Europe Employee Onboarding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

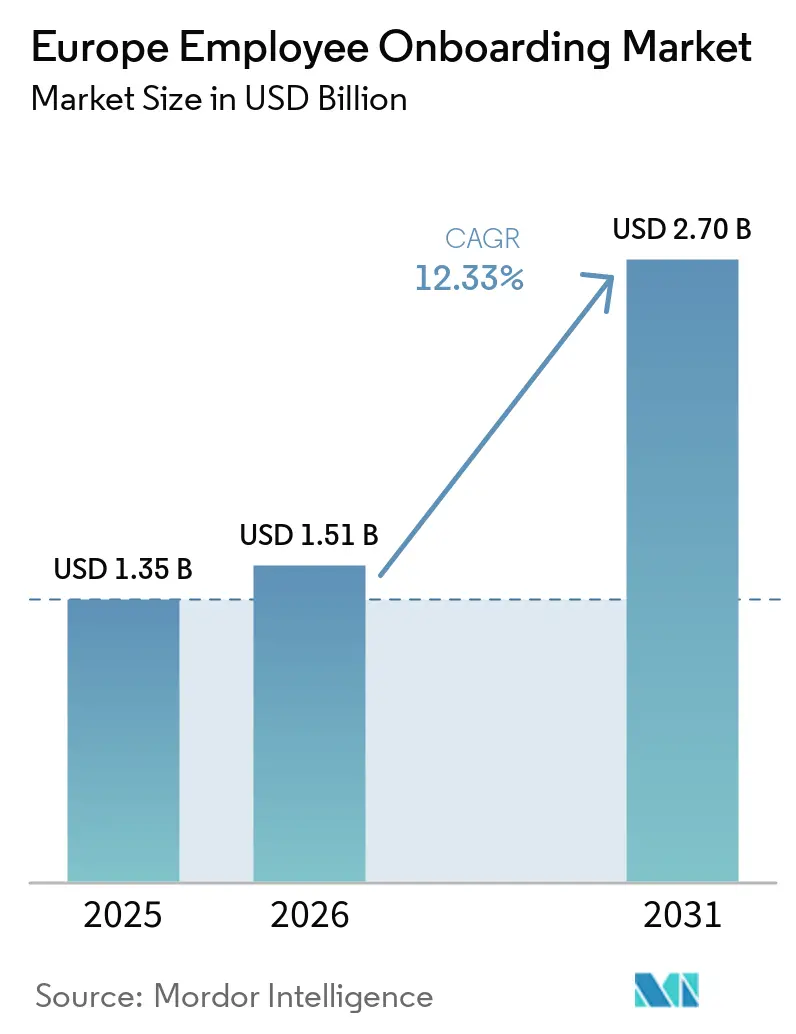

| Base Year Market Size (2025) | USD 1.35 Billion |

| Market Size (2026) | USD 1.51 Billion |

| Market Size (2031) | USD 2.70 Billion |

| Growth Rate (2026 - 2031) | 12.33% CAGR |

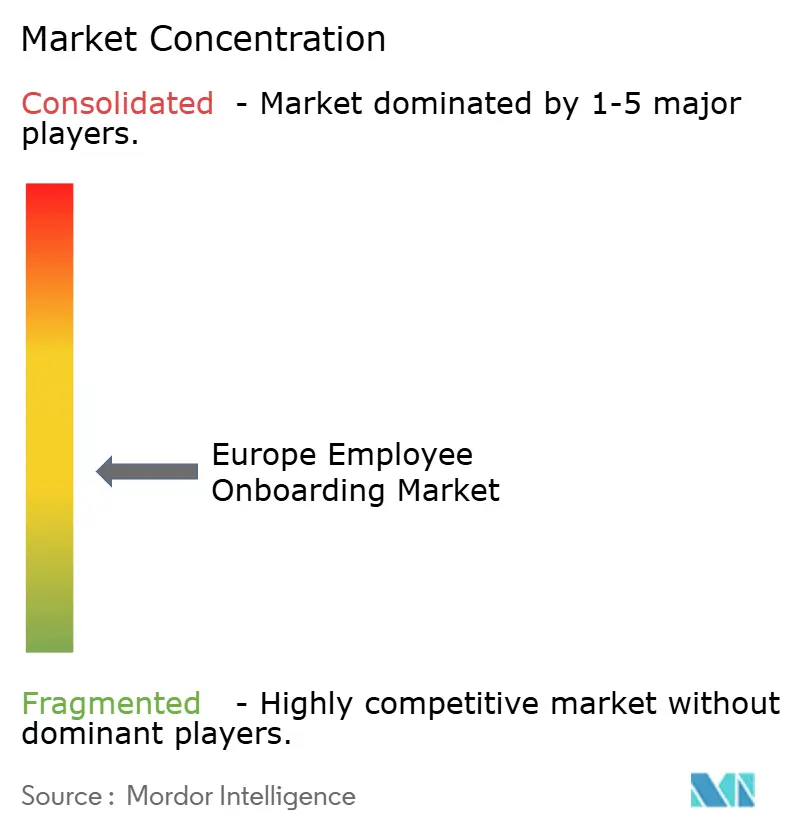

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Employee Onboarding Market Analysis by Mordor Intelligence

The Europe employee onboarding market size is projected to be USD 1.35 billion in 2025, USD 1.51 billion in 2026, and reach USD 2.70 billion by 2031, growing at a CAGR of 12.33% from 2026 to 2031. The Europe employee onboarding market is moving through a structural replacement cycle as employers retire paper-heavy processes and adopt connected digital workflows that support consent capture, document handling, audit trails, and cross-border hiring within a single operating model. Regulatory pressure is reinforcing that shift because employers now need systems that can handle GDPR obligations, prepare for pay transparency, and conduct sector-specific credential checks without creating manual work at each local office. Competition remains moderately fragmented, with European-native vendors competing on localization and compliance depth, while U.S.-headquartered platforms are investing in EU data residency and certification to stay relevant in regulated buying cycles. The Europe employee onboarding market is also being shaped by practical architectural choices, as many organizations are not moving to full cloud environments and instead are building hybrid models around legacy HR, payroll, and IT systems. The medium-term opportunity centers on platforms that combine verified digital identity, credential portability, analytics, and compliance document management to improve first-day readiness and give people teams stronger visibility into early retention outcomes.

Key Report Takeaways

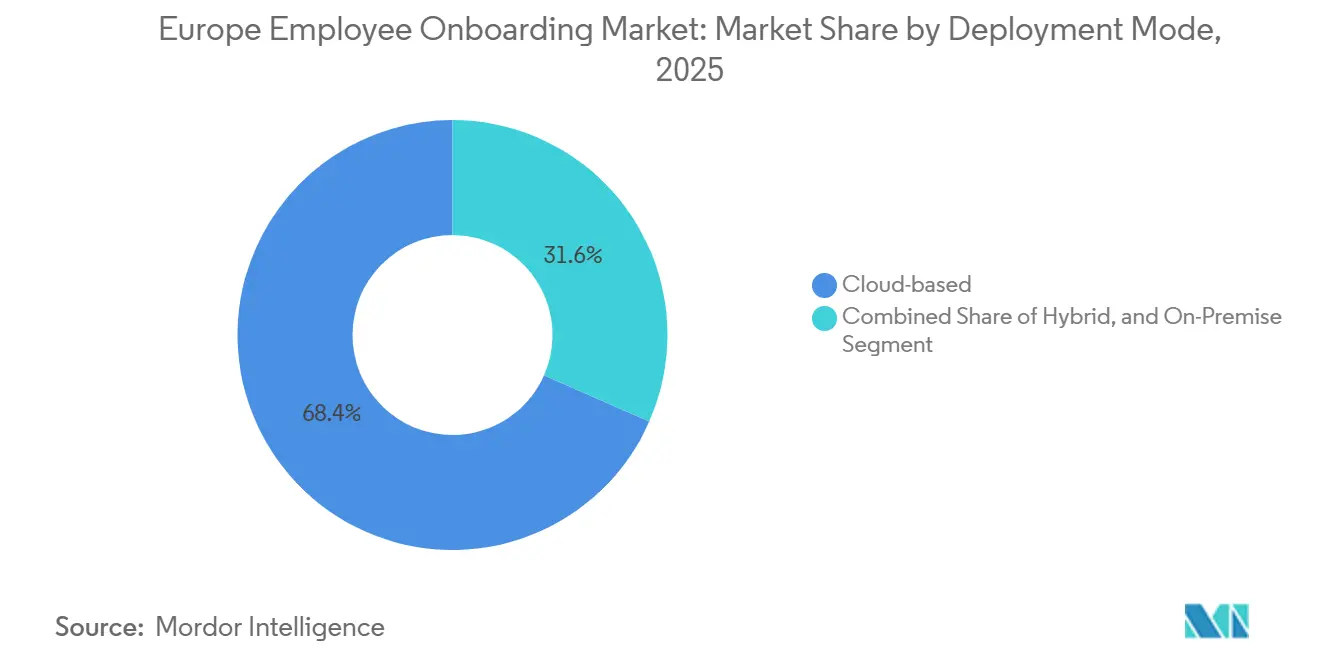

- By deployment mode, cloud-based deployment accounted for 68.41% of total revenue in 2025, while hybrid is projected to expand at a 13.82% CAGR through 2031 in the Europe employee onboarding market.

- By end-user enterprise size, large enterprises accounted for 61.29% of total revenue in 2025, while small and medium-sized enterprises are projected to grow at a 15.47% CAGR through 2031.

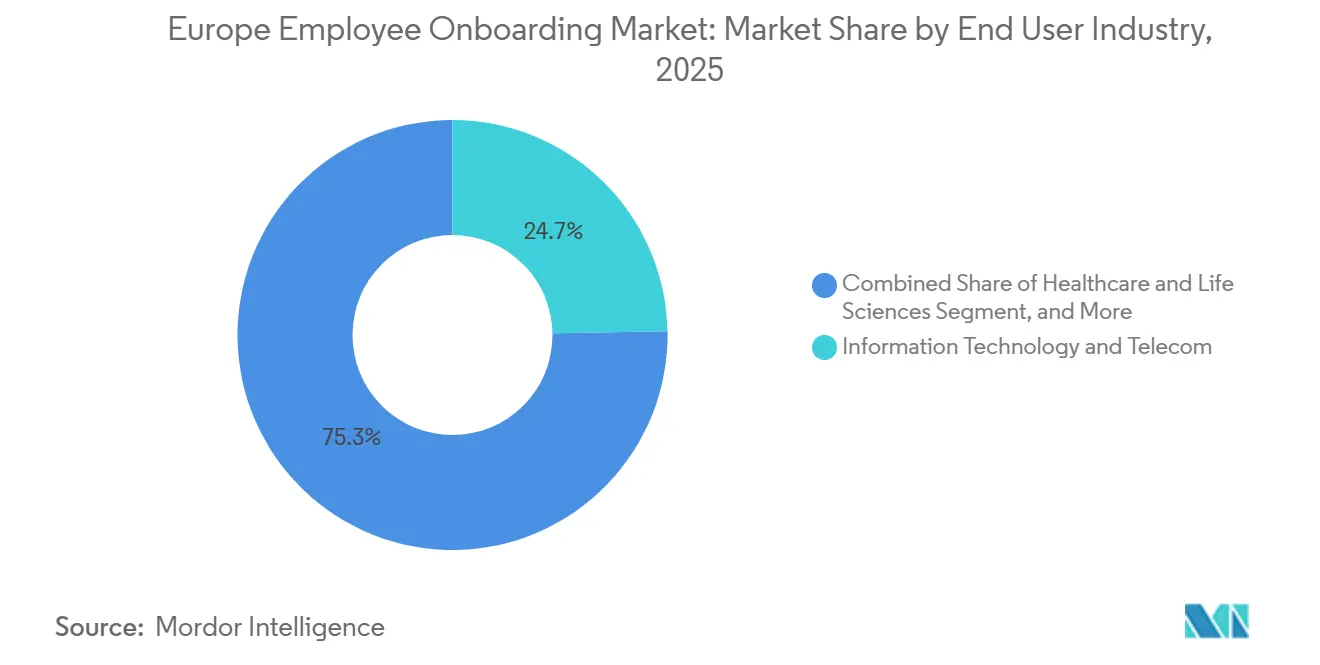

- By end user industry, Information Technology and Telecom represented 24.73% of revenue in 2025, while Healthcare and Life Sciences are projected to expand at a 16.29% CAGR through 2031.

- By functionality, Workflow Automation and Task Orchestration accounted for 22.87% of revenue in 2025, while Analytics and Progress Tracking are projected to grow at a 17.64% CAGR through 2031.

- By geography, the United Kingdom held 21.49% of the Europe employee onboarding market in 2025, while Germany is projected to record the highest CAGR at 14.92% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Employee Onboarding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for GDPR-compliant and multilingual onboarding | +2.3% | Pan-European, particularly acute in DACH, France, and the Nordics | Short term (≤ 2 years) |

| Shift from manual HR administration to automated workflow orchestration | +2.0% | Pan-European, core impact in UK, Germany, and France | Medium term (2-4 years) |

| Stronger focus on early retention and employee experience | +1.7% | Pan-European, acute in UK, Germany, and Nordics | Medium term (2-4 years) |

| Need to coordinate HR, IT, and compliance tasks in one workflow | +1.4% | Pan-European, strongest uptake in large enterprise markets | Short term (≤ 2 years) |

| EU Pay Transparency Directive readiness reshaping hiring and onboarding data flows | +1.1% | EU member states, gold-plating in France, Lithuania, Ireland, and Denmark | Short term (≤ 2 years) |

| EUDI Wallet and verified digital credential adoption for faster identity checks | +0.7% | Pan-EU, deployment acceleration in Germany, Netherlands, and Austria | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for GDPR-Compliant and Multilingual Onboarding

European employers increasingly want onboarding systems that create a defensible record of consent, data minimization, and deletion handling, rather than tools that only automate forms and reminders. That requirement matters more in the Europe employee onboarding market because a single hiring process may involve several labor regimes, languages, and internal reviewers before a new hire is active. Vendors that built field-level encryption, tenant separation, and records support into their core architecture are taking share from generic HR products that treated privacy compliance as an afterthought. The multilingual requirement adds another layer of buyer urgency because employers operating across Germany, France, Spain, and the Netherlands need contracts, policies, and training content in local languages without maintaining manual versions of these documents. Digital adoption is still uneven across Europe, leaving room for GDPR-native platforms to replace manual workflows over time. 52.7% of EU enterprises used paid cloud computing services in 2025, and adoption still varied widely by enterprise type and country, according to EUROSTAT. That combination of privacy depth and language localization is giving specialized vendors a durable edge in the Europe employee onboarding market when procurement teams evaluate long-term compliance risk.[1]Eurostat, “Digitalisation in Europe - 2026 Edition,” European Commission Interactive Publications, ec.europa.eu

Shift From Manual HR Administration to Automated Workflow Orchestration

Operational breakdowns in sequential task handling are driving the automation case in Europe, because new-hire readiness depends on HR, IT, payroll, legal, and line managers acting simultaneously rather than in sequence. In the Europe employee onboarding market, a contract signature is increasingly expected to trigger downstream actions such as laptop provisioning, payroll setup, compliance enrollment, and manager notifications without manual chasing. That model aligns with the wider enterprise technology base now in place across Europe, where 52.7% of EU enterprises used paid cloud services in 2025, and 85% of large enterprises had already adopted cloud services. The practical effect is that onboarding ROI is no longer judged solely within HR, because delays in IT provisioning and identity setup are counted as real business costs at the point of deployment. Vendors that can sit above the ATS, HRIS, payroll, and IT stack, rather than asking buyers to replace them, are gaining traction because this lowers implementation risk within existing enterprise architectures. The Europe employee onboarding market is therefore rewarding orchestration layers that simplify task routing across systems rather than platforms that depend on a full replacement strategy.

Stronger Focus on Early Retention and Employee Experience

Employers are treating early attrition as a measurable business problem, pushing onboarding from an administrative process into a retention program in the Europe employee onboarding market. A 2025 survey of 1,000 HR leaders found that 60.8% said early attrition had increased over the previous 12 months, and 20.5% said that up to 50% of new hires left within their first 90 days. The same pressure is visible in technology hiring, where average attrition in European tech reached 17.4% in 2025, including 19% in the UK and 18% in Germany. Replacing an employee earning above GBP 26,000 (USD 33,330) could cost more than GBP 30,000 (USD 38,460), which makes structured onboarding easier to defend as a cost-avoidance investment. Another important point is that 82% of HR leaders in the survey cited lack of clarity around career progression as the top retention challenge, which means platforms that connect first-week workflows to goal-setting and development plans are becoming more valuable than tools focused only on day-one paperwork. The Europe employee onboarding market is therefore shifting toward platforms that can demonstrate how onboarding quality affects engagement, productivity, and retention in the first months of employment.[2]Ravio, “Retention Trends 2026: Attrition Rates Data and Employee Retention Strategies,” Ravio Compensation Trends Report, ravio.com

Need To Coordinate HR, IT, and Compliance Tasks in One Workflow

Onboarding failures often occur when task dependencies across departments are broken, which is why buyers increasingly want a single workflow record that assigns, tracks, escalates, and documents every required action. That need is especially strong in the Europe employee onboarding market because regulated employers cannot grant system or site access until compliance attestations, identity checks, and policy acknowledgments are complete. IT provisioning remains the most visible bottleneck, since a new hire who arrives without system access loses productive time on the first day and creates a poor early experience that can weaken engagement. Research published in 2026 found that AI-assisted onboarding reduced time-to-productivity by up to 60% and delivered savings above PLN 250,000 (USD 63,250) per deployment cycle, with automated document handling and real-time progress monitoring cited as major value drivers. That evidence strengthens the case for workflow platforms that connect HR and IT execution rather than treating them as parallel projects handled in separate systems. Vendors with pre-certified connectors to identity and access management tools are shortening deployment cycles in the Europe employee onboarding market by eliminating the need for expensive middleware design at the start of the project.[3]Zenodo, “Integration of AI Modules into Onboarding Processes: Methodology and Implementation Results in a Polish HR Agency,” Zenodo, zenodo.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration complexity across ATS, HRIS, payroll, and IT systems | -1.4% | Pan-European, most acute in large enterprise and multi-country deployments | Medium term (2-4 years) |

| Budget and change-management friction among small and medium-sized enterprises | -1.1% | Pan-European, particularly pronounced in Southern and Eastern Europe | Short term (≤ 2 years) |

| Works council consultation and country-specific labor rules extending rollout timelines | -0.8% | Germany, Netherlands, France, and Austria | Medium term (2-4 years) |

| Data sovereignty screening narrowing eligible vendor pools | -0.6% | DACH, France, Netherlands, and Nordic countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity Across ATS, HRIS, Payroll, and IT Systems

The biggest operational drag on adoption is not software selection, but the difficulty of connecting the onboarding layer to fragmented enterprise systems that were never designed to share data in a common format. In the Europe employee onboarding market, a multinational employer may use a single ATS, a single core HR system, different payroll providers by country, and a separate IT provisioning stack, which makes implementation a multi-stream integration project. When candidate data must be translated from the ATS into a new hire record, then again into payroll and IT systems, the cost and delay can become disproportionate to the platform license itself. Germany adds a specific friction point because DATEV remains deeply embedded in the Mittelstand payroll environment and often requires certified interface partners rather than generic API links. Data-model mismatches, such as different employee ID structures or classification rules, then force manual reconciliation, which puts administrative work back into a process the software was meant to simplify. The Europe employee onboarding market is favoring vendors that bring certified connectors to systems such as Workday, SAP SuccessFactors, DATEV, and AFAS because buyers want faster deployment and lower professional services exposure.[4]GFOS GmbH, “HR Software from Germany | Made in Germany,” GFOS, gfos.com

Budget and Change-Management Friction Among Small and Medium-Sized Enterprises

Small and medium-sized employers represent the fastest-growing segment, but they also face a steeper path to adoption because budgets, internal capacity, and software governance are usually far thinner than in enterprise accounts. Only 52% of EU SMEs used paid cloud services in 2025, compared with 85% among large enterprises, and SMEs reached a basic digital intensity of 71%, which remained well below the EU's 2030 target. That gap matters in the Europe employee onboarding market because even modest subscription fees can feel hard to justify for employers hiring only a few people each month. Change management is often the less visible obstacle, since the same HR manager may also handle office administration, policy updates, and manager support, leaving little time to drive a software rollout. The OnBoard project, which officially began in January 2026, is developing onboarding curricula and digital toolkits to help European SMEs build more structured practices. Vendors that offer pre-built templates, AI-assisted setup, and fast deployment tracks are converting that hesitation into a clearer time-to-value argument across the European employee onboarding market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Hybrid Adoption Reshapes The Cloud Migration Narrative

Cloud-based deployment held 68.41% of the Europe employee onboarding market size in 2025, while hybrid is projected to expand at a 13.82% CAGR through 2031. That lead reflected years of investment by European employers in SaaS platforms that package GDPR data residency, security certifications, and workflow tools as standard capabilities rather than optional add-ons. The Europe employee onboarding market still benefits from a favorable infrastructure base, as 52.7% of EU enterprises used paid cloud services in 2025, up 7.4 percentage points from 2023. The same dataset showed that cloud adoption among large enterprises had already reached 85%, which helps explain why higher-value buyers remain comfortable with hosted delivery models. Cloud, therefore, remained the default choice for organizations seeking faster deployment, lower internal maintenance costs, and easier multi-country rollouts within a single platform.

Hybrid, however, is growing faster because many employers are not abandoning cloud strategy; they are adapting it to regulated operating conditions and legacy system realities. In the Europe employee onboarding industry, hybrid design lets employers keep sensitive identity, document, or payroll steps in tightly controlled environments while still using SaaS workflows for collaboration and progress management. That approach fits sectors where sovereign hosting obligations, internal security policies, or critical infrastructure rules make a full cloud migration difficult to approve. It also suits enterprises that already invested heavily in on-premises HR or IT stacks and now want a layered transition rather than a disruptive replacement. The Europe employee onboarding market is therefore rewarding vendors that can support cloud, hybrid, and on-premises paths without forcing buyers into a single architecture that ignores procurement and compliance constraints.

By End User Enterprise Size: SMEs Emerge As The Structural Growth Engine

Large enterprises accounted for 61.29% of the Europe employee onboarding market size in 2025, while SMEs are projected to grow at a 15.47% CAGR through 2031. Large organizations held the lead because they face the hardest coordination burden, including cross-border hiring, multi-language contract generation, works council obligations, and deep integration across HR, payroll, identity, and compliance systems. In practical terms, structured onboarding for these employers is less a discretionary software purchase and more a control layer that reduces errors across complex hiring operations. The Europe employee onboarding market also remains enterprise-led because large buyers have budget capacity to absorb implementation services, policy redesign, and manager training alongside the software license. That scale advantage keeps enterprise demand strong even as vendors simplify implementation and broaden self-service features.

The faster expansion in SMEs reflects a different set of conditions, centered on lower entry barriers and a clearer link between onboarding quality and avoidable turnover. A 2025 survey showed that 20.5% of HR leaders said up to 50% of new hires left within the first 90 days, which makes even a smaller software investment easier to justify when early exits are frequent. A 2026 publication also showed that SME cloud adoption still trailed that of large enterprises by a wide margin, indicating substantial room for first-time digitalization across the smaller employer base. As pricing falls and setup becomes easier through templates and guided configuration, the Europe employee onboarding industry is turning SMEs from a peripheral segment into a core expansion field. That shift matters because vendors that win early among smaller employers can create long customer lifecycles before those organizations move into more complex workforce and compliance needs.

By End User Industry: Healthcare Compliance Pressure Accelerates Adoption

Information Technology and Telecom held 24.73% of the Europe employee onboarding market share in 2025, while Healthcare and Life Sciences are projected to grow at a 16.29% CAGR through 2031. Technology firms led because they continued to hire at scale, operate distributed teams, and adopt SaaS tools earlier than most other verticals, which made digital onboarding a natural extension of existing HR practices. High-volume recruiting also increased the value of automation in that segment, since manual coordination breaks down quickly when dozens or hundreds of hires move through the process simultaneously. The Europe employee onboarding market has therefore long found an early adoption base in Information Technology and Telecom, where digital process maturity was already well established. That maturity gave vendors a large installed base, but it does not mean the next wave of growth will come from the same vertical.

Healthcare and Life Sciences are moving faster because workforce credential portability, identity verification, and readiness for regulated environments are becoming central buying criteria. One example highlighted support for an AI-native platform that uses digital staff passports to verify identity, right-to-work status, and Core Skills Training Framework credentials in real time. That shows why healthcare buyers often need something more specialized than generic HR workflow automation, especially when a delayed credential check can postpone clinical deployment. BFSI also remains important because AML, training acknowledgment, and policy sign-off requirements create a strong case for consolidated compliance records, while manufacturing and government show steady demand with slower procurement cycles. Across these verticals, the Europe employee onboarding market increasingly favors vendors that combine workflow automation with security certifications, compliance attestations, and document control that can withstand regulated procurement scrutiny.

By Functionality: Analytics Becomes A Strategic Retention Tool

Workflow Automation and Task Orchestration held 22.87% of the European employee onboarding market size in 2025, while Analytics and Progress Tracking is projected to advance at a 17.64% CAGR through 2031. The leading functionality remained task orchestration because it solves the first and most visible operational problem: coordinating actions across HR, IT, payroll, managers, and compliance owners without relying on email or spreadsheets. Buyers still start platform evaluations with workflow capability because delayed tasks are easy to see, measure, and connect to new-hire readiness on day one. That is why the Europe employee onboarding market continues to treat automation as the initial buying trigger across most enterprise segments. The function also tends to anchor expansion, as once task routing is standardized, adjacent modules become easier to add within the same vendor relationship.

Analytics is growing faster because employers now want evidence that onboarding affects time-to-productivity, early attrition, and manager effectiveness after the first weeks of employment. One product update in April 2026 introduced an AI Copilot that could answer cross-module questions by linking engagement data, goal progress, and absence patterns, demonstrating how reporting is becoming a more active decision-support layer. That development fits a broader shift in the Europe employee onboarding market where HR teams need cohort-level visibility, not only completion dashboards, to justify recurring platform spend. Document Management and E-signature remain essential, especially as eIDAS-compliant qualified electronic signatures matter more in countries such as Germany, France, and Spain, while employee self-service reduces helpdesk load by allowing new hires to update records directly. The result is a market where workflow automation opens the door, but analytics increasingly determines whether a platform expands into a wider people operations role.

Geography Analysis

The United Kingdom held 21.49% of the Europe employee onboarding market share in 2025, which made it the largest country market in the region. That position reflected a mature HR technology environment, high SaaS adoption in financial and professional services, and the push for day-one written employment particulars under the Employment Rights Act 2025. Attrition in the UK technology sector reached 19% in 2025, keeping attention focused on onboarding quality as a retention lever rather than merely an administrative requirement. In practice, UK fintech, legal services, and healthcare employers are leaning toward platforms that combine right-to-work verification, background-check management, and workflow automation into a single operating layer. France and the Netherlands also stand out because local implementation of pay transparency and employee consultation rules is increasing demand for platforms that can store, version, and audit pay-related hiring documentation from the first point of hire.

Germany is projected to grow at a 14.92% CAGR through 2031, making it the fastest-growing geography in the Europe employee onboarding market. The main driver is the large Mittelstand base, which had lagged larger Western European peers in HR software adoption and is now moving more decisively toward cloud-native and hybrid HR stacks. Germany also illustrates how local integration and labor-process design can influence vendor success, especially when buyers expect DATEV compatibility and localized documentation for works council review. Italy showed improving infrastructure readiness, with enterprise cloud adoption reaching 76% in 2025, which signals that one of the earlier barriers to software rollout is weakening.

Spain adds another layer of demand because higher workforce mobility increases the value of a stronger pre-boarding and first-month experience, especially where offer-to-start drop-off and early exits remain costly. The Nordic countries, led by Sweden, Finland, and Denmark, remain the most digitally mature sub-region for complex onboarding requirements across municipal government, health services, and defense-related employers. That maturity supports demand for platforms that can standardize onboarding across many sites, job roles, and compliance conditions without losing local traceability. Russia remained peripheral for Western-origin vendors in the Europe employee onboarding market because sanctions and data transfer restrictions continued to limit practical commercial scope.

Competitive Landscape

The Europe employee onboarding market remains moderately fragmented, and no single vendor holds a dominant position across all countries, regulatory settings, and enterprise tiers. European-origin platforms retain an advantage in many public-sector and regulated-industry evaluations because they were designed from the outset around GDPR-native architectures, localized labor practices, and multilingual support. U.S.-headquartered vendors remain active competitors, but many are having to strengthen EU data residency, certification, and governance features to stay credible in procurement cycles that place compliance risk close to the center of the decision. The main strategic pattern is platform expansion, with vendors extending from onboarding into performance, engagement, learning, analytics, and adjacent HR operations to displace narrower point solutions. That broader product logic is reshaping the Europe employee onboarding market because customers increasingly prefer suites that can connect recruiting, onboarding, employee development, and workflow analytics in one commercial relationship.

Greenhouse Software provided clear examples of that approach in 2026. In May 2026, it announced an agreement to acquire Ezra AI Labs, deepening its AI interviewing and structured assessment capabilities before onboarding begins. In the same month, it launched the Model Context Protocol, which provides enterprise customers with a governed way to connect external AI tools to hiring and onboarding data, with organization-level controls. The message behind both moves is that vendors now compete not only on workflow depth, but also on how safely their systems can support AI-enabled operating models in sensitive enterprise environments.

Regional consolidation is also changing the shape of competition. A merger completed in January 2026 created a combined Nordic HR technology group serving nearly 4,000 customers and 1.2 million users, with combined revenue of NOK 700 million (USD 63 million). Leapsome's April 2026 product release added a cross-module AI Copilot and workflow design tools, showing how vendors are trying to turn onboarding data into a broader operating system for people teams. These moves show that the Europe employee onboarding market still has room for specialized positions in SME workflows, digital identity, and credential management, but larger vendors are moving quickly to close open product gaps. Procurement screens are also tightening, meaning certifications such as ISO 27001 are increasingly required before commercial differentiation can even begin.

Europe Employee Onboarding Industry Leaders

Factorial HR, S.L.

Hi Bob Limited

BambooHR LLC

Talentech Group AS

Personio SE and Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Greenhouse Software agreed to acquire Ezra AI Labs, adding voice AI interviewing to strengthen talent-matching; deal closes Q2 2026.

- May 2026: Greenhouse Software launched Greenhouse MCP, a governed framework for connecting third-party AI tools to hiring and onboarding data.

- April 2026: Leapsome released an AI Copilot for HR actions and a Timeline Canvas to streamline onboarding workflow setup.

- March 2026: Greenhouse Software launched Hire Link for Workday, automating new hire data transfer to initiate onboarding workflows.

Europe Employee Onboarding Market Report Scope

The European employee onboarding market comprises technology platforms and services that automate and optimize the integration of new employees into organizations across the region. These solutions cover functionalities such as workflow automation and task orchestration, document management and e-signature, learning and training management, compliance and policy acknowledgment, analytics and progress tracking, and employee self-service and communication. Delivered through cloud-based, on-premises, and hybrid deployment models, they serve both large enterprises and small and medium-sized enterprises across industries, including BFSI, healthcare and life sciences, information technology and telecom, retail and e-commerce, industrial manufacturing, government and public sector, and other end-user industries. The core purpose of this market is to help organizations in Europe streamline onboarding processes, ensure compliance, enhance employee experience, and accelerate workforce productivity through digital automation and data-driven insights.

The Europe employee onboarding market report is segmented by Deployment Mode (Cloud-based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-sized Enterprises), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, and Government and Public Sector), Functionality (Workflow Automation and Task Orchestration, Document Management and E-signature, Learning and Training Management, Compliance and Policy Acknowledgment, Analytics and Progress Tracking, and Employee Self-service and Communication), and Geography (United Kingdom, Germany, France, Italy, Spain, Russia, Netherlands, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-based |

| On-premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| Workflow Automation and Task Orchestration |

| Document Management and E-signature |

| Learning and Training Management |

| Compliance and Policy Acknowledgment |

| Analytics and Progress Tracking |

| Employee Self-service and Communication |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Russia |

| Netherlands |

| Rest of Europe |

| By Deployment Mode | Cloud-based |

| On-premises | |

| Hybrid | |

| By End User Enterprise Size | Large Enterprises |

| Small and Medium-sized Enterprises | |

| By End User Industry | BFSI |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Retail and E-commerce | |

| Industrial Manufacturing | |

| Government and Public Sector | |

| Other End-user Industries | |

| By Functionality | Workflow Automation and Task Orchestration |

| Document Management and E-signature | |

| Learning and Training Management | |

| Compliance and Policy Acknowledgment | |

| Analytics and Progress Tracking | |

| Employee Self-service and Communication | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe |

Key Questions Answered in the Report

What is the size of the Europe employee onboarding market?

The Europe employee onboarding market stood at USD 1.51 billion in 2026 and is forecast to reach USD 2.70 billion by 2031, growing at a 12.33% CAGR over 2026-2031.

Which deployment model leads in Europe employee onboarding software?

Cloud-based deployment led with 68.41% of revenue in 2025, although hybrid is expected to grow faster through 2031 as employers balance cloud adoption with data residency and legacy system needs.

Why are SMEs becoming important buyers of onboarding platforms in Europe?

SMEs are projected to grow at a 15.47% CAGR through 2031 because pricing is becoming more accessible, setup is getting easier, and employers are placing more value on reducing early attrition and manual work.

Which vertical is expected to grow the fastest through 2031?

Healthcare and Life Sciences is projected to expand at a 16.29% CAGR through 2031, supported by credential verification needs, workforce portability, and stricter compliance requirements.

What functionality is gaining the most momentum in onboarding platforms?

Analytics and Progress Tracking is the fastest-growing functionality, with a 17.64% CAGR through 2031, because employers want visibility into time-to-productivity, task completion, and early attrition signals.

Which countries are shaping regional demand the most?

The United Kingdom held the largest share at 21.49% in 2025, while Germany is forecast to grow the fastest at a 14.92% CAGR through 2031 as the Mittelstand accelerates HR software modernization.

Page last updated on: