Europe EV Powertrain Testing Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 1.12 Billion |

| Market Size (2030) | USD 2.08 Billion |

| Growth Rate (2025 - 2030) | 13.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe EV Powertrain Testing Services Market Analysis by Mordor Intelligence

The Europe EV Powertrain Testing Services market size stood at USD 1.12 billion in 2025 and is forecast to reach USD 2.08 billion by 2030, reflecting a 13.21% CAGR. Rising electrification mandates, escalating OEM investment in next-generation 800 V platforms, and the European Commission’s high-profile countervailing duties on imported Chinese EVs are accelerating demand for localized powertrain validation. Battery test capacity additions dominate current spending as regulatory timelines for carbon-footprint disclosure and digital battery passports tighten. Simultaneously, simulation-based validation gains momentum because it compresses program lead times and eases hardware bottlenecks. Outsourcing keeps climbing as Tier-1 suppliers convert capital-intensive test assets into variable operating costs while retaining access to specialized facilities certified under UNECE R100 and R136.

Key Report Takeaways

- By service type, battery testing led with 59.41% of the Europe EV Powertrain Testing Services market share in 2024, whereas simulation testing is projected to advance at 13.32% CAGR through 2030.

- By vehicle type, passenger vehicles accounted for 95.81% of the European EV Powertrain Testing Services market size in 2024, while commercial vehicles are poised to grow fastest at 13.98% CAGR between 2025 and 2030.

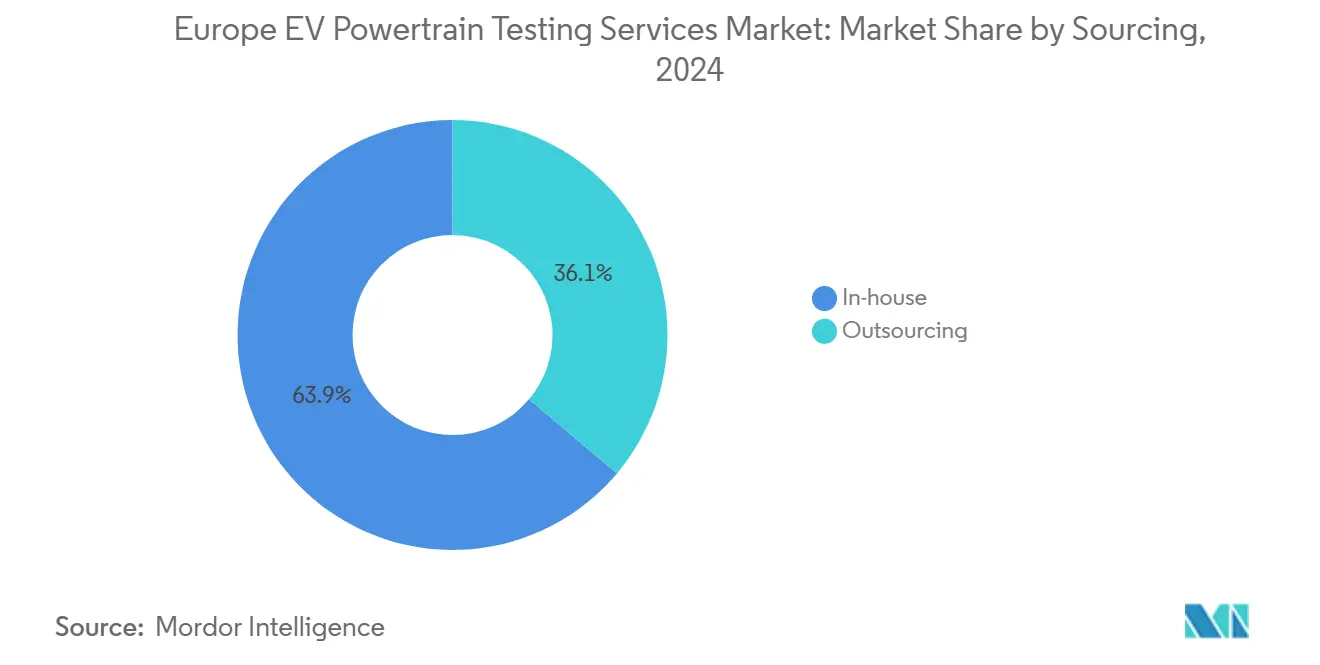

- By sourcing, in-house programs commanded a 63.87% share of the European EV Powertrain Testing Services market in 2024, and outsourcing is forecast to grow at a 13.83% CAGR

- By propulsion, battery-electric platforms comprised 64.61% of the European EV Powertrain Testing Services market size in 2024; fuel-cell programs are set to rise at a 13.54% CAGR to 2030.

- By country, Germany captured 29.31% revenue in 2024, whereas Spain is expected to post the quickest 13.59% CAGR through 2030.

Europe EV Powertrain Testing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Europe Battery-Production Mandates | +2.1% | Germany, France, Spain | Medium term (2-4 years) |

| Stringent UNECE R100 and R136 Updates | +1.8% | Europe-wide | Short term (≤ 2 years) |

| OEM Shift to 800 V Architectures | +1.6% | Germany, Italy, France | Medium term (2-4 years) |

| Outsourcing Surge from Tier-1 Suppliers | +1.4% | Germany, Spain, United Kingdom | Short term (≤ 2 years) |

| Eco-Design Regulation Linking WLTP Range | +1.2% | Europe-wide | Long term (≥ 4 years) |

| Battery-Passport Traceability Requirements | +1.0% | Europe-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Europe Battery-Production Mandates Accelerating Local Validation Demand

The European Battery Regulation obliges manufacturers of traction batteries above 2 kWh to disclose embodied-carbon values by 2025 and to embed a digital battery passport from 2027[1]“Regulation (EU) 2023/1542 on Batteries and Waste Batteries,”, European Commission, eur-lex.europa.eu. Demand for Europe EV Powertrain Testing Services market solutions intensifies because lifecycle verification, performance durability checks, and passport data validation must occur within the Union. Test labs integrate carbon footprint analytics with electrical, thermal, and abuse validation to gain pricing power. OEM gigafactory announcements in Germany, France, Spain, and the Nordics synchronize start-of-production milestones with third-party test-capacity reservations, elevating the need for turnkey compliance workflows.

Stringent UNECE R100 and R136 Updates on High-Voltage Safety

The 04 series of UNECE R100 and the newly amended R136 expand requirements for protection against electric shock, thermal runaway detection, and electromagnetic compatibility. Certification now requires dynamic loading, immersion, and temperature-gradient sequences replicating on-road duty[2]“UN Regulations No. 100 & 136,”, UNECE, unece.org. Test centers must operate 1,000 V-rated chambers, high-capacity calorimeters, and shielded EMC cells to deliver full-vehicle validation. Europe EV Powertrain Testing Services market participants that invested early in next-generation equipment—such as AVL’s High-Voltage E-Drive Lab in Graz—are attracting multi-year framework contracts from global OEMs.

Outsourcing Surge from Tier-1 Suppliers to Meet SOP Timelines

Tier-1 suppliers simultaneously manage ICE sunset programs and new-energy product lines. Transferring validation to specialized labs mitigates capital pressure and shortens critical-path scheduling. Framework agreements covering hardware-in-the-loop, SIL, and full-vehicle dyno work convert capex into opex and secure preferential access to scarce high-power benches. Europe EV Powertrain Testing Services market leaders offering co-location with OEM engineering hubs in Bavaria, Catalonia, and Warwickshire experience the highest utilization.

Battery-Passport Traceability Requirements Under EU Regulation

Digital battery passports assign each pack a unique ID capturing raw-material provenance, environmental indicators, and end-of-life routing. Test houses incorporating blockchain-secured databases and automated compliance checking tools create differentiated service offerings. Early adopters—such as the AVL Digital Battery Passport platform—position themselves as single-window partners for validation, data integrity, and regulatory reporting[3]“Digital Battery Passport Platform,”, AVL List GmbH, avl.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Accredited Fuel-Cell Labs | −1.3% | Germany, France, Netherlands | Medium term (2-4 years) |

| High CAPEX for Multi-Physics Benches | −1.1% | Europe-wide | Short term (≤ 2 years) |

| Data-Sovereignty Constraints | −0.9% | EU-wide | Long term (≥ 4 years) |

| Skilled-Labor Shortage in HIL/SIL | −0.8% | Germany, France, Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Accredited Labs for Fuel-Cell Drivetrain Tests

Hydrogen corridor build-outs spur OEM investment in fuel-cell trucks and coaches. Yet only a handful of European facilities hold ISO/IEC 17025 accreditation for stack performance, hydrogen leakage, and integrated powertrain durability. Limited bench hours delay prototype sign-off and inflate testing costs, trimming the Europe EV Powertrain Testing Services market growth outlook by 1.3 percentage points. Providers expanding capacity—such as TÜV SÜD’s Hydrogen Center of Excellence—must still navigate stringent safety approvals before commercial operation.

Data-Sovereignty Concerns Limiting Cloud-Based Testing

GDPR, UNECE WP.29 cybersecurity, and OEM intellectual-property policies impose strict local-data hosting rules. High-frequency CAN logs, thermal images, and inverter firmware traces must reside on-premise or inside EU-located servers, curtailing real-time remote diagnostic offerings. Labs able to demonstrate ISO 27001 certification and edge-computing secure gateways can partially offset this drag, yet still face higher operating costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Battery Testing Dominates Amid Simulation Growth

Battery testing generated the largest slice of the European EV Powertrain Testing Services market size, equivalent to 59.41% revenue in 2024. Stricter thermal-runaway and cycle-life requirements keep cell, module, and pack validation benches fully booked. Europe EV Powertrain Testing Services market share for battery labs remains buoyed by mandatory performance declarations tied to warranty terms. Looking ahead, simulation testing’s 13.32% CAGR signals OEM confidence in digital twins that front-load design verification and reduce hardware iterations.

Integration of physical and virtual environments is reshaping provider value propositions. AVL’s CONCERTO suite merges field data with AI-aided models to predict degradation under varied duty cycles, enabling rapid troubleshooting before hardware tests commence. Providers mastering such hybrid workflows can monetize license fees and bench time, reinforcing customer stickiness across the development lifecycle.

By Vehicle Type: Commercial Vehicles Drive Future Growth

Passenger cars retained 95.81% of the 2024 Europe EV Powertrain Testing Services market size due to the sheer volume of model launches. However, commercial fleets are scaling faster, showing a 13.98% CAGR through 2030 as last-mile delivery, municipal buses, and regional haulage electrify to meet CO₂ fleet regulations. High-load profiles and long-duty-cycle durability tests demand bespoke dyno rigs and thermal-soak chambers operating at continuous high currents.

Testing centers adapting to megawatt-class charging validation and integrating auxiliary systems—such as electric refrigeration units—capture emergent demand. Providers collaborating with logistics operators to replicate depot charging patterns can offer differentiated insights that cut downtime and energy costs, deepening their footprint in the expanding commercial segment of the European EV Powertrain Testing Services market.

By Sourcing: Outsourcing Model Gains Strategic Momentum

In-house programs commanded a 63.87% share of the European EV Powertrain Testing Services market in 2024, and Outsourcing is forecast to grow at a 13.83% CAGR. Tier-1 suppliers and niche OEMs favor external partners to avoid multimillion-dollar capex commitments for equipment with five-year obsolescence cycles. Outsourcing also grants access to certified auditors critical for UNECE type-approval dossiers, compressing schedules to meet start-of-production targets.

Service providers respond by offering subscription-based bench access, flexible shifts, and embedded engineering support in customer premises. This hybrid staffing approach aligns with agile sprint cycles and improves knowledge transfer without jeopardizing intellectual-property controls, reinforcing the outsourcing trajectory.

By Propulsion Type: Fuel Cells Accelerate Despite BEV Dominance

Battery-electric platforms comprised 64.61% of the 2024 Europe EV Powertrain Testing Services market share. Yet fuel-cell projects, especially in heavy-duty and long-range segments, manifest a 13.54% CAGR owing to EU Hydrogen Strategy incentives. Rigorous hydrogen leak, stack-aging, and purge-cycle validations expand the service envelope. Providers scaling hydrogen-compatible safety systems—blast-proof enclosures, ATEX-rated sensors—can seize high-margin contracts while competition remains thin.

Hybrid and plug-in hybrid validations persist as transitional technology needs, focusing on energy-management and NVH interactions between ICE and e-motors. Nonetheless, resource allocation is tilting toward pure electric and fuel-cell powertrains, reflecting customer road-maps and regulatory deadlines.

Geography Analysis

Germany commanded 29.31% of the 2024 Europe EV Powertrain Testing Services market size, leveraging its dense cluster of OEM headquarters, Tier-1 suppliers, and certification bodies. Continuous government support through programs like “IPCEI Batteries” accelerated test-infrastructure build-outs, particularly around Bavaria and Baden-Württemberg. German providers’ proximity to UNECE working groups further cements their influence on global validation protocols.

Though smaller in absolute terms, Spain represents the fastest-growing territory at 13.59% CAGR through 2030. State-backed Perte VEC funding catalyzes EV manufacturing lines in Catalonia and Valencia, creating downstream demand for localized powertrain verification. National metrology rules were introduced in 2024, requiring periodic charger recalibration and adding further test volume, especially for high-capacity DC infrastructure.

Elsewhere, France and Italy maintain mature yet expanding markets benefiting from legacy aerospace-automotive competencies and public-private R&D programs. The United Kingdom’s cluster around the Midlands and the North East draws on catapult centers focused on battery manufacturing scale-up. The rest of Europe cohort—comprising Scandinavia, Central, and Eastern nations—registers steady demand as imported EV models require homologation under national regulations aligned with UNECE.

Competitive Landscape

The Europe EV Powertrain Testing Services market competition is moderate, with scale players and specialist firms coexisting. AVL, TÜV SÜD, and Applus+ IDIADA anchor the high-end with multidisciplinary labs, global accreditation matrices, and proprietary software ecosystems. Their investments span hydrogen stack benches, 800 V e-drive dynos, and integrated EMC battery chambers. Mid-tier players carve niches in software-only test automation, battery cell analytics, or high-speed data acquisition.

M&A activity centers on augmenting geographic reach and filling technology gaps. AVL’s acquisition of a Nordic hydrogen test facility and TÜV SÜD’s partnership with Rohde and Schwarz on automated EMC capture exemplify strategic positioning. Start-ups emphasizing AI-enabled anomaly detection or cloud-based digital twins attract venture funding but face scale challenges tied to data-sovereignty compliance. Success hinges on combining physical capacity, digital competence, and regulatory advisory under one umbrella to serve time-pressed OEM programs.

Europe EV Powertrain Testing Services Industry Leaders

AVL List GmbH

TÜV SÜD

Intertek Group plc

HORIBA Group

Applus+ IDIADA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: UL Solutions Inc. has inaugurated its Europe Advanced Battery Testing Laboratory in Aachen, Germany. This facility will evaluate batteries for electric vehicles (EVs) and large-scale energy storage systems. This move not only broadens the company's battery technology testing capabilities but also strengthens its presence in Europe.

- January 2025: AVL launched its Digital Battery Passport platform, ensuring automated lifecycle traceability in line with the EU's Sustainable Batteries Regulation. This platform aims to enhance transparency and compliance by providing detailed insights into the battery's lifecycle, from production to recycling. It supports stakeholders in meeting regulatory requirements while promoting sustainability within the battery market.

Europe EV Powertrain Testing Services Market Report Scope

| Battery Testing |

| Simulation Testing |

| Passenger Vehicle |

| Commercial Vehicle |

| Outsourcing |

| In-house |

| Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| United Kingdom |

| Germany |

| Spain |

| Italy |

| France |

| Russia |

| Rest of Europe |

| By Service Type | Battery Testing |

| Simulation Testing | |

| By Vehicle Type | Passenger Vehicle |

| Commercial Vehicle | |

| By Sourcing | Outsourcing |

| In-house | |

| By Propulsion Type | Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) | |

| Plug-in Hybrid Electric Vehicle (PHEV) | |

| Fuel Cell Electric Vehicle (FCEV) | |

| By Country | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe EV Powertrain Testing Services market in 2025?

The market is valued at USD 1.12 billion in 2025 and is projected to reach USD 2.08 billion by 2030, reflecting a 13.21% CAGR.

Which service type captures the biggest revenue in the region?

Battery testing dominates with a 59.41% share of 2024 revenue, driven by strict EU safety and carbon-footprint mandates.

Why is outsourcing gaining traction among Tier-1 suppliers?

Outsourcing converts multimillion-dollar capex into operating expense while ensuring access to certified benches and regulatory expertise, fostering 13.83% CAGR growth for the model.

Which country is expected to grow fastest through 2030?

Spain leads regional growth at a 13.59% CAGR thanks to new EV manufacturing plants and supportive infrastructure programs.

What technology shift is reshaping test-bench requirements?

The move to 800 V electrical architectures requires high-current dynos, advanced safety systems, and upgraded power electronics validation capabilities.

Page last updated on: