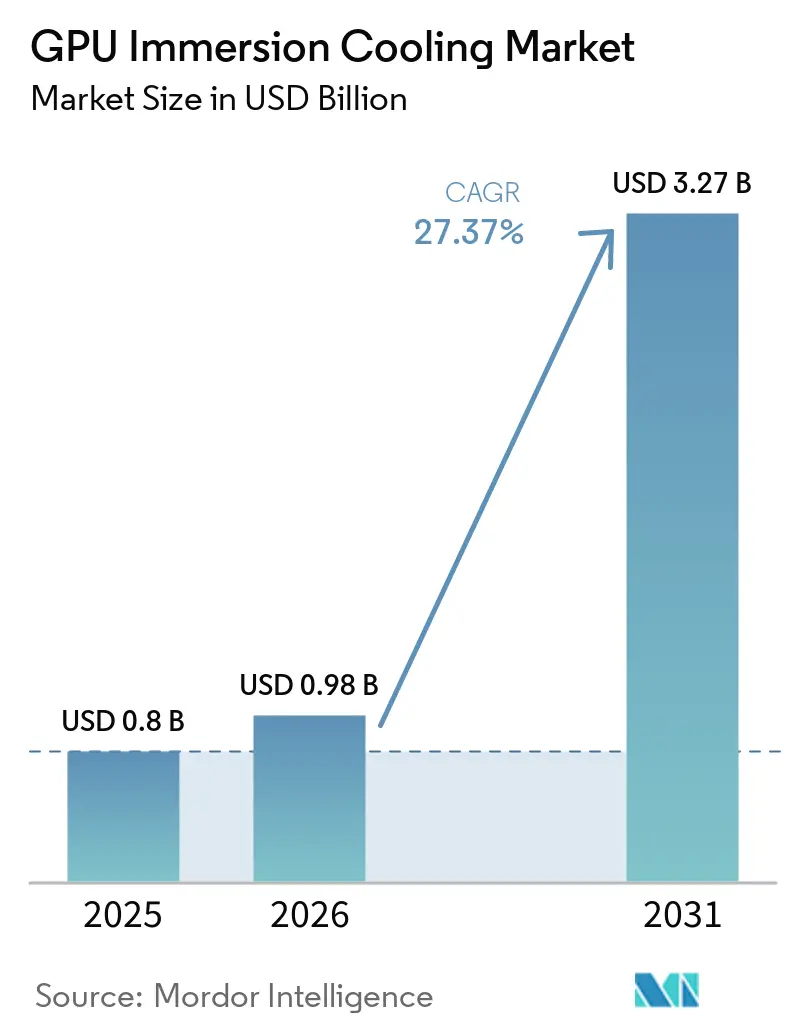

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 3.27 Billion |

| Growth Rate (2026 - 2031) | 27.37% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GPU Immersion Cooling Market Analysis by Mordor Intelligence

The GPU immersion cooling market size is expected to increase from USD 0.80 billion in 2025 to USD 0.98 billion in 2026 and reach USD 3.27 billion by 2031, growing at a CAGR of 27.37% over 2026-2031. Rapid advances in AI accelerators are driving rack densities beyond 100 kilowatts, a threshold that conventional air systems cannot meet without prohibitive floor-space and HVAC costs. Immersion technology lowers power usage effectiveness to the 1.02-1.08 range, cuts energy consumption by up to 40%, and removes evaporative water demand, advantages that compress payback periods below two years in high-electricity regions. GPU suppliers and server OEMs now ship immersion-ready reference designs, while dielectric-fluid prices have fallen 20-30% since 2024, lowering capital intensity and broadening the addressable customer base. Regulatory mandates in China, the European Union, and Washington state further tilt total cost of ownership in favor of liquid-based cooling.

Key Report Takeaways

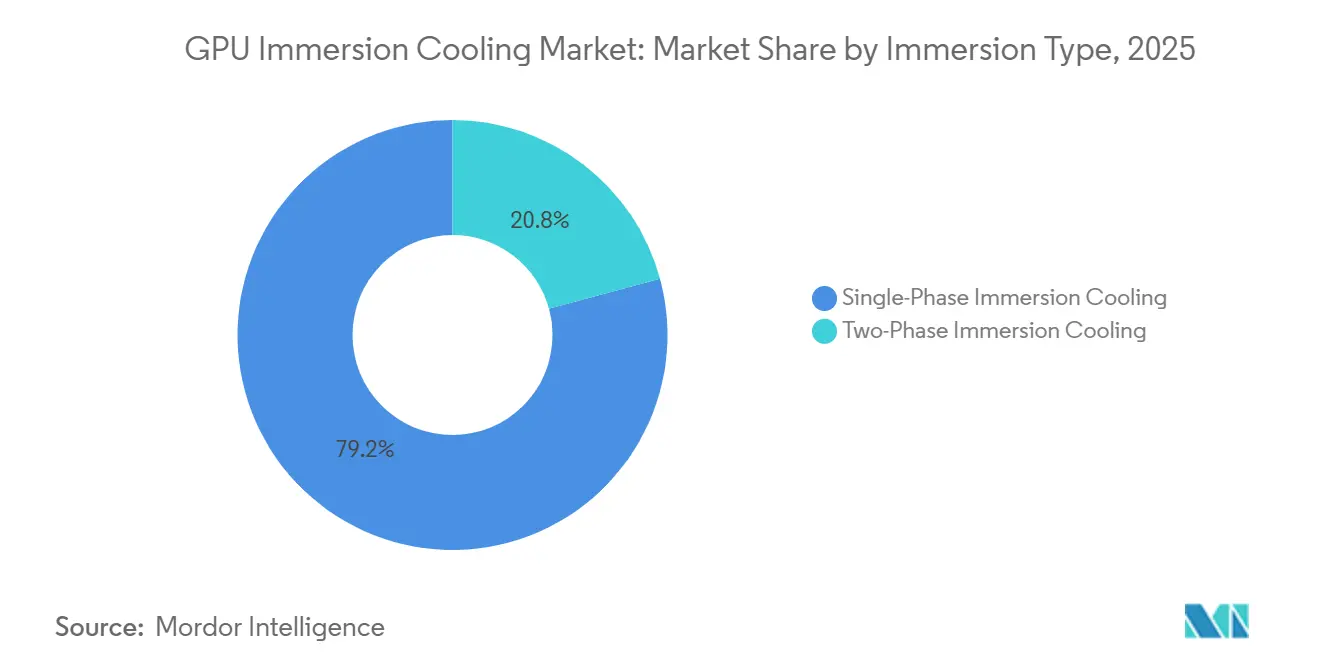

- By immersion type, single-phase solutions led with 79.22% share of the GPU immersion cooling market in 2025, while two-phase systems are projected to grow at a 27.54% CAGR through 2031.

- By solution type, tanks and associated systems controlled 56.45% of revenue in 2025; immersion-optimized GPU servers are forecast to expand at a 27.66% CAGR.

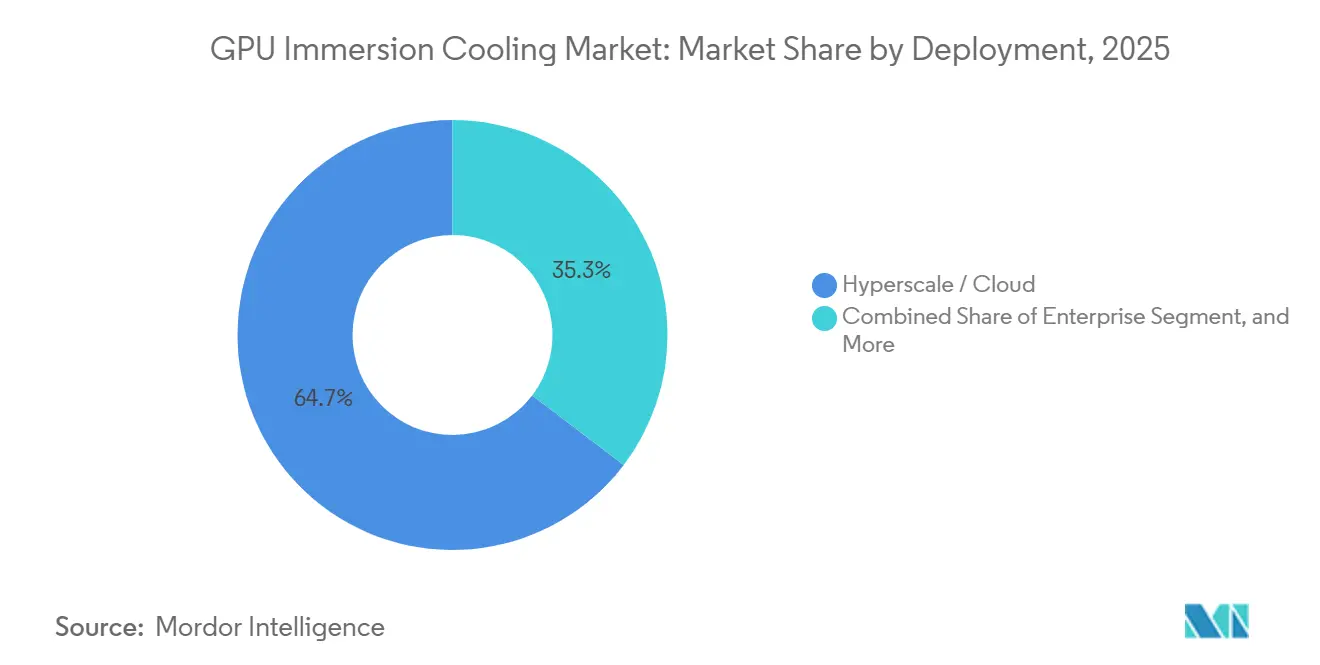

- By deployment, hyperscale and cloud facilities captured 64.67% share of the GPU immersion cooling market in 2025, yet the enterprise segment is on course for a 27.56% CAGR as carbon pricing accelerates retrofits.

- By GPU power density, the 300-700 watt class held 52.23% share of the GPU immersion cooling market in 2025, whereas the above-700 watt segment should post a 27.64% CAGR thanks to next-generation accelerators.

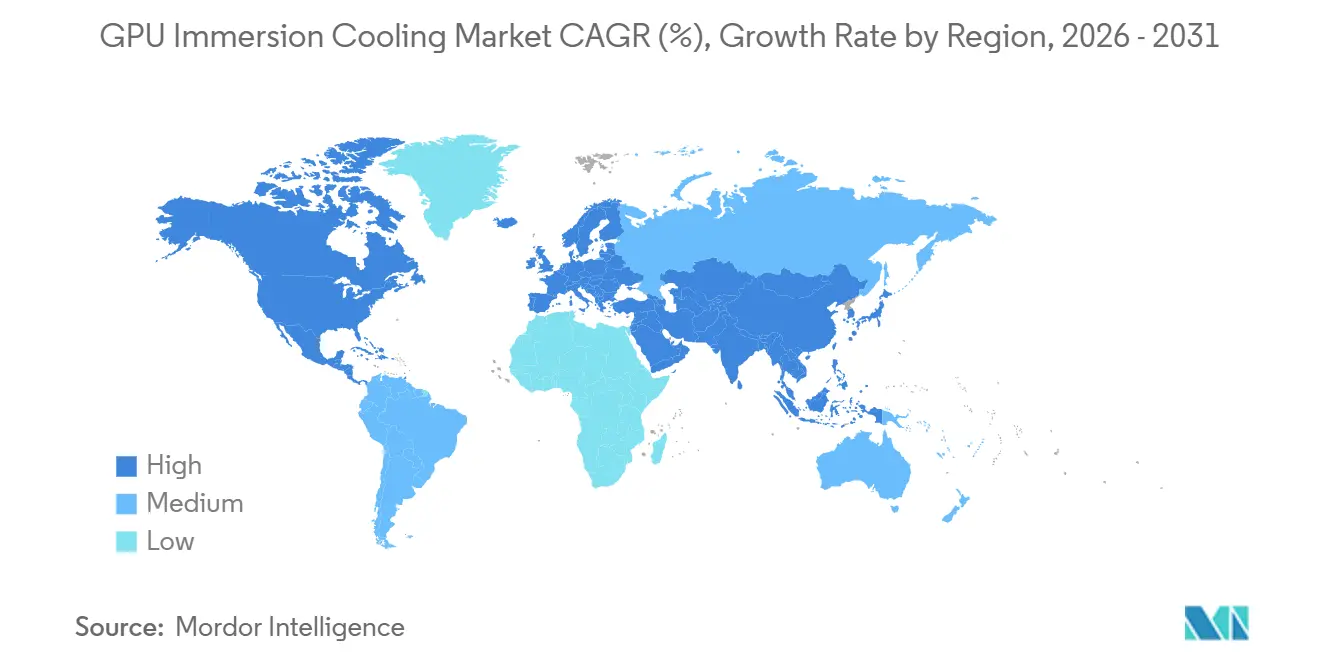

- By geography, Asia-Pacific commanded 67.34% share in 2025 and is set to advance at a 28.05% CAGR through 2031, propelled by strict power-usage-effectiveness mandates.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GPU Immersion Cooling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Rack Power Density in AI Training Facilities | +6.8% | Global, with peak impact in North America and Asia‑Pacific | Short term (≤ 2 years) |

| Accelerated Data‑Center Sustainability Mandates | +5.2% | Europe, North America, and Asia‑Pacific | Medium term (2-4 years) |

| Water Scarcity Driving Liquid‑Free Cooling Adoption | +4.1% | Middle East & Africa, Western United States, Australia, and India | Medium term (2-4 years) |

| Declining Cost Curve of Synthetic Dielectric Fluids | +3.9% | Global, with fastest declines in Asia‑Pacific and North America | Short term (≤ 2 years) |

| OEM Release of Immersion‑Ready GPU Reference Designs | +3.5% | Global, led by North America and Asia‑Pacific | Short term (≤ 2 years) |

| Carbon‑Pricing Policies Elevating Total Cost Gap vs. Air Cooling | +3.2% | Europe, Asia‑Pacific, and select U.S. states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Rack Power Density In AI Training Facilities

NVIDIA's internal roadmaps indicate that its GB200 NVL72 rack, which currently delivers 132 kilowatts, is expected to scale up significantly to a range of 240-800 kilowatts per rack by 2028.[1]NVIDIA Corporation, “NVIDIA DGX SuperPOD,” nvidia.com However, supporting these higher loads requires substantial enhancements to air infrastructure, including the implementation of oversized plenums and auxiliary handlers. These components can consume a considerable portion of a facility's power, accounting for approximately 40-50% of total energy usage. In contrast, immersion cooling solutions offer a more energy-efficient alternative, enabling the maintenance of Power Usage Effectiveness (PUE) values as low as 1.02. This approach has the potential to reduce annual energy consumption by up to 40% for facilities with a 10-megawatt capacity, presenting a compelling case for its adoption in high-performance computing environments.

Accelerated Data-Center Sustainability Mandates

Beginning in 2026, the European Energy Efficiency Directive will require the reuse of heat for sites with energy consumption exceeding 1 megawatt. This regulation effectively establishes liquid cooling systems as the default solution in urban areas across Europe.[2]European Commission, “Energy Efficiency Directive,” energy.ec.europa.eu In Germany, the directive mandates a minimum of 30% heat recovery, further emphasizing the shift toward energy-efficient practices. Similarly, Washington state has set a stringent target of achieving a Power Usage Effectiveness (PUE) of less than 1.2 by 2027, while China has introduced a regulation requiring new hyperscale data center builds to meet a PUE threshold of below 1.25 by 2026. These binding regulatory frameworks are driving the widespread adoption of immersion cooling technologies, marking a significant transformation in energy efficiency standards globally.

Water Scarcity Driving Liquid-Free Cooling Adoption

Evaporative towers, which consume up to 3 liters of water per kilowatt-hour, represent a significant operational challenge in regions experiencing water scarcity. According to data from the U.S. Geological Survey, 40% of counties in the western United States are classified as being under high water stress. In response to these conditions, utilities in states such as Arizona and Nevada have implemented restrictions on new connections for evaporative towers to mitigate further strain on water resources. Alternatively, closed-loop immersion systems, when integrated with dry coolers, offer a highly efficient solution by reducing water consumption by approximately 90%. This substantial reduction in water usage has attracted considerable interest from sustainability-focused initiatives, including Singapore’s Green Mark certification program and India’s draft star-rating schemes, which aim to promote environmentally responsible practices in infrastructure and technology development.[3]U.S. Geological Survey, “Water Stress in the United States,” usgs.gov

Declining Cost Curve Of Synthetic Dielectric Fluids

In 2025, the exit of 3M's Novec line from the market created opportunities for companies such as Shell, Engineered Fluids, and others to expand their presence. This market shift resulted in a notable reduction in prices for single-phase synthetic fluids, which now range between USD 18-25 per liter, compared to the significantly higher range of USD 45-90 observed two years earlier. Concurrently, mineral-oil blends have become more competitively priced, with current listings between USD 3-12 per liter. These developments have led to a substantial decrease in the fluid costs associated with a 100-kilowatt tank, dropping from an estimated USD 12,000 in 2024 to under USD 9,000 by 2026. This reduction has effectively lowered financial barriers, particularly for mid-tier operators, enabling them to allocate resources more efficiently and potentially enhance their operational capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Field‑Service Skill Sets for Immersion Cooling Systems | -2.8% | Global, with acute shortages in India, Southeast Asia, and the Middle East & Africa | Short term (≤ 2 years) |

| Long Qualification and Validation Cycles for Tier‑1 Cloud Providers | -2.3% | North America and Europe hyperscale data‑center operators | Medium term (2-4 years) |

| Regulatory Ambiguity Surrounding New PFAS‑Free Coolants | -1.9% | Europe and the United States | Medium term (2-4 years) |

| High Up‑Front CAPEX for Retrofit Immersion Deployments | -1.7% | Legacy data‑center facilities in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Field Service Skill Sets For Immersion Systems

Immersion cooling requires technicians to manage dielectric fluid chemistry, monitor dissolved-gas analysis, and perform hot-swap server maintenance within liquid-filled enclosures, competencies absent from traditional data center training curricula. Equipment manufacturers are responding by launching certification programs; Green Revolution Cooling introduced its ElectroSafe Partner Program in 2022, certifying over 200 technicians globally by 2025, yet this remains insufficient to support the projected deployment pipeline. The skill gap is most acute in emerging markets, where data center infrastructure is expanding rapidly but technical education infrastructure lags. India's Ministry of Electronics and Information Technology has partnered with industry associations to develop immersion-cooling training modules, though widespread deployment is not expected until 2027.

Long Qualification Cycles For Tier-1 Cloud Providers

Hyperscalers generally conduct pilot programs lasting 12 to 18 months before approving and implementing new cooling architectures. For example, Microsoft completed a 14-month trial before planning its 2025 deployment of a 4,600-GPU system. On the other hand, Amazon is still in the process of evaluating two-phase cooling designs. These designs demand a tank mean time between failures (MTBF) exceeding 10,000 hours, which introduces additional challenges and slows the overall pace of market adoption. Despite the availability of open standards provided by the Open Compute Project, these stringent requirements contribute to the delayed transition within the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Immersion Type: Two-Phase Systems Gain Ground In Ultra-High-Density Clusters

Single-phase technology carried 79.22% of the GPU (Graphics Processing Unit) immersion cooling market share in 2025, favored for operational simplicity and lower fluid cost. It integrates with existing chillers and suits enterprise retrofits. Two-phase immersion delivers latent-heat boiling that handles >150 kilowatts per rack and is projected for a 27.54% CAGR, ideal for frontier AI clusters where single-phase approaches thermal ceilings.

Hyperscale pilots, such as Microsoft’s GB300 cluster, show two-phase racks operating at 1.06 PUE while eliminating pumps. The trade-off remains the high price of fluorinated fluids and looming PFAS regulations. Even so, rising rack power density and the elimination of active pumping are expected to pull two-phase adoption sharply higher in high-electricity jurisdictions.

By Solution Type: Server OEMs Vertically Integrate Immersion Optimization

In 2025, tanks and external systems accounted for 56.45% of total revenue of the GPU immersion cooling market, highlighting the growing preference for modular pods specifically designed to accommodate off-the-shelf servers. This trend reflects the increasing demand for flexible and scalable solutions in data center infrastructure. While dielectric fluids contribute to a steady and recurring revenue stream, their share of the overall value remains comparatively smaller. Immersion-optimized Graphics Processing Unit servers are projected to achieve a significant 27.66% CAGR, driven by the adoption of factory-sealed chassis by OEMs. These chassis eliminate the need for third-party tanks, streamlining the installation process and delivering cost savings of 10-15% on installed systems.

Supermicro’s HGX B300, along with equivalent offerings from Dell, HPE, and Lenovo, integrates advanced features such as condensers and drip-less quick disconnects. However, these innovations result in the establishment of proprietary fluid ecosystems, which may limit interoperability. Vendors that incorporate predictive maintenance analytics and heat-reuse integration into their solutions are gaining a competitive edge. These enhancements align with the market's shift toward vertical integration, enabling companies to differentiate themselves in an increasingly competitive landscape.

By Deployment: Enterprise Segment Accelerates As Carbon Pricing Bites

In 2025, hyperscalers are expected to secure a dominant 64.67% market share, primarily driven by the deployment of AI training clusters operating at a multi-megawatt scale. This dominance underscores the increasing demand for high-performance computing infrastructure capable of supporting large-scale AI workloads in the GPU immersion cooling market. Concurrently, the enterprise segment is anticipated to experience significant growth, with its market share projected to expand at a robust CAGR of 27.56%. This upward trajectory is attributed to regulatory measures such as the EU Emissions Trading System and Taiwan's carbon fee, which are driving up effective power costs. These rising costs are, in turn, accelerating the adoption of immersion cooling technologies by reducing payback periods to an efficient 24-30 months.

Additionally, turnkey cooling-as-a-service models are gaining traction among industries such as banking, pharmaceuticals, and manufacturing. These sectors, often lacking in-house thermal management expertise, are increasingly relying on external solutions to meet their cooling needs efficiently. Furthermore, government and research high-performance computing (HPC) sites represent a niche yet strategically important segment. These entities are actively piloting immersion cooling technologies, positioning themselves as early adopters and paving the way for broader implementation in alignment with exascale computing roadmaps.

By GPU Power Density: Above-700-Watt Segment Mirrors Accelerator Roadmaps

In 2025, Graphics Processing Units within the 300-700 watt range, primarily driven by NVIDIA's H100 and AMD's MI300X, held a dominant 52.23% share of the GPU immersion cooling market. This segment continues to benefit from advancements in technology and increasing demand for high-performance computing solutions. Conversely, the sub-300 watt segment is experiencing a decline as legacy accelerators are gradually phased out due to their inability to meet modern performance requirements. Projections indicate that the above-700 watt category will experience significant growth, with a forecasted compound annual growth rate (CAGR) of 27.64%. This growth is fueled by the introduction of 1,000-watt class GPUs, such as the B200 and GB200 models, which render traditional air cooling systems impractical and make direct-to-chip cooling only marginally effective.

As wattage increases, immersion cooling is emerging as a critical solution, offering linear scalability and enabling rack configurations to exceed 200 kilowatts without the need for auxiliary blower systems.Additionally, the adoption of unified clusters that integrate both training and inference workloads is eliminating the requirement for separate air-cooled inference farms. This technological shift enhances operational efficiency and strengthens the business case for implementing immersion cooling solutions across all stages of deployment, ensuring optimal performance and cost-effectiveness.

Geography Analysis

Asia-Pacific led the Graphics Processing Unit immersion cooling market with 67.34% share in 2025 and will likely post a 28.05% CAGR to 2031. China’s mandate for sub-1.25 PUE by 2026 forces liquid adoption for new builds above 10 megawatts. Japan’s Green Transformation League grants tax credits for liquid cooling, while Singapore’s Green Mark adds bonus points for eliminating evaporative water. India is drafting star-ratings that include immersion incentives expected post-2027.

North America ranks second, anchored by U.S. hyperscalers. Washington state’s sub-1.2 PUE law and California’s updated Title 24 energy code encourage immersion in new projects. Microsoft’s 132-kilowatt racks reached 1.06 PUE, proving commercial viability; Canada and Mexico follow with pilot deployments.

Europe’s trajectory is shaped by statutory heat-reuse and carbon costs of EUR 60-90 (USD 70-105) per metric ton. Germany demands 30% waste-heat capture, the U.K. is consulting on mandatory PUE disclosure, and France funds municipal heat integrations. South America and the Middle East and Africa are nascent but motivated by high electricity prices, water scarcity, and sovereign AI programs, with Brazil exploring tariff incentives and the UAE piloting immersion for its national AI strategy.

Competitive Landscape

Competition is moderate, with system integrators, fluid suppliers, and OEMs jostling across a still-forming value chain in the GPU immersion cooling market. Green Revolution Cooling, LiquidStack, and Submer produce modular tanks and turnkey services aimed at vendor-agnostic buyers. Fluid specialists, notably Shell and Engineered Fluids, vie on performance and PFAS-free credentials; Shell’s DLC Fluid S3 launch in 2025 ignited pricing pressure.

Server OEMs, Dell, HPE, Lenovo, Supermicro, and Fujitsu, now bundle immersion-ready chassis, compressing supply chains and shifting margin upstream. Proprietary fluid ecosystems create customer lock-in but raise switching costs, favoring incumbents with hyperscale ties.

White-space opportunities emerge in heat-reuse integration and edge computing, where compact tanks fit telecom central offices and mobile military bases. Smaller entrants such as Asperitas and DCX focus on containerized and pop-up systems, while Open Compute Project standards trim vendor lock-in yet qualification cycles and capital demands still privilege well-funded incumbents.

GPU Immersion Cooling Industry Leaders

Submer Technologies SL

Green Revolution Cooling Inc.

LiquidStack Inc.

Asperitas B.V.

Shell plc (Immersion Fluids)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Submer Technologies partnered with Hammer Distribution to extend immersion solutions across the U.K. and Ireland, targeting colocation sites adapting to Energy Efficiency Directive rules.

- March 2026: UNICOM Engineering and Green Revolution Cooling expanded collaboration to deliver single-vendor immersion packages for hyperscale and enterprise users.

- January 2026: Shell launched the Triple 10 Challenge to demonstrate immersion battery cooling using its Starship Hybrid 3.0 dielectric fluid.

- December 2025: Supermicro began volume shipments of HGX B300 liquid-cooled systems featuring factory-sealed chambers.

Global GPU Immersion Cooling Market Report Scope

The GPU Immersion Cooling Market pertains to the industry segment dedicated to the application of immersion cooling technology for Graphics Processing Units (GPUs). This approach involves submerging Graphics Processing Units in specially engineered dielectric fluids, enabling more efficient heat dissipation compared to conventional air or liquid cooling methods.

The GPU Immersion Cooling Market Report is Segmented by Immersion Type (Single-Phase Immersion Cooling, Two-Phase Immersion Cooling), Solution Type (Immersion Cooling Tanks / Systems, Dielectric Fluids, Immersion-Optimized GPU Server Systems), Deployment (Hyperscale / Cloud, Enterprise, Government and Research (HPC)), GPU Power Density (Below 300W, 300W - 700W, Above 700W), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Single-Phase Immersion Cooling |

| Two-Phase Immersion Cooling |

| Immersion Cooling Tanks / Systems |

| Dielectric Fluids |

| Immersion-Optimized GPU Server Systems |

| Hyperscale / Cloud |

| Enterprise |

| Government and Research (HPC) |

| Below 300W |

| 300W - 700W |

| Above 700W |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Rest of South America | |

| Middle East and Africa |

| By Immersion Type | Single-Phase Immersion Cooling | |

| Two-Phase Immersion Cooling | ||

| By Solution Type | Immersion Cooling Tanks / Systems | |

| Dielectric Fluids | ||

| Immersion-Optimized GPU Server Systems | ||

| By Deployment | Hyperscale / Cloud | |

| Enterprise | ||

| Government and Research (HPC) | ||

| By GPU Power Density | Below 300W | |

| 300W - 700W | ||

| Above 700W | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected GPU immersion cooling market size by 2031?

The market is projected to reach USD 3.27 billion by 2031, growing from USD 0.98 billion in 2026.

How fast is two-phase immersion cooling expected to expand during the forecast period?

Two-phase solutions are forecast to register a 27.54% CAGR between 2026 and 2031, driven by racks exceeding 150 kilowatts that require latent-heat boiling for thermal control.

Which region is set to lead adoption through 2031?

Asia-Pacific is positioned to remain the largest and fastest-growing geography, helped by China's sub-1.25 PUE mandate and Japan's Green Transformation incentives.

Why are enterprise data centers shifting toward immersion cooling?

Rising carbon-pricing costs and falling dielectric-fluid prices shorten payback periods to about two years, making immersion financially attractive for enterprises seeking lower total cost of ownership.

What are the main barriers to deploying immersion systems today?

Limited field-service expertise, lengthy hyperscale qualification cycles, regulatory uncertainty around PFAS-free coolants, and high retrofit capital costs still slow broader adoption.

How does immersion cooling improve sustainability metrics?

It delivers power usage effectiveness as low as 1.02, eliminates most evaporative water use, and enables 30-40% annual energy savings versus air systems, helping operators meet tightening global efficiency mandates.

Page last updated on: