Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

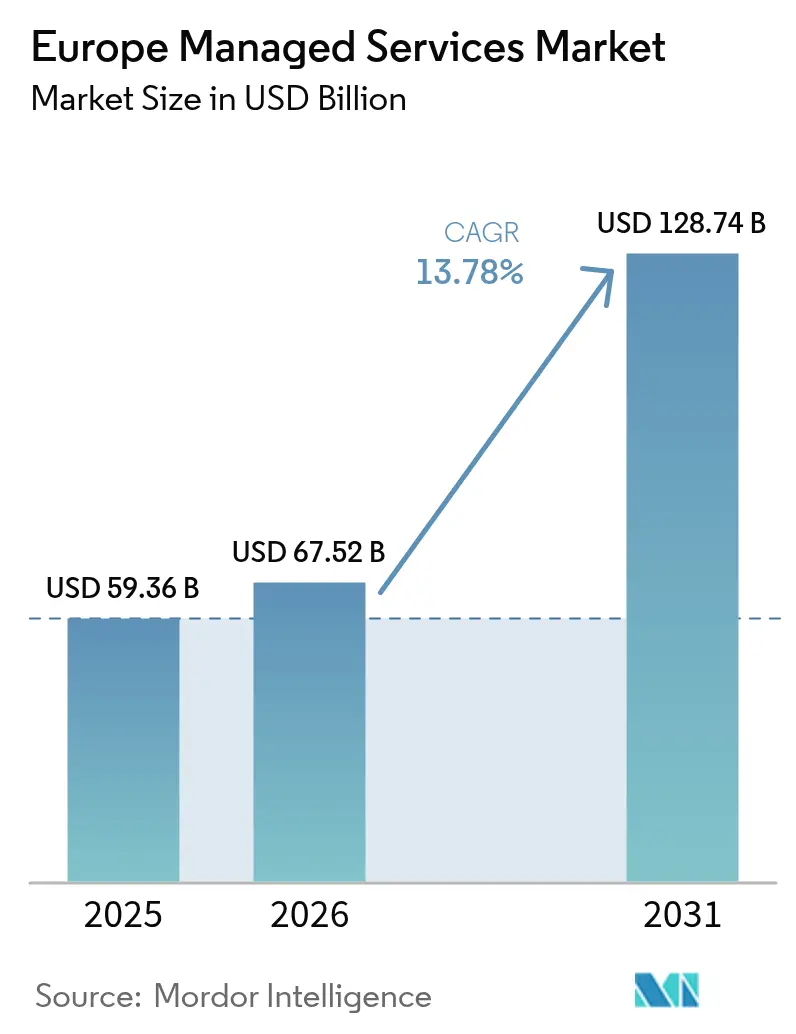

| Base Year Market Size (2025) | USD 59.36 Billion |

| Market Size (2026) | USD 67.52 Billion |

| Market Size (2031) | USD 128.74 Billion |

| Growth Rate (2026 - 2031) | 13.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Managed Services Market Analysis by Mordor Intelligence

The Europe managed services market size is projected to be USD 59.36 billion in 2025, USD 67.52 billion in 2026, and reach USD 128.74 billion by 2031, growing at a CAGR of 13.78% from 2026 to 2031. Demand is accelerating as organizations migrate from capital-intensive data-center assets to predictable operating-expense agreements that bundle infrastructure, security, and application management. Hybrid and multi-cloud strategies dominate because they let firms balance latency, compliance, and cost while still meeting strict EU data-sovereignty laws. Escalating cyber-threat volumes, the NIS2 Directive, and the Digital Operational Resilience Act are turning managed security into the fastest-growing service line, while EU grants for SME digitalization are widening the customer base. At the same time, edge-cloud data-centers positioned inside sovereign jurisdictions are helping providers support low-latency workloads for manufacturing, financial trading, and telemedicine. Competitive intensity remains moderate; global systems integrators, telecom carriers, and Indian IT services companies are racing to lock in multi-year contracts, often through platform-agnostic alliances with hyperscalers.

Key Report Takeaways

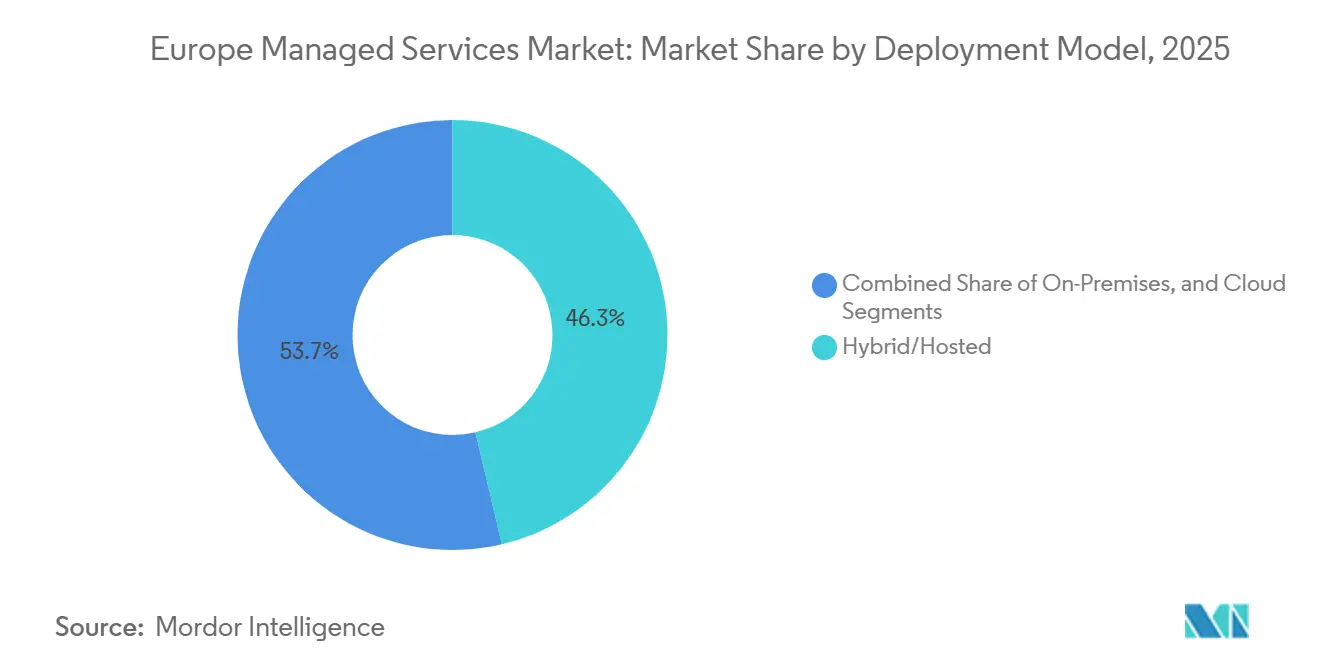

- By deployment model, hybrid and hosted configurations led with 46.32% of Europe managed services market share in 2025 while pure cloud deployments are advancing at a 14.18% CAGR to 2031.

- By service type, managed security accounted for 29.54% of the Europe managed services market size in 2025 and is expanding at a 15.58% CAGR through 2031.

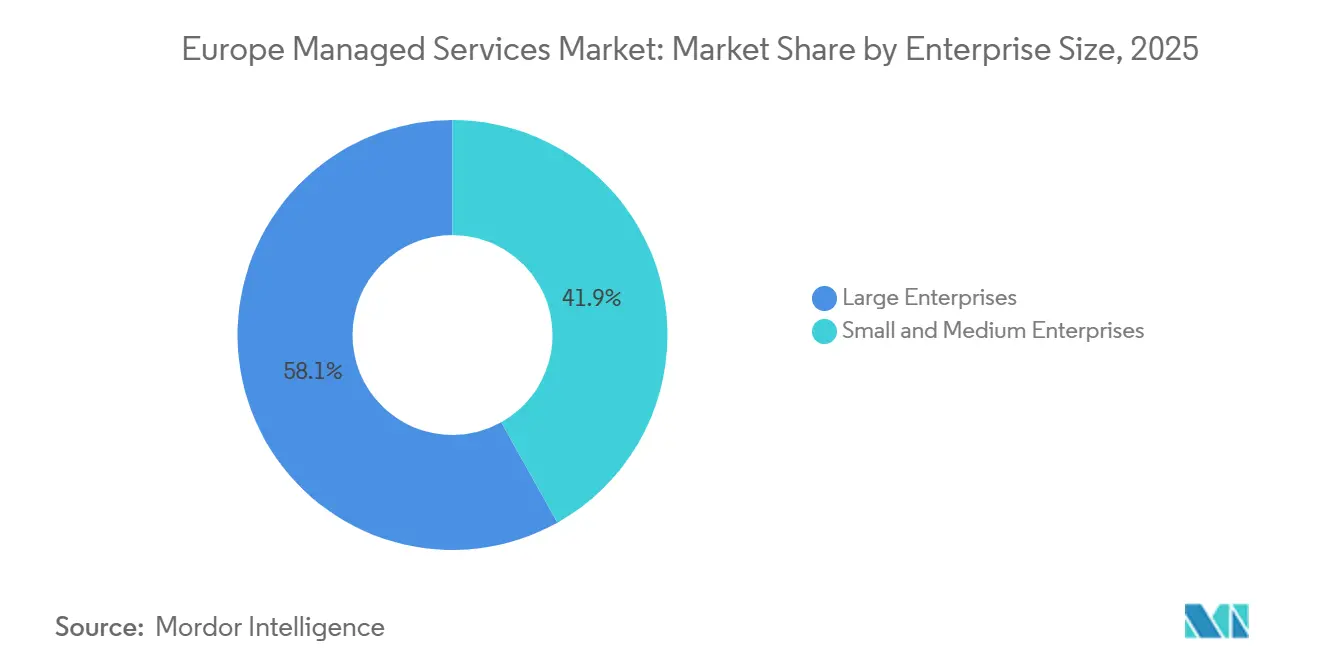

- By enterprise size, large enterprises commanded 58.11% spending in 2025, whereas SME adoption is rising at a 14.38% CAGR on the back of EU digitalization grants.

- By end-user vertical, BFSI captured 23.39% revenue share in 2025, but healthcare and life sciences is projected to grow at a 15.74% CAGR to 2031.

- By country, the United Kingdom held 21.44% of the Europe managed services market share in 2025, while Poland represents the fastest-growing country with a 14.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Managed Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Adoption of Hybrid and Multi-Cloud Architectures | +3.2% | Germany, United Kingdom, France | Medium term (2-4 years) |

| Rising Demand for Cost Optimization and Predictable OPEX | +2.8% | Spain, Italy, Poland | Short term (≤ 2 years) |

| Increasing Cybersecurity Threats Driving Managed Security Uptake | +3.5% | BFSI and healthcare sectors across Europe | Short term (≤ 2 years) |

| Shortage of In-House IT Talent Across Europe | +2.1% | Nordics, Netherlands, Germany | Medium term (2-4 years) |

| Emergence of Edge-Cloud Zonal Datacentres for Data-Sovereign Workloads | +1.4% | Germany, France, Poland, Netherlands | Long term (≥ 4 years) |

| MSP Bundling of AIOps and FinOps Platforms to Automate Cost Governance | +1.2% | United Kingdom, Germany, Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of Hybrid and Multi-Cloud Architectures

European enterprises are increasingly distributing workloads across on-premises assets, private clouds, and several public-cloud platforms to align performance with compliance mandates. A PwC survey showed that 68% managed at least three clouds in 2025, but only 22% had enough in-house skills to integrate identity federation, network automation, and disaster-recovery workflows. Managed service providers are stepping in with Kubernetes control planes, unified observability, and cloud brokerage layers that keep data portable, an outcome reinforced by the EU Data Act’s anti-lock-in clauses.[1]European Commission, “EU Data Act,” ec.europa.eu Financial institutions exemplify the trend by keeping transaction data on-premises while pushing analytics to sovereign zones run by Deutsche Telekom, illustrating why sub-10 ms connectivity and SD-WAN overlays are now must-have features. Because latency budgets are tight, telecom carriers monetize dedicated interconnects as part of bundled managed services, blending network and security SLAs in a single contract.

Rising Demand for Cost Optimization and Predictable OPEX

Cloud overspending is eroding the savings that initially justified migration; Deloitte reported that 54% of European CFOs blew past their 2024 cloud budgets by more than 20%. FinOps modules embedded within managed services continuously right-size compute, enforce tagging for cost show-back, and park non-production workloads during off-peak hours, delivering 15-30% savings without refactoring.[2]FinOps Foundation, “State of FinOps 2025,” finops.org Bundled offerings appeal to SMEs that lack procurement teams, essentially converting unpredictable capital outlays into steady monthly fees. Public money amplifies the effect. The European Investment Bank issued EUR 1.2 billion (USD 1.28 billion) in 2025 to subsidize SME cloud uptake, with certified MSP engagement mandated for grant eligibility. Spain, Italy, and Poland, where SME digitization lags Northern Europe, are showing the steepest adoption curves because subsidies sharply lower entry barriers.

Increasing Cybersecurity Threats Driving Managed Security Uptake

Ransomware attacks against European hospitals, municipalities, and supply-chain firms jumped 34% in 2025. The new NIS2 Directive forces a 24-hour breach notification window and personal board liability, prompting enterprises to outsource around-the-clock monitoring to ISO 27001-certified providers. In finance, the Digital Operational Resilience Act requires geographically redundant security operations centers located inside EU borders, giving regional specialists an advantage over extra-EU hyperscalers. Subscription-based managed detection and response packages now bundle threat intelligence, vulnerability scanning, and forensic support capabilities that would be cost-prohibitive for a single firm to build. Access to cross-client telemetry allows providers to spot zero-day exploits sooner than isolated internal teams.

Shortage of In-House IT Talent Across Europe

Managed service providers pool scarce engineers, enabling a single network architect to serve multiple clients across follow-the-sun shifts. Although the EU’s Pact for Skills set aside EUR 800 million (USD 856 million) for upskilling, certification pipelines can take up to 2 years, leaving near-term demand unmet. Nordic salary premiums running 40% above EU averages drive companies to outsource to MSP teams based in Poland, Portugal, and Romania, where labor costs are lower but skill levels remain strong. This geographical arbitrage further cements outsourcing as the default approach for talent-strapped enterprises.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex EU Data-Sovereignty and Privacy Regulations | -2.4% | Germany, France, Netherlands | Short term (≤ 2 years) |

| Integration Complexity with Legacy Systems | -1.8% | Manufacturing and government verticals in Germany, Italy, France | Medium term (2-4 years) |

| Rising Energy Costs Squeezing Data-Centre Service Margins | -1.1% | Germany, Netherlands, United Kingdom | Short term (≤ 2 years) |

| Escalating Carbon-Accounting Scrutiny on Outsourced Workloads | -0.9% | Nordics, Germany, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complex EU Data-Sovereignty and Privacy Regulations

The coexistence of GDPR, the EU Data Act, and sector-specific frameworks such as the Medical Device Regulation forces MSPs to maintain separate infrastructure stacks, raising compliance overhead. Germany’s BSI bars public-sector workloads from traveling outside sovereign clouds controlled by EU-headquartered operators. France’s SecNumCloud certificate adds even stricter controls and can take 18 months to earn. Fragmentation inflates legal costs and stretches procurement cycles because each member state enforces slightly different audit standards. A voluntary CISPE initiative to harmonize certifications is still in pilot, so managed-services rollouts remain slowed by regulatory sprawl.

Integration Complexity with Legacy Systems

A 2025 McKinsey survey found 62% of manufacturers and 58% of government agencies still rely on COBOL-based mainframes. Bridging these environments with cloud-native stacks requires middleware, event brokers, and dual-write patterns that introduce latency and raise project cost. Payment systems on IBM z/OS must exchange data with AI fraud engines on Kubernetes, so MSPs charge premium rates for bespoke replication pipelines. Although the Digital Europe Programme earmarked EUR 500 million (USD 535 million) for modernization pilots, most of that money flows to refactoring, not to managed services. Providers are responding by buying niche mainframe consultancies, yet toolsets remain fragmented, leaving complexity as a persistent brake on adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Configurations Dominate Amid Sovereignty Pressures

Hybrid and hosted environments captured 46.32% of Europe managed services market share in 2025, while cloud-only setups are recording a brisk 14.18% CAGR to 2031. Enterprises keep sensitive datasets on-premises to meet GDPR while exploiting cloud burst capacity for analytics. Edge-cloud zones inside telecom exchanges offer sub-5 ms latency and sovereign certifications, letting providers strike a balance between performance and compliance. Hosted deployments keep growing among mid-sized firms that prefer predictable fees without multitenancy risk, particularly in Frankfurt and Amsterdam where colocation capacity expanded in 2025. Although on-premises spending is declining as a share of the Europe managed services market size, absolute dollars remain steady because German manufacturers and Italian banks refresh hardware through managed-infrastructure contracts instead of full cloud migrations.

The Gaia-X federation is reshaping the landscape by certifying interoperable services that combine cloud scale with data-residency guarantees. MSPs now embed Gaia-X-compliant orchestration layers to move workloads among sovereign zones and hyperscaler regions, reinforcing hybrid as the long-term norm. SMEs accelerate straight to cloud because they lack capex budgets, but even they often adopt a light hybrid stance by running backups or sensitive HR data locally. Consequently, the Europe managed services market continues to favor providers that can optimize workload placement across this hybrid continuum.

By Service Type: Managed Security Leads Growth Under New Mandates

Managed security held 29.54% revenue share in 2025 and is projected to remain the fastest-growing line at 15.58% CAGR. Regulatory deadlines, ransomware risk, and board-level scrutiny push enterprises to embed 24×7 monitoring, incident response, and forensic analysis within wider infrastructure contracts.[3] European Banking Authority, “Digital Operational Resilience Act,” eba.europa.eu Managed data-center services appeal to trading hubs that need low-latency proximity to exchanges in London, Frankfurt, and Paris, while managed network services such as SD-WAN and carrier-neutral interconnects weave together on-premises, edge, and multi-cloud domains. Communications and collaboration services have plateaued after the remote-work boom, causing vendors to shift focus toward real-time translation and contact-center AI.

Managed infrastructure and hosting remain baseline offerings but face commoditization as hyperscalers automate server provisioning through code templates. Consequently, providers differentiate by layering disaster-recovery drills and predictive capacity planning. Managed mobility is growing in healthcare and field services, where remote device provisioning and compliance enforcement are mission-critical. The convergence of managed security and network operations lets MSPs map threat intelligence to traffic anomalies in a single console, a feature regulators are starting to deem essential under DORA.

By Enterprise Size: SMEs Close the Gap With Grant-Backed Adoption

Large organizations accounted for 58.11% of market spending in 2025, yet SMEs are charting a faster 14.38% CAGR as EU grants trim initial costs. Firms with over 250 staff see managed services as pivotal to freeing internal teams for digital-product work, so they are consolidating vendors; Deloitte notes a drop from 8.4 providers in 2024 to 5.1 in 2025 as enterprises seek integrated platforms. Meanwhile, SMEs representing 99% of European businesses leverage standardized service tiers and self-service portals to gain enterprise-grade capabilities. The InvestEU program disbursed EUR 2.4 billion (USD 2.57 billion) in 2025, with 40% funneled into managed security and cloud migration.

AIOps and self-healing workflows let providers support hundreds of SMEs with staff sized for a few dozen large clients. Poland, Spain, and Italy are seeing the steepest uptake because government incentives overlap with lower wage costs that make outsourcing cost-effective. As a result, the Europe managed services industry is becoming more inclusive, deepening the total addressable base without undermining margins.

By End-User Vertical: Healthcare Surges on Interoperability Mandates

Healthcare and life sciences clock the highest growth at 15.74% CAGR through 2031, fueled by electronic health record interoperability, cross-border data exchange under the European Health Data Space, and AI-driven diagnostics that demand sub-second query times. BFSI retained 23.39% share in 2025 thanks to DORA, PCI-DSS, and strict uptime SLAs. Manufacturing leverages managed services for Industry 4.0 analytics yet grapples with air-gapped operational-technology environments that slow adoption. Retail and e-commerce lean on MSPs for PCI compliance and holiday-season scalability, while the public sector migrates citizen services into sovereign clouds, particularly in the Netherlands and Estonia.

Energy and utilities adopt managed security to protect smart-grid telemetry and to meet EU Emissions Trading reporting. Logistics firms focus on managed network services for real-time tracking, whereas media companies emphasize CDN optimization. Healthcare’s momentum is expected to stay intact because aging populations and AI diagnostics generate continuous data-governance and uptime requirements that smaller hospital IT teams cannot meet internally.

Geography Analysis

The United Kingdom led with 21.44% of Europe managed services market share in 2025, anchored by London’s financial cluster and post-Brexit adequacy rules that still allow seamless service delivery. Germany ranks second, propelled by manufacturing digitalization and stringent sovereignty laws that encourage hybrid topologies housed in Frankfurt hyperscaler zones. France follows, where SecNumCloud rules carve out a protective niche for domestic champions like OVHcloud.[4]ANSSI, “SecNumCloud Certification Framework,” ssi.gouv.fr Italy posts steady growth as SME invoicing mandates and the national digital-ID scheme push firms toward cloud governance. Spain leverages new edge infrastructure around Madrid and Barcelona to offer low-latency managed workloads, while the Netherlands remains a continental network gateway with dense colocation assets.

Poland is the star performer, expanding at a 14.01% CAGR through 2031. Nearshoring strategies situate delivery centers in Warsaw and Krakow, letting Western European clients enjoy EU-compliant services at lower labor rates. Nordic countries show high penetration but moderate growth, prioritizing managed security to offset premium salary markets. Central and Eastern European countries such as Romania and Hungary are emerging as secondary delivery hubs. The European Commission’s Digital Decade targets, which call for 75% cloud adoption by 2030, are nudging public agencies across member states to shift workloads to MSPs.

Germany’s sovereign-cloud partnership model exemplified by Deutsche Telekom’s alliances with hyperscalers is likely to spread across the bloc if interoperability standards mature. Conversely, geopolitical risk limits expansion in Russia, where sanctions have forced several Western providers to halt operations. Overall, country-level nuances mean providers must tailor compliance artifacts and language support while maintaining a unified service portfolio for economies of scale.

Competitive Landscape

The top ten providers captured roughly 35-40% of revenues in 2025, confirming moderate fragmentation within the Europe managed services market. Kyndryl’s spin-off from IBM and subsequent Azure, AWS, and VMware alliances showcase a platform-agnostic play that resonates with EU Data Act portability goals.

Telecom carriers such as Deutsche Telekom, Orange, and Vodafone differentiate through fiber footprints and edge nodes that guarantee sub-10 ms latency an advantage for manufacturing automation and high-frequency trading. Indian IT services firms are investing heavily in Polish and Romanian delivery centers, drawn by multilingual talent and EU-level data-residency compliance.

White-space opportunities remain in carbon-accounting modules that quantify Scope 3 emissions from outsourced workloads, a reporting mandate under the Corporate Sustainability Reporting Directive. Specialist MSPs focused on operational technology are gaining traction among energy and manufacturing clients that need deep protocol expertise. Generative-AI-based runbook automation is emerging as a key differentiator, as early adopters demonstrate measurable reductions in mean-time-to-repair. Sector-specific accreditations such as PCI-DSS and TISAX increasingly influence vendor shortlists, pushing providers to expand compliance portfolios beyond the ISO 27001 and SOC 2 baselines.

Europe Managed Services Industry Leaders

IBM Corporation

Fujitsu Limited

Capgemini SE

Atos SE

Accenture plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Microsoft announced an additional USD 1 billion investment to open two new Azure regions in Warsaw, broadening its sovereign-cloud footprint and deepening partner ecosystems.

- December 2025: Deutsche Telekom and Google Cloud launched a German sovereign cloud offering aimed at regulated sectors that require EU-governed managed services.

- November 2025: Kyndryl acquired a European OT-focused managed security specialist, expanding its footprint in manufacturing and energy markets.

- October 2025: Orange Business Services introduced an AI-powered FinOps module that helped pilot customers cut monthly cloud bills by 20-25%.

Europe Managed Services Market Report Scope

The Europe Managed Services Market Report is Segmented by Deployment Model (On-Premises, Cloud, Hybrid/Hosted), Service Type (Managed Data Centre, Managed Security, Managed Network, Managed Communication and Collaboration, Managed Infrastructure and Hosting, Managed Mobility, Managed Cloud and Application, Managed Workplace/Service Desk), Enterprise Size (Small and Medium Enterprises, Large Enterprises), End-User Vertical (BFSI, Manufacturing, Healthcare and Life Sciences, Retail and E-Commerce, Government and Public Sector, IT and Telecom, Energy and Utilities, Rest of End-User Verticals), and Country (United Kingdom, Germany, France, Italy, Spain, Netherlands, Sweden, Russia, Poland, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

By Deployment Model

| On-Premises |

| Cloud |

| Hybrid/Hosted |

By Service Type

| Managed Data Centre |

| Managed Security |

| Managed Network |

| Managed Communication and Collaboration |

| Managed Infrastructure and Hosting |

| Managed Mobility |

| Managed Cloud and Application |

| Managed Workplace / Service Desk |

By Enterprise Size

| Small and Medium Enterprises |

| Large Enterprises |

By End-User Vertical

| BFSI |

| Manufacturing |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Government and Public Sector |

| IT and Telecom |

| Energy and Utilities |

| Rest of End-User Verticals |

By Country

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Russia |

| Poland |

| Rest of Europe |

| By Deployment Model | On-Premises |

| Cloud | |

| Hybrid/Hosted | |

| By Service Type | Managed Data Centre |

| Managed Security | |

| Managed Network | |

| Managed Communication and Collaboration | |

| Managed Infrastructure and Hosting | |

| Managed Mobility | |

| Managed Cloud and Application | |

| Managed Workplace / Service Desk | |

| By Enterprise Size | Small and Medium Enterprises |

| Large Enterprises | |

| By End-User Vertical | BFSI |

| Manufacturing | |

| Healthcare and Life Sciences | |

| Retail and E-Commerce | |

| Government and Public Sector | |

| IT and Telecom | |

| Energy and Utilities | |

| Rest of End-User Verticals | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Russia | |

| Poland | |

| Rest of Europe |

Key Questions Answered in the Report

How fast is spending on managed security growing across Europe?

Managed security is advancing at a 15.58% CAGR from 2026-2031 as NIS2 and DORA force continuous monitoring and incident response.

Which deployment model currently leads adoption?

Hybrid and hosted configurations commanded 46.32% share in 2025 because they balance data-sovereignty compliance with cloud elasticity.

Why are small and medium enterprises accelerating outsourcing?

EU grants plus standardized service tiers let SMEs access enterprise-grade infrastructure and security without large up-front capital outlays, driving 14.38% CAGR adoption.

What makes Poland the fastest-growing market?

Nearshoring demand, sovereign cloud zones, and government incentives are propelling Poland at a 14.01% CAGR through 2031.

Which vertical is forecast to expand the quickest?

Healthcare and life sciences lead with a 15.74% CAGR as interoperability mandates and AI diagnostics require compliant, low-latency managed services.

How fragmented is the competitive landscape?

The top ten vendors hold about 35-40% share, indicating moderate fragmentation where telecom carriers, global integrators, and Indian IT firms all compete.

Page last updated on: