Europe Excavator And Loaders Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

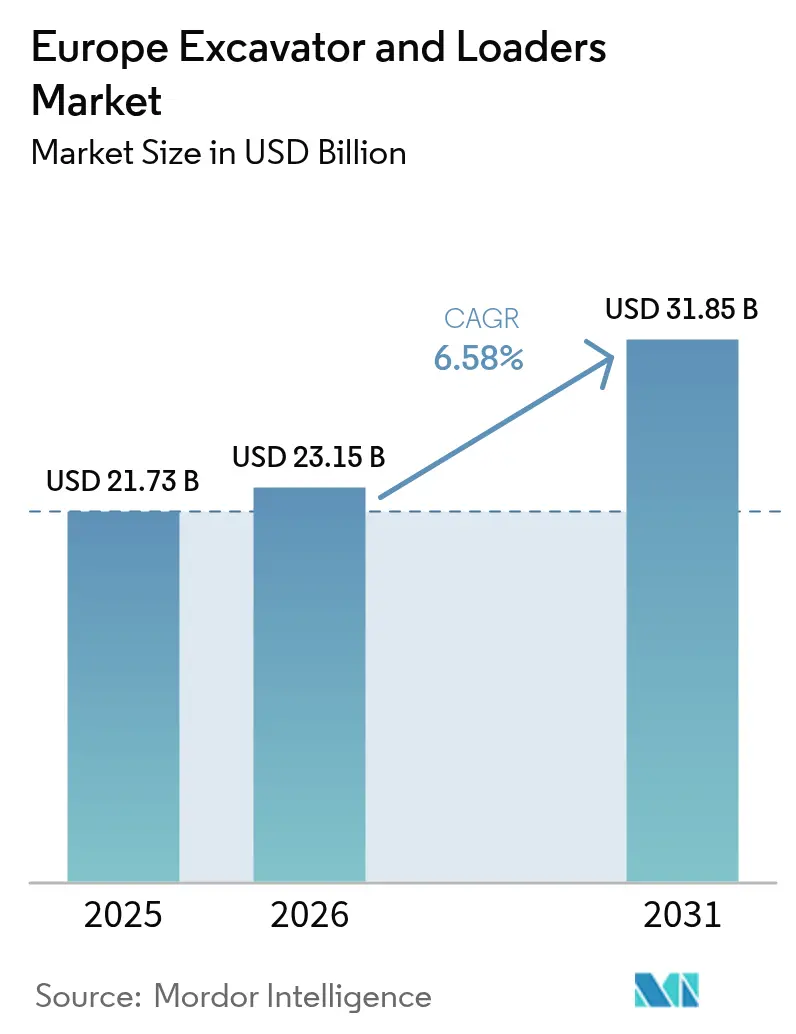

| Base Year Market Size (2025) | USD 21.73 Billion |

| Market Size (2026) | USD 23.15 Billion |

| Market Size (2031) | USD 31.85 Billion |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

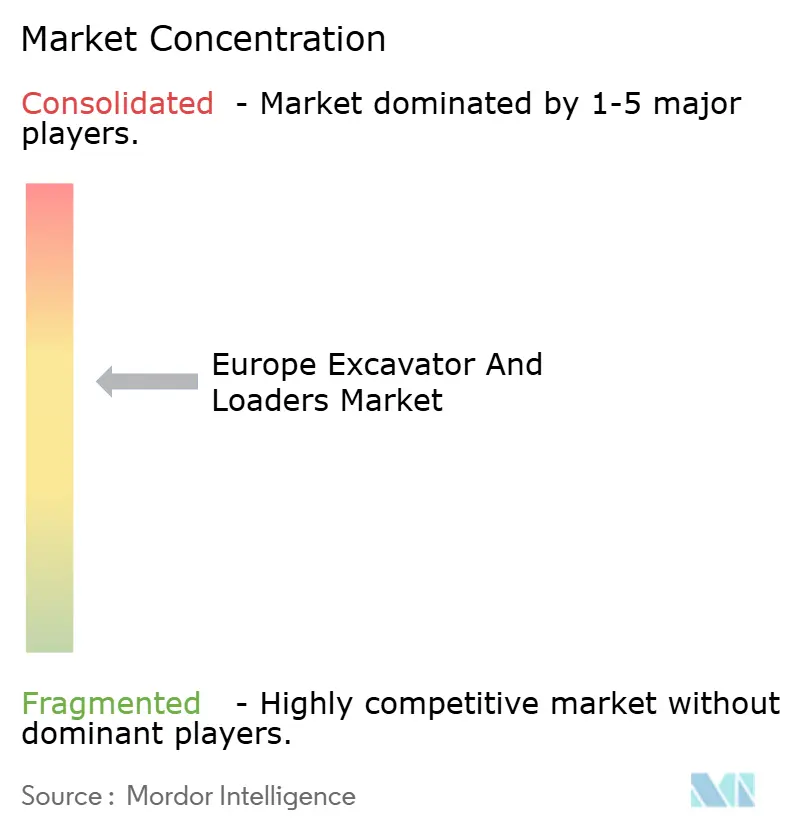

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Excavator And Loaders Market Analysis by Mordor Intelligence

The Europe Excavator And Loaders Market size is projected to be USD 21.73 billion in 2025, USD 23.15 billion in 2026, and reach USD 31.85 billion by 2031, growing at a CAGR of 6.58% from 2026 to 2031. Demand momentum rests on three pillars: net-zero infrastructure mandates, Stage V fleet replacement, and an urban shift toward compact equipment that fits tight job-sites. Contractors weigh retrofit costs against the four-year payback of electric drivetrains, while rental groups exploit high utilization to expand fleets despite elevated financing costs. Digital-twin automation and Equipment-as-a-Service contracts are further tilting preferences toward connected machines that lower unplanned downtime and de-risk residual values. As a result, the European excavators & loaders market is experiencing structural, not cyclical, growth.

Key Report Takeaways

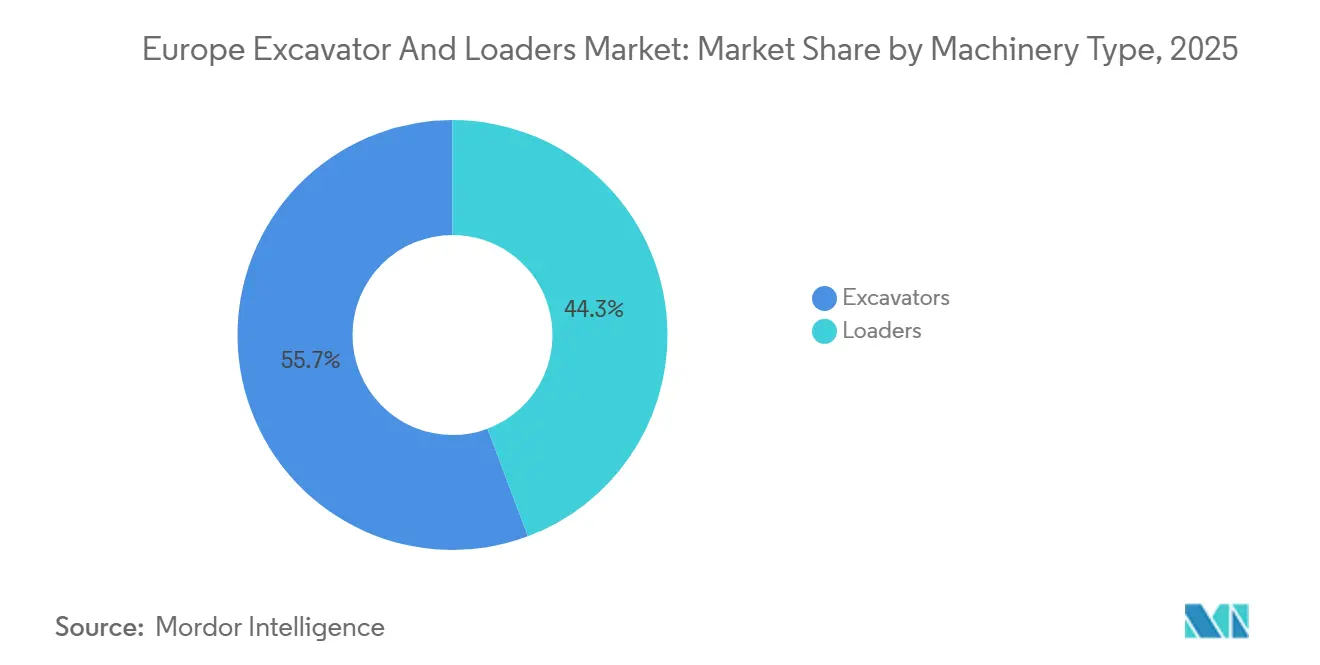

- By machinery type, excavators led the European excavators & loaders market with a 55.71% market share in 2025; loaders are forecast to expand at a 6.55% CAGR through 2031.

- By drive type, diesel and hydraulic systems accounted for 88.15% market share in 2025, while electric units are pacing at a 6.66% CAGR through 2031, continuing to reshape the European excavators & loaders market.

- By operating weight, the 6-to-14-tonne class commanded a 38.45% share of the European excavators & loaders market in 2025, yet sub-6-tonne machines are advancing at a 6.63% CAGR through 2031.

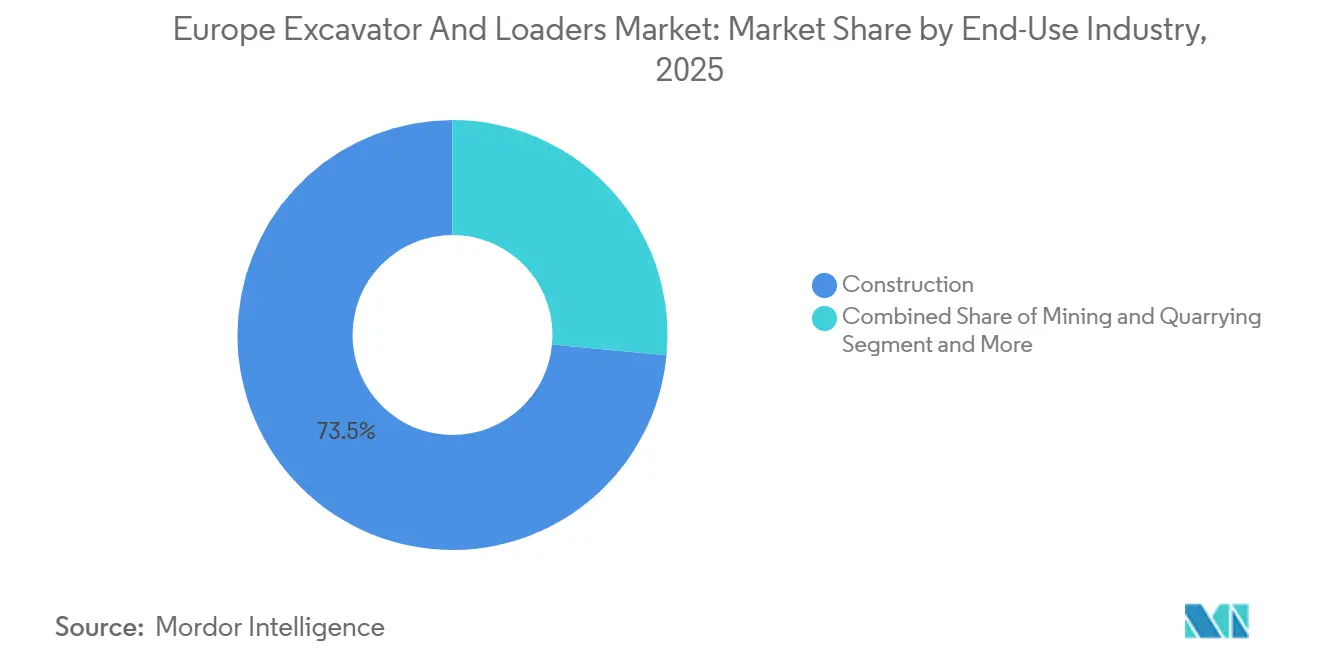

- By end-use, construction accounted for 73.51% market share in 2025. In contrast, utilities and urban infrastructure are the fastest-growing, with a 6.68% CAGR through 2031, underscoring diversification within the Europe excavators & loaders market.

- By application, excavation and earthmoving captured 41.25% market share in 2025. Demolition is projected to expand at a 6.71% CAGR through 2031.

- By country, Germany held 24.46% of market share in 2025 in the European excavators & loaders market; Norway posts the highest forecast CAGR at 6.73% by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Excavator And Loaders Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stage V Emission Norms Driving Fleet Renewal | +1.4% | EU-27, UK, Norway, Switzerland | Medium term (2-4 years) |

| EU Green-Deal Infrastructure Funding Boom | +1.2% | Pan-European, with concentration in Germany, France, Netherlands | Medium term (2-4 years) |

| Post-Pandemic Construction Backlog Release | +0.9% | France, Italy, Spain, with spillover to Eastern Europe | Short term (≤ 2 years) |

| Zero-Emission Site Mandates in Scandinavia | +0.7% | Norway, Sweden, Denmark, with pilot adoption in Netherlands | Long term (≥ 4 years) |

| Equipment-as-a-Service Business Models | +0.6% | UK, Germany, Benelux, expanding to Southern Europe | Medium term (2-4 years) |

| Digital-Twin Job-Site Automation Uptake | +0.5% | Germany, UK, France (early adopters in large-scale infrastructure) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stage V Emission Norms Driving Fleet Renewal

In Europe’s construction equipment market, Stage V emission norms are accelerating fleet renewal, particularly for excavators and loaders. Many operators, especially small- and mid-sized contractors, are trading in their older machines sooner than anticipated due to the steep costs of retrofitting them with advanced after-treatment systems. Meanwhile, electric drivetrains are gaining momentum, sidestepping retrofit costs, thanks to Germany’s tax incentives and sustainability mandates. This evolving landscape is not only reshaping procurement strategies but also amplifying leasing and certified pre-owned programs. Furthermore, it's spurring original equipment manufacturers (OEMs) to ramp up investments in electrification, hybridization, and cutting-edge battery technologies.

EU Green Deal Infrastructure Funding Boom

Under the Connecting Europe Facility, substantial funding is set to flow into transport and energy corridors over the next few years. This surge in investment is poised to boost the demand for mid-size excavators and wheel loaders. Notably, Germany and France have identified projects that will necessitate a significant increase in machinery during the latter part of the decade. Furthermore, with accelerated depreciation for zero-emission assets, rental cycles have shortened considerably, leading to a trend of early replacements in the European excavators and loaders market.

Post-Pandemic Construction Backlog Release

In 2025, Europe witnessed a pronounced surge in equipment rentals, especially in Italy, Spain, and France. This uptick followed a post-pandemic construction recovery, as governments and contractors tackled significant project backlogs from lockdowns and supply chain disruptions. Rental fleets, providing flexible machinery access without hefty capital investments, primarily absorbed this pent-up demand. This surge underscored the pivotal role of rental channels in managing short-term demand fluctuations, especially for excavators and loaders, even as new equipment sales held steady.

Zero-Emission Site Mandates in Scandinavia

Scandinavian nations are reshaping the construction equipment market with zero-emission site mandates. Norway's upcoming regulations and Sweden's bold push for emission-free targets are spurring a swift shift towards electric excavators. These initiatives are strongly motivating contractors to move away from diesel machinery, especially in urban projects with tight emission controls. Subsidies are easing the financial burden of electric equipment's higher initial costs, hastening the journey to cost parity and making the switch to electrification more feasible. This strategy is crafting a blueprint for other EU countries, merging regulatory demands with financial incentives to drive a greener fleet renewal and transform the market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Interest-Rate Environment Dampening CAPEX | -1.1% | Pan-European, with acute pressure in Southern Europe and Eastern Europe | Medium term (2-4 years) |

| Growth of Rental Fleets Suppressing Purchases | -0.8% | UK, Germany, France, Netherlands, with emerging impact in Spain, Italy | Short term (≤ 2 years) |

| Battery-Material Cost Volatility | -0.4% | EU-27, UK (affects electric-equipment adoption rates) | Medium term (2-4 years) |

| Dealer-Network Consolidation Blocking New Entrants | -0.3% | Germany, France, Italy, Spain (limits competitive pressure on pricing) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Interest-Rate Environment Dampening CAPEX

Across Europe, high interest rates are curbing capital expenditure in the construction equipment market, especially for excavators and loaders. Due to the European Central Bank's tight monetary policy, contractors face higher financing costs, making outright purchases less appealing. As a result, many contractors are either extending loan tenors to alleviate repayment pressures or choosing mid-life overhauls to prolong the service life of their current fleets. This prudent strategy not only decelerates the equipment refresh cycle and diminishes demand for new machinery but also strengthens the focus on maintenance strategies, altering procurement habits until borrowing costs become more favorable.

Growth of Rental Fleets Suppressing Purchases

During the forecast period, rental penetration grew significantly. This increase was driven by Ashtead and Loxam, which expanded their fleets substantially. Despite utilization reaching unprecedented levels, the fleet expansion limited shipments from OEMs. In the European excavators and loaders market, bundled maintenance and insurance services have reduced the breakeven point for ownership, leading to a slowdown in direct sales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machinery Type: Excavators Pull Ahead in Compact Urban Jobs

Europe's excavator and loader market size peaked at 55.71% in 2025. Mini excavators below 6 tonnes post the fastest gains, favored by zero-tail-swing designs that slip into tight pedestrian zones. Midi units between 6 and 14 tonnes hold significant weight-segment revenue and anchor foundation and trenching needs. Loaders trail but still grow at 6.55% as wheel loaders remain indispensable at aggregate plants. Skid-steer and compact track loaders win share inside interior demolition and soft-ground agriculture, respectively, reflecting diversified pull on the European excavators & loaders market.

Replacement of backhoe loaders with dedicated mini excavators and telehandlers continues, shrinking the backhoe portion. At the same time, small articulated loaders carve out space in municipal snow removal. Attachment versatility—quick couplers that allow tool swaps in 90 seconds—elevates utilization, helping OEMs lock in service revenue in the European excavators & loaders market.

By Drive Type: Electric Momentum Builds Despite Diesel Lead

Diesel and hydraulic equipment account for 88.15% of the market share, yet their grip is easing as electric shipments expand at a 6.66% CAGR through 2031. Europe excavators & loaders market share for electric machines will climb by 2031 on the back of charging costs undercutting diesel on high-hour fleets. Hybrid drivetrains appeal where charging is scarce.

Hydrogen fuel-cell pilots remain below 20 units, signaling long-term optionality but negligible volume before 2031. Cable-tethered excavators thrive in Norway’s hydropower dams, where grid access is stable. Biodiesel blends ease compliance but void warranties unless OEM-approved, leaving many contractors to leapfrog straight to battery power, a strategic inflection for the European excavators & loaders market.

By Operating Weight: Sub-6-Tonne Machines Outpace Heavier Classes

The middle 6-to-14-tonne group, with 38.45% of 2025 revenue, remains the volume workhorse and anchors rental fleets. Sub-6-tonne units grow at 6.63% as urban densification in Paris, Milan, and Brussels demands footprints under 1.8 meters and noise under 95 dB(A).

Machines weighing more than 45 tonnes, tied to quarrying and dam projects, inch forward amid coal phase-out policies. Utilization metrics favor compact models, achieving higher utilization rates for equipment weighing more than 30 tonnes, bolstering returns, and reinforcing the shift within the European excavators & loaders market.

By End-Use Industry: Construction Dominates, Utilities Surge

Construction accounted for 73.51% of demand in 2025, but utilities and urban infrastructure rose 6.68% annually as district heating and fiber-optic trenching expanded. Germany’s broadband push needs compact excavators through 2027.

Aggregate extraction and waste recycling require robust material handlers to lift non-construction shares. OEMs embed telematics as standard on rental-destined machines, keeping uptime above 90% and sharpening competitiveness across the European excavators & loaders market.

By Application: Excavation Leads, Demolition Takes Flight

Excavation and earthmoving still account for 41.25% of activity, but demolition posts the highest CAGR at 6.71% as circular-economy rules press for building deconstruction and high material-recovery rates. High-reach demolition excavators have boom capacities exceeding 30 meters.

Road building accounts for a smaller share of activity, while snow removal punches above its weight during Q1 rentals in Alpine markets. Attachment flexibility and quick-coupler systems increase machine utilization, extending the revenue arc in the European excavators & loaders market.

Geography Analysis

Germany delivered 24.46% of 2025 revenue, supported by a USD 295 billion federal transport plan that lifts machine intensity to 14.2 units per 1,000 construction employees. Electric equipment hit 11.3% of new German sales due to 50% first-year depreciation. Rental penetration climbed to 34%, softening direct OEM orders but maintaining high utilization in the European excavators & loaders market.

Norway registers the fastest 6.73% CAGR through 2031 following its 2027 zero-emission mandate and a USD 18.8 million subsidy program. Cheap hydropower at USD 0.08 per kWh assures total-cost parity above 1,200 utilization hours, explaining why 42% of 2025 orders there were electric. Sweden and the Netherlands follow growth on the back of urban renewal and offshore wind projects.

France's demand is fueled by a USD 59 billion France 2030 plan, while Italy and Spain hover near 10% as pandemic backlog unwinds [2]“France 2030 Investment Plan,” French Government, gouvernement.fr . Eastern Europe adds revenue but faces higher borrowing costs that slow replacement, a drag on localized slices of Europe.

Competitive Landscape

In 2025, Caterpillar, Komatsu, Volvo CE, and CNH Industrial collectively accounted for a significant share of European revenue, indicating a moderately concentrated profile for the European excavators & loaders market. Despite offering substantial price discounts, Chinese challengers Sany and XCMG have limited combined market share. This is mainly due to dealer exclusivity clauses that prevent them from accessing crucial service bays.

Contracts like Equipment-as-a-Service from Volvo CE and JCB shift the residual-value risk onto OEMs. This move is particularly beneficial for contractors with tighter balance sheets, facilitating a broader adoption of electric machinery. Furthermore, systems such as Caterpillar’s Command for Excavation, which utilize digital-twin and autonomous grade control technologies, have demonstrated significant reductions in operator input and fuel consumption.

Starting in 2027, the EU Machinery Directive mandates the integration of cybersecurity measures and over-the-air updates in machinery. This requirement is driving up the per-unit R&D expenditure considerably. As a result, smaller brands might either exit the market or seek consolidation, reshaping current fragmentation and bolstering the dominance of leading players in the European excavators & loaders market.

Europe Excavator And Loaders Industry Leaders

Caterpillar Inc.

Komatsu Corp.

Liebherr Group

Volvo Construction Equipment

JC Bamford Excavators Limited (JCB)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Kiloutou, aiming to generate half of its revenue from outside France, has bolstered its heavy earthmoving and aerial lift fleets by acquiring Thor Jørgensen in Denmark and F.I.M. in Italy.

- June 2025: Fayat Group has acquired Mecalac, a specialist in compact equipment, expanding its portfolio with 29 new production sites and diversifying its offerings beyond traditional road-building products.

- April 2025: Kubota entered an OEM pact to source 14-ton excavators from a peer manufacturer, with European sales slated for spring 2026.

Europe Excavator And Loaders Market Report Scope

The scope of the report includes Machinery Type (Excavators and Loaders), Drive Type (Diesel/Hydraulic, Electric, and More), Operating Weight (Below 6t and More), End-Use (Construction, Mining, and More), Application (Excavation, Material Handling, and More), and Geography.

| Excavators | Mini (Below 6 t) |

| Midi (6 to 14 t) | |

| Crawler | |

| Wheeled | |

| Amphibious | |

| Large (Above 45 t) | |

| Loaders | Wheel Loader |

| Skid Steer Loader | |

| Compact Track Loader | |

| Backhoe Loader | |

| Small Articulated Loader |

| Diesel / Hydraulic |

| Electric |

| Hybrid |

| Hydrogen Fuel-Cell (emerging) |

| Cable / Grid-tethered |

| Below 6 |

| 6 to 14 |

| 14 to 30 |

| 30 to 45 |

| Above 45 |

| Construction |

| Mining and Quarrying |

| Agriculture and Forestry |

| Waste and Recycling |

| Utilities and Urban Infrastructure |

| Rental Companies |

| Excavation and Earthmoving |

| Material Handling |

| Demolition |

| Landscaping |

| Snow Removal |

| Road Building and Maintenance |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Norway |

| Rest of Europe |

| By Machinery Type | Excavators | Mini (Below 6 t) |

| Midi (6 to 14 t) | ||

| Crawler | ||

| Wheeled | ||

| Amphibious | ||

| Large (Above 45 t) | ||

| Loaders | Wheel Loader | |

| Skid Steer Loader | ||

| Compact Track Loader | ||

| Backhoe Loader | ||

| Small Articulated Loader | ||

| By Drive Type | Diesel / Hydraulic | |

| Electric | ||

| Hybrid | ||

| Hydrogen Fuel-Cell (emerging) | ||

| Cable / Grid-tethered | ||

| By Operating Weight (t) | Below 6 | |

| 6 to 14 | ||

| 14 to 30 | ||

| 30 to 45 | ||

| Above 45 | ||

| By End-Use Industry | Construction | |

| Mining and Quarrying | ||

| Agriculture and Forestry | ||

| Waste and Recycling | ||

| Utilities and Urban Infrastructure | ||

| Rental Companies | ||

| By Application | Excavation and Earthmoving | |

| Material Handling | ||

| Demolition | ||

| Landscaping | ||

| Snow Removal | ||

| Road Building and Maintenance | ||

| By Country | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Norway | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large is the European excavators & loaders market today, and where is it headed by 2031?

It stands at USD 23.15 billion in 2026 and is projected to climb to USD 31.85 billion by 2031 at a 6.58% CAGR.

Which machinery type holds the biggest revenue share?

Excavators led with 55.71% of 2025 revenue thanks to their versatility across excavation, demolition, and material handling.

Why is electric adoption accelerating in this equipment class?

Stage V regulations, zero-emission site mandates, and four-year payback periods in high-utilization fleets make battery units increasingly economical.

Which country will grow the fastest through 2031?

Norway, posting a 6.73% CAGR, is driven by its 2027 zero-emission public works requirement and low-cost hydropower.

How are rental trends shaping equipment demand?

Rental fleets absorbing demand while higher interest rates delay contractor purchases, a dynamic likely to persist until ECB rate cuts.

Page last updated on: