Financial Services and Investment Intelligence

29th JulyWealth Management Intelligence for the Middle East

4 Min Read

The Europe Travel Insurance Market Report is Segmented by Coverage Type (Single Trip Travel Insurance, Annual Multi-Trip Travel Insurance), End User (Senior Citizens, Education Travelers, Business Travelers, and More), Distribution Channel (Insurance Intermediaries, Insurance Companies, Banks, and More), and Geography (United Kingdom, Germany, France, and More). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

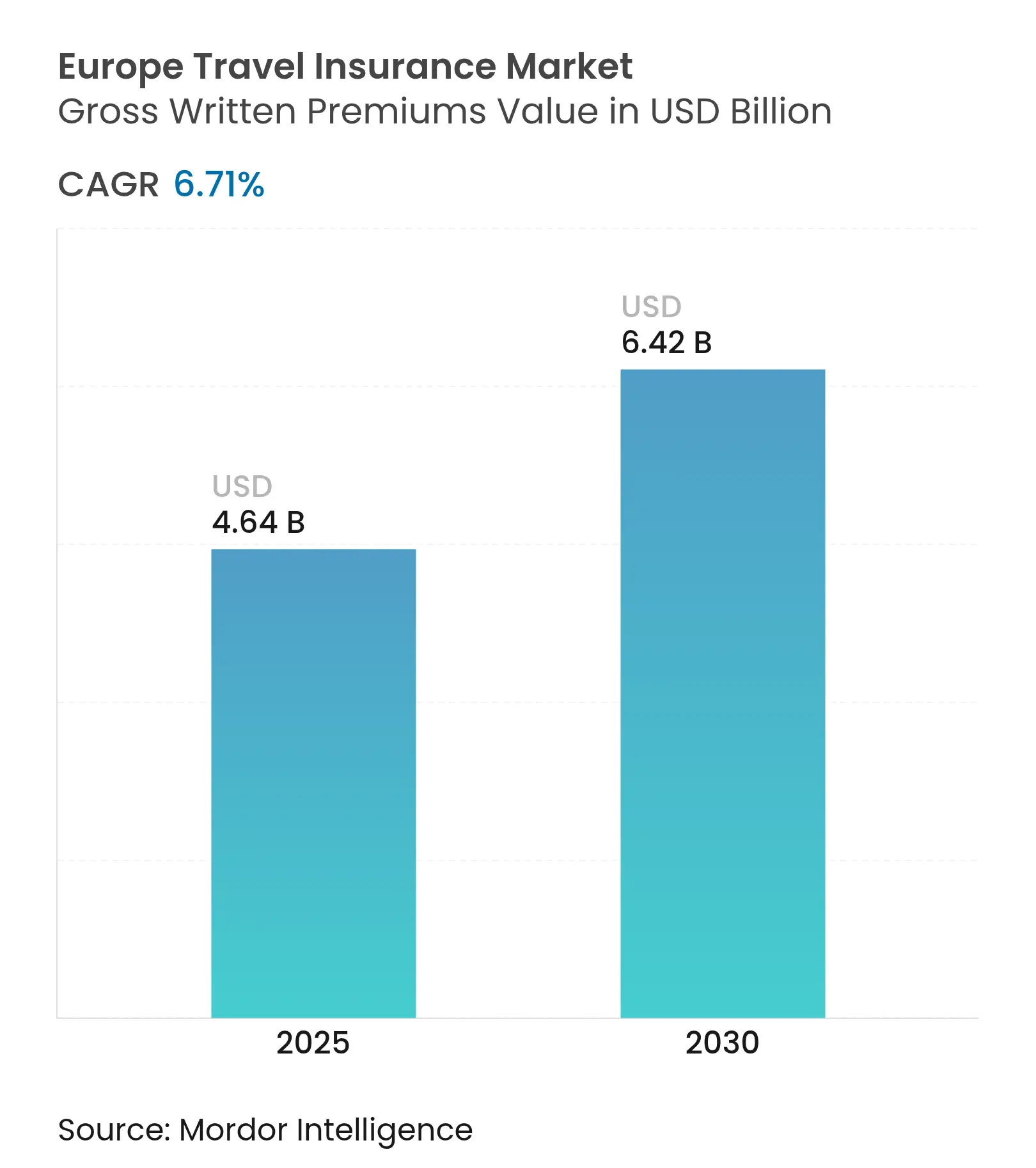

| Market Size (2025) | USD 4.64 Billion |

| Market Size (2030) | USD 6.42 Billion |

| Growth Rate (2025 - 2030) | 6.71 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The Europe travel insurance market size reached USD 4.64 billion in 2025 and is forecast to climb to USD 6.42 billion by 2030, expanding at a 6.71% CAGR. The rebound of cross-border tourism, stricter entry rules that demand proof of medical cover, and the rapid digitalization of distribution are strengthening the Europe travel insurance market. Pent-up leisure demand, higher average trip values, climate-related disruption risks, and demographic shifts toward an older traveler base add further momentum to the Europe travel insurance market. Competitive pressure is intensifying as embedded policies sold through airlines, online travel agencies, and neobanks lower acquisition costs and raise customer expectations. Meanwhile, EIOPA’s 2025 supervisory guidelines on sustainability and IT risk are pushing insurers to upgrade compliance systems, favoring incumbents that already possess large capital buffers and advanced data analytics capabilities[1]European Insurance and Occupational Pensions Authority, “EIOPA publishes Guidelines on digitalization and IT risk,” eiopa.europa.eu..

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Tourism rebounds after pandemic

restrictions

Tourism rebounds after pandemic

restrictions

| +2.1% | Mediterranean destinations, pan-European corridors | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

+2.1%

|

Geographic Relevance

:

Mediterranean destinations, pan-European

corridors

|

Impact Timeline

:

Short term (≤ 2 years)

|

€30,000 Schengen medical-cover rule and

EU Digital ID rollout

€30,000 Schengen medical-cover rule and

EU Digital ID rollout

| +1.8% | Schengen Area and UK–EU routes | Medium term (2-4 years) | |||

Rise of digital and embedded distribution

models

Rise of digital and embedded distribution

models

| +1.4% | Northern Europe and the DACH region | Medium term (2-4 years) | |||

An aging population seeking high-limit

medical cover

An aging population seeking high-limit

medical cover

| +0.9% | Western Europe and Nordic countries | Long term (≥ 4 years) | |||

Climate-driven trip disruption cover

Climate-driven trip disruption cover

| +0.6% | Mediterranean and Alpine regions | Medium term (2-4 years) | |||

Parametric “instant-payout” products

Parametric “instant-payout” products

| +0.4% | Netherlands, Germany, United Kingdom | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rebound of Tourism Across Europe

Visitor arrivals surpassed pre-2020 highs in 2025, renewing demand for emergency medical and trip-cancellation policies that underpin premiums in the Europe travel insurance market. Southern European resort hubs recorded record summer occupancy, stressing local health systems and underscoring the need for overseas treatment cover[2]European Environment Agency, “Economic losses from weather- and climate-related events in Europe,” eea.europa.eu.. Cruise lines resumed full itineraries, encouraging multi-trip policies that protect frequent voyagers against port deviations and quarantine costs. Blended “bleisure” travel has lengthened average stays, lifting perceived value of annual coverage. Technology-enabled medical assistance networks now coordinate cross-border care faster, boosting customer confidence.

Schengen Visa Rule & EU Digital ID

Mandatory proof of at least USD 31,246.8 (EUR 30,000) medical protection for Schengen visa applicants effectively transforms insurance from an optional purchase to an entry prerequisite. Spain’s July 2025 rule requiring British visitors to show private travel insurance is one example of these tougher standards [3]International Travel & Health Insurance Journal, “Spain makes insurance mandatory for British tourists,” itij.com. . The forthcoming EU Digital ID will allow border agents to verify policies in real time, shrinking fraud risk and shortening airport queues. Larger insurers are investing in interoperable policy databases that comply with privacy codes, while smaller firms face higher certification costs. Over time, standardized rules are likely to lift baseline coverage limits across the Europe travel insurance market.

Rapid Growth of Digital & Embedded Distribution

More than one-third of personal-lines premiums in Europe are already sold online, and travel products are at the forefront of that shift. German carrier ERGO embedded “O2 Care | Travel” into mobile phone bills, turning roaming data triggers into insurance activation events. Irish insurtech Companjon integrates cancel-for-any-reason protection directly into Omio’s rail, bus, and ferry bookings, illustrating context-aware underwriting. Such models reduce customer acquisition expense and collect granular travel data that refines risk pricing. As conversion rates rise, insurers reallocate marketing budgets away from paid-search aggregator listings toward API-based partnerships that scale across multiple markets.

Aging Population Needs Higher-Limit Cover

Europe’s median traveler age continues to rise, pushing demand for premium policies with expansive medical limits, repatriation guarantees, and pre-existing condition waivers. The European Commission notes that people aged 65 years and older now represent more than 20% of the region’s residents[4]European Commission, “Ageing Europe — statistics on population developments,” ec.europa.eu.. Senior travelers are willing to pay for telemedicine and post-trip follow-up care options, creating upselling opportunities. Insurers add wearable-device monitoring and multilingual assistance lines to appeal to this demographic. Accurate underwriting for chronic conditions remains complex, prompting carriers to partner with specialist medical networks.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Premium inflation from rising

cross-border healthcare costs

Premium inflation from rising

cross-border healthcare costs

| -1.6% | Nordic countries and high-income markets | Short term (≤ 2 years) |

(~) % Impact on CAGR Forecast

:

-1.6%

|

Geographic Relevance

:

Nordic countries and high-income markets

|

Impact Timeline

:

Short term (≤ 2 years)

|

Commoditization and price wars on

comparison sites

Commoditization and price wars on

comparison sites

| -1.2% | United Kingdom and Germany | Medium term (2-4 years) | |||

Regulatory scrutiny of high

ancillary-sales commissions

Regulatory scrutiny of high

ancillary-sales commissions

| -0.8% | All EU member states | Medium term (2-4 years) | |||

Expansion of EHIC-plus digital health

cover

Expansion of EHIC-plus digital health

cover

| -0.7% | Intra-EU travel corridors | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Premium Inflation Pressure

Hospital costs in several Nordic capitals climbed by double digits in 2024, forcing underwriters to raise medical-benefit premiums. Larger players can pool exposure across geographies, but smaller carriers struggle to absorb sudden spikes. Travelers in price-sensitive segments, notably students and backpackers, sometimes downgrade coverage or travel uninsured, eroding penetration rates. Some insurers respond with tiered deductibles or co-pays that temper headline pricing yet risk negative customer perception. Reinsurers are also tightening terms, particularly for destinations with volatile healthcare pricing. As pharmaceutical advancements and medical technologies evolve, treatment costs, especially for emergency interventions and specialized procedures sought by travelers, continue to rise.

Commoditization Across Online Channels

Aggregator sites list dozens of near-identical policies, often sorted by price. This transparency compresses margins as insurers undercut one another to secure clicks. Marketing costs on search engines and social media rise, diluting net premium earned per policy. To differentiate, incumbents emphasize 24/7 assistance, instant claims settlement, and lifestyle add-ons like cyber-security protection. Smaller underwriters find it difficult to fund similar service upgrades, prompting market exit or merger activity in the Europe travel insurance market. As competition for advertising heats up on search engines and social media platforms, the costs of acquiring customers through digital channels are on the rise.

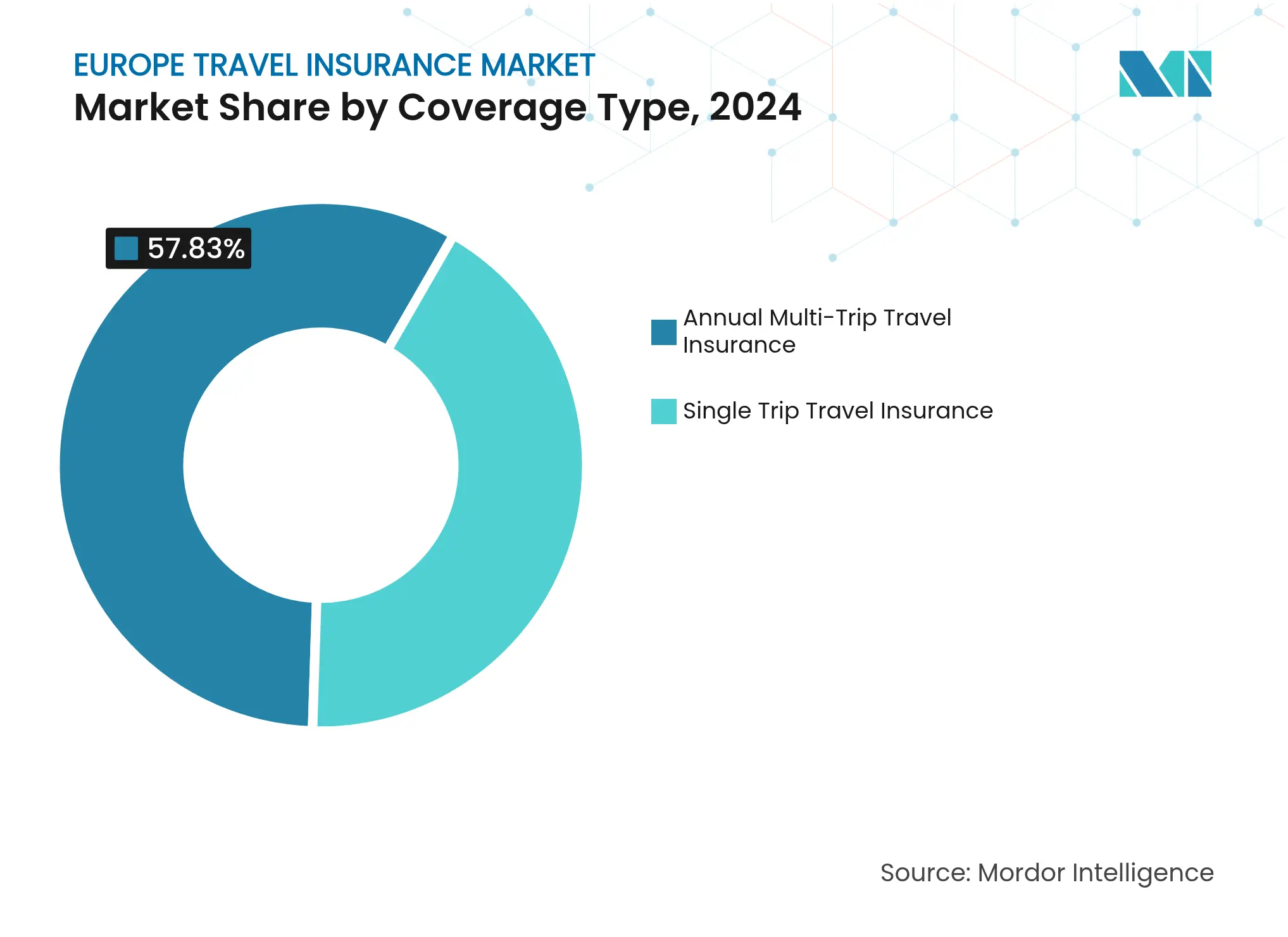

By Coverage Type: Annual Plans Drive Premium Growth

The annual-plan segment accounted for 57.83% of Europe travel insurance market share in 2024, benefiting from frequent-flier business professionals and affluent families who require multiple-trip protection. This dominance translates into a larger absolute contribution to Europe travel insurance market size, given premiums that routinely exceed USD 200 per adult policy. Embedded payment-card benefits, and loyalty-program cross-promotions reinforce repeat purchase behavior. Allianz’s Allyz subscription offers one-click renewal, real-time safety alerts, and in-app document storage, deepening retention.

Single-trip products grow faster, posting a 7.12% CAGR through 2030 as cost-sensitive leisure travelers and students return to continental sightseeing. Embedded checkout add-ons on platforms such as Omio or low-cost carriers deliver convenient, event-based cover, often priced below USD 15. Parametric features that pay if snowfall cancels ski holidays or if luggage delays exceed four hours enhance perceived value. With rising climate volatility, carriers are adding modular extensions for severe-weather protection, which could raise average policy revenue within the single-trip category.

Note: Segment shares of all individual segments available upon report purchase

By End User: Families Retain Lead While Education Surges

Family travelers represented 39.75% of 2024 premium volume, a sizable slice of Europe travel insurance market size, owing to multigenerational vacations and villa rentals that elevate per-trip values. Policies bundling children at no additional charge and offering 24-hour pediatric teleconsultations resonate strongly. Loyalty programs that integrate with holiday-park chains or cruise lines spur cross-selling and repeat purchases.

Education travelers record the fastest 7.92% CAGR through 2030, propelled by Erasmus-style exchanges and gap-year backpacking. These customers demand academic interruption, laptop theft, and extended-stay medical benefits absent from standard leisure products. Leading carriers deploy multilingual customer support and campus liaison partnerships to expedite claims. Although premiums per head remain lower than in senior or business segments, rising student mobility makes the cohort strategically significant.

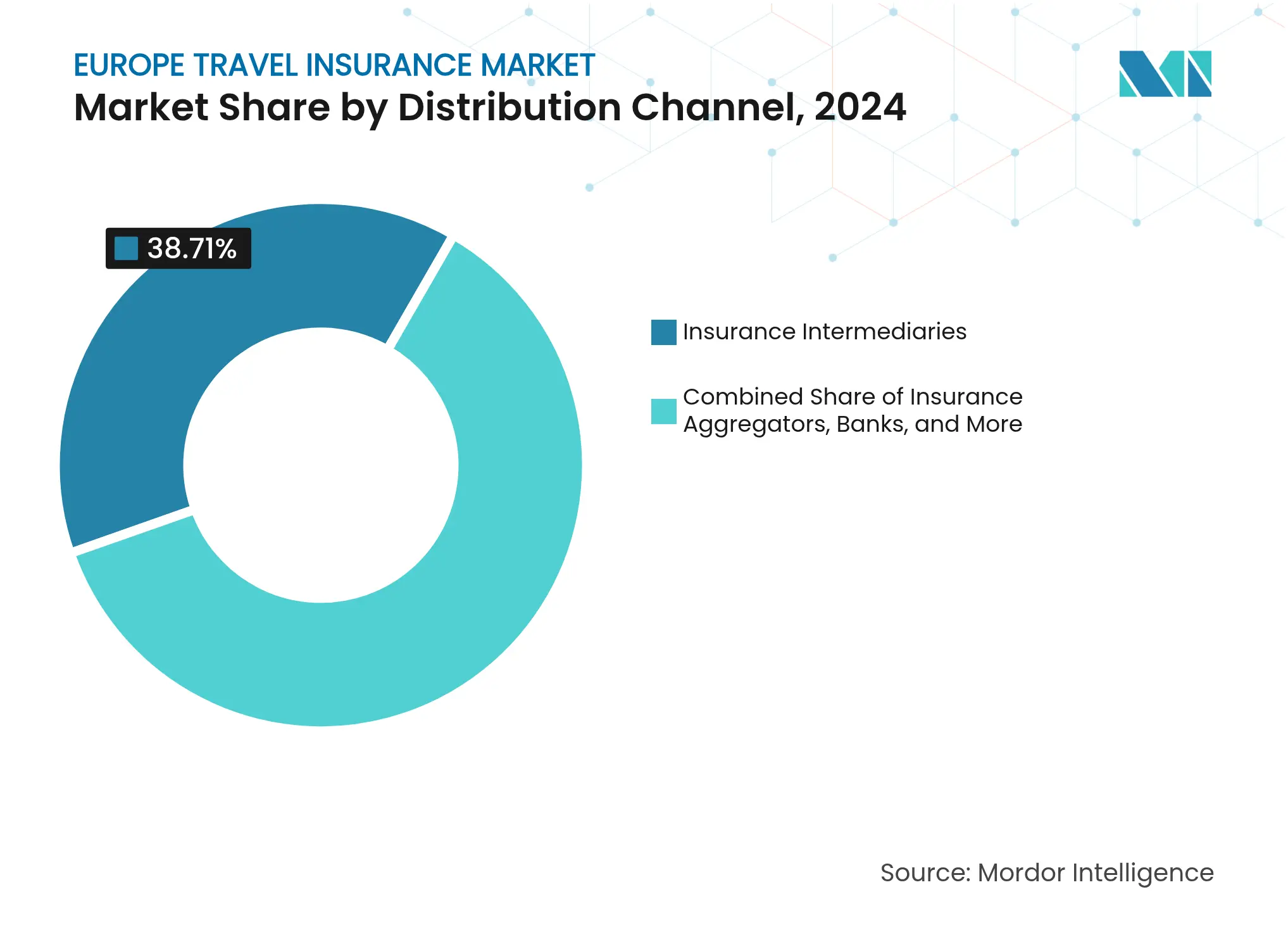

By Distribution Channel: Aggregators Accelerate

Intermediaries like tour operators, corporate travel managers, and retail agents still command 38.71% of gross written premiums, reflecting decades of relationship-based selling in the Europe travel insurance market. These sales often involve complex itineraries requiring nuanced underwriting. However, insurance aggregators, posting an 8.34% CAGR, are reshaping buyer expectations for transparency and speed. Comparison portals rank policies on price and star ratings, pressuring carriers to simplify terms and accelerate issuance. Some insurers counter by building white-label APIs that feed real-time quotes into multiple aggregators simultaneously, preserving volume while limiting brand dilution.

Banks and direct insurer websites maintain a steady share as they cross-sell to clients already holding credit cards or home insurance. Yet the embedded channel is blurring lines: neobanks integrate one-click travel cover into mobile apps, while airlines pre-select insurance during ticket checkout, minimizing friction. The strategic pivot toward API ecosystems is set to redefine customer ownership economics over the forecast horizon.

Note: Segment shares of all individual segments available upon report purchase

The United Kingdom contributed 18.63% of Europe travel insurance market premiums in 2024, a reflection of high outbound-travel propensity and compulsory medical cover for post-Brexit visits to EU states. Comparison-site culture makes UK buyers highly price aware, prompting insurers to introduce add-on tiers that balance affordability with pandemic cancellation and extreme-weather benefits. Aviva’s July 2025 acquisition of Direct Line Group expanded its policyholder base to roughly 20 million and created cross-sell headroom for travel products across motor and home portfolios.

Germany and France follow in absolute size, benefiting from dense distributor networks and world-famous outbound leisure markets. ERGO’s tie-up with O2 Telefónica exemplifies how German insurers leverage telecom footprints for embedded expansion, while Allianz’s Allyz super-app drives French uptake by bundling travel alerts and concierge services.

Italy posts the region’s fastest growth, an 8.12% CAGR through 2030, buoyed by booming inbound tourism and rising domestic weekend trips. Policy comparisons are rapidly moving online, aided by aggregator penetration in Milan, Rome, and Naples. Spain showcases regulatory-driven demand: its July 2025 mandate for British visitors to carry private travel insurance has already lifted single-trip policy volume, proving how local rules influence the Europe travel insurance market. BENELUX nations display sophisticated annual-plan uptake due to frequent cross-border commutes, whereas Nordic countries emphasize high medical limits and evacuation cover, echoing their higher healthcare costs. Central and Eastern European markets remain underpenetrated yet attractive because rising disposable incomes and low base coverage rates create ample headroom for growth.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

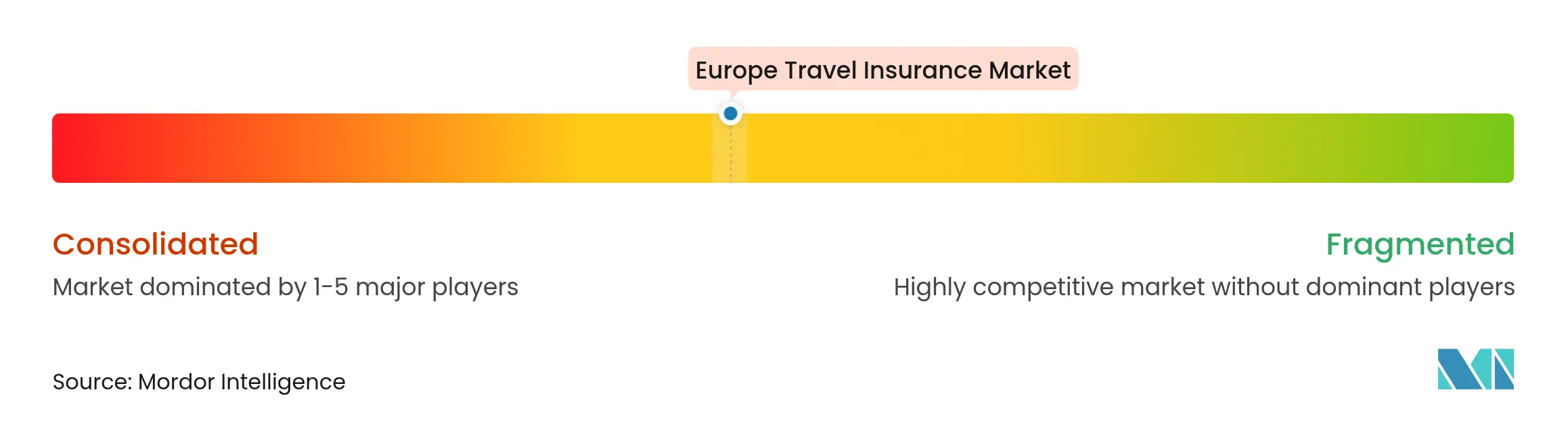

Market Concentration

Europe’s travel insurance arena is moderately fragmented. Allianz Partners leads on both scale and technology, recording USD 3,434.02 billion (EUR 3.297 billion) in travel insurance revenue for 2023 and leveraging its Allyz platform to integrate claims, medical assistance, and trip-monitoring into a single interface. The firm’s AI-driven triage routes 70% of medical cases to digital self-care or telehealth, containing cost escalation.

Zurich Insurance Group’s 2024 agreement to acquire AIG’s personal travel portfolio underscores aggressive inorganic expansion. The deal broadens Zurich’s distributor network across 50 jurisdictions and grants immediate access to thousands of corporate accounts, positioning the carrier to lift its Europe travel insurance market share above the mid-single-digit range. Integration plans call for unified underwriting engines and shared assistance centers to extract cost collaborations.

Insurtechs target white-space opportunities. Companion underwrites parametric cancel-for-any-reason policies in 32 states of the European Economic Area, paying claims within seconds via API. Nexible, ERGO’s digital subsidiary, markets a modular annual cover that lets users bolt on gadget or rental-car extensions, mirroring consumer demand for personalization. Chubb experiments with automatic roaming-activated policies launched in Bulgaria, embedding premiums into daily mobile charges and signaling a gradual shift toward usage-based pricing. Established players are responding with venture investments and sandbox pilots to preserve relevance as distribution digitizes.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts

6. Competitive Landscape

7. Market Opportunities and Future Outlook

The report focuses on the complete background of the European Travel Insurance Market, which comprises an assessment of the developing market trends by segments, important changes in the market dynamics, and a market overview.

Europe Travel Insurance Market is Segmented By Insurance Coverage (Single-Trip Travel Insurance, Annual Multi-trip Travel Insurance, and Others), By Distribution channels (Insurance Companies, Insurance Intermediaries, Banks, Insurance Brokers, and Other Distribution Channels), By End-User (Senior Citizens, Education Travelers, Family Travelers, and Others End Users) and by Country (Germany, United Kingdom, France, Italy, Spain, and Rest of Europe). The report offers Market size and forecasts for Europe Travel Insurance Market in value (USD) for all the above segments.

Wealth Management Intelligence for the Middle East

4 Min Read

Driving Growth in the Embedded Insurance Market

4 Min Read

Unlocking Saudi Arabia’s Regional Tourism Growth Potential

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.