Identity Verification For Employee Onboarding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.78 Billion |

| Market Size (2031) | USD 6.01 Billion |

| Growth Rate (2026 - 2031) | 16.67% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Identity Verification For Employee Onboarding Market Analysis by Mordor Intelligence

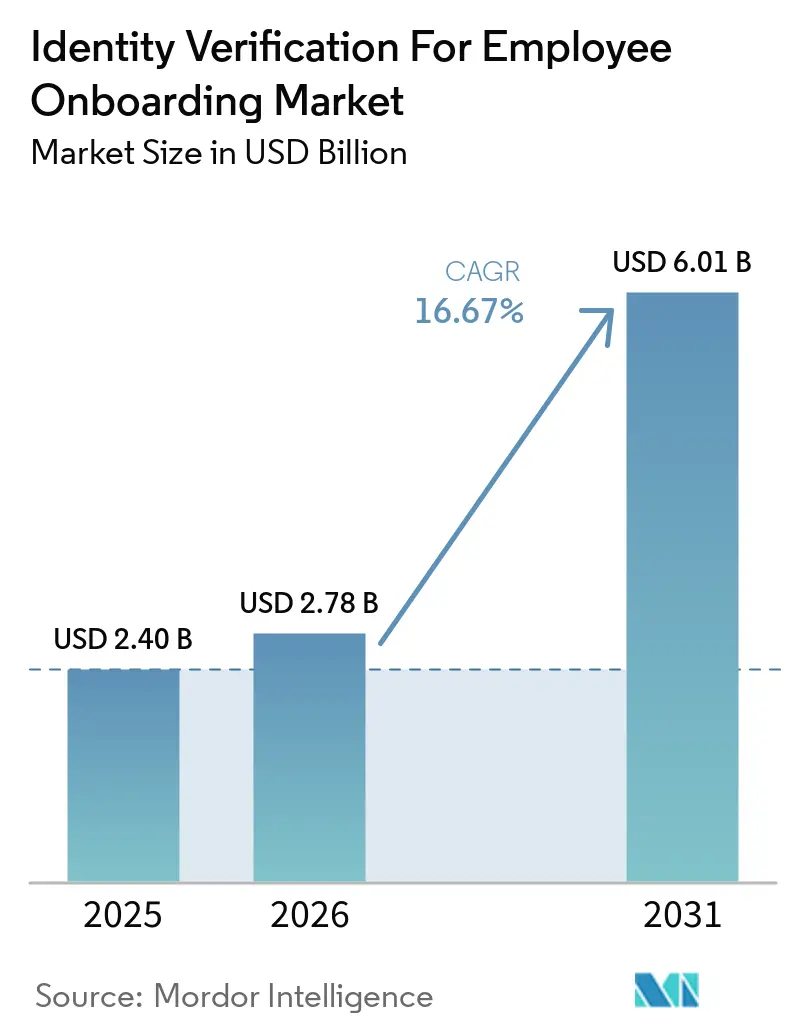

The identity verification for employee onboarding market size is expected to increase from USD 2.40 billion in 2025 to USD 2.78 billion in 2026 and reach USD 6.01 billion by 2031, growing at a CAGR of 16.67% over 2026-2031. The identity verification for employee onboarding market is being pushed forward by the lasting shift to remote and hybrid hiring, which has removed many in-person checks that once served as basic identity controls. The rise of synthetic identities and deepfake-enabled impersonation is also changing buying behavior, because employers now view onboarding fraud as a direct financial and security exposure rather than a narrow compliance task. The reported USD 25 million loss linked to a deepfake-enabled video call at Arup illustrates why employers are expanding identity controls across hiring, access, payroll, and account recovery workflows. Regional demand remains uneven, with North America benefiting from dense employment eligibility rules and biometric privacy laws, while Asia-Pacific is gaining momentum through government-backed digital identity systems. Competition is also shifting, as ATS and HRIS vendors embed verification hooks into core workflows, while leading providers are moving from one-time checks at hire toward reusable digital credentials and continuous identity intelligence across the workforce lifecycle.

Key Report Takeaways

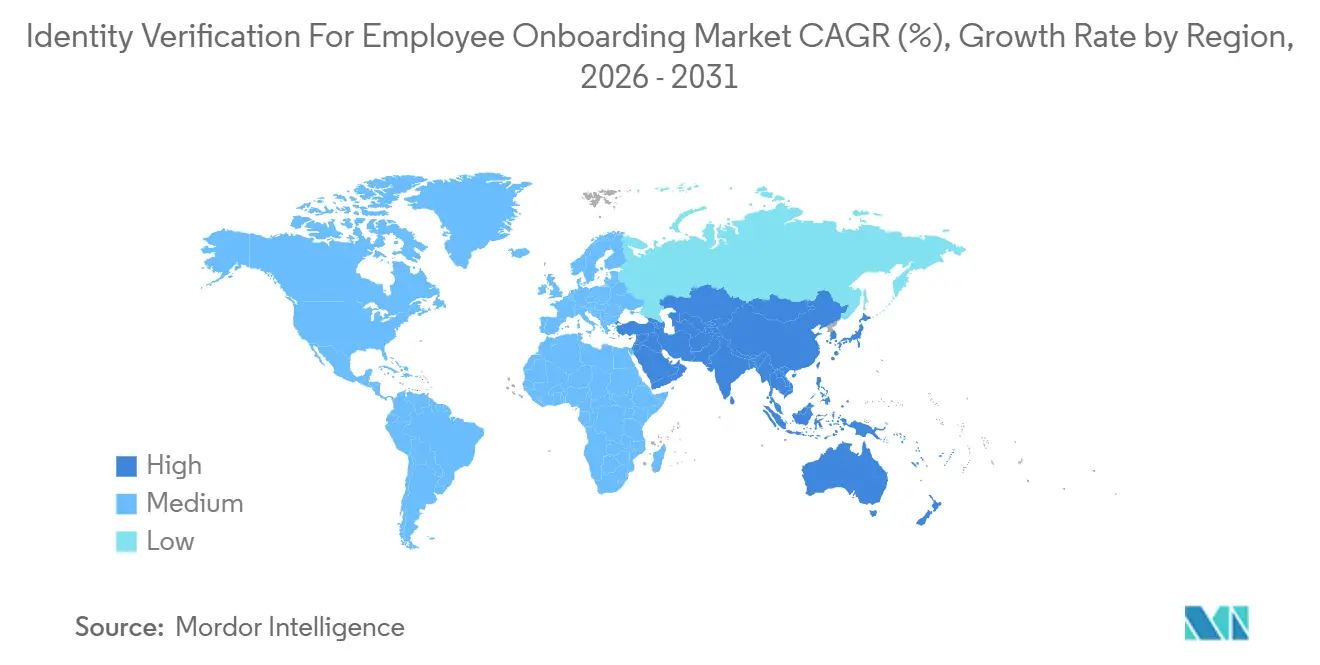

- By geography, North America held 39.71% of the identity verification for employee onboarding market in 2025, while Asia-Pacific is projected to record the fastest regional CAGR of 18.41% through 2031.

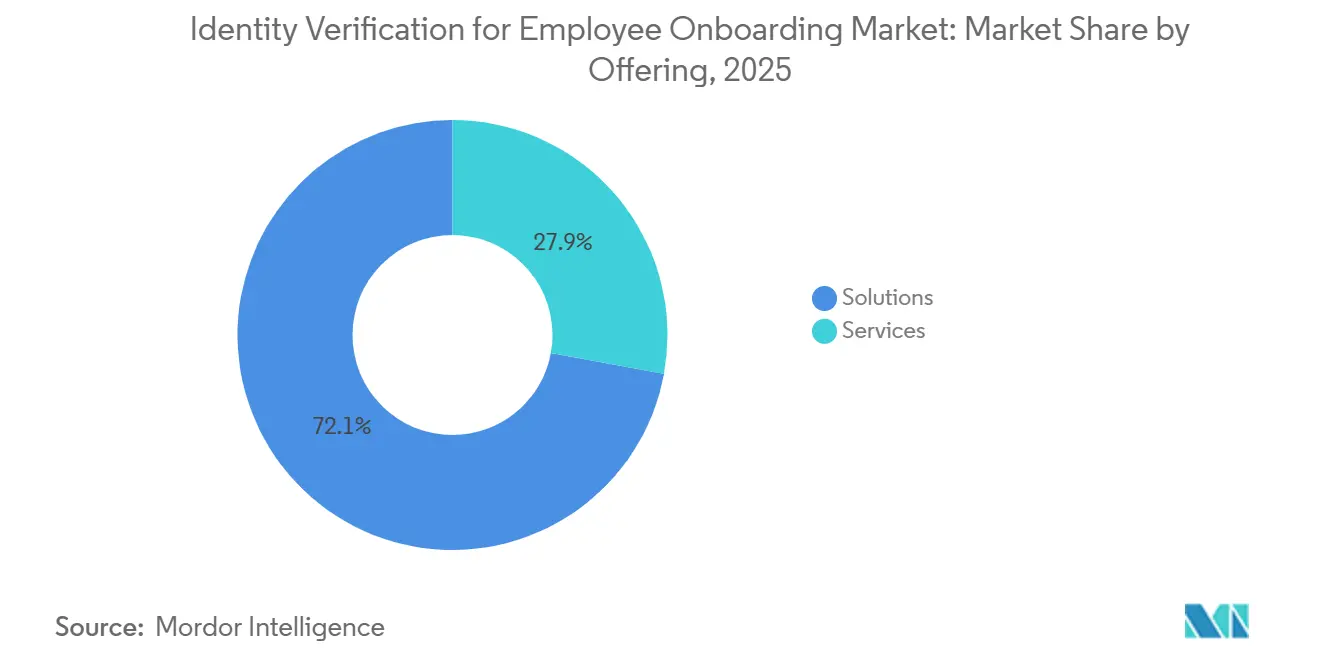

- By offering solutions led with a 72.12% share in 2025, while services are expected to expand at the fastest CAGR of 17.71% from 2026 to 2031.

- By deployment mode, cloud-based deployments accounted for 69.41% of the market in 2025, while hybrid deployments are projected to grow at a 16.73% CAGR through 2031.

- By end-user enterprise size, large enterprises held 63.29% share of the identity verification for employee onboarding market in 2025, while SMEs are projected to advance at the fastest CAGR of 18.29% through 2031.

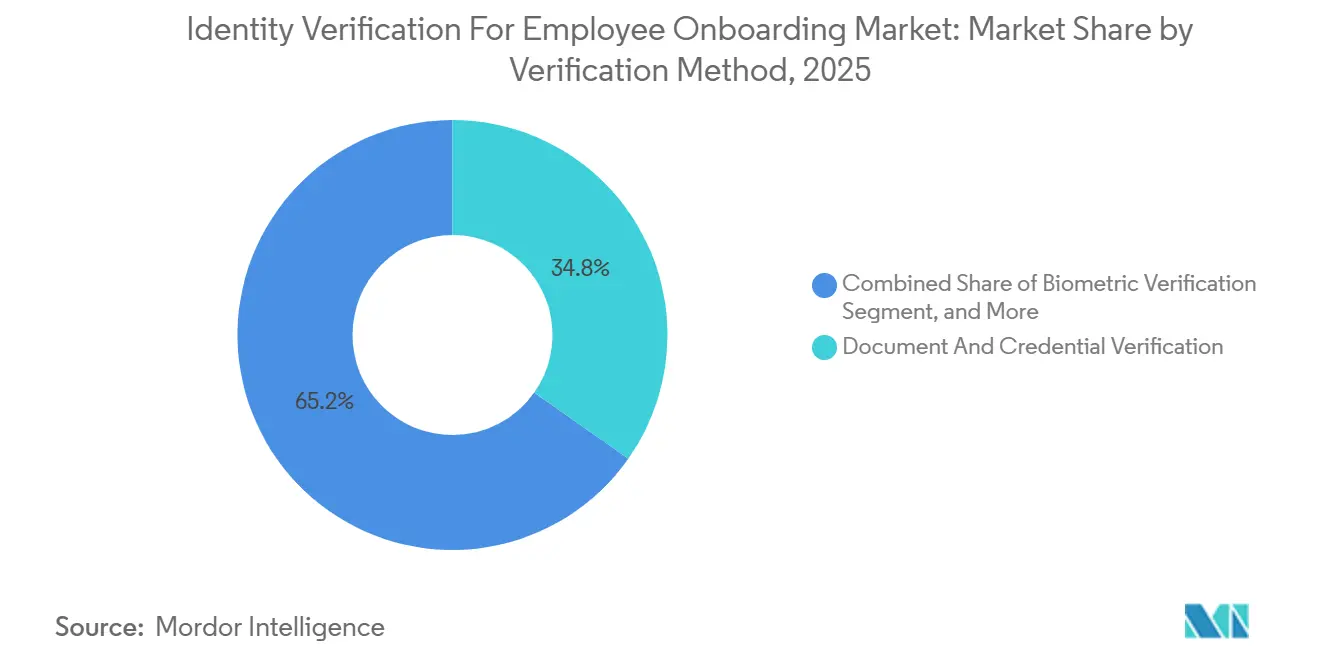

- By verification method, document and credential verification accounted for 34.77% of the market in 2025, while biometric verification is projected to grow at a 19.13% CAGR through 2031.

- By end-user industry, BFSI held 28.63% share of the identity verification for employee onboarding market in 2025, while healthcare and life sciences are expected to expand at the fastest CAGR of 17.67% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Identity Verification For Employee Onboarding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Candidate Impersonation, Synthetic Identity, And Insider Fraud Risks | +3.2% | Global, with acute early impact in North America, Europe, and APAC tech corridors | Short term (≤ 2 years) |

| Growth In Remote And Hybrid Hiring Workflows | +2.8% | Global, deepest penetration in North America, Northern Europe, and Australia | Short term (≤ 2 years) |

| Stricter Right-To-Work, Employment Eligibility, And Workforce Compliance Requirements | +2.4% | North America and EU core, with spill-over to the UK, GCC, and APAC regulated markets | Medium term (2-4 years) |

| Rising Adoption Of Biometric And Liveness Verification In Digital Onboarding | +2.1% | Global, accelerating in APAC and North America | Medium term (2-4 years) |

| Reusable Digital Identity Wallets For Repeat Workforce Onboarding | +1.5% | EU and North America, with early gains in Brazil and Singapore | Long term (≥ 4 years) |

| ATS And HRIS Embedding Of Identity APIs For High-Volume Hiring | +1.3% | Global, concentrated in North America and Western Europe enterprise segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Candidate Impersonation, Synthetic Identity, and Insider Fraud Risks

Hiring pipelines have become a visible attack surface for identity verification for the employee onboarding market, because remote workflows let fraudulent applicants reach employers without any physical identity touchpoint. Organized schemes now span candidate impersonation, synthetic identities, insider fraud, and ghost-hire activity, which means the risk no longer ends once a worker clears the first screening step. AI-generated phishing attacks created in 5 minutes are more than 4 times as effective as human-crafted attacks, which helps explain why employers are reassessing how easily bad actors can manipulate pre-hire and post-hire interactions. This threat pattern is widening the scope of buying decisions, because identity verification now needs to support payroll changes, device enrollment, credential recovery, and privileged access controls rather than only day-one onboarding. The identity verification for employee onboarding market is therefore seeing stronger demand for layered document, biometric, liveness, and behavior-linked controls in a single workflow. That shift is also favoring vendors that can support continuous reverification, since a point-in-time pass at the hiring stage no longer satisfies enterprise security teams.[1] Daon, “Daon Introduces Workforce Identity Fraud Prevention to Restore Trust Across the Employee Lifecycle,” Daon, daon.com

Growth In Remote and Hybrid Hiring Workflows

The permanent shift to remote and hybrid hiring continues to expand the addressable market for identity verification in employee onboarding, as employers cannot rely on in-person office visits or document inspection at scale. Distributed recruiting also creates handoff gaps across talent acquisition, hiring managers, IT, and compliance teams, giving fraud rings more room to exploit weak ownership of the process. Checkr launched its IDV product in March 2026, with liveness detection, forensic document analysis, and device and network intelligence built into the early hiring flow, demonstrating how vendors are moving identity checks closer to the first candidate touchpoint. Remote hiring has also increased the frequency with which employers verify the same person, because contractor re-engagement, marketplace work, and repeat staffing cycles now trigger new checks rather than a single historical verification. That pattern is changing vendor economics, since per-transaction models become less attractive when employers want identity coverage across the full workforce lifecycle. The identity verification market for employee onboarding is benefiting from this shift, because subscription and platform pricing better align with recurring verification than one-off document-review fees.

Stricter Right-To-Work, Employment Eligibility, and Workforce Compliance Requirements

Compliance pressure remains a central driver of the identity verification market for employee onboarding, because employment eligibility checks are mandatory in many jurisdictions, even when fraud risk appears low. In the United States, the combination of Form I-9 obligations, E-Verify expansion, and state-level mandates keeps workforce identity controls tied closely to payroll and onboarding systems. The United Kingdom created a formal route for certified digital identity service providers to perform right-to-work checks, providing vendors with a clearer path to replace manual reviews with approved digital workflows.[2]UK Government, “Digital Identity Certification for Right to Work, Right to Rent and Criminal Record Checks,” UK Home Office, gov.uk Japan’s Digital Agency issued guidance in February 2026 that expanded JPKI-based identity verification to private employment workflows, strengthening the legal and operational case for digital hiring verification in that market. In Europe, eIDAS 2.0 and the planned EUDI Wallet rollout are already shaping vendor roadmaps, because providers want to align with emerging government-backed identity infrastructure before broad employer adoption accelerates. The identity verification for employee onboarding market is therefore being lifted by regulations that increase both the volume of checks and the standard of proof employers must maintain.[3]Japan Digital Agency, “Guidelines on the Handling of Digital Identity in Administrative Procedures,” Japan Digital Agency, digital.go.jp

Rising Adoption Of Biometric and Liveness Verification In Digital Onboarding

Biometric and liveness verification is moving toward baseline status in the identity verification market for employee onboarding, especially where employers need stronger assurance against impersonation during remote hiring. iProov launched its Workforce Solution Suite in March 2026, aligned with NIST SP 800-63-4 and certified to ISO 30107-3, FIDO Face Verification, and CEN 18099, which gives enterprise buyers a more concrete benchmark for liveness performance. Passive liveness is gaining preference over active challenge-response flows because it reduces candidate friction and lowers drop-off during high-volume onboarding while preserving fraud controls. Liquid Inc. reported more than 150 million cumulative identity verifications and over 600 contracted clients in Japan in April 2025, demonstrating that AI-enabled biometric onboarding can operate at scale while meeting strict data protection requirements. This operating proof matters to enterprise buyers because it reduces concerns that biometric verification remains too specialized or too burdensome for everyday hiring volumes. The identity verification for employee onboarding market is also being supported by the fact that procurement teams increasingly want certified liveness controls rather than broad vendor claims about fraud detection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy, Biometric Consent, And Data Residency Constraints | -2.1% | Global, with highest friction in Illinois, the EU, India, and China | Short term (≤ 2 years) |

| Integration Complexity Across Legacy HR, ATS, And Compliance Systems | -1.6% | Global, amplified in large enterprises with fragmented ERP and HRIS stacks | Medium term (2-4 years) |

| False Reject Risk In Tight Labor Markets | -1.0% | North America and the EU, with early impact on early-career and underrepresented candidate segments | Short term (≤ 2 years) |

| Jurisdiction-Specific Employment Document Rules Limiting Global Standardization | -0.7% | APAC, Middle East and Africa, and South America, with spill-over to multinational hiring programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Privacy, Biometric Consent, and Data Residency Constraints

Privacy law remains one of the clearest limits on adoption in the identity verification for employee onboarding market, because the strongest fraud controls often depend on facial biometrics, liveness checks, and long-lived identity records. Illinois BIPA still requires strict written consent, retention schedules, and destruction policies, even after the April 2026 Seventh Circuit ruling reduced historical per-scan exposure for some defendants.[4]Foley and Lardner, “BIPA Alert: Seventh Circuit Ruling Applies BIPA Amendments Retroactively, Ending ‘Per Scan’ Exposure for Companies Operating in Illinois,” Foley and Lardner, foley.com GDPR Article 9 treats biometric data used for unique identification as special-category data, which means employers in Europe face tighter legal bases and process design requirements before deployment. The EU AI Act adds another layer, as biometric identification systems may fall under high-risk obligations that increase compliance burdens for vendors and employers. India’s data protection regime and China’s PIPL also make global rollout harder, as multinational employers often need regional infrastructure, local data-handling policies, and separate legal workflows to remain compliant. These legal and operational burdens slow conversion cycles, raise total ownership costs, and lead some employers to limit biometric use to higher-risk roles rather than broad workforce onboarding.

Integration Complexity Across Legacy HR, ATS, And Compliance Systems

System integration continues to slow identity verification for employee onboarding, because most large employers run layered HR stacks that were not designed for modular, real-time identity workflows. Identity results need to move across ATS platforms, HRIS records, payroll engines, background screening tools, and access systems, and each handoff adds field mapping, testing, and audit requirements. Persona launched Candidate Verification in March 2026 with direct integrations into Ashby, Greenhouse, and Workday, which shows where vendors are trying to remove friction in common hiring environments. Nametag expanded that integration push in May 2026 through native links with Workday, Greenhouse, Okta, Microsoft Entra, and Cisco Duo, reflecting how buyers increasingly want identity assurance to sit across HR and IT rather than inside a separate portal. Even with these connectors, employers using Oracle HCM, SAP SuccessFactors, or customized internal systems still face longer deployment cycles and higher project costs. The problem is not only technical, because compliance teams also want audit logs and verification outcomes written back into the system of record, and that requirement remains hard to deliver consistently across older environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Platform Depth And Service Wrapping Define Revenue Mix

Solutions held 72.12% of the identity verification for employee onboarding market share in 2025, which reflects the continued strength of SaaS platforms that bundle document verification, biometric matching, liveness checks, workflow orchestration, and compliance reporting into a single enterprise product. This lead also shows that buyers still prefer configurable software control when identity verification must connect with recruiting, payroll, and access management systems across different business units. Platform-based delivery works well for employers that want direct API access, policy configuration, internal governance controls, and centralized audit records without depending on a manual review team for every exception. The dominance of solutions also aligns with the needs of large enterprises, which often standardize on a few core security and HR platforms and want identity controls embedded in those systems rather than outsourced as isolated tasks. In the identity verification for employee onboarding market, this structure favors vendors that can support broad document libraries, cross-border hiring workflows, and enterprise-grade reporting inside the same stack.

Services are projected to expand at a 17.71% CAGR from 2026 to 2031, as buyers increasingly seek verified outcomes, updated compliance logic, and managed fraud operations, rather than just software access. Managed verification workflows are gaining traction among employers that lack dedicated identity teams and need help with template updates, rule tuning, exception handling, and policy changes across jurisdictions. This is especially relevant in the mid-market, where hiring volumes can be high enough to create risk exposure but not large enough to justify a specialized internal identity operations function. The service layer is also becoming more recurring, because advisory retainers, compliance monitoring, and ongoing workflow optimization now extend well beyond initial implementation. As that pattern grows, the identity verification for employee onboarding market is narrowing the line between software licensing and service delivery. Vendors that once sold point products are increasingly building long-term managed relationships, which changes revenue mix, customer stickiness, and the basis on which enterprise buyers compare providers.

By Deployment Mode: Cloud Leadership Holds, Hybrid Demand Builds In Regulated Environments

Cloud-based deployments accounted for 69.41% of the market share in 2025, underscoring how closely the identity verification for employee onboarding market aligns with the broader SaaS architecture of modern HR, payroll, and recruiting systems. Cloud delivery aligns with hiring workflows by enabling fast updates to document templates, real-time improvements to fraud signal, elastic processing during recruitment surges, and easier rollout across geographically dispersed teams. It also aligns with how employers buy ATS and HRIS software, since many organizations already run onboarding, screening, and access provisioning in the cloud. These advantages make cloud deployment the default option for most employers, especially where speed, standardization, and lower internal IT burden matter more than deep infrastructure control. The identity verification market for employee onboarding continues to benefit from this bias, as cloud deployment reduces onboarding friction for both vendors and customers.

The identity verification market for employee onboarding in hybrid deployments is projected to expand at a 16.73% CAGR from 2026 to 2031, driven by regulated employers seeking stronger control over sensitive data while still leveraging cloud-based verification intelligence. Hybrid models appeal to financial institutions, government contractors, and healthcare systems that want certain records and workflows to remain inside controlled environments. They also provide a middle path for companies responding to GDPR-related data-handling requirements, HIPAA-linked workforce onboarding concerns, and internal security rules governing protected information. On-premises deployment remains relevant for a narrower set of defense, public-sector, and highly restricted environments, but it is unlikely to gain a significant share. Hybrid growth, therefore, reflects a practical compromise rather than a return to legacy architecture. It lets employers combine local data governance with cloud-scale matching, document analysis, and fraud model updates that would be harder to maintain internally.

By End-User Enterprise Size: Large Accounts Still Dominate, SME Adoption Is Broadening The Base

Large enterprises held a 63.29% share in 2025, indicating that revenue in the identity verification for employee onboarding market still depends heavily on organizations with high hiring volumes, complex compliance obligations, and multi-system technology environments. These companies can justify deep integrations because onboarding failures create wider consequences across payroll, identity access, insider risk, and audit readiness. Large employers also tend to negotiate multi-year contracts that bundle verification APIs, orchestration, audit logs, reporting tools, and support commitments into a broader workforce identity program. That contracting model raises switching costs and makes enterprise wins especially valuable, which is why competitive intensity remains high in this segment. The identity verification for employee onboarding industry, therefore, still revolves around vendors that can deliver security depth, regulatory support, and operational reliability at scale.

SMEs are projected to grow at the fastest CAGR of 18.29% from 2026 to 2031, indicating that the addressable base in the identity verification for employee onboarding market is expanding beyond traditional enterprise buyers. Didit published bundle pricing of around USD 0.50 per onboarded hire in May 2026, including identity verification, AML screening, and HR questionnaire workflow support, which lowers the barrier for smaller employers. Affordable per-hire pricing also matches the needs of companies that hire in bursts, use contingent workers, or lack the volume stability needed for enterprise software contracts. This part of the market is maturing as vendors simplify setup, narrow implementation work, and package compliance functionality into easier subscription models. The identity verification for employee onboarding industry is therefore gaining a broader revenue foundation, even if large enterprises still control the highest contract values. Over time, stronger SME adoption should reduce dependence on a narrow set of enterprise customers and make vendor growth less tied to a few large deals.

By Verification Method: Documents Remain Foundational, Biometrics Drive The Fastest Expansion

Document and credential verification accounted for 34.77% of the market share in 2025, keeping it at the center of the identity verification for employee onboarding market, as right-to-work and eligibility checks usually begin with official documents. This method remains essential even when employers add biometric layers, since legal and operational requirements still depend on verifying government-issued records, work authorization evidence, and other formal credentials. Document verification also benefits from established enterprise familiarity, because employers understand the control objective and can map it directly to onboarding policy, audit records, and regulatory evidence. Improvements in document analysis accuracy have further reinforced its role, making it suitable for high-stakes hiring decisions in many jurisdictions without raising the same privacy concerns as biometrics. Database and identity network verification, along with video-assisted verification, continue to matter where additional supervision, cross-checking, or local compliance rules make a simple document scan insufficient.

The identity verification market size for employee onboarding biometric verification is projected to expand at a 19.13% CAGR from 2026 to 2031, reflecting how quickly employers are responding to deepfakes, impersonation, and the risk of repeat account takeovers. iProov’s March 2026 workforce launch clearly signaled this shift, positioning certified liveness and government-grade assurance as practical requirements for remote hiring and ongoing workforce trust. Checkr launched portable Checkr Profiles in April 2026, while Jumio expanded selfie.DONE across South America the same month, and both moves show that verified credentials are starting to travel with workers across hiring events and platforms. This does not displace document verification, but it does shift the growth mix within the identity verification for employee onboarding industry, as biometric and wallet-linked methods are better suited to reusable trust models. Liveness and deepfake detection are also moving from premium add-ons toward baseline procurement requirements in regulated sectors. As a result, the market is shifting from static identity proofing toward repeated, portable, and higher-assurance verification throughout the worker relationship.

By End-User Industry: BFSI Leads Current Spending, Healthcare Moves Faster On Future Growth

BFSI held a 28.63% share in 2025, making it the largest vertical in the identity verification for employee onboarding market, as financial institutions must align employment verification with broader KYC, AML, and internal control obligations. This sector cannot separate workforce onboarding from financial crime risk, since new hires often receive access to sensitive systems, customer data, payment workflows, and regulated operating processes. The need for traceable audit records, stronger identity assurance, and layered security controls keeps spending elevated across banks, insurers, fintech companies, and related service providers. BFSI also tends to adopt new fraud defenses early, which strengthens its role as a lead customer group for biometric verification, liveness detection, and continuous monitoring. In the identity verification for employee onboarding industry, that combination of regulatory depth and operational risk keeps BFSI at the front of enterprise buying activity.

Healthcare and life sciences are projected to expand at a 17.67% CAGR from 2026 to 2031, because onboarding in this sector now sits at the intersection of provider credentialing, interoperability mandates, and rising impersonation risk in clinical settings. Ping Identity and OLOID announced a verified-trust model for clinical workforce onboarding in May 2026 that uses reusable credentials and passwordless access for clinicians, showing how identity proofing is being linked directly to downstream access security. That architecture matters because healthcare employers need confidence not only at hire but also at shared workstations, during account recovery, and across repeated access events inside care environments. Information technology and telecom, retail and e-commerce, and government and public sector also maintain meaningful demand, especially where onboarding leads quickly to privileged system access or fast-cycle workforce turnover. Industrial manufacturing is becoming a clearer opportunity area as automation, distributed work sites, and contractor-heavy staffing create more frequent identity checkpoints. The identity verification market for employee onboarding is therefore expanding beyond traditional compliance-heavy verticals into sectors where operational continuity increasingly depends on verified workforce identity.

Geography Analysis

North America held 39.71% of the identity verification for employee onboarding market share in 2025, keeping it firmly ahead of other regions because employment eligibility rules and biometric privacy requirements are both more active and enforceable there. The United States provides a broad structural base for demand, since any employer with even 1 U.S.-based hire must complete identity and work authorization checks as part of onboarding. That requirement makes workforce identity verification a common operational need rather than a niche control reserved for a few regulated employers. State-level biometric laws, led by Illinois BIPA, also raise the importance of consent, retention, and audit design, which gives vendors more room to sell compliance-ready workflow features. Europe remained the second-largest regional block in the identity verification for employee onboarding market, supported by eIDAS 2.0 planning and employer interest in wallet-based digital identity ecosystems. The United Kingdom’s Digital Identity and Attributes Trust Framework added practical momentum by defining a recognized certification route for providers that perform right-to-work checks for employers.

The identity verification for employee onboarding market size in Asia-Pacific is projected to expand at 18.41% CAGR from 2026 to 2031, which makes the region the strongest growth engine over the forecast period. Japan is central to that outlook, because My Number Card circulation passed 100 million cards and exceeded 80% population penetration by December 2025, giving employers a much stronger digital credential base for formal identity workflows. The Digital Agency’s February 2026 guidance then extended JPKI-based verification into private employment settings, which moved digital identity closer to mainstream hiring operations. Demae-can adopted NEC’s financial-grade identity verification service for delivery driver registration in March 2026, showing that gig and platform labor is becoming a meaningful demand pool rather than a side case. India and South Korea are also becoming more important in the identity verification for employee onboarding market, supported by digital identity infrastructure, fintech staffing needs, and tighter compliance expectations in remote and cross-border hiring environments.

South America, the Middle East, and Africa remained earlier-stage regions in 2026, but the identity verification for employee onboarding market is building a clearer long-term opportunity base there. Brazil is the most developed South American market in the current mix, and Jumio expanded selfie.DONE across South America in April 2026 after first launching it in Brazil in October 2025. Saudi Arabia and the United Arab Emirates are generating demand through digital workforce infrastructure programs tied to broader economic modernization and sector expansion in financial services, construction, and hospitality. In Africa, South Africa and Nigeria stand out because fintech-led hiring and improving mobile connectivity are creating more workable conditions for biometric and liveness-based onboarding at scale.

Competitive Landscape

The identity verification market for employee onboarding in 2026 is clearly in a transitional phase, where fragmentation coexists with intensifying competition. Global leaders like Jumio, Veriff, Trulioo, and IDnow anchor the top tier, but regional specialists remain highly relevant because they can tailor document coverage, pricing, and deployment models to local employer needs. That balance keeps the market open to new entrants who solve specific workflow pain points more effectively than broad platforms. Importantly, the competitive scope is widening beyond day-one onboarding, since buyers increasingly expect identity assurance to remain active across account recovery, access changes, and repeat workforce engagement. Roadmaps are therefore shifting toward continuous identity intelligence rather than static pass/fail checks.

A structural divide is emerging between horizontal trust platforms and HR-native specialists. Horizontal platforms aim to unify employee, customer, and counterparty identities within a single orchestration layer, while HR-focused vendors optimize for recruiting, pre-employment screening, onboarding, and workforce access. Nametag’s Recruit module and integrations with Workday, Greenhouse, Okta, Microsoft Entra, and Cisco Duo illustrate this overlap between HR and IT. Persona’s Candidate Verification integrations with Ashby, Greenhouse, and Workday show how workflow placement is becoming as critical as verification accuracy. Checkr’s launch of its IDV stack and portable Profiles further signals convergence between background screening and identity verification into a broader hiring trust layer.

Standards alignment is raising the bar for regulated deployments. Buyers increasingly expect compliance with frameworks such as NIST SP 800-63-4, ISO 30107-3, FIDO Face Verification, and CEN 18099 before committing to sensitive deployments. iProov’s workforce launch positioned certified liveness and government-grade assurance as core features, not optional extras. Veriff’s acquisition of Vespia and its partnership with Data Zoo highlight how vendors are combining identity proofing, KYB, and access to authoritative data into broader trust platforms. Jumio’s launch of Jumio Watch pushed competition toward lifecycle risk monitoring, confirming that the next battleground is ongoing workforce trust rather than just initial verification.

Identity Verification For Employee Onboarding Industry Leaders

Jumio Corporation

Veriff OÜ

Trulioo Information Services Inc.

IDnow GmbH

Persona Identities, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Nametag launched its Recruit module, enabling identity assurance across the full hiring pipeline with native integrations into Workday, Greenhouse, Okta, Microsoft Entra, and Cisco Duo, bridging the HR and IT verification gap for enterprise customers.

- May 2026: Daon launched its Workforce Identity Fraud Prevention solution, integrating its TrustX SaaS platform, xProof IDV engine, xFace facial authentication, and xAuth MFA into a unified candidate-to-employee lifecycle identity product using standards-based OIDC APIs.

- May 2026: Ping Identity and OLOID announced a joint passwordless, verified-trust model for clinical workforce onboarding, enabling clinician-held verifiable credentials in Apple Wallet and Google Wallet and covering day-one access, shared workstation login, and account recovery.

- April 2026: Jumio launched Jumio Watch, a continuous identity intelligence product built on the Jumio Identity Graph, reporting up to 25% more risk detected after initial onboarding and 700% year-over-year growth in injection attempts, with daily proactive risk alerts for fraud and compliance teams.

Global Identity Verification For Employee Onboarding Market Report Scope

The identity verification for employee onboarding market refers to technology platforms and services that enable organizations to securely authenticate and verify the identities of new hires during onboarding. These solutions leverage methods such as document and credential verification, biometric checks, database and identity network validation, liveness and deepfake detection, video-assisted verification, and reusable digital identity wallets. Delivered through cloud-based, on-premises, and hybrid deployment models, they serve both large enterprises and small and medium-sized enterprises across industries, including BFSI, healthcare and life sciences, information technology and telecom, retail and e-commerce, industrial manufacturing, government and public sector, and other end-user industries. The core purpose of this market is to reduce identity fraud, ensure compliance with labor and data protection regulations, safeguard organizational assets, and enhance employee experience by streamlining secure, automated, and user-friendly verification workflows.

The identity verification for employee onboarding market report is segmented by Offering (Solutions, and Services), Deployment Model (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium-sized Enterprises), Verification Method (Document and Credential Verification, Biometric Verification, Database and Identity Network Verification, Liveness and Deepfake Detection, Video and Assisted Verification, and Reusable Identity and Wallet Verification), End-user Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Solutions |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Document And Credential Verification |

| Biometric Verification |

| Database And Identity Network Verification |

| Liveness And Deepfake Detection |

| Video And Assisted Verification |

| Reusable Identity And Wallet Verification |

| BFSI |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Sector |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Offering | Solutions | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By Verification Method | Document And Credential Verification | |

| Biometric Verification | ||

| Database And Identity Network Verification | ||

| Liveness And Deepfake Detection | ||

| Video And Assisted Verification | ||

| Reusable Identity And Wallet Verification | ||

| By End User Industry | BFSI | |

| Healthcare and Life Sciences | ||

| Information Technology and Telecom | ||

| Retail and E-commerce | ||

| Industrial Manufacturing | ||

| Government and Public Sector | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of identity verification for employee onboarding?

The identity verification for employee onboarding market stood at USD 2.40 billion in 2025, rises to USD 2.78 billion in 2026, and is projected to reach USD 6.01 billion by 2031 at a 16.67% CAGR.

What is driving faster adoption of digital identity checks in hiring?

Remote and hybrid hiring, synthetic identity fraud, deepfakes, and tighter right-to-work compliance are pushing employers to move from manual checks to digital and continuous verification workflows.

Which region leads spending, and which region is growing fastest?

North America led with 39.71% share in 2025 because of strong employment eligibility rules, while Asia-Pacific is projected to grow the fastest at 18.41% CAGR through 2031.

Which verification method is expanding the fastest?

Biometric verification is projected to grow at a 19.13% CAGR through 2031 as employers respond to impersonation risk and adopt liveness controls for remote onboarding.

Why are cloud deployments still dominant in hiring verification?

Cloud-based deployments held 69.41% share in 2025 because they fit SaaS-native HR stacks, support fast document updates, and scale more easily during large hiring cycles.

Which end-user sectors are creating the strongest demand?

BFSI led with 28.63% share in 2025 because of AML and KYC layering, while healthcare and life sciences is projected to grow fastest at 17.67% CAGR as credentialing and access security become more tightly linked.

Page last updated on: