Europe EV Charging As A Service Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

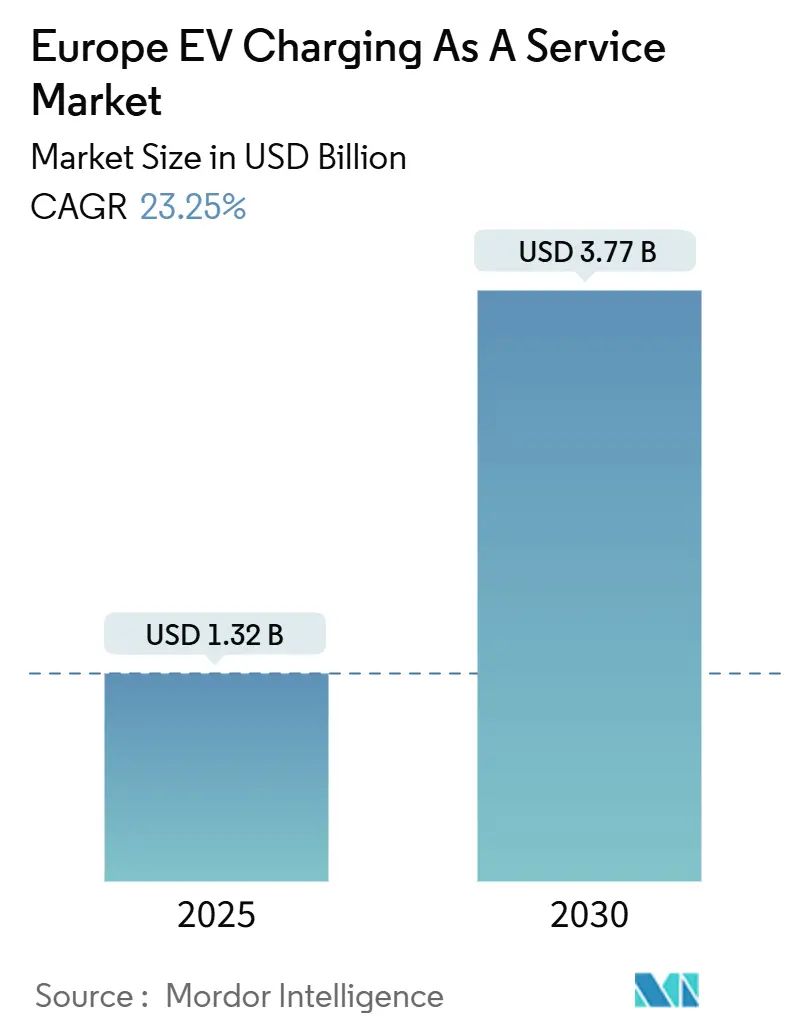

| Market Size (2025) | USD 1.32 Billion |

| Market Size (2030) | USD 3.77 Billion |

| Growth Rate (2025 - 2030) | 23.25% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe EV Charging As A Service Market Analysis by Mordor Intelligence

The Europe EV Charging as a Service market size is USD 1.32 billion in 2025 and is projected to reach USD 3.77 billion by 2030, advancing at a 23.25% CAGR. This sharp rise reflects a synchronized push from binding European regulations, rapid technological improvements in high-power hardware, and large-scale fleet electrification programs that collectively create steady and geographically diversified demand. Binding targets under the Alternative Fuels Infrastructure Regulation (AFIR) and the broader “Fit for 55” package remove policy uncertainty and force minimum charging-network densities across member states. Corporate fleet decarbonization mandates amplify public and depot chargers utilization because company cars account for most new-car emissions in the region. Meanwhile, corridor alliances among automotive OEMs accelerate the roll-out of interoperable high-power stations that bypass slow legacy retail channels. Together, these forces support sustained capital inflows and encourage software-centric service models that monetize pricing flexibility, dynamic load management, and vehicle-to-grid (V2G) functionality.

Key Report Takeaways

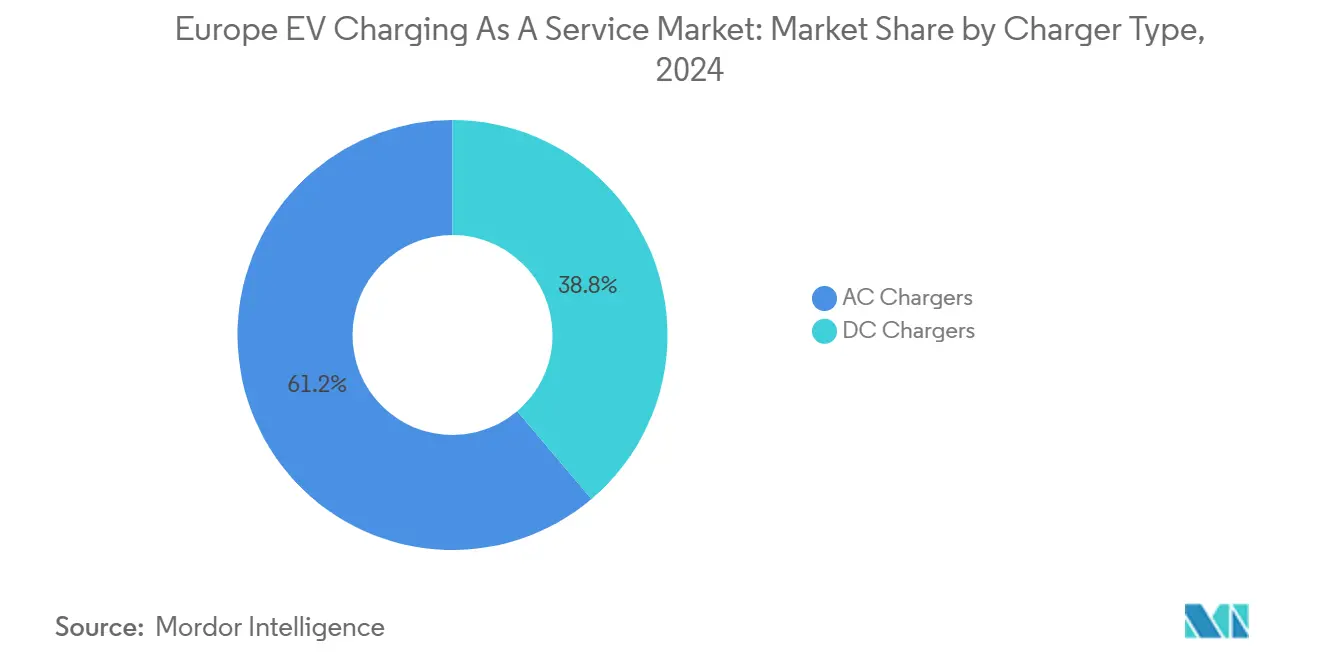

- By charger type, AC chargers led with 61.23% revenue share in 2024, while DC chargers are advancing at a 27.38% CAGR to 2030.

- By power output, Level 1/AC (≤ 22 kW) accounted for 47.54% of the Europe EV Charging as a Service market share in 2024, whereas high-power DC (> 150 kW) is forecast to expand at a 37.01% CAGR through 2030.

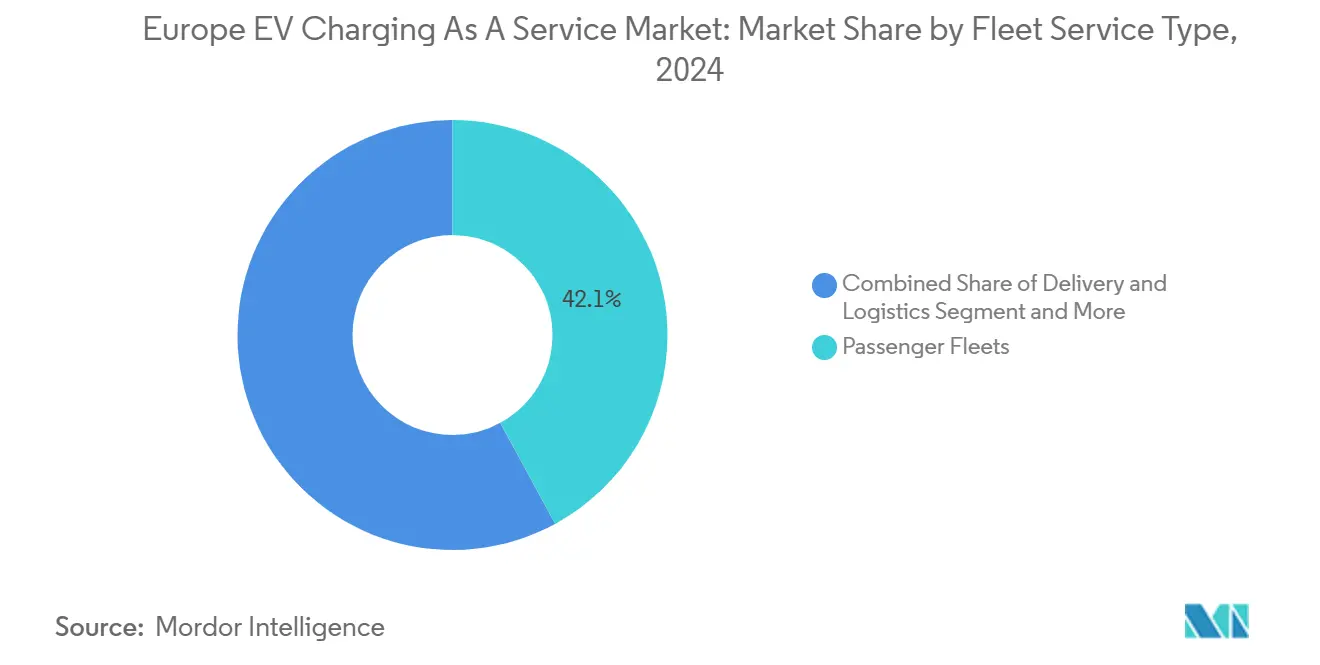

- By fleet service, passenger fleets held 42.08% of the Europe EV Charging as a Service market size in 2024, and delivery and logistics fleets recorded the fastest growth at 28.26% CAGR to 2030.

- By end-use, public setups maintained a 64.17% share in 2024; semi-public charging is growing at a 24.53% CAGR on the back of workplace and destination deployments.

- By geography, Germany captured a 22.68% revenue share in 2024, while Poland posted the highest country-level CAGR at 23.16% to 2030.

Proportional positioning is established by comparing regional contributions against the global total, including that of Europe. The ev charging as a service market share in our global report expresses these relative weights.

Europe EV Charging As A Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU AFIR and "Fit-for-55" Rollout Deadlines | +6.2% | EU-wide, strongest in Germany, France, Netherlands | Medium term (2–4 years) |

| OEM–Led Corridor Alliances (IONITY, CV-Charging Europe) | +4.8% | Pan-European highways, Nordic countries, Central Europe | Long term (≥ 4 years) |

| Corporate-Fleet Electrification Mandates | +5.1% | Germany, UK, France, Benelux region | Short term (≤ 2 years) |

| Declining Levelised Cost of More Than 150 kW DC Chargers | +3.9% | Urban centers, highway corridors across Europe | Medium term (2–4 years) |

| AI-Driven Dynamic-Pricing Engines Raise Site Utilisation | +3.7% | Germany, Netherlands, UK, Nordic countries | Short term (≤ 2 years) |

| Surplus-Renewables Trading and V2G Revenue Stacking | +2.4% | Nordic countries, Germany, Netherlands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU AFIR and "Fit-for-55" Rollout Deadlines

Regulatory enforcement mechanisms create binding infrastructure deployment schedules that eliminate market uncertainty while establishing minimum performance thresholds. The AFIR mandates that all non-residential buildings with over 20 parking spaces must install at least one EV charging point as of January 2025, with businesses facing penalties for non-compliance. This regulatory framework extends beyond passenger vehicles to encompass heavy-duty transport, requiring one Hydrogen Refueling Station every 200km on the TEN-T Core network by 2030 with a daily capacity of one ton. The Clean Vehicles Directive establishes procurement targets for public sector fleets, requiring Member States to meet minimum percentages of clean vehicles in public procurement, particularly zero-emission buses from 2026. Spain's implementation demonstrates regulatory precision through Order ITU/1475/2024, mandating certified meters for both AC and DC chargers with periodic verifications every eight years starting January 2025. These deadlines compress deployment timelines while standardizing technical specifications across member states, reducing operational complexity for pan-European charging service providers.

OEM–led Corridor Alliances (IONITY, CV-Charging Europe)

Strategic partnerships between automotive manufacturers create dedicated high-power charging networks that bypass traditional fuel retail distribution channels. IONITY's expansion under CEO Jeroen van Tilburg focuses on maintaining HPC stations within 150 km intervals, particularly in key markets like France, Sweden, and the UK, while addressing urban charging needs in metropolitan areas. Hyundai Motor Group's partnership with IONITY as a strategic partner and shareholder demonstrates how OEMs leverage charging infrastructure as a competitive differentiator, utilizing the CCS charging standard and operating on 100% renewable energy. The Spark Alliance formation creates interoperability across member networks, allowing drivers to use preferred charging apps at any member station while maintaining transparent pricing structures. Volkswagen and BP's Flexpole 150kW DC charger deployment exemplifies integrated OEM-energy partnerships, featuring battery storage that enables connection to low voltage grids while reducing installation times and costs. These alliances establish proprietary charging ecosystems that enhance customer retention while accelerating infrastructure deployment beyond traditional market mechanisms.

Corporate-fleet Electrification Mandates

Fleet electrification mandates create concentrated demand nodes that justify high-power charging infrastructure investments while establishing predictable utilization patterns. Transport & Environment's proposal for binding 100% zero-emission vehicle targets for large corporate fleets starting in 2030 would generate demand for over 2.1 million EVs by 2030 to meet CO₂ emission standards. The UK's Zero Emission Vehicle Mandate requires 80% of new cars and 70% of new vans to be zero emission by 2030, increasing to 100% by 2035, with the UK government investing GBP 20 billion in vehicle production. Swedish tax incentives increased the share of electric vehicles in company purchases from 16% in 2018 to 74% in 2023, demonstrating policy effectiveness in accelerating fleet transitions[1]"Nordic companies lead the charge on electric vehicles," Financial Times, www.ft.com..

Declining Levelized Cost of More than 150 kW DC Chargers

Technological advances in power electronics and economies of scale reduce high-power charging infrastructure costs while improving charging speeds and reliability. Fraunhofer ISE's development of medium voltage technology enables peak loads of several megawatts using silicon carbide semiconductors, supporting 15 to 25 charging points drawing 1.5 to 3.5 megawatts of power. The modular design reduces material requirements and environmental impact while enabling compatibility with CCS1, CCS2, and the upcoming Megawatt Charging System standards. Virta's cost analysis indicates that 150 kW DC charging models can reach EUR 30,000, while 25 kW DC wall boxes start at a few thousand EUR, demonstrating significant cost variations based on power output. IONITY's procurement of the Megawatt Charging System Alpitronic HYC1000 represents the first deployment of next-generation charging technology that supports faster charging solutions. Nature Communications research comparing levelized cost of charging across 30 European countries reveals costs ranging from EUR 0.173/kWh in Hungary to EUR 0.330/kWh in Germany, with residential charging and solar PV integration offering the lowest cost options.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-Connection Delays and Capacity Bottlenecks | -4.3% | Germany, Eastern Europe, Southern Europe | Short term (≤ 2 years) |

| High Upfront CAPEX/ROI Risk at Low-Traffic Sites | -3.1% | Rural areas, Eastern Europe, peripheral regions | Medium term (2–4 years) |

| Battery-Swapping Stations as Substitute Solution | -2.2% | Urban freight corridors, select Southern EU member states | Medium term (2–4 years) |

| Software-Stack Fragmentation/Roaming Failures | -2.0% | EU-wide, especially in cross-border and multi-operator zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Grid-connection Delays and Capacity Bottlenecks

Infrastructure deployment constraints create systematic delays that compound investment risks while limiting market expansion velocity. German retailers report grid connection delays reaching 18 months for EV charging points, with some grid operators refusing connections due to insufficient capacity. The European Commission's Action Plan for Grids identifies EUR 584 billion in required electricity grid investments by 2030, with electricity consumption expected to rise by 60% as clean mobility and electrification accelerate. Bruegel estimates annual investment needs between EUR 65 billion and EUR 100 billion for Europe's electricity networks, emphasizing the critical role of coordinated grid planning and regulatory frameworks. Italy's charging infrastructure development faces bureaucratic hurdles and regional disparities, despite the government's allocation of EUR 740 million from the National Recovery and Resilience Plan for 21,400 ultra-fast charging stations by 2025. EY analysis warns that unmanaged charging scenarios could destabilize the grid, requiring managed charging solutions that control charging times and capacities to transform potential liabilities into assets.

High Upfront CAPEX/ROI Risk at Low-traffic Sites

Economic viability challenges at peripheral locations create geographic coverage gaps that limit network completeness while concentrating investments in high-density corridors. Norway's experience demonstrates utilization challenges, with many charging operators struggling with profitability due to low utilization rates despite leading global EV adoption with 96.9% market share. California Energy Commission research on DC fast charging economics shows that demand charges represent over 40%[2]"Improving Commercial Viability of Fast Charging by Providing Renewable Integration and Grid Services With Integrated Multiple DC Fast Chargers," California Energy Commission, energy.ca.gov. of annual utility costs, with potential savings of USD 4,700 to USD 6,000 annually through solar photovoltaic integration. These economic constraints require innovative financing mechanisms and strategic site selection to achieve network coverage while maintaining profitability across diverse geographic markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Charger Type: AC Dominance Faces DC Disruption

AC Chargers command 61.23% market share in 2024, reflecting their cost-effectiveness and widespread deployment across residential and workplace applications. DC Chargers demonstrate superior growth momentum at 27.38% CAGR through 2030, driven by corridor charging requirements and fleet applications demanding rapid turnaround times. The segmentation shift reflects evolving user behavior patterns. Transport & Environment analysis shows that while home charging accounts for 70% of usage, workplace charging becomes critical for urban EV owners lacking home access. GridX's European EV charging report reveals that fast chargers above 150 kW comprise nearly 10% of the public charging network, with average charging speed reaching 42 kW across Europe.

IONITY's launch of the IONITY Go tariff at EUR 0.71 per kWh without subscription fees demonstrates how high-power DC charging operators compete against AC alternatives through simplified pricing structures. Shell's testing of dynamic pricing models at fast charging stations exemplifies how DC operators optimize utilization through demand-responsive tariffs. The competitive dynamics favor DC charging for commercial applications, while AC charging maintains dominance in residential and extended-dwell scenarios where charging speed requirements remain modest.

By Power Output: High-Power Infrastructure Accelerates

Level 1/AC (less than 22 kW) maintains a 47.54% market share in 2024, supported by residential installations and workplace charging deployments where overnight charging patterns align with lower power requirements. High-Power DC (over 150 kW) emerges as the fastest-growing segment at 37.01% CAGR, reflecting corridor charging investments and fleet electrification demands. Level 2 (22 to 50 kW) and Fast DC (50 to 150 kW) segments serve intermediate applications, bridging residential convenience with commercial charging speed requirements.

Technological advances enable megawatt-class charging capabilities, with Fraunhofer ISE's medium voltage technology supporting peak loads of several megawatts through silicon carbide semiconductors. The modular design accommodates various vehicle types while maintaining compatibility with CCS1, CCS2, and upcoming Megawatt Charging System standards. IONITY's procurement of the Alpitronic HYC1000 Megawatt Charging System represents the first-generation deployment of ultra-high-power charging technology. Power output segmentation reflects infrastructure maturation, with high-power installations concentrated along highway corridors and urban fast-charging hubs where utilization rates justify capital investments.

By Fleet Service Type: Logistics Drives Growth

Passenger Fleets hold 42.08% market share in 2024, benefiting from corporate electrification mandates and favorable total cost of ownership economics in urban applications. Delivery and Logistics represent the fastest-growing segment at 28.26% CAGR, driven by last-mile electrification requirements and zero-emission zone implementations across European cities. Company Vehicles and Motor Pools complete the segmentation, serving diverse commercial applications with varying utilization patterns and charging requirements.

The International Council on Clean Transportation analysis demonstrates that battery-electric trucks achieve a competitive total cost of ownership compared to diesel alternatives in European markets, particularly for high-mileage applications. Amsterdam University research on zero-emission service logistics emphasizes the importance of comprehensive charging strategies and innovative logistics concepts to enhance efficiency while reducing emissions. Fleet service differentiation creates distinct charging infrastructure requirements, with delivery applications demanding rapid charging capabilities while passenger fleets benefit from overnight charging solutions at lower power levels.

By End-use: Semi-Public Gains Momentum

Public Charging Setup maintains 64.17% market share in 2024, encompassing highway corridors, urban fast-charging hubs, and retail locations where accessibility drives utilization. Semi-Public Charging Setup accelerates at 24.53% CAGR through 2030, reflecting workplace charging expansion and destination charging deployments at hotels, shopping centers, and commercial facilities. The segmentation reflects evolving charging behavior patterns, with residential charging accounting for 70% of usage while public infrastructure addresses range anxiety and enables long-distance travel[3]Karri Takki, "Navigating Europe's EV Charging Expansion," Statzon, statzon.com..

Zaptec's workplace charging solutions demonstrate semi-public segment growth, with OZEV-approved chargers enabling businesses to claim government grants covering up to 75% of installation costs. Go-e's analysis of company car charging reveals that home charging often costs less than public stations while enhancing employee satisfaction and work-life balance. The UK's pilot of EV charging "gullies" for residents without driveways represents innovative semi-public infrastructure that bridges home and public charging gaps. End-use segmentation evolution reflects infrastructure maturation, with semi-public installations offering controlled access and predictable utilization patterns that improve economic viability compared to fully public alternatives.

Geography Analysis

Germany commands 22.68% market share in 2024, leveraging its automotive manufacturing base and systematic infrastructure deployment programs. The country operates 161,686 public charging points as of February 2025, representing 21% annual growth with total capacity reaching 6.1 GW. The government's EUR 2 billion investment targets one million public charging points by 2030, supported by the "Deutschlandnetz" project, adding 9,000 fast charging points at 1,000 locations with EUR 1.8 billion federal funding. New legislation mandates large gas stations to install at least one fast charging point by 2028, potentially adding 8,000 points to the network. Grid connection challenges persist, with retailers reporting 18-month delays for new charging point connections due to capacity constraints.

Poland is the fastest-growing geography at 23.16% CAGR through 2030, supported by a EUR 380 million incentive program offering subsidies for new EV purchases. The Nordic region demonstrates market leadership, with Norway achieving 96.9% EV market share and 447 chargers per 100,000 inhabitants. Sweden shows two-thirds of cars sold in 2023 being electric or plug-in hybrids, though growth slowed in 2024 following subsidy reductions. France maintains 154,694 public charging points by December 2024, targeting 400,000 by 2030, with employment in the EV charging sector projected to grow from 80,000 jobs in 2025 to 162,000 by 2030.

Southern European markets accelerate infrastructure deployment through targeted investment programs and regulatory frameworks. Italy aims for 110,000 public charging points by 2030, supported by EUR 740 million from the National Recovery and Resilience Plan for 21,400 ultra-fast charging stations. Spain's implementation of Order ITU/1475/2024 mandates certified meters for charging stations starting January 2025, establishing technical standards that enhance measurement accuracy and transparency. Mobilize plans to open 650 charging stations across France, Italy, Belgium, and Spain by 2028, demonstrating coordinated regional expansion strategies. The Netherlands leads in charging density with 183,000 installed charge points and 10.04 charge points per 1,000 inhabitants, while the UK benefits from TotalEnergies and SSE's joint venture "Source", deploying up to 3,000 high-power charge points within five years.

Mordor Intelligence examines the ev charging as a service market across diverse other regional markets as well, offering granular country-level perspectives for China, India, United States, and South Korea and more.

Competitive Landscape

The European EV charging market exhibits fragmented characteristics with multiple regional and international players competing across different segments and geographies. Market concentration remains low, with Tesla leading in charge point numbers and capacity, followed by IONITY and Enel X, while EnBW's mobility+ service commands the most extensive network with 414,000 charging points. Strategic alliance formation represents the primary competitive response, exemplified by the Spark Alliance uniting Atlante, Electra, Fastned, and IONITY to create Europe's largest public charging network spanning over 1,700 stations and 11,000 charging points across 25 countries.

Technology differentiation focuses on interoperability solutions. ChargePoint is releasing the first payment terminal that is compliant with OCPI standards and EU AFIR regulations to support payments for up to 99 chargers at a single site. White-space opportunities emerge in software standardization and grid integration services, as 84% of surveyed charging stations do not implement Transport Layer Security protocols, creating security vulnerabilities that undermine user confidence. Emerging disruptors leverage AI-driven optimization, with gridX and E.ON developing AI-based load management systems that increase energy distribution to electric vehicles by 30% compared to previous systems. Electra's EUR 433 million green loan, securing over EUR 1 billion in total funding, demonstrates how specialized charging operators access capital markets to accelerate expansion.

The competitive landscape evolution favors integrated service providers capable of delivering end-to-end charging solutions while maintaining interoperability across diverse vehicle and payment systems, with regulatory frameworks like AFIR mandating standardized user experiences that reduce proprietary advantages.

Europe EV Charging As A Service Industry Leaders

-

Allego B.V.

-

IONITY

-

Fastned

-

Enel X Way

-

BP Pulse

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Electra secured a EUR 433 million green loan, bringing its total funding to over EUR 1 billion to accelerate EV charging infrastructure expansion across Europe. This funding milestone positions Electra among the most capitalized independent charging operators in the European market.

- May 2025: IONITY secured EUR 600 million in funding to expand its high-performance charging network across Europe, targeting enhanced customer experience through the relaunch of the IONITY App and urban charging station development. The investment supports IONITY's strategy to maintain HPC stations within 150 km intervals across key European markets.

- April 2025: The Spark Alliance launched, uniting Atlante, Electra, Fastned, and IONITY to create Europe's largest public charging network with over 1,700 stations and 11,000 charging points across 25 countries. The alliance enables seamless charging access through preferred apps at any member station.

Europe EV Charging As A Service Market Report Scope

| AC Chargers |

| DC Chargers |

| Level 1/AC (Less than 22 kW) |

| Level 2 (22 to 50 kW) |

| Fast DC (50 to 150 kW) |

| High-Power DC (More than 150 kW) |

| Company Vehicles and Motor Pools |

| Delivery and Logistics |

| Passenger Fleets |

| Semi-Public Charging Setup |

| Public Charging Setup |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Norway |

| Sweden |

| Denmark |

| Poland |

| Rest of Europe |

| By Charger type | AC Chargers |

| DC Chargers | |

| By Power Output | Level 1/AC (Less than 22 kW) |

| Level 2 (22 to 50 kW) | |

| Fast DC (50 to 150 kW) | |

| High-Power DC (More than 150 kW) | |

| By Fleet Service Type | Company Vehicles and Motor Pools |

| Delivery and Logistics | |

| Passenger Fleets | |

| By End-use | Semi-Public Charging Setup |

| Public Charging Setup | |

| By Geography – Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Norway | |

| Sweden | |

| Denmark | |

| Poland | |

| Rest of Europe |

Key Questions Answered in the Report

What CAGR is expected for Europe’s EV charging-as-a-service segment through 2030?

The Europe EV Charging as a Service market is forecast to grow at a 23.25% CAGR from 2025 to 2030, reaching USD 3.77 billion.

Which charger type leads in market share?

AC chargers hold 61.23% of 2024 revenue because they fit residential and workplace use cases with lower installation costs.

Why are corporate fleets pivotal to charging demand?

Company cars represent over half of new-car sales and 71% of related emissions, so regulatory fleet mandates ensure high utilization at depot and workplace chargers.

What is the main barrier to faster charger deployment?

Grid-connection delays average 18 months in high-demand regions, slowing the commissioning of fully funded sites despite hardware readiness.

How are OEM alliances shaping the network?

Partnerships such as IONITY and the Spark Alliance pool capital and create roaming access to more than 11,000 high-power points across 25 countries, accelerating cross-border coverage.

Which country posts the fastest market growth?

Poland leads with a projected 23.16% CAGR through 2030, supported by generous purchase subsidies and dedicated infrastructure grants.

Page last updated on: