Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 22.58 Billion |

| Market Size (2031) | USD 24 Billion |

| Growth Rate (2026 - 2031) | 1.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Life And Non-Life Insurance Market Analysis by Mordor Intelligence

The Poland life and non-life insurance market size reached USD 22.58 billion in 2026 and is projected to reach USD 24.00 billion by 2031 at a 1.23% CAGR during the forecast period (2026-2031).

The demand environment reflects a mature profile shaped by aging demographics and a shrinking working-age population, yet insurance remains central to long-term savings, healthcare access, and enterprise risk transfer across the economy. Non-life lines anchor volumes due to mandatory motor third-party liability and rising property exposures, while private health cover is the fastest growing line as households and employers seek faster care outside the public system. Capital strength and a stable Solvency II regime support resilience against climate shocks and macro volatility, with solvency ratios comfortably above prudential thresholds across the market. Digital distribution and embedded models are reshaping acquisition as comparison platforms and mobile-first journeys become mainstream, while scale carriers invest in analytics and automation to manage costs and improve claims experiences.

Key Report Takeaways

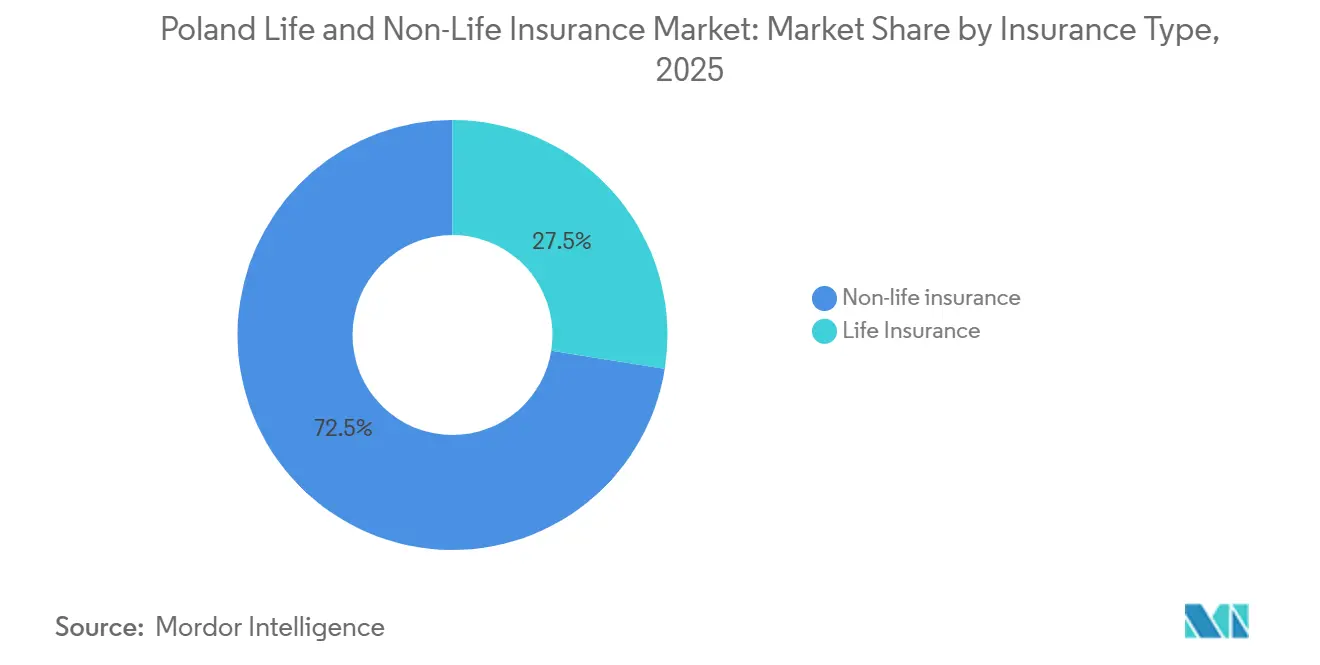

- By insurance type, non-life led with 72.50% of the Poland Life and Non-Life Insurance Market share in 2025 and health insurance in the Poland Life and Non-Life Insurance Market is forecast to expand at a 5.60% CAGR through 2031.

- By customer segment, retail accounted for 71.20% share of the Poland Life and Non-Life Insurance Market size in 2025, and retail is projected to grow at a 3.50% CAGR through 2031.

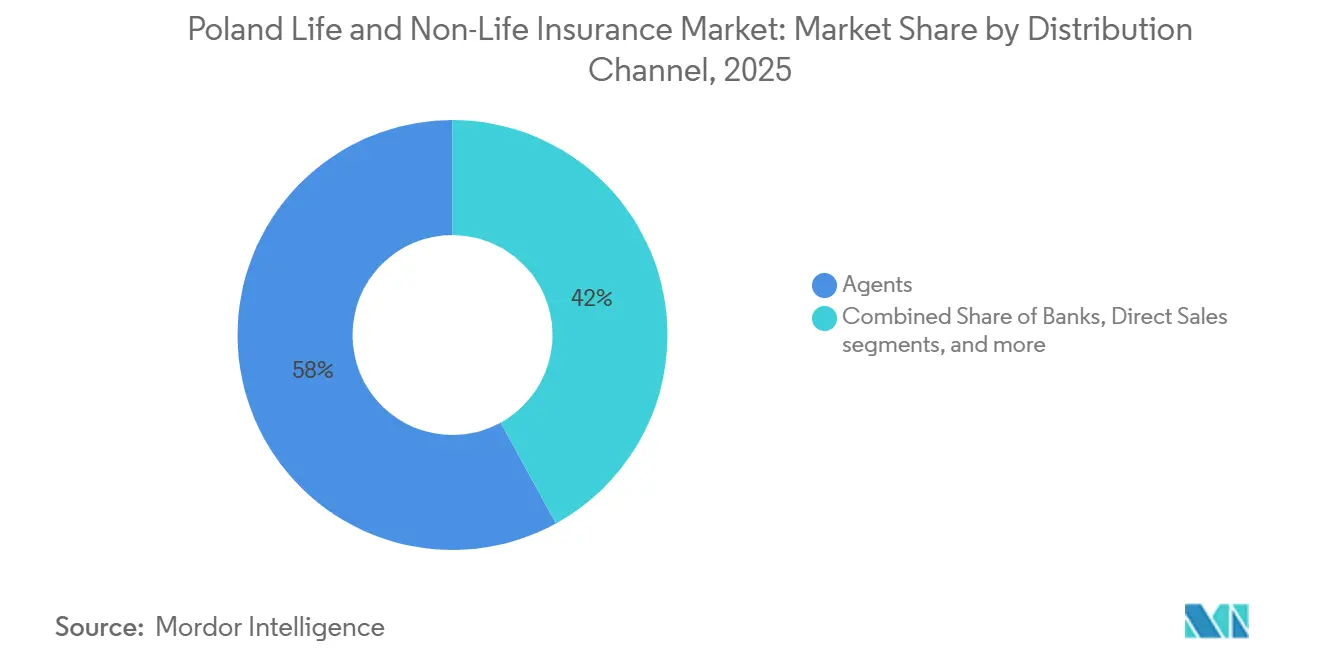

- By distribution channel, agents commanded 58% of the Poland Life and Non-Life Insurance Market share in 2025, while direct channels are projected to grow at a 4.40% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Poland Life And Non-Life Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macroeconomic growth and the strong role of insurers as institutional investors | +0.3% | National, with concentration in Warsaw, Kraków, and Wrocław, commercial hubs | Medium term (2-4 years) |

| Rising role of insurance in household security, savings, and retirement planning | +0.4% | National, higher adoption in urban centers and among middle-income households | Long term (≥ 4 years) |

| Structural shift from life to non-life with motor and property growth | +0.2% | National, spill-over from EU safety and emissions regulations | Medium term (2-4 years) |

| Expansion of unit-linked and investment-type life products | +0.2% | National, especially in major metropolitan areas | Medium term (2-4 years) |

| Stable Solvency II-based regulatory and solvency framework | +0.1% | National, uniform KNF supervision | Long term (≥ 4 years) |

| Significant contribution to GDP, employment, and economic activity | +0.1% | National, pronounced in Warsaw’s financial cluster and regional hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Macroeconomic Growth and Institutional Investment Role

Poland recorded 2.9% GDP growth in 2024 and is projected to expand by 3.0–3.6% in 2025, which supports premium formation as household consumption and corporate investment remain constructive in the near term[1]UNIQA Group, “UNIQA Poland: A Cornerstone of Growth,” uniqagroup.com. EU recovery funding channeled toward infrastructure, healthcare, agriculture, and energy transition adds a further lift to capex and employment that underpins non-life and savings-linked demand. Insurers act as large institutional investors that stabilize the financial system, with PZU Group managing PLN 503 billion in assets at year-end 2024, which helps finance public borrowing and corporate growth through bonds and equity investment[2]PZU, “GRUPA PZU | Factsheet 2024,” pzu.pl. Investment income from these portfolios provides a buffer against underwriting volatility in motor and property lines during periods of claims inflation and catastrophe activity. The combined effect is a supportive macro backdrop for the Poland life and non-life insurance market as real-economy growth and insurer balance sheets reinforce each other.

Rising Role in Household Security, Savings, and Retirement

Households are expanding coverage across protection, savings, and retirement as public-system constraints widen the role of private solutions for healthcare and long-term planning. Private health insurance premiums rose 35.3% year-on-year to PLN 2.3 billion in 2024 and covered 5.39 million people, which signals broad-based employer and individual adoption in response to longer waiting times in the public system[3]Polska Izba Ubezpieczeń (PIU), 'Polish companies in 2024 insured trade turnover worth over PLN 939 billion,' piu.org.pl. The Insurance Distribution Directive framework is nudging the market toward suitability and transparency, which supports the uptake of voluntary products over time as consumers gain confidence and understanding. Demographic aging is intensifying the need for private savings and income protection as dependency ratios increase and households seek efficient vehicles for retirement. These trends deepen the long-run penetration path for the Polish life and non-life insurance market as protection and savings become a stable component of household financial planning.

Structural Shift from Life to Non-Life with Motor and Property Growth

Non-life continues to lead the portfolio mix as mandatory MTPL and property risks maintain steady demand that is reinforced by higher asset values and claims-cost inflation. In the first half of 2025, MTPL gross written premiums reached PLN 9.77 billion, and the average premium rose to PLN 548, which returned the MTPL line to a technical profit of PLN 52.96 million after a prior-year loss. Telematics and safety programs help carriers segment risk and provide discounts for safer driving, while repair costs rise due to advanced safety systems that require specialized calibration. Property underwriting faces pressure from extreme-weather events, highlighted by September 2024 floods that generated PLN 3.84 billion in claims and pushed non-life combined ratios higher. This shift strengthens the Poland life and non-life insurance market as underwriting responds through pricing, risk selection, and customer incentives that better align premiums with exposure.

Product flexibility that includes partial surrenders, premium holidays, and annuity conversion fits evolving household retirement needs and gives carriers room to personalize benefits. Regulatory and judicial scrutiny after past mis-selling has driven clearer disclosure and simpler fee structures, which reduce friction and support renewed trust in investment-type life products. PZU Group’s scale and distribution depth, coupled with regulatory expectations for bancassurance practices and sustainable finance classification, shape the pathway for transparent growth in investment-linked offerings. Together, these developments support the role of investment-type policies in the Poland life and non-life insurance market as households seek tax-efficient, market-linked savings vehicles that complement protection cover.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low insurance penetration and household wealth compared with Western Europe | -0.3% | National, with a pronounced effect in rural and lower-income regions | Long term (≥ 4 years) |

| Financial literacy and insurance-awareness gaps among households | -0.2% | National, particularly in smaller cities and agricultural communities | Medium term (2-4 years) |

| Premium Sensitivity to Economic & Interest-Rate Cycles | -0.4% | National, acute in urban middle-class and investment-linked segments | Medium term (2-4 years) |

| Demographic Ageing Straining Public Systems & Insurer Liabilities | -0.3% | National, with higher pressure in urban and industrial regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Low Insurance Penetration and Household Wealth Differential

Penetration remains well below Western Europe, and this gap shows in property and motor protection shortfalls that elevate household vulnerability to accidents and extreme weather losses. Poland’s per capita spending and GDP-penetration metrics are lower than peers such as Austria, which leads to underinsurance in property and limited uptake of comprehensive motor beyond compulsory MTPL. The shortfall persists across lines as households balance affordability against risk, which constrains growth in discretionary covers and narrows risk pooling. Public compensation for agricultural disasters reduces incentives to buy private property cover and heightens moral hazard where budgets are tight. These factors weigh on growth and narrow the risk base of the Polish life and non-life insurance market, even as insurers and policymakers test solutions that could improve affordability and uptake over time.

Financial Literacy and Insurance-Awareness Gaps

Financial literacy is uneven, and a sizable share of consumers carry only compulsory coverage, which reduces willingness to consider complex or long-duration products. Implementation of the Insurance Distribution Directive aims to reinforce suitability and disclosure, yet smaller networks face execution gaps that slow consumer understanding and dampen trust. Consumer-protection oversight has increased, and complaints on unfair terms and claims practices are driving simpler wording and clearer product comparisons. Carriers are investing in digital education and self-service platforms to explain coverage and support better shopping decisions that reflect customer risk profiles and budgets. Progress is steady rather than rapid, and broader awareness is a prerequisite for sustained expansion of the Poland life and non-life insurance market beyond compulsory lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insurance Type: Non-Life Dominance Anchored by Motor, with Health as Growth Catalyst

Non-life accounted for 72.50% of the Poland life and non-life insurance market size in 2025, which reflects the combined pull of mandatory MTPL and persistent property exposures across households and enterprises. Casco attachment increased as vehicle values rose and customers sought own-damage protections that lower replacement-cost risk, while telematics incentives supported safer driving and more granular pricing. Property underwriting absorbed heavy weather losses in September 2024 when floods generated claims that pushed combined ratios higher and prompted repricing in exposed zones. These conditions show non-life’s structural lead in the Poland life and non-life insurance market as carriers refine risk selection and claim efficiency to balance exposure with earnings.

Health is the fastest-growing non-life line and is projected to expand at a 5.60% CAGR through 2031 as households and employers seek faster access and broader provider networks than public coverage can deliver. Private health premiums increased 35.3% in 2024 and covered 5.39 million people, which affirms the role of employer-sponsored plans and rising interest in telemedicine and negotiated provider tariffs. Partnerships with nationwide medical networks improve appointment access and keep claims inflation in check through contracted rates, although urban capacity constraints can still create delays for non-urgent procedures. Investment in prevention and integrated health-management services is growing as carriers bundle occupational-health and wellness with property and liability cover for corporate clients, which supports cross-sell and retention. Life products continue to evolve as unit-linked offerings gain share within long-term savings, and this mix shift complements non-life growth to sustain the Poland life and non-life insurance market through the cycle.

By Customer Segment: Retail Majority with Corporate Lines Gaining Traction

Retail customers held 71.2% of gross written premiums in 2025, which underscores household demand for motor, property, health, and long-term savings that remains core to growth. In retail motor, policy counts and average premiums rose in 2025 as pricing reflected higher claims costs and vehicle values, while telematics discounts and digital journeys improved shopping and switching. Private health continued to expand with 5.39 million covered at year-end 2024, driven by employer benefits and rising self-pay adoption to access faster diagnostics and specialist care. Underinsurance in property remains a constraint since many insured homes carry sums below replacement cost, and flood riders are not universal, although severe weather events have increased awareness and policy upgrades. Insurers are deploying straight-through-processing and AI-based fraud controls to reduce expense ratios in retail lines, which improves sustainability and helps the Poland life and non-life insurance market manage price-sensitive demand.

Corporate clients made up the remaining share and tend to show steadier loss ratios due to structured risk management, lower acquisition costs, and larger policy limits, although exposure to catastrophe losses can create lumpiness. Fleet motor is a competitive arena where targeted pricing, driver training, and telematics integration reduce incidents and align premiums with behavior, supporting total cost-of-risk improvement for logistics and delivery operators. Commercial property and business interruption remain core corporate lines, while financial lines such as D&O and cyber continue to grow with regulatory and litigation exposures in the EU context. Credit insurance trends reflect macro cycles and insolvency patterns, which require tight underwriting and strong recoveries to protect margins. These dynamics reinforce the diversification benefits of the Poland life and non-life insurance industry and allow scale carriers to bundle risk engineering with cover to meet enterprise needs.

By Distribution Channel: Agent Networks Dominant, but Direct and Digital Channels Accelerating

Agents commanded a 58% share in 2025 as face-to-face advice remained important for life, health, and multi-line household coverage, where product complexity and personal context matter. Multi-agent platforms and proprietary networks continue to professionalize distribution using CRM and compliance tools that support suitability and disclosure, which align with supervisory expectations under the Insurance Distribution Directive. PZU maintains an extensive footprint with branches, exclusive agents, and broker partnerships that deliver national reach and enable multi-product cross-sell, which supports scale efficiency. Bancassurance remains critical for life and credit-linked protection, where supervisory guidance has shifted portfolios toward more customer value and regular-premium structures. This blend of distribution approaches sustains access and trust across customer cohorts and underpins momentum in the Poland life and non-life insurance market.

Direct distribution is the fastest-growing channel at a projected 4.40% CAGR to 2031 as digital-native customers prioritize convenience, transparency, and instant fulfilment for standard products such as motor and home. Embedded models are advancing through partnerships such as Orange Poland and bolttech, which bring telco-scale reach to insurance comparison and purchase, with optional agent support by phone to satisfy regulated advice needs. Comparison sites aggregate quotes and streamline selection across carriers, while direct-to-consumer motor specialists leverage telematics and usage-based pricing to attract lower-risk drivers. Brokers focus on complex and large risks, place reinsurance capacity, and align incentives with client outcomes through fiduciary duty and licensed independence. This multi-channel architecture improves reach and economics, which broadens participation in the Poland life and non-life insurance market across retail and corporate segments.

Geography Analysis

Major urban centers with high income levels, asset values, and corporate activities are the main areas for regional premium formation. Digital adoption in these areas facilitates broader product uptake and cross-selling. In 2026, the life and non-life insurance market in Poland was valued at a significant amount, with projections to grow further by 2031, reflecting a modest CAGR. However, this growth rate does not reflect the differences between metropolitan hubs and rural areas. Warsaw stands out due to dense clusters of corporate headquarters, high-value residential properties, and affluent households. These households typically maintain diverse portfolios, including motor, home, health, and investment-linked life products. In 2024, Tri-City Gdańsk recorded the highest average MTPL premium, influenced by factors such as traffic density, port logistics, and coastal weather impacting claims. Carriers are varying prices by postal code and using telematics and mobility data to identify risks more precisely and improve risk-adjusted growth in Poland's insurance market.

In 2024, Southern Poland experienced severe floods, leading to significant claims. This increase in claims raised non-life combined ratios and highlighted the need for strong reinsurance and local mitigation strategies. Insurers have tightened terms in flood-prone areas and are advising on risk reduction measures. These include installing property-level flood defenses and relocating critical equipment to reduce expected losses. Property underinsurance remains a challenge as many households lack comprehensive coverage or adequate sums insured, leaving them vulnerable to total losses during severe events. Policymakers are exploring ways to increase coverage rates. At the same time, carriers and industry associations are conducting educational campaigns to emphasize the value of coverage and encourage adoption. These efforts aim to improve risk awareness and ensure that pricing and coverage align with exposure in Poland's insurance market.

Eastern regions show lower penetration due to lower incomes and older demographics, which reduces demand for voluntary products beyond compulsory MTPL and basic property cover. Agricultural insurance needs are distinct, and uptake of unsubsidized policies is limited, which can amplify loss volatility in severe weather and reduce resilience for farm operations. Cross-border reinsurance provides capacity for catastrophe and specialty risks, with Polish Re and global markets helping domestic carriers manage accumulation. Regulatory harmonization under Solvency II and the Insurance Recovery and Resolution Directive ensures capital and resolution standards align with Western European peers, which supports confidence for foreign-owned subsidiaries. These features sustain stability and allow investment in new products and risk modeling to strengthen long-run resilience in the Poland life and non-life insurance market.

Competitive Landscape

The market is moderately concentrated and intensely competitive as scale carriers and focused mid-tier players deploy pricing, digital engagement, and specialty capabilities to protect and grow share.

PZU leverages brand strength, national distribution, and large asset portfolios to negotiate favorable reinsurance terms, secure provider discounts, and sustain a low expense ratio that supports profitability in motor and property. Warta gained share in large-fleet MTPL in the first half of 2025 based on targeted underwriting, telematics-linked pricing, and integrated fleet-management solutions that help clients reduce accident frequency. ERGO Hestia strengthened its digital service through a highly rated mobile app and AI-powered customer support, which compresses claims cycle times and reduces loss-adjustment expenses in standard motor products. These moves reflect broader shifts toward analytics, automation, and value-added services that differentiate offerings beyond headline price in the Poland life and non-life insurance market.

Strategic emphasis on health coverage is expanding due to public system constraints and employer demand, which supports bundled offerings that integrate prevention, telemedicine, and occupational health. UNIQA positioned Poland as a cornerstone of its CEE growth and launched Sustainable Business Solutions that combine climate-risk advisory and ESG support with traditional property and liability lines for corporate clients. Allianz and Generali continue to deepen bancassurance distribution to cross-sell protection at account opening or mortgage origination, which improves share of wallet across retail customers. Embedded distribution models are advancing through Orange Poland and bolttech, which use telco reach to open digital front doors for motor and home insurance purchases with optional agent assistance. Together, these strategies broaden acquisition, increase stickiness, and strengthen lifetime value in the Poland life and non-life insurance market.

Capital strength and risk transfer remain central to performance, and ratings have recognized robust solvency and underwriting in recent years. S&P’s positive outlook on PZU reflected strong capital and earnings, while reinsurance access from global markets supports the underwriting of catastrophe and specialty risks without breaching capital thresholds. The memorandum of understanding between PZU and Bank Pekao proposes a financial conglomerate that could enhance bancassurance and lending capacity if approved, which would reshape distribution and capital allocation. Vienna Insurance Group simplified its local structure through mergers that support operating and capital efficiencies, a sign of continued rationalization in the market. Investments in AI and cloud platforms aim to reduce expense ratios, accelerate claims, and detect fraud, which strengthens competitiveness in price-transparent lines across the Polish life and non-life insurance market.

Poland Life And Non-Life Insurance Industry Leaders

PZU Group

Allianz Group

UNIQA Group

Generali Group

Ergo Hestia Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Orange Poland partnered with insurtech bolttech to launch “Insure with Orange”, a digital insurance comparison platform allowing customers to compare and purchase motor and home insurance policies online, leveraging mobile channels to disrupt traditional distribution.

- June 2025: PZU Group and Bank Pekao signed a memorandum of cooperation for a potential merger, creating a financial conglomerate with planned completion by June 30, 2026, potentially unlocking significant capital surpluses and supporting strategic lending growth.

- January 2025: The EU’s Insurance Recovery and Resolution Directive (IRRD) entered into force on January 28, 2025, establishing a harmonised EU framework for insurers’ recovery and resolution planning to strengthen sector stability and protect policyholders, with Member States required to adopt implementing rules by January 29, 2027.

Poland Life And Non-Life Insurance Market Report Scope

The life and non-life insurance market is defined as the sector offering financial protection. Life insurance covers individuals, providing death benefits or savings, while non-life insurance covers property, liability, and other risks, including health, auto, and home insurance. Both segments mitigate financial risks for individuals and businesses.

The Polish life and non-life insurance market is Segmented by insurance type (life [individual and group] and non-life [home, motor, and other non-life insurance types]) and distribution channel (direct, agency, bank, and other distribution channels). The report offers market size and forecasts in terms of value (USD) for all the above segments.

By Insurance Type

| Life Insurance | |

| Non-Life Insurance | Motor Insurance |

| Health Insurance | |

| Property Insurance | |

| Liability Insurance | |

| Other Insurance |

By Customer Segment

| Retail |

| Corporate |

By Distribution Channel

| Brokers/Agents |

| Banks |

| Direct Sales |

| Other Channels |

| By Insurance Type | Life Insurance | |

| Non-Life Insurance | Motor Insurance | |

| Health Insurance | ||

| Property Insurance | ||

| Liability Insurance | ||

| Other Insurance | ||

| By Customer Segment | Retail | |

| Corporate | ||

| By Distribution Channel | Brokers/Agents | |

| Banks | ||

| Direct Sales | ||

| Other Channels | ||

Key Questions Answered in the Report

What is the current Poland life and non-life insurance market outlook to 2031?

The Poland life and non-life insurance market size is USD 22.58 billion in 2026 and is projected to reach USD 24.00 billion by 2031 at a 1.23% CAGR.

Which segment leads the Poland life and non-life insurance market, and which is growing fastest?

Non-life leads with a 72.50% share, while health is the fastest-growing product line with a 5.60% CAGR through 2031.

How concentrated is competition in the Poland life and non-life insurance market?

The top five carriers control roughly 78% of premiums, which points to moderate concentration with active competition.

Which distribution channels dominate in the Poland life and non-life insurance market?

Agents hold a 58% share and remain central for complex products, while direct channels are the fastest growing with a 4.40% CAGR.

What is driving the rise of private health cover in the Poland life and non-life insurance market?

Longer public waiting times and employer demand for benefits are pushing households toward private health insurance, lifting coverage to 5.39 million people in 2024.

How do solvency and regulation support stability in the Poland life and non-life insurance market?

Strong Solvency II capitalization and the forthcoming IRRD enhance resilience through robust capital, governance, and recovery and resolution tools.

Page last updated on: