Europe Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

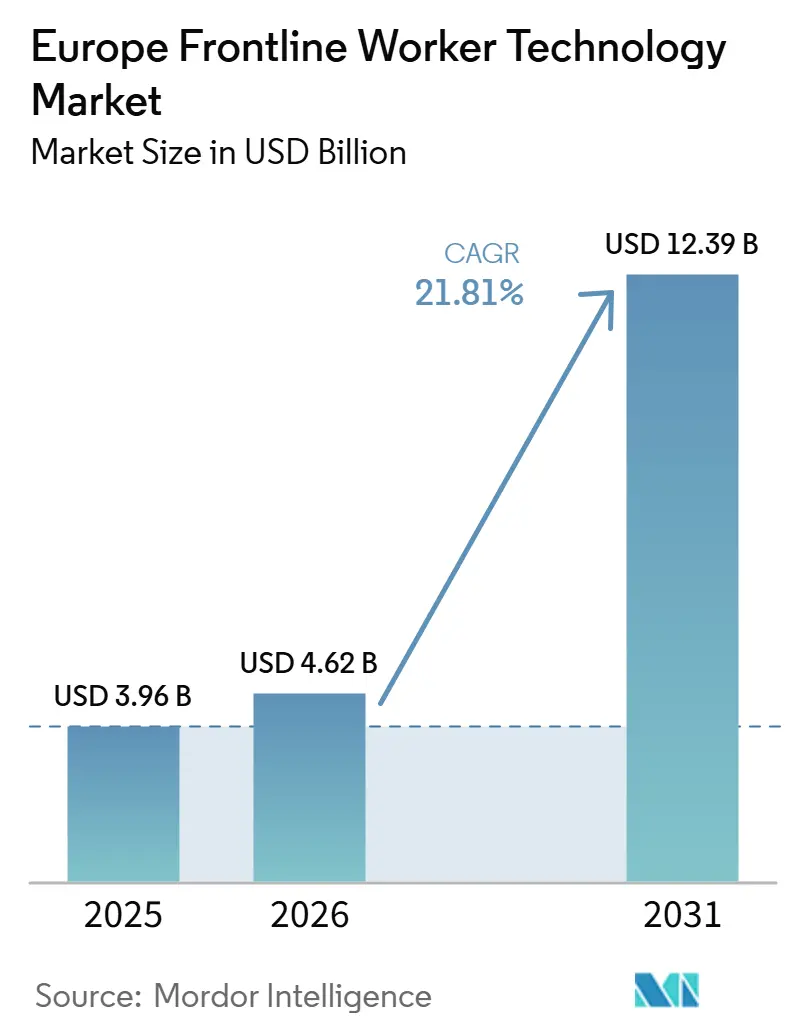

| Base Year Market Size (2025) | USD 3.96 Billion |

| Market Size (2026) | USD 4.62 Billion |

| Market Size (2031) | USD 12.39 Billion |

| Growth Rate (2026 - 2031) | 21.81% CAGR |

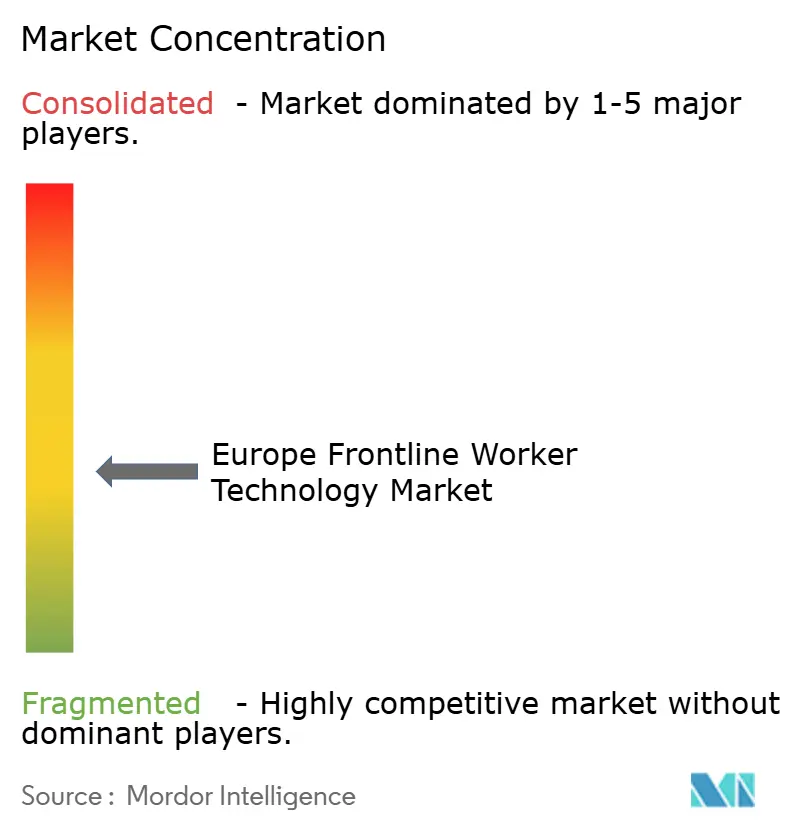

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Frontline Worker Technology Market Analysis by Mordor Intelligence

The Europe frontline worker technology market size is projected to be USD 3.96 billion in 2025, USD 4.62 billion in 2026, and reach USD 12.39 billion by 2031, growing at a CAGR of 21.81% from 2026 to 2031. The Europe frontline worker technology market is moving from fragmented paper-based and radio-based workflows toward mobile platforms that combine communication, scheduling, task execution, and reporting for deskless workers. Adoption is rising because large employers now need faster handovers, clearer safety communication, and stronger operational visibility across distributed sites, especially where corporate email and desktop access are limited. The market also benefits from the spread of cloud delivery, which makes compliance updates and remote administration easier across multiple countries and facilities. Vendor strategy is shifting toward platform depth, with hardware firms adding software layers and enterprise software providers building dedicated frontline products instead of treating frontline use cases as extensions of office tools. Regulatory review still slows some rollouts, but that same pressure is increasing demand for platforms that support audit trails, privacy controls, and localized workflow rules across the Europe frontline worker technology market.

Key Report Takeaways

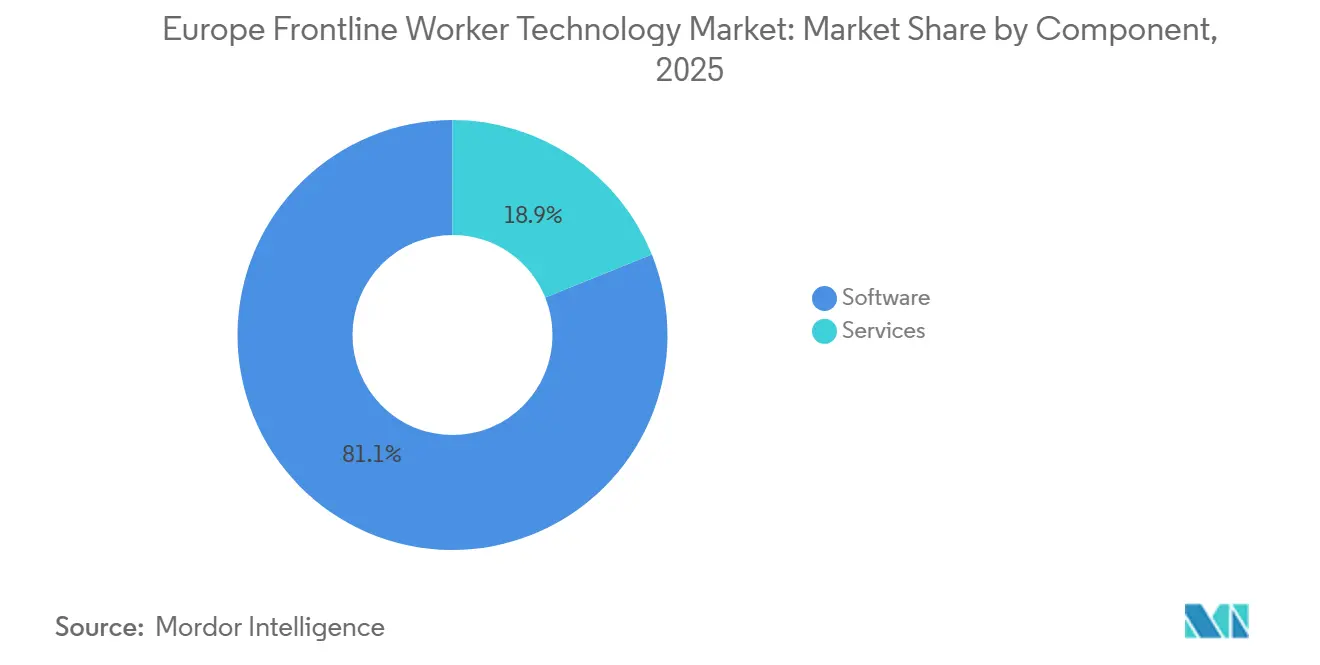

- By component, software held 81.11% share in the Europe frontline worker technology market in 2025, while services are projected to expand at a 22.41% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 76.61% of the market share in 2025 and is projected to record the highest CAGR of 23.16% through 2031.

- By organization size, large enterprises held 69.66% share in 2025, while small and medium enterprises are projected to grow at a 24.89% CAGR through 2031.

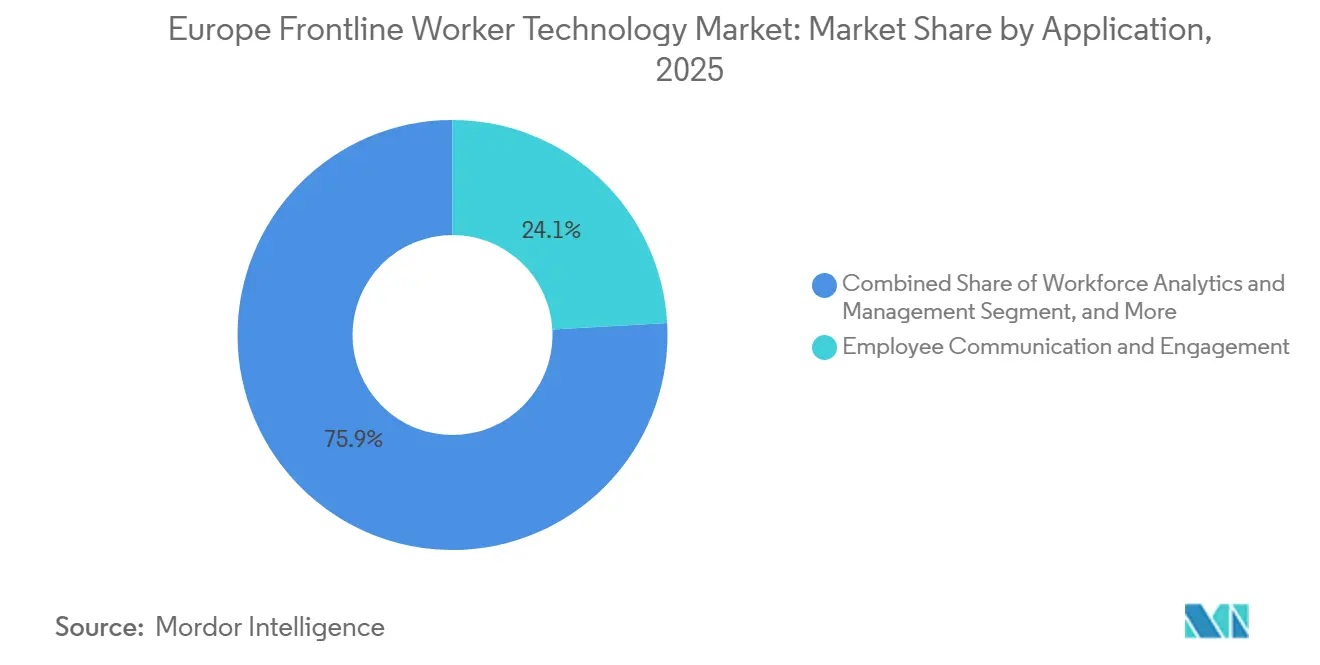

- By application, employee communication and engagement held 24.11% share in 2025, while workforce analytics and performance management is projected to advance at a 26.72% CAGR through 2031.

- By end-user industry, industrial manufacturing led with 29.11% share in 2025, while transportation and logistics is projected to expand at a 28.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Mobile-First Operational Software | +5.8% | Western Europe, especially Germany, the UK, France, and Benelux | Short term (≤ 2 years) |

| Real-Time Communication and Task Orchestration Demand | +4.5% | Western Europe core with expansion into Central and Eastern Europe | Short term (≤ 2 years) |

| AI-Assisted Scheduling and Exception Management | +3.6% | Germany, France, Nordics, with additional uptake in Spain and Benelux | Medium term (2-4 years) |

| Worker Safety, Traceability, and Audit-Ready Workflows | +2.2% | EU-wide, with stronger pressure in Germany, the UK, and France | Medium term (2-4 years) |

| Labor Shortages and Retention Pressures | +1.8% | Germany, Austria, the Netherlands, and Nordics | Medium term (2-4 years) |

| Rugged Devices, Wearables, and Connected PPE Adoption | +1.1% | Germany, the UK, and Nordics in heavy industry and energy | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Mobile-First Operational Software Across Retail, Healthcare, Manufacturing, and Logistics

The Europe frontline worker technology market is gaining from the replacement of fixed-terminal workflows with mobile tools that put instructions and updates directly in workers' hands. Microsoft expanded its frontline offering in 2026 with Frontline Hub, Smart Scheduling in Shifts, the Communicator App, and voice-driven capabilities in Frontline Agent, showing that frontline workflows now sit closer to the center of product roadmaps rather than at the edge.[1]Microsoft Corporation, “Introducing New Frontline Innovations at Microsoft 365 Community Conference,” Microsoft Tech Community, microsoft.com Honeywell also moved in the same direction with Performance+ for Guided Work, which combined voice-driven task guidance with analytics across warehousing, retail, and logistics environments and supported 48 languages. This shift matters because mobile-first systems reduce delays between instruction, execution, and confirmation, which is especially valuable in busy facilities with temporary staff and multiple shifts. TeamViewer reported that Vandemoortele reduced temporary worker training time by 25% after deploying vision-picking workflows across 6 warehouse sites, demonstrating how mobile and assisted workflows are becoming direct labor productivity tools in the Europe frontline worker technology market.

Rising Demand For Real-Time Communication and Task Orchestration Among Deskless Teams

Real-time communication remains a basic need because many frontline employees still work without the digital channels that office staff use every day. The Europe frontline worker technology market is therefore seeing stronger demand for platforms that combine messaging, task assignment, acknowledgment, and escalation in one mobile interface. LumApps stated in 2025 that the combined LumApps AI Employee Hub and Beekeeper platform served more than 7 million users across more than 2,000 organizations and supported more than 200 languages, underscoring the scale of multilingual frontline communication demand in Europe.[2]LumApps, “Beekeeper Is Now Part of LumApps | Frontline Platform,” LumApps, lumapps.com UKG found in March 2026 that 75% of frontline workers said technology had made it easier to manage their work schedules, but 64% still worked voluntary overtime, suggesting that better communication tools improve workflow clarity even when staffing pressure remains. As operations become more distributed, vendors that tie communication to real-time execution are gaining ground in the Europe frontline worker technology market because buyers want fewer handoff gaps and clearer accountability at the site level.

Expansion of AI-Assisted Scheduling, Task Prioritization, and Exception Management

AI-assisted scheduling is moving into mainstream use cases where labor rules, skill constraints, and demand changes need to be managed within a single workflow. A 2025 European Parliament Research Service study found that 69% of EU firms already used instruction tools such as scheduling and task allocation platforms, and it also showed meaningful exposure to algorithmic management in transport and healthcare. Fraunhofer IPK presented the STARK project in March 2026 as an AI-assisted knowledge transfer and scheduling system for manufacturing workers, linking workforce planning to the growing need to preserve know-how as experienced staff retire.[3]Fraunhofer Institut für Produktionsanlagen und Konstruktionstechnik, “Ein Buddy Für Den Wissenstransfer, STARK-Projekt,” Fraunhofer IPK, fraunhofer.de ServiceNow introduced this direction at Hannover Messe 2026 with Industrial Connected Workforce, which connected plant workers to enterprise systems via conversational interfaces in Microsoft Teams or kiosks. The Europe frontline worker technology market is therefore moving beyond digital communication alone and toward automated prioritization, guided action, and exception handling that can support both operational continuity and labor-rule complexity.

Compliance Pressure Around Worker Safety, Traceability, And Audit-Ready Workflows

Compliance is becoming a direct buying reason because employers need clearer evidence of what was assigned, what was completed, and how safety procedures were followed. The Europe frontline worker technology market is seeing this most clearly in manufacturing, construction, food processing, and regulated logistics settings where audits are frequent and documentation standards are strict. The Datenfabrik.NRW initiative deployed 51 applications across factory settings with support from Fraunhofer institutes and companies, including CLAAS and Schmitz Cargobull, showing that digital guidance, planning, and compliance support are being embedded into shop-floor operations rather than being kept as side tools.[4]it’s OWL Technologienetzwerk, “Datenfabrik.NRW, How CLAAS and Schmitz Cargobull Are Bringing AI into the Factory Floor,” it’s OWL Technologienetzwerk, its-owl.de RealWear documented in May 2026 that Prysmian Group used its headset with OverIT's SPACE1 augmented reality application for remote acceptance testing and knowledge transfer, improving documentation quality while reducing the need for expert travel. These use cases show why compliance is not only a restraint through regulation; it is also a growth factor in the Europe frontline worker technology market, as digital records reduce operational and inspection risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR and Worker Privacy Constraints | -1.8% | EU-wide, with stronger friction in Germany and France | Short term (≤ 2 years) |

| Fragmented Legacy IT Environments | -1.3% | Eastern and Southern Europe and mid-market users in Western Europe | Medium term (2-4 years) |

| Union and Works Council Resistance | -0.9% | Germany, France, Austria, and Benelux | Medium term (2-4 years) |

| Interoperability Gaps Across Devices and Enterprise Systems | -0.7% | Multi-site and multi-vendor deployments across Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

GDPR and Worker Privacy Constraints on Location, Behavior, and Performance Monitoring

Privacy rules continue to slow deployments that involve platforms collecting detailed data on worker behavior, location, or output. The Europe frontline worker technology market is responding by shifting product design toward smaller data footprints, clearer permission structures, and stronger audit controls. The broader regulatory setting is reinforced by European debate around algorithmic management and worker protections, which the European Parliament Research Service highlighted as an expanding issue across the workplace. This means vendors cannot rely solely on feature depth, because buyers now ask whether monitoring functions can be configured to meet local legal and labor expectations. Procurement, therefore, takes longer in parts of the Europe frontline worker technology market, but privacy-by-design products are also gaining an advantage because they reduce compliance uncertainty during rollout.

Fragmented Legacy IT Environments Increase Integration Time And Deployment Cos

Many employers still run older ERP, warehouse management, and human capital systems that were never designed to work smoothly with modern frontline tools. That raises deployment costs because new applications must connect to multiple systems of record before they can automate tasks or report at scale. SD Worx identified fragmented systems and limited integration capability as major barriers to workforce planning progress in Europe, which aligns with the slower pace of change in organizations with mixed technology stacks. Zebra addressed this issue in June 2026 with Workcloud Integration and Orchestration, a standardized layer that connects workforce applications to core business systems, such as point-of-sale tools. Even with more integration tooling, the European frontline worker technology market still faces slower adoption where multi-site operations use different software versions across countries and facilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leads Revenue While Services Gain Strategic Weight

Software accounted for 81.11% of the market in 2025, making it the largest component of the Europe frontline worker technology market. That position reflected strong adoption of workflow management platforms, communication tools, and software-as-a-service scheduling systems that scaled quickly as cloud deployment became easier. At the same time, services are projected to grow at a 22.41% CAGR through 2031, indicating that implementation work is becoming increasingly important as buyers move from pilots to broader rollouts. The Europe frontline worker technology market size for software remained well ahead of services in 2025, but new revenue growth is spreading into deployment support, localization, and change management as use cases become more complex. This pattern shows that software is still the core commercial layer, while service depth often determines how much value large buyers can unlock after purchase.

ATOSS Software SE reported FY2025 revenue of EUR 189.3 million (USD 204.4 million), with cloud and subscription revenue up 28% year over year, which reflects demand for platform-led workforce solutions with recurring commercial models. Its customer base included large employers such as Deutsche Bahn, Lufthansa, and Decathlon, which illustrates how multi-country scheduling and staffing rules create a bigger role for implementation expertise. In the Europe frontline worker technology industry, service teams also act as account entry channels because they help vendors identify workflow gaps that can later support analytics or automation expansion. This gives local specialists an advantage where buyers need country-specific scheduling logic, multilingual rollout support, and alignment with local operating practices. The Europe frontline worker technology market therefore shows software dominance in terms of share, but service capability remains a major factor in account growth and retention.

By Deployment Mode: Cloud Expansion Reshapes Buying Priorities

Cloud-based deployment captured 76.61% of the market share in 2025, placing it clearly ahead of hybrid and on-premises approaches in the Europe frontline worker technology market. This reflected buyer preference for lower ownership cost, remote administration, and easier compliance updates across distributed sites. Cloud is also projected to grow at a 23.16% CAGR through 2031, keeping it both the largest and fastest-growing deployment model. Cloud-based systems accounted for 76.61% of the Europe frontline worker technology market in 2025, indicating a clear shift away from hardware-tied or site-bound software estates. The strong share position also suggests that many buyers now want faster rollout cycles and lower internal infrastructure burdens when extending tools to deskless workers.

Even so, hybrid deployment still holds strategic value in settings where security expectations, data residency needs, or operational sensitivity make full cloud use less practical. The installed base of on-premises systems remains meaningful in parts of Germany and France because long implementation cycles have created customized environments that are costly to replace quickly. Vendors with EU-hosted infrastructure and regional support teams are therefore more likely to pass procurement reviews in enterprise accounts seeking cloud flexibility without losing control over where operational data resides. In the Europe frontline worker technology industry, this creates a split between buyers that can move quickly to cloud and buyers that still need staged migration models. The Europe frontline worker technology market is thus consolidating around cloud delivery, while hybrid options remain important in regulated and security-conscious environments.

By Organization Size: Large Enterprises Still Dominate While SMEs Drive The Next Growth Wave

Large enterprises held 69.66% share in 2025, making them the main revenue base for the Europe frontline worker technology market. Their lead came from bigger deployment budgets, longer contracts, and stronger internal capacity to manage country-by-country rollouts and change programs. Small and medium enterprises are projected to grow at a 24.89% CAGR through 2031, indicating that adoption barriers are easing beyond the large-enterprise base. This gap between current share and future growth shows how the Europe frontline worker technology market is broadening from large complex buyers toward smaller organizations that previously lacked the budget or technical staff to buy full platforms. It also points to a change in vendor pricing and packaging, as cloud delivery has reduced per-seat and implementation costs for smaller teams.

The input also shows that labor shortages are pushing this shift, especially among mid-sized manufacturers and service operators that need better scheduling and productivity support. Wolt selected Legion's workforce management suite across EMEA, including labor budgeting, AI-driven demand forecasting, automated scheduling, and frontline communications, demonstrating that distributed, growth-stage businesses are moving directly to modern platforms rather than older workforce systems. The SME opportunity is especially important in Central and Southeastern Europe, where penetration remains low and future growth potential is tied to logistics expansion and manufacturing activity. Vendors that can simplify deployment, localize workflows, and reduce integration work are more likely to win these accounts. The Europe frontline worker technology market is therefore still funded by large enterprises today, but much of its next volume growth is likely to come from smaller employers.

By Application: Communication Holds The Largest Share While Analytics Gains Priority

Employee communication and engagement accounted for 24.11% of the market share in 2025, making it the leading application across the Europe frontline worker technology market. That leadership reflects the basic need to reach workers who do not use corporate email or desktop systems during their shifts. Workforce analytics and performance management are projected to grow at a 26.72% CAGR through 2031, making it the fastest-rising application as buyers seek clearer operational evidence from digital tools. Workforce analytics and performance management is projected to expand at a 26.72% CAGR in the Europe frontline worker technology market through 2031, indicating how quickly buyer focus is shifting from connection alone toward measurable performance visibility. This change suggests that many organizations first solved the communication gap and are now trying to understand what that new data can reveal about staffing, execution, and labor efficiency.

The middle tier of applications remains broad and commercially important. Workforce execution and task management serve retail and logistics buyers who need faster exception handling and more reliable in-shift follow-through. Workforce scheduling and coordination remain important, as labor-rule complexity and skill matching affect daily staffing quality, while learning and knowledge enablement are gaining relevance as older skilled workers retire and training cycles need to shorten. Safety and compliance management is also growing in high-risk settings because digital records support audits and site-level accountability. The Europe frontline worker technology market is therefore shifting from communication-first buying to broader application stacks that support both action and measurement.

By End-User Industry: Manufacturing Anchors Current Demand While Logistics Expands Faster

Industrial manufacturing held a 29.11% share in 2025, placing it at the center of the Europe frontline worker technology market. The segment benefits from recurring needs in shift handover, assembly guidance, quality documentation, and traceability across complex plants. Transportation and logistics are projected to grow at a 28.11% CAGR through 2031, which makes it the fastest-growing end-user vertical in the market. Industrial manufacturing held 29.11% of the Europe frontline worker technology market share in 2025, while transportation and logistics is projected to record the strongest expansion as digital workflows move deeper into fleet, warehouse, and fulfillment operations. This split shows that manufacturing still provides the revenue base, but logistics is now setting the pace for future adoption.

Concrete deployment examples support the manufacturing case. Uhlmann Pac-Systeme's SmartAssist AI solution won the Allianz Industrie 4.0 Award in Germany in 2025, demonstrating that assisted worker systems are already being used in practical industrial settings rather than kept as trial concepts. In logistics, Geotab reported in 2026 that 64% of European fleets used AI-powered route optimization and that 69% of enterprise fleets had reduced delivery times, reflecting a broader push toward real-time coordination and measurable operational gains. Descartes also reported in late 2025 that only 3% of European shippers had not yet adopted AI in their transport operations, indicating the depth of digital adoption in this vertical. The Europe frontline worker technology market is also active in retail, healthcare and life sciences, hospitality, construction, and government settings, but manufacturing and logistics currently set the main pattern for revenue scale and growth direction.

Geography Analysis

Germany held a 21.11% share in 2025, making it the largest country market in the Europe frontline worker technology market. Its position is tied to a large industrial base, multi-shift production environments, and labor frameworks that reward clearer scheduling records and audit-ready workflows. Public and private deployment activities also support this, as does the Datenfabrik. The NRW program involved 51 applications across factory operations with participation from firms such as CLAAS and Schmitz Cargobull. The United Kingdom sits on a different track because employers need scheduling flexibility and localized workforce management configurations that reflect a separate regulatory path. Legion's 2026 Frontline Workforce Index, based on 2,000 UK frontline workers, found that late-arriving rotas and short-notice shift changes were the main pain points, which supports demand for AI-driven scheduling tools.

France remains an important market because logistics density and employer consultation requirements both shape technology adoption. The Europe frontline worker technology market in France is seeing demand from logistics operators seeking better workforce enablement, but deployment timing can be affected by consultation processes for new workplace systems. Spain is emerging as a more visible opportunity, with vendors increasingly targeting logistics, warehousing, and manufacturing users that need shift scheduling and operational coordination. Russia appears in the regional framework used for market coverage, but cross-border procurement and data-transfer constraints have materially limited the role of Western-developed frontline platforms there. As a result, the more practical growth pattern in the Europe frontline worker technology market is being set by Western Europe and selected Central European economies rather than by Russia.

The rest of Europe is projected to grow at a 29.43% CAGR through 2031, making it the fastest-growing geographic grouping in the Europe frontline worker technology market. This area includes countries such as Poland, the Czech Republic, Romania, and the Netherlands, where e-commerce expansion, logistics investment, and manufacturing reshoring are increasing demand for frontline digitization. The rest of Europe is projected to advance at a 29.43% CAGR in the Europe frontline worker technology market, indicating growth is broadening beyond the traditional Western European core. ATOSS disclosed that only 6% of its revenue came from outside the DACH region in 2025, underscoring the untapped potential in wider Europe. The geography picture, therefore, combines a large German base, differentiated conditions in the UK and France, and the fastest future expansion in the wider regional group outside the biggest Western markets.

Competitive Landscape

The Europe frontline worker technology market is moderately fragmented, with competition spread across hardware-led vendors, workforce software specialists, and broad enterprise platform providers. The hardware-led group includes Zebra Technologies, Honeywell, and Panasonic, while the specialist software group includes ATOSS Software SE, Beekeeper under LumApps, and YOOBIC. A third layer comes from larger enterprise software names such as Microsoft, SAP, ServiceNow, and Oracle, which are extending existing customer relationships into frontline use cases. This structure means buyers often compare very different product starting points, from rugged devices and warehouse tools to workforce orchestration suites and collaboration platforms. The Europe frontline worker technology market, therefore, does not revolve around a single dominant vendor model because competition plays out across hardware depth, workflow fit, analytics capabilities, and integration strength.

A major theme in 2026 is the use of AI as a practical product layer rather than a branding message. Zebra launched Workcloud Business Intelligence and Workcloud Integration and Orchestration in June 2026 to add analytics and system connectivity above its existing device and workflow footprint. ServiceNow introduced Industrial Connected Workforce at Hannover Messe 2026 and continued expanding its Autonomous Workforce offer, signaling a clear push to connect frontline execution with broader enterprise workflows. Microsoft also strengthened its frontline product set in 2026 with Frontline Hub, Smart Scheduling, the Communicator App, and voice-led workflow features inside Teams. These moves show that leading vendors are trying to own the workflow layer that sits between enterprise systems and daily frontline activity.

ATOSS offers another strong example of strategic positioning, as it is further integrating AI into forecasting, planning, and automation while also growing its cloud and subscription base. White space remains in hospitality and construction, where buyers need frontline scheduling and compliance tools, but no vendor clearly dominates the segment across European small and mid-sized accounts. Emerging challengers such as Blink, Speakap, and Relesys are relevant because they focus on mobile-first communication and operations with lower rollout burden than some legacy workforce suites. TeamViewer also remains visible through connected worker deployments at European sites such as Vandemoortele, which support the view that assisted workflows can deliver measurable operating gains. The Europe frontline worker technology market is therefore becoming more competitive around integration, ownership, AI-supported workflows, and deployment simplicity rather than around hardware alone.

Europe Frontline Worker Technology Industry Leaders

Microsoft Corporation

SAP SE

Zebra Technologies Corporation

Honeywell International Inc.

Workday, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Zebra Technologies launched Zebra Nucleus, Workcloud Business Intelligence, and Workcloud Integration and Orchestration at its ZONE annual customer conference (June 1-4, 2026). Workcloud IO creates a standardized integration layer connecting frontline workforce management tools to core business systems including point-of-sale, enabling real-time task orchestration across retail and logistics sites.

- May 2026: ServiceNow expanded its Autonomous Workforce at Knowledge 2026 (Las Vegas), launching AI specialists for IT, customer relationship management, employee services, and security functions. Separately, at Hannover Messe 2026 (Germany), ServiceNow introduced Industrial Connected Workforce and EmployeeWorks, connecting factory-floor workers to enterprise workflows via Microsoft Teams or kiosk interfaces.

- May 2026: RealWear published a case study (May 22, 2026) documenting Prysmian Group's deployment of RealWear HMT-1 headsets running OverIT's SPACE1 augmented reality application to enable remote acceptance testing and knowledge transfers across industrial sites, reducing the need for expert travel and improving documentation accuracy.

- April 2026: SAP unveiled agentic AI solutions for manufacturing at Hannover Messe 2026, with AI agents linking development, planning, procurement, production, logistics, and service management into unified operations platforms. The solutions target European manufacturers moving from reactive ERP management to intelligent, real-time production orchestration.

Europe Frontline Worker Technology Market Report Scope

The Europe frontline worker technology market refers to the ecosystem of software and services designed to empower non-desk employees those who primarily execute their duties away from a traditional office setting. This includes tools that facilitate communication, task management, scheduling, knowledge sharing, and performance tracking for workers in sectors such as retail, manufacturing, healthcare, and logistics. The market encompasses cloud-based, on-premises, and hybrid deployment models tailored to the operational and security needs of organizations of varying sizes, from small and medium enterprises to large corporations. Key applications include workforce scheduling and coordination, safety and compliance management, and learning enablement, all aimed at improving operational efficiency, employee engagement, and real-time decision-making at the edge of business operations. The market scope is defined by the revenues generated by technology vendors and service providers across major European economies, including Germany, the United Kingdom, France, Russia, Spain, and the rest of the region.

The Europe Frontline Worker Technology Market Report is Segmented by Component (Software and Services), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises and Small and Medium Enterprises), Application (Employee Communication and Engagement, Workforce Execution and Task Management, Workforce Scheduling and Coordination, Learning and Knowledge Enablement, Workforce Analytics and Performance Management, Safety and Compliance Management, and Other Applications), End-User Industry (Retail and E-Commerce, Industrial Manufacturing, Healthcare and Life Sciences, Transportation and Logistics, Hospitality, Construction, Government and Public Administration, and Other Industries), and Geography (Germany, United Kingdom, France, Russia, Spain, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other Industries |

| Germany |

| United Kingdom |

| France |

| Russia |

| Spain |

| Rest of Europe |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other Industries | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the 2026 size of the Europe frontline worker technology space?

The Europe frontline worker technology market stood at USD 4.62 billion in 2026 and is forecast to reach USD 12.39 billion by 2031 at a 21.81% CAGR.

Which component leads revenue in Europe frontline worker technology?

Software led with 81.11% share in 2025, showing that workflow, scheduling, and communication platforms remain the main revenue base.

Which deployment model is expanding the fastest?

Cloud-based deployment led with 76.61% share in 2025 and is projected to grow at a 23.16% CAGR through 2031, supported by easier updates and remote administration.

Which application is growing the fastest across frontline platforms?

Workforce analytics and performance management is projected to grow at a 26.72% CAGR, reflecting rising demand for measurable labor and execution visibility.

Why is Germany the leading country in this space?

Germany held 21.11% share in 2025 because of its large industrial base, multi-shift operations, and strong need for traceable scheduling and workflow records.

What is slowing adoption for some employers in Europe?

Privacy rules, worker monitoring concerns, and legacy system integration issues are the main barriers, especially where older ERP and workforce systems still dominate daily operations.

Page last updated on: