Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

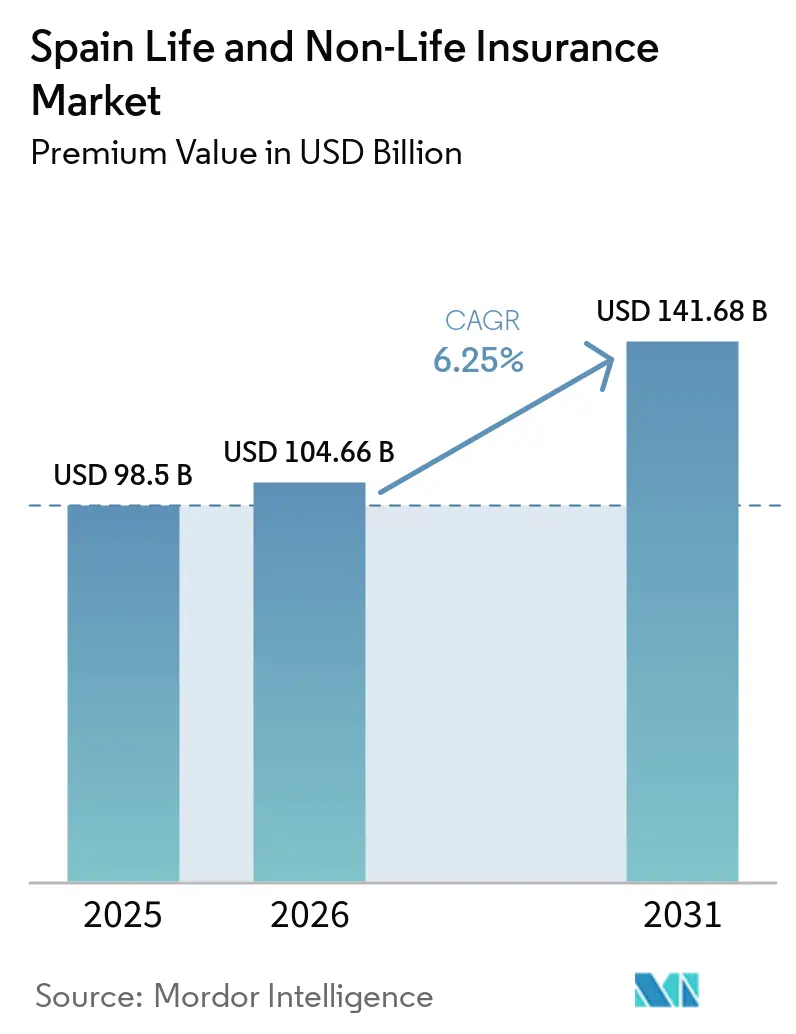

| Base Year Market Size (2025) | USD 98.5 Billion |

| Market Size (2026) | USD 104.66 Billion |

| Market Size (2031) | USD 141.68 Billion |

| Growth Rate (2026 - 2031) | 6.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Life and Non-Life Insurance Market Analysis by Mordor Intelligence

The Spain Life And Non-Life Insurance Market size in terms of premium value is projected to expand from USD 98.5 billion in 2025 and USD 104.66 billion in 2026 to USD 141.68 billion by 2031, registering a CAGR of 6.25% between 2026 to 2031.

Strong premium growth signals deeper insurance penetration, rising disposable income, and a steady migration from savings products to protection and retirement solutions. Mandatory coverages in motor, rapid uptake of private health policies, and a spike in property-catastrophe demand underpin the non-life momentum, while pension reforms and longevity trends channel fresh capital toward annuities. Digitalization is redrawing distribution economics, with bancassurance widening reach and mobile platforms improving price transparency. Scale advantages, robust risk-pricing engines, and access to granular customer data are emerging as the decisive competitive levers in the Spain life and non-life insurance market.

Key Report Takeaways

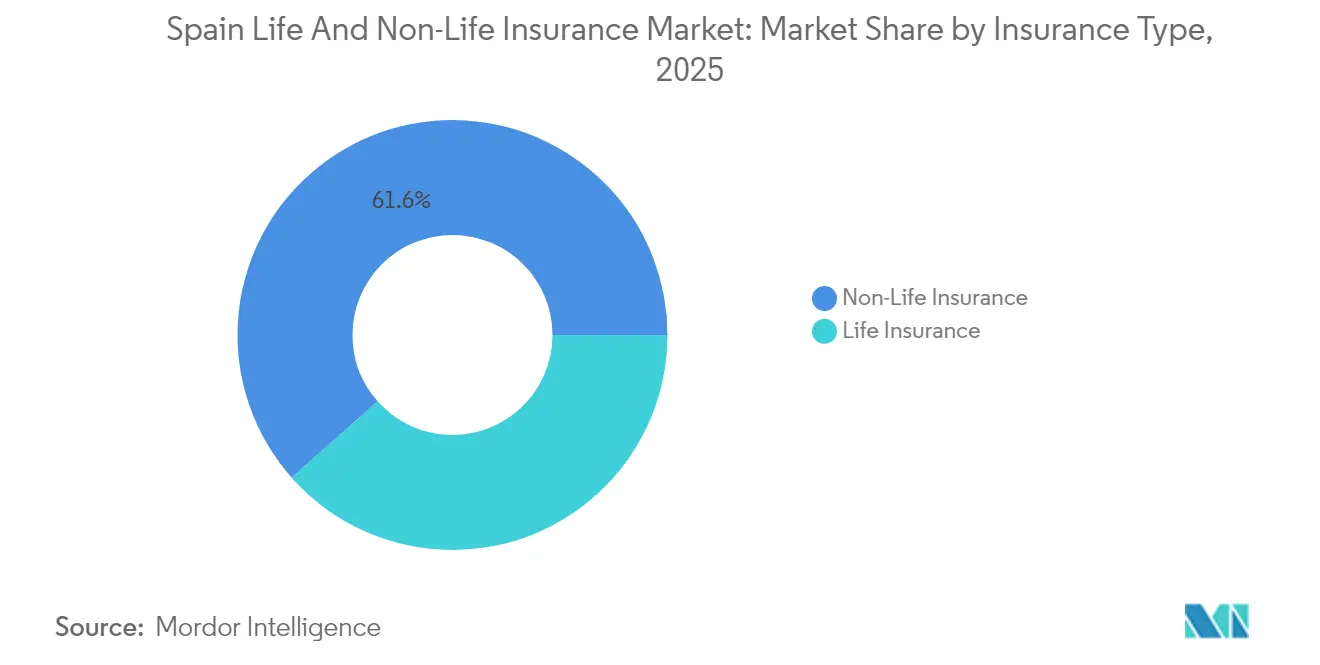

- By insurance type, non-life held 61.55% of Spain life and non-life insurance market share in 2025, while pension and annuity lines are projected to advance at a 5.6% CAGR through 2031.

- By distribution channel, bancassurance controlled 43.65% of the Spain life and non-life insurance market in 2025, whereas online and mobile sales are forecast to post a 11.75% CAGR by 2031.

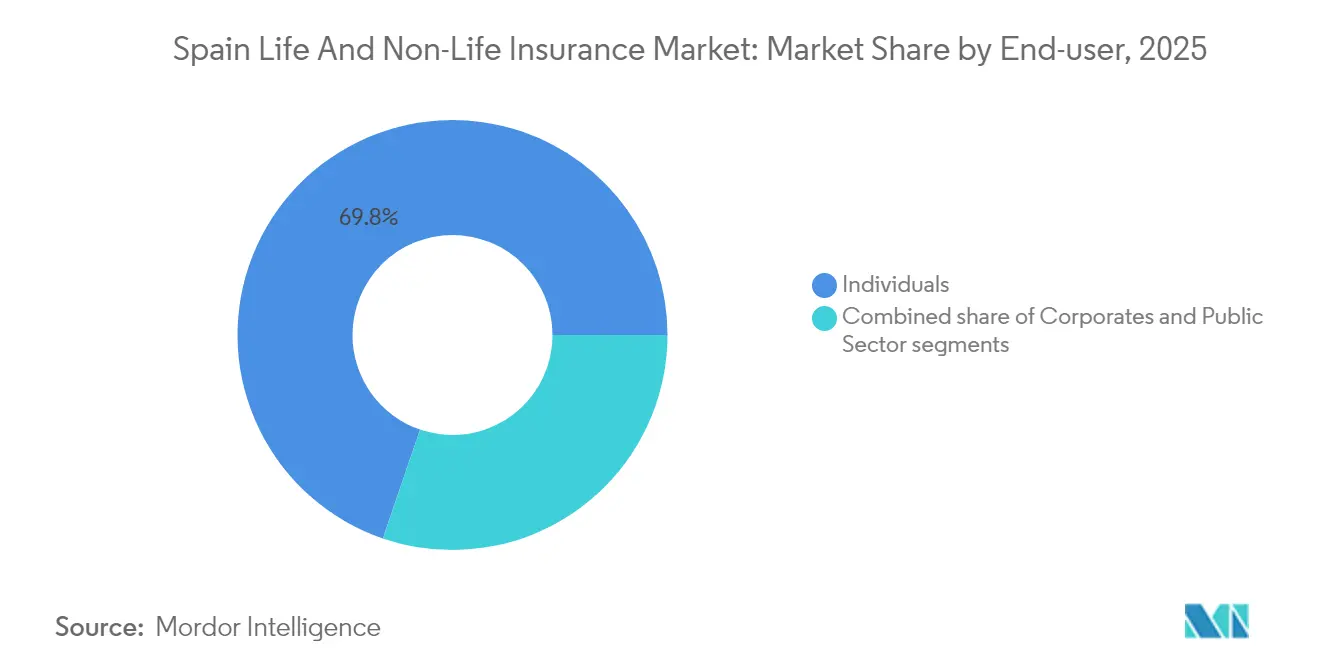

- By end-user, individuals accounted for 69.75% of Spain life and non-life insurance market size in 2025; SMEs represent the fastest-growing segment, expanding at 7.05% CAGR during 2026-2031.

- By geography, Madrid led with a 22.05% share of Spain life and non-life insurance market size in 2025, while the Valencia Community is set to log the quickest regional CAGR at 6.34% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Life and Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population driving demand for pension & annuity products in Spain | +1.8% | National; highest effect in Madrid, Catalonia, Basque Country | Long term (≥ 4 years) |

| Growth of digital bancassurance partnerships accelerating policy sales | +1.2% | Nationwide, with early traction in major urban centres | Medium term (2-4 years) |

| Mandatory motor insurance regulations boosting non-life premiums | +0.7% | National | Short term (≤ 2 years) |

| Rising climate-related catastrophes increasing demand for property & crop covers | +1.1% | Valencia, Andalusia, Catalonia; spill-over nationwide | Medium term (2-4 years) |

| Integration of health insurance with private healthcare networks expanding penetration | +0.9% | Madrid, Catalonia, Balearic Islands | Medium term (2-4 years) |

| EU Solvency II reforms enabling capital optimisation for Spanish carriers | +0.5% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population Driving Demand for Pension & Annuity Products in Spain

One in five Spaniards is already older than 65, and that share will pass 26% by 2035[1]OECD, “OECD Capital Market Review of Spain 2024,” oecd.org. The demographic swing is pushing life insurers to prioritize retirement products, with pension and annuity premiums expanding at a 5.86% CAGR between 2025 and 2030. CaixaBank’s “Generation+” suite bundles annuities, senior protection, and equity-release mortgages into a single advisory pitch, tapping a cohort that controls close to 40% of household wealth. Revised mortality tables (PER2020) sharpen pricing accuracy and highlight longevity risk hedging needs. Insurers able to match long-dated liabilities with higher-yielding assets are set to gain a share in the Spain life and non-life insurance market.

Growth of Digital Bancassurance Partnerships Accelerating Policy Sales

In 2024, banks accounted for 14.2% of domestic profits from insurance, highlighting the integral role of bancassurance in daily banking. This channel commands 44.1% of total written premiums and is now enhancing its mobile apps with features like robo-advice, data-driven cross-selling, and instant policy issuance. SegurCaixa Adeslas showcases the power of scale by seamlessly integrating CaixaBank’s 21 million retail clients with timely health, home, and motor insurance offers. With reduced acquisition costs and improved conversion rates, bancassurance is becoming more productive, driving growth in Spain's life and non-life insurance sectors.

Mandatory Motor Insurance Regulations Boosting Non-Life Premiums

Spanish law obliges every registered vehicle to carry liability cover, and improved enforcement tools such as real-time traffic-police databases are shrinking the uninsured pool. Motor premiums account for over one-quarter of non-life revenues. Despite a combined ratio above 100% in 2024, telematics-based pricing and tighter fraud controls are helping carriers adjust rates. New-vehicle registrations rebounded in early 2024, supporting volume and regulatory certainty should keep motors a cornerstone of the Spain life and non-life insurance market.

Rising Climate-Related Catastrophes Increasing Demand for Property and Crop Covers

Floods, wildfires, and droughts are lifting insured losses and sharpening risk perception. The Consorcio de Compensación de Seguros (CCS) has paid USD 11.04 billion for extraordinary events since 1987, cushioning private-sector volatility[2]Fitch Ratings, “Spain’s CCS aids re/insurance stability amid climate risks,” fitchratings.com. After the 2024 Valencia flood, combined multi-risk property ratios remained below 95%, proving the model’s resilience. Premiums in flood-prone zones are rising by low single digits, and demand for agriculture covers is climbing as crop yields grow more erratic. Climate risk, therefore, adds a structural tailwind to the Spain life and non-life insurance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently low interest-rate environment compressing life-insurance margins | -0.8% | National | Short term (≤ 2 years) |

| High combined ratios in motor line limiting profitability for non-life insurers | -0.6% | National | Medium term (2-4 years) |

| Increasing competition from insurtechs eroding traditional agents’ share | -0.4% | Urban hubs, notably Madrid and Barcelona | Medium term (2-4 years) |

| Stricter IFRS 17 reporting requirements raising compliance costs | -0.5% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistently Low Interest Rate Environment Compressing Life Insurance Margins

Guaranteed-return savings blocks still sit on many life balance sheets, and ultra-low yields compress spread income. Although the European Central Bank began tightening in 2024, reinvestment rates lag minimum credited rates on legacy policies. Life players are pivoting to unit-linked contracts that transfer investment risk, but transition costs weigh on near-term profitability across the Spain life and non-life insurance market.

High Combined Ratios in Motor Line Limiting Profitability for Non-Life Insurers

Supply-chain inflation, pricier spare parts, and larger bodily injury awards pushed the 2024 motor combined ratio past 100%. Carriers are filing for sharper rate increases and deploying AI-driven claims triage, yet loss severity remains sticky. Until underwriting breaks even, capital allocation to faster-growing lines such as health and SME packages may dilute Motor’s growth contribution within the Spain life and non-life insurance market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Non-Life Dominates While Pension Products Surge

Non-life generated 61.55% of total written premiums in 2025, a position reinforced by the compulsory motor cover, climate-linked property demand, and a 30% health insurance penetration rate in several urban provinces. The Spain life and non-life insurance market continues to rely on the motor for volume, yet property and crop lines are rising steadily after the October 2024 Valencia floods. Life products captured the remaining 38.45% of premium income, with pension and annuity contracts rising 5.6% per year to 2031 as households seek predictable post-retirement cash flows. Revised PER2020 mortality tables raise capital for longevity risk but give pricing accuracy that supports new annuity issuance.

Growth in life savings has shifted toward unit-linked schemes that insulate insurers from investment-guarantee drag while meeting clients' appetite for equity exposure. Meanwhile, whole-life policies remain a niche wealth-transfer tool for high-net-worth individuals in Madrid and Catalonia. The Spain life and non-life insurance market size tied to non-life still dwarfs life, yet the margin contribution from pension contracts is climbing, aided by solvency-friendly reinsurance. Carriers that can balance capital-intensive traditional reserves with fee-based asset-light products should widen ROE spreads. Claims automation and behavioral pricing in motor and household lines further enhance expense ratios, giving diversified groups a structural advantage.

By Distribution Channel: Bancassurance Leads as Digital Disrupts

Bancassurance wrote 43.65% of premiums in 2025, leveraging 30,000+ Spanish bank branches and the trust halo of incumbent lenders. The Spain life and non-life insurance market depends on these alliances to reach mass-market savers, especially for pension plans sold alongside current accounts. Embedded application-programming-interface (API) links now let bank mobile apps issue instant quotes, cross-sell hospital cash policies, and push renewal prompts that cut lapse rates below 3%.

Still, online and mobile direct platforms are scaling at a 11.75% CAGR through 2031, the fastest of any channel, as comparison sites and digital aggregators encourage price-first shopping. Agents and brokers retain an advisory edge in complex liability and marine covers for exporters, though fee pressure mounts. As omnichannel behavior takes hold, insurers with seamless hand-offs from the web to branch to call center report higher Net Promoter Scores and lower churn. The Spain life and non-life insurance market share mix is therefore migrating to digital, but bancassurance will likely remain core in life products because of bank deposit stickiness and big-data underwriting.

By End-User: Individuals Dominate While SMEs Accelerate

Individual households accounted for 69.75% of premium volume in 2025, underpinned by mandatory auto policies and the appeal of private health as waiting lists lengthen in public hospitals. The Spain life and non-life insurance market benefits from extensive consumer awareness campaigns and tax incentives for retirement products. Within the retail base, affluent clients demand universal-life wrappers for wealth transfer, while millennials lean toward usage-based auto and micro-duration travel covers purchased via smartphones.

SMEs, comprising more than 99% of Spanish firms, are now the fastest-growing segment at 7.05% CAGR as insurers roll out bundled multiline packages that cover property, liability, and employee benefits. VidaCaixa’s MyBox Vida Negocios offers self-employed professionals flexible coverage and tax deductibility, while MAPFRE pursues cross-selling through Bankinter branches. Digital underwriting portals shorten turnaround times from days to minutes, a key draw for resource-constrained small-business owners. Large corporates continue to self-insure high retentions but still source catastrophic risk transfer and expatriate medical plans from the commercial arms of major insurers.

By Cross Segmentation: Distribution Channel Reshapes Insurance-Type Dynamics

Distribution preferences vary sharply by product. Bancassurance captures nearly two-thirds of individual pension sales as bank advisers package retirement funds and annuities with mortgages. Conversely, direct-to-consumer digital portals win in standardized motor and gadget covers, where instant fulfillment and transparent pricing override face-to-face interaction. This pattern shows how the Spain life and non-life insurance industry aligns high-advice products with human channels while routing commoditised risks to algorithms.

Embedded insurance, a flight-booking site selling travel protection, or a lender bundling payment-protection premium into a loan expands reach without extra distribution cost. Yet product complexity can accelerate if coverages are mismatched to the channel, exposing carriers to reputational loss. Comparative-advantage analysis confirms bancassurance’s cost efficiency but hints at service-quality trade-offs, pushing some incumbents to co-brand with insurtechs to lift experience scores. Strategic channel orchestration will, therefore, define future winners in the Spain life and non-life insurance market.

Geography Analysis

Madrid contributed 22.05% of premium income in 2025 on the back of a dense corporate footprint, the nation’s highest GDP per capita, and a 40.46% private health insurance penetration rate. Foreign direct investment stock of EUR 379.82 billion (USD 395.60 billion) magnifies risk-transfer needs, catalyzing sophisticated employee-benefit schemes and high-sum-assured life contracts. Catalonia ranks second; Barcelona’s tech cluster and manufacturing base favor cyber, marine, and supply-chain policies that require bespoke underwriting. Penetration remains high, with 34.16% of residents holding private health cover, and insurers nurture insurtech partnerships to meet urban digital demand.

Andalusia, with its large population and growing tourism sector, trails in penetration yet offers significant upside as disposable incomes climb. Health and property lines dominate new premium intake, while agricultural micro-covers gain from the region’s extensive farming footprint. The Basque Country features a cooperative insurer ecosystem and above-average income, supporting multi-risk commercial packages for industrial exporters.

Valencia Community is tipped as the fastest-growing territory at a projected 6.34% CAGR to 2031, spurred by reconstruction demand following the 2024 floods and a vibrant SME base in ceramics and agri-food. The state-backed CCS scheme ensured prompt claims payment, boosting consumer trust and willingness to renew cover. Finally, the Balearic and Canary Islands exhibit high travel and health-insurance uptake tied to tourism economies, while rural interior provinces remain under-penetrated but are opening up through mobile sales platforms, deepening the Spain life and non-life insurance market footprint.

Competitive Landscape

The top five players, VidaCaixa, Mapfre, Mutua Madrileña, Zurich, and AXA, command the lion’s share of written premiums, reflecting a moderately concentrated Spain life and non-life insurance market. VidaCaixa excels in life and pension lines through CaixaBank’s branch network, achieving a scale that supports short payback on digital investments. Mapfre combines 3,000+ retail offices with one of the country’s most downloaded insurance apps and plans to add another 300 outlets by 2028.

Health insurance is more tightly held: SegurCaixa Adeslas, Sanitas, Asisa, DKV, and Mapfre account for a majority stake, leveraging vertical integration with private hospital chains. In property catastrophe, the CCS backstop levels the playing field, but carriers with sophisticated catastrophe-model capabilities can price granular risks more accurately and keep combined ratios sub-100%.

Digital insurgents such as Prima Seguros and Simple focus on auto or SME niches, using straight-through processing and customer-experience design to erode incumbent share. International specialists, for example, Munich Re Specialty, will underwrite from 2025 and may push rates lower in facultative reinsurance layers. M&A continues: BMS bought Rasher for credit and surety expansion, while MEDVIDA Partners absorbed VidaCaixa’s legacy books to build scale and chase annuity flows. Players that master both acquisition cost control and capital-light product design appear best positioned to retain margins.

Spain Life and Non-Life Insurance Industry Leaders

Mapfre S.A.

VidaCaixa (CaixaBank Group)

Mutua Madrileña

AXA Seguros S.A.

Allianz Seguros

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: MAPFRE is committed to open 300 additional offices within three years and improving auto-insurance profitability while targeting SME life growth.

- March 2025: Inocsa acquired Grupo Catalana Occidente for GBP 1.94 billion, marking one of the largest recent Spanish insurance takeovers.

- November 2024: The CCS disbursed claims after the severe Valencia and Malaga floods, drawing on EUR 10 billion (USD 10.41 billion) reserves and demonstrating systemic resilience.

- May 2024: MEDVIDA Partners acquired VidaCaixa’s life portfolio to achieve scale in closed-book management.

- May 2024: AM Best shifted Spain’s non-life outlook from negative to stable as rate adequacy improved.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Spanish life and non-life insurance market as all direct written premiums and policy fees collected in Spain for life, pension and annuity, motor, property, liability, health, marine, aviation, transport and credit covers. Figures are expressed in current United States dollars and represent gross written premium before outward reinsurance; a view we find most useful for clients comparing carrier opportunity.

We exclude inward reinsurance, Lloyd's-placed Spanish risks and surety bonds for foreign projects because they sit outside the domestic premium pool we measure.

Segmentation Overview

- By Insurance Type (Gross Written Premium, USD Billion)

- Life Insurance

- Term Life

- Endowment

- Whole Life / Universal

- Pension & Annuities

- Non-Life Insurance

- Motor

- Property & Casualty

- Health

- Liability

- Credit & Surety

- Marine, Aviation & Transport

- Life Insurance

- By Distribution Channel

- Agents & Brokers

- Bancassurance

- Direct (Tied) Sales

- Online & Mobile

- Affinity & Partnerships

- By End-user

- Individuals

- Mass Market

- High-Net-Worth Individuals

- Corporates

- SMEs

- Large Enterprises

- Public Sector

- Individuals

- By Region (Spain)

- Madrid

- Catalonia

- Andalusia

- Valencia Community

- Basque Country

- Rest of Spain

Detailed Research Methodology and Data Validation

Primary Research

We spoke with regulators, senior actuaries at composite carriers, bancassurance managers in Madrid and Barcelona, and founders of motor-telematics insurtechs. These interviews helped us confirm pricing moves, lapse behavior, and digital uptake that raw statistics rarely reveal.

Desk Research

Our team began with official premium series from the Directorate-General for Insurance and Pension Funds, ICEA surveys, Banco de España macro data, and Eurostat demographics; then mapped regulatory shifts through IAIS, Swiss Re sigma, and OECD papers that track solvency and pricing controls. We supplemented those with company filings, investor decks, and news captured via D&B Hoovers and Dow Jones Factiva to pinpoint line-level growth and average selling price trends. The sources listed are illustrative; many additional open datasets supported consistency checks.

Market-Sizing & Forecasting

A top-down build converts audited gross written premium by line into USD using the annual average exchange rate; then sets our base year. Results are tested with selective bottom-up carrier roll-ups and channel checks on policy counts and sampled ASP values. We feed GDP growth, disposable income, ten-year sovereign yield, vehicle registrations, new housing completions, and per-capita health spend into a multivariate regression to create scenario bands; the mid-band becomes the published number. Any bottom-up data gaps are bridged with sampled ASP × volume from ten leading carriers.

Data Validation & Update Cycle

Our analysts run variance and peer-ratio checks, re-contact experts when anomalies appear, and pass every model through multi-step review before sign-off. Mordor refreshes the study each year and issues interim updates when events such as tax reform or extreme weather losses materially shift the baseline.

Why Mordor's Spain Life and Non-Life Insurance Baseline Commands Reliability

Published estimates often diverge, and we acknowledge that users need to know why.

Differences usually reflect scope choices, currency treatment, and refresh timing.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 98.5 B | Mordor Intelligence | - |

| USD 78.1 B | Global Consultancy A | Excludes pension annuity premiums and uses three-year average FX rates |

| USD 64.23 B | Industry Data Service B | Stops at 2024 data and omits unit-linked life premiums |

These contrasts show that Mordor's disciplined scope selection, timely updates, and twin validation steps give decision-makers a transparent, dependable baseline.

Key Questions Answered in the Report

What is the current value of the Spain life and non-life insurance market and how fast is it growing?

Premiums total USD 104.66 billion in 2026 and are forecast to expand to USD 141.68 billion by 2031 at a 6.25% CAGR.

Which product lines are posting the fastest growth?

Pension and annuity premiums are rising at a 5.6% CAGR (2026-2031), the quickest pace among all life insurance categories.

How important is bancassurance compared with digital channels?

Bancassurance controls 43.65% of total written premiums, while online and mobile sales are the fastest-growing channel, with a 11.75% CAGR projected through 2031.

Which regions hold the largest and fastest-growing shares of premium income?

Madrid leads with a 22.05% share of total premiums in 2025; Valencia Community is expected to record the highest regional growth at a 6.34% CAGR to 2031.

What regulatory changes are shaping market dynamics?

Ongoing Solvency II updates and IFRS 17 implementation improve capital optimization but raise compliance costs, favoring larger carriers with stronger risk-management systems.

Why do motor insurers face profitability pressure?

Inflation in repair costs and higher bodily-injury claims pushed the 2024 motor combined ratio above 100%, prompting rate increases and wider use of telematics-based pricing to restore margins.

Page last updated on: