Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

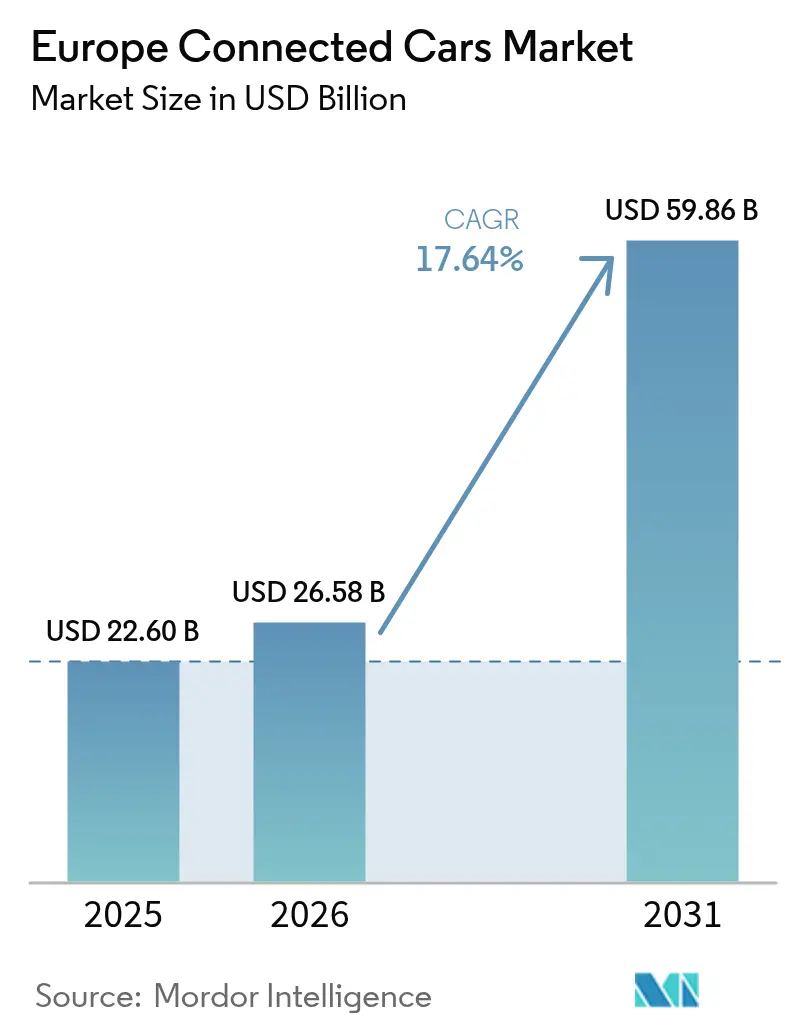

| Base Year Market Size (2025) | USD 22.60 Billion |

| Market Size (2026) | USD 26.58 Billion |

| Market Size (2031) | USD 59.86 Billion |

| Growth Rate (2026 - 2031) | 17.64% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Connected Cars Market Analysis by Mordor Intelligence

The European connected car market size was valued at USD 22.60 billion in 2025 and estimated to grow from USD 26.58 billion in 2026 to reach USD 59.86 billion by 2031, at a CAGR of 17.64% during the forecast period (2026-2031). The market's expansion stems from converging regulatory mandates, including the EU's eCall emergency response system and General Safety Regulation requirements that became effective in 2024, creating baseline connectivity standards for new vehicles[1]"Connected and automated mobility", European Commission, digital-strategy.ec.europa.eu.. This expansion mirrors the powerful mix of mandatory connectivity in every new vehicle, the region-wide 5G build-out, and the pivot toward software-defined vehicles. Automakers benefit from common EU rules such as eCall and the General Safety Regulation, enabling them to design one pan-European platform instead of many country variants. Rapid electric-vehicle (EV) uptake further lifts demand for connected services because battery health, charging, and route planning rely on live data. Germany's scale, Norway's early-mover advantage in EVs, and Nordic 5G ubiquity combine to keep Western and Northern Europe in the lead, while Eastern and Southern Europe add volume as hardware prices fall.

Key Report Takeaways

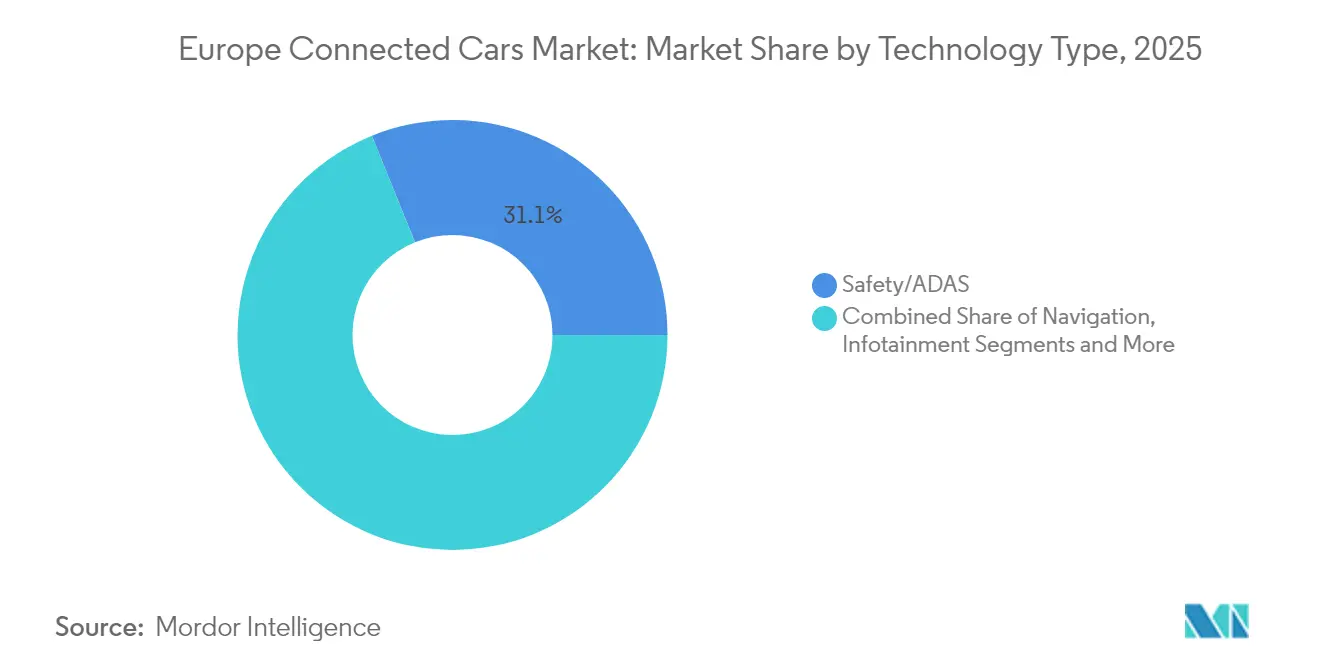

- By technology type, safety/ADAS systems led with 31.12% revenue share of the European connected car market size in 2025, while telematics and OTA updates are projected to expand at a 22.85% CAGR through 2031.

- By connectivity architecture, embedded solutions captured 51.90% of the European connected car market share in 2025, whereas hybrid connectivity is forecast to rise at 23.65% CAGR to 2031.

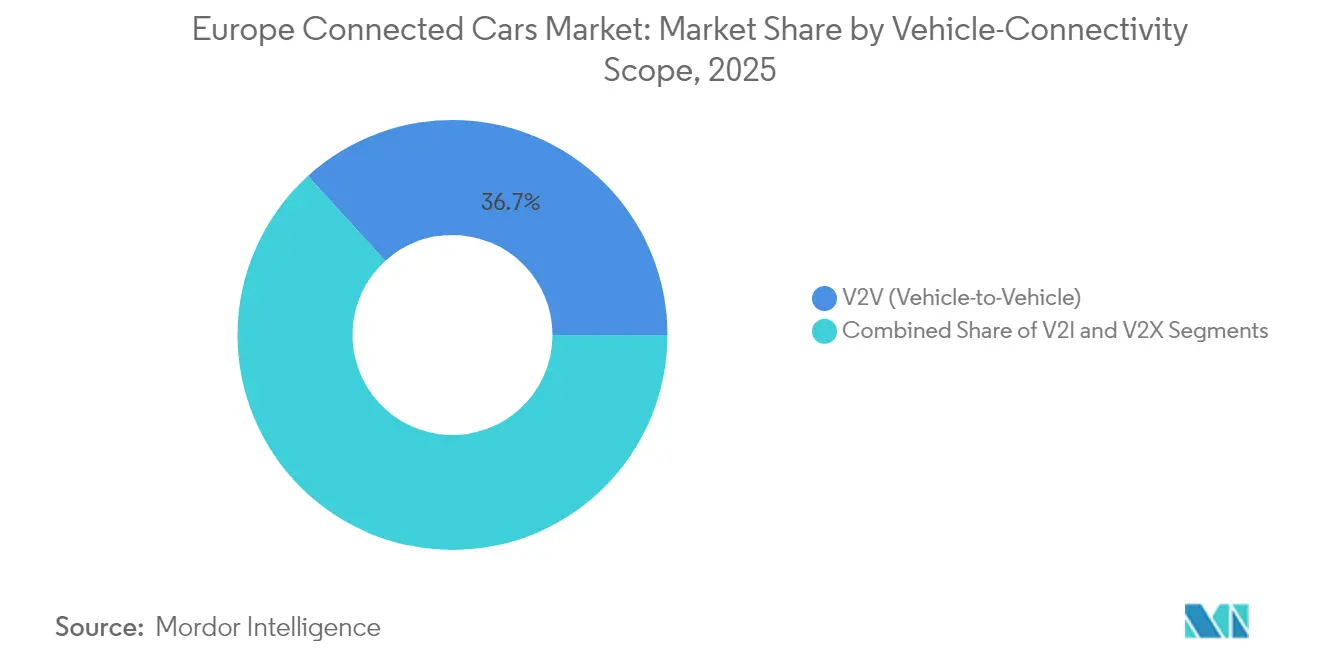

- By vehicle-connectivity scope, vehicle-to-vehicle applications held 36.74% share of the European connected car market size in 2025, and vehicle-to-everything applications are advancing at a 30.15% CAGR through 2031.

- By end-user, OEM factory-fit installations commanded 71.05% share of the European connected car market size in 2025; the fleet operators segment is expected to grow strongest at 19.05% CAGR to 2031.

- By country, Germany held 26.55% of the European connected car market share in 2025, while Norway is poised for a 18.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Connected Cars Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU eCall and General Safety Regulation Compliance Push | +4.2% | EU-wide, strongest in Germany, France, Italy | Short term (≤ 2 years) |

| 5G Roll-out Enabling Low-latency V2X | +3.8% | Nordic countries, Germany, Netherlands leading | Medium term (2-4 years) |

| Shift to Software-Defined Vehicles and OTA Updates | +3.5% | Germany, France, Sweden automotive hubs | Long term (≥ 4 years) |

| Electric Vehicle Adoption Driving Connectivity Requirements | +3.2% | Norway, Netherlands, Germany EV leaders | Medium term (2-4 years) |

| Rising Demand for Infotainment and Digital Cockpit | +2.9% | Western Europe core, expanding to Eastern Europe | Medium term (2-4 years) |

| Usage-based Insurance Accelerating Telematics Installs | +2.1% | UK, Italy, Spain with mature insurance markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU eCall and General Safety Regulation Compliance Push

The EU’s General Safety Regulation, which has been in force since 2024, obliges every new passenger car and light commercial vehicle to ship with advanced driver assistance features that rely on constant data flow. OEMs, therefore, fit embedded connectivity by default rather than as an option, driving economies of scale that lower hardware cost per vehicle. Continental’s newly branded division Aumovio illustrates the commercial response, supplying integrated sensors and connectivity stacks to multiple carmakers. The regulation’s pan-European scope removes fragmentation, enabling suppliers to market a single platform across 27 member states. Insurance firms benefit from reliable crash data, which speeds claims handling and fraud detection.

5G Roll-out Enabling Low-latency V2X

Over EUR 3 billion in Connecting Europe Facility Digital funds is earmarked for corridor-wide 5G along 26,000 km of highways, underpinning sub-20 ms latency required for safety-critical vehicle-to-everything (V2X) services. Nordic operators already show near-complete coverage; Denmark stands at 83.4% 5G availability, and Norway approaches 100%. Real-world pilots cut congestion up to 30% as vehicles coordinate with traffic lights. Satellite back-up supplied by the European Space Agency and Deutsche Telekom covers rural zones, closing gaps where terrestrial towers are sparse. While Europe trails North America on standalone 5 G roll-outs, coordinated spectrum plans should lift core-network upgrades beyond 40% coverage by 2027.

Shift to Software-Defined Vehicles and OTA Updates

Stellantis executed 94 million over-the-air updates across 13.8 million vehicles in 2023, illustrating the maturing software pipeline inside the European connected car market. The move eliminates physical recalls, cuts warranty cost, and keeps older models feature-fresh. Open-source infrastructure—such as HARMAN’s Eclipse-hosted Connected Services Platform—reduces vendor lock-in and speeds cloud-vehicle orchestration. Integrated data lakes now enable predictive maintenance that trims unscheduled downtime for fleets by up to 25%. Suppliers pivot away from pure hardware, positioning as system integrators to capture a larger share of lifecycle revenue.

Rising Demand for Infotainment and Digital Cockpit

Consumer expectations for smartphone-like experiences in vehicles drive OEMs to prioritize digital cockpit development as a differentiation strategy. Automakers forecast up to USD 1,600 annual service revenue per connected vehicle, stimulating a wave of app-store style offerings. HARMAN and the Volkswagen Group now furnish more than 70 in-car apps ranging from streaming media to IoT-device control. Subscription packages dominate, with users favoring annual billing over monthly top-ups. Hyundai’s Bluelink service, active in 15 European countries, demonstrates the scale required for localization, language, and regulatory compliance while serving more than 1 million active users.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GDPR-Driven Privacy and Cybersecurity Concerns | -2.8% | EU-wide, particularly Germany, France | Short term (≤ 2 years) |

| High Hardware and Subscription Cost of Embedded Units | -1.9% | Price-sensitive markets: Eastern Europe, Southern Europe | Medium term (2-4 years) |

| OEM–MNO Revenue-Sharing Stalemate | -1.6% | EU-wide, affecting all connectivity models | Short term (≤ 2 years) |

| Coverage Gaps on Trans-European Corridors | -1.2% | Cross-border routes, rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GDPR-Driven Privacy and Cybersecurity Concerns

The 2025 EU Data Act compels OEMs to share vehicle data with third parties, yet that same data is now classed as personal when linked to a driver, widening GDPR compliance scope. The Cyber Resilience Act adds life-cycle security obligations for every connected product sold in Europe. Meeting overlapping rules raises engineering cost, especially for smaller tier-2 suppliers. Class-action risk grows: a single sensor misconfiguration could expose movement history or biometric data, triggering regulatory fines of up to 4% of global turnover.

High Hardware and Subscription Cost of Embedded Units

Entry-level telematics control units still cost OEMs USD 700–800, a hurdle in markets where the average B-segment car sells for below EUR 20,000. Consumers in Eastern and Southern Europe remain price-sensitive, with survey data showing a gap between willingness to pay and the current premium pricing of connected plans. Embedded-SIM technology reduces roaming fees but forces redesign of vehicle electrical architectures, delaying launches. Finally, automakers and mobile-network operators continue to wrangle over revenue splits, slowing the rollout of mass-market bundles that could close the affordability gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology Type: Safety Systems Drive Current Adoption

Safety and ADAS functions held 31.12% of the European connected car market in 2025, propelled by regulation that mandates automated emergency braking, lane-keeping, and intelligent speed assistance. Across trim lines, brands embed dual-redundant cellular modules, lidar, and camera arrays to meet Euro NCAP targets, lowering per-vehicle connectivity cost and giving every buyer a baseline of connected capability. Telematics and OTA update platforms are the fastest-growing slice, rising at 22.85% CAGR as OEMs shift toward subscription revenue once the vehicle departs the showroom. In this context, the European connected car market size for telematics is projected to add USD 7.42 billion between 2026 and 2031.

A rising focus on fleet efficiency also pushes vehicle-management software. Insurers leverage rich driving telemetry to tailor premiums, supporting adoption in delivery, ride-hailing, and leasing fleets that now refresh vehicles every 36 months instead of the previous 48. Partnerships such as Volkswagen–Valeo–Mobileye illustrate the link between ADAS and software monetization, integrating Level 2+ self-driving as an optional post-purchase feature. Software up-selling, extended warranties, and functional on-demand packages redefine how automakers extract value over the life of each connected car.

By Connectivity Architecture: Hybrid Models Gain Momentum

Embedded connectivity captured 51.90% of the European connected car market in 2025 because factory-integrated modems give automakers end-to-end control. The architecture ensures uniform user experience, stable over-the-air update paths, and compliance with eCall. However, combining embedded modules with smartphone tethering, hybrid solutions are scaling faster at 23.65% CAGR. This blend preserves embedded safety for crash calls while letting entertainment traffic shift to a user’s data plan in weak-coverage regions.

BMW’s Ubigi Personal eSIM across 15 European countries is emblematic: a driver can buy a 5G plan through the infotainment screen, while fallback routing leverages the handset if local roaming tariffs spike. Such flexibility is critical in the European connected car market, where wholesale roaming fees vary widely. The European connected car market size attributable to hybrid architectures is expected to triple by 2030, reflecting component price drops and wider consumer acceptance. Tethered-only systems decline in share yet remain relevant in retrofit kits for older fleets and emerging-market imports.

By Vehicle-Connectivity Scope: V2X Approaches an Inflection Point

Vehicle-to-vehicle (V2V) links represented 36.74% of the European connected car market share in 2025, benefiting from well-established cooperative awareness standards such as ETSI ITS-G5. Still, vehicle-to-everything (V2X) traffic is where growth surges—30.15% CAGR—as cities digitalize traffic lights, signage, and curbside sensors. The C-Roads platform ensures a harmonized service menu so a car built in Spain can communicate flawlessly with road gantries in Poland.

Germany categorizes V2I bandwidth as critical infrastructure, easing municipal right-of-way permits for roadside units. Real-world pilots in Hamburg show a 22% drop in idle time at junctions once lights broadcast phase-and-timing data to connected vehicles. Looking ahead, bidirectional-charging initiatives push a new V2G use case: electric cars feeding power back into the grid during peak evenings. Analysts expect the European connected car market size linked to V2X energy services to exceed USD 2.28 billion by 2031.

By End-User: Fleets Underwrite Future Volume

OEM factory-fit solutions accounted for 71.05% of the European connected car market in 2025, due to mandatory safety hardware and automakers’ desire to own customer data. Fleets, however, are the fastest-rising group at 19.05% CAGR. Large logistics groups integrate telematics into route planning software, saving fuel and cutting CO₂ per kilometer. Stellantis’ tie-up with Samsara provides instant access to CAN bus data without aftermarket dongles, showing how embedded connectivity shortens deployment cycles.

Smaller fleets still lag, but government incentives such as reduced insurance premiums once driver-behavior monitoring is enabled accelerate take-up. Mobility providers—car-sharing, short-term rental, and ride-hailing firms—demand continuous vehicle state data for asset utilization. As autonomous shuttles enter service later in the decade, their always-connected, operator-owned business model will amplify this trend, ensuring the European connected car market gains sturdy multi-year tailwinds.

Geography Analysis

Germany held 26.55% of the European connected car market in 2025, reflecting its dominant production base and early 5G deployment. Even amid a 5% revenue drop to EUR 536 billion for the broader auto industry, German registrations of hybrid and electric vehicles rose briskly. Germany's vehicle fleet shows strong adoption of alternative drive systems, with hybrid vehicles increasing 22.2% to 3.56 million units and electric vehicles rising 17.2% to 1.65 million units as of January 2025.

Norway is projected to compound at 18.22% CAGR, the fastest in Europe. Near-universal 5G and EV adoption create perfect conditions for sophisticated vehicle-to-everything pilots, positioning the country as a test bed for autonomous features before wider EU roll-out. France blends mature telecom infrastructure with a growing 19.40% EV share of new registrations, supported by the France 2030 program’s EUR 65 million fund for 6G research that will eventually deliver 100-fold speed gains over 5G.

Southern and Eastern Europe catch up as hardware prices fall. Italy’s EV sales leaped 132.20% year-on-year in January 2025, and public chargers exceeded 64,000 by late 2024. Spain’s MOVES III plan underwrites vehicle and home-charger subsidies, while the Netherlands collaborates with Hyundai on smart-mobility sandboxes. These markets add vital volume and diversity to the European connected car market as manufacturers tailor service bundles to local income levels and data-pricing realities.

Competitive Landscape

The European connected car market shows moderate concentration. Tier-1 suppliers such as Continental, Bosch, and Valeo historically sold hardware modules; now they extend into cloud orchestration and cybersecurity, closing capability gaps that pure software firms once filled. Continental’s Aumovio spin-off underscores this pivot, grouping sensors, displays, and over-the-air stacks in one portfolio to win system-integrator contracts. HARMAN’s decision to open-source its middleware via the Eclipse Foundation creates a community that accelerates standards but still drives paid customization work back to HARMAN.

OEMs experiment with vertical integration. Volkswagen’s USD 5.8 billion platform JV with Rivian bundles German scale with Californian software DNA, aiming to unlock Level 4 autonomy by 2027. Stellantis’ EUR 4.1 billion battery plant JV with CATL tightens control over propulsion but also embeds connectivity into battery-management systems from day one[3]Michael Wayland, "Rivian-Volkswagen joint venture deal rises to up to $5.8 billion, VW cars expected as early as 2027", cnbc.com.. Meanwhile, telecom operators seek larger revenue shares by bundling in-car data plans with consumer mobile contracts, as Vodafone’s recent MVNO acquisitions show.

White-space opportunities gather around cross-border roaming optimization, cybersecurity certification, and data-brokerage hubs that mediate consent under GDPR. Chinese tech entrants, often arriving via minority stakes in EU suppliers, add competitive pressure on price and time-to-market. Collaboration across industries defines success: hardware alone no longer secures a margin, and software without vehicle know-how struggles to meet the EU’s stringent safety and privacy rules.

Europe Connected Cars Industry Leaders

-

Continental AG

-

Robert Bosch GmbH

-

Autoliv Inc.

-

Harman

-

Denso Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: HARMAN became one of the first companies to open-source a complete connected services platform with the Eclipse Foundation, supporting connected car deployments for up to 100,000 vehicles and enabling vehicle-to-cloud connectivity, data management, and user identity management functions. This strategic move accelerates software-defined vehicle development across the industry while establishing HARMAN as a platform leader in the connected car ecosystem.

- April 2025: Continental introduced its new automotive brand Aumovio following the planned spin-off and IPO scheduled for September 2025, focusing on software-defined vehicles and modern mobility solutions including advanced sensor technologies, smart displays, and assistance systems for connected and autonomous vehicles. The brand positioning emphasizes technological leadership and local presence in global mobility markets.

- March 2025: HARMAN introduced Ready Aware in Europe during MWC 2025, offering near real-time in-vehicle contextual alerts. These alerts, referred to as 'sight beyond sight,' are designed to improve driving safety at intersections and various road hazards.

Europe Connected Cars Market Report Scope

A connected car is a vehicle connected to the internet, in other words, WLAN ( Wireless local area network). This helps the vehicles to share car data with external devices/services. The market studies thus cover all the technological aspects and latest developments in the market.

The European connected cars market is segmented by technology type, Connectivity type, Vehicle connectivity type, end-user type, and country. By technology type, the market is segmented into navigation, entertainment, safety, vehicle management, and other technology types. By connectivity type, the market is segmented into integrated, embedded, and tethered. By vehicle connectivity type, the market is segmented into V2Vehicle, V2Infrastructure, and V2X.

By end-user type, the market is segmented into OEM and aftermarket; by country, the market is segmented into Germany, France, the United Kingdom, and the Rest of Europe. For each segment, market sizing and forecast have been done on the basis of value (USD billion).

By Technology Type

| Navigation |

| Infotainment |

| Safety/ADAS |

| Vehicle Management |

| Telematics and OTA Updates |

| Other Types |

By Connectivity Type

| Integrated |

| Embedded |

| Tethered |

| Hybrid (Integrated + Embedded) |

By Vehicle-Connectivity Scope

| V2V (Vehicle-to-Vehicle) |

| V2I (Vehicle-to-Infrastructure) |

| V2X ( V2C, V2P, and V2G) |

By End-User

| OEM Factory-fit |

| Aftermarket |

| Fleet Operators/Mobility Providers |

By Country

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Norway |

| Rest of Europe |

| By Technology Type | Navigation |

| Infotainment | |

| Safety/ADAS | |

| Vehicle Management | |

| Telematics and OTA Updates | |

| Other Types | |

| By Connectivity Type | Integrated |

| Embedded | |

| Tethered | |

| Hybrid (Integrated + Embedded) | |

| By Vehicle-Connectivity Scope | V2V (Vehicle-to-Vehicle) |

| V2I (Vehicle-to-Infrastructure) | |

| V2X ( V2C, V2P, and V2G) | |

| By End-User | OEM Factory-fit |

| Aftermarket | |

| Fleet Operators/Mobility Providers | |

| By Country | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Norway | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size of the European connected car market?

The European connected car market stands at USD 26.58 billion in 2026 and is projected to hit USD 59.86 billion by 2031.

Which technology segment grows fastest in the forecast period?

Telematics and over-the-air update platforms lead with a 22.85% CAGR as OEMs monetize software beyond the initial sale.

Why do embedded connectivity solutions dominate today?

EU safety mandates such as eCall require always-on modems, prompting automakers to integrate embedded hardware into every new vehicle.

Which country provides the largest revenue in connected cars?

Germany leads with 26.55% share due to its big production base and early roll-out of 5G and software-defined architectures.

Page last updated on: