Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 57.28 Billion |

| Market Size (2026) | USD 58.86 Billion |

| Market Size (2031) | USD 67.43 Billion |

| Growth Rate (2026 - 2031) | 2.75% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Motor Insurance Market Analysis by Mordor Intelligence

The Germany motor insurance market size was valued at USD 57.28 billion in 2025 and estimated to grow from USD 58.86 billion in 2026 to reach USD 67.43 billion by 2031, at a CAGR of 2.75% during the forecast period (2026-2031). Mandatory third-party liability coverage entrenched in national legislation keeps penetration near 100%, limiting volume volatility while repair-cost inflation, electric-vehicle (EV) adoption, and telematics-based underwriting lift average premium per policy. Structural trends—ranging from tight workshop labor markets and OEM parts pricing power to digital aggregator price transparency—are accelerating product innovation and compelling incumbents to refine cost-containment capabilities. Data-driven underwriting, customer-centric mobile journeys, and embedded insurance partnerships with carmakers are now central to revenue strategy across the German motor insurance market. Competitive differentiation pivots on seamless claims servicing, ecosystem alliances, and real-time behavioral risk scoring rather than legacy branch reach alone.

Key Report Takeaways

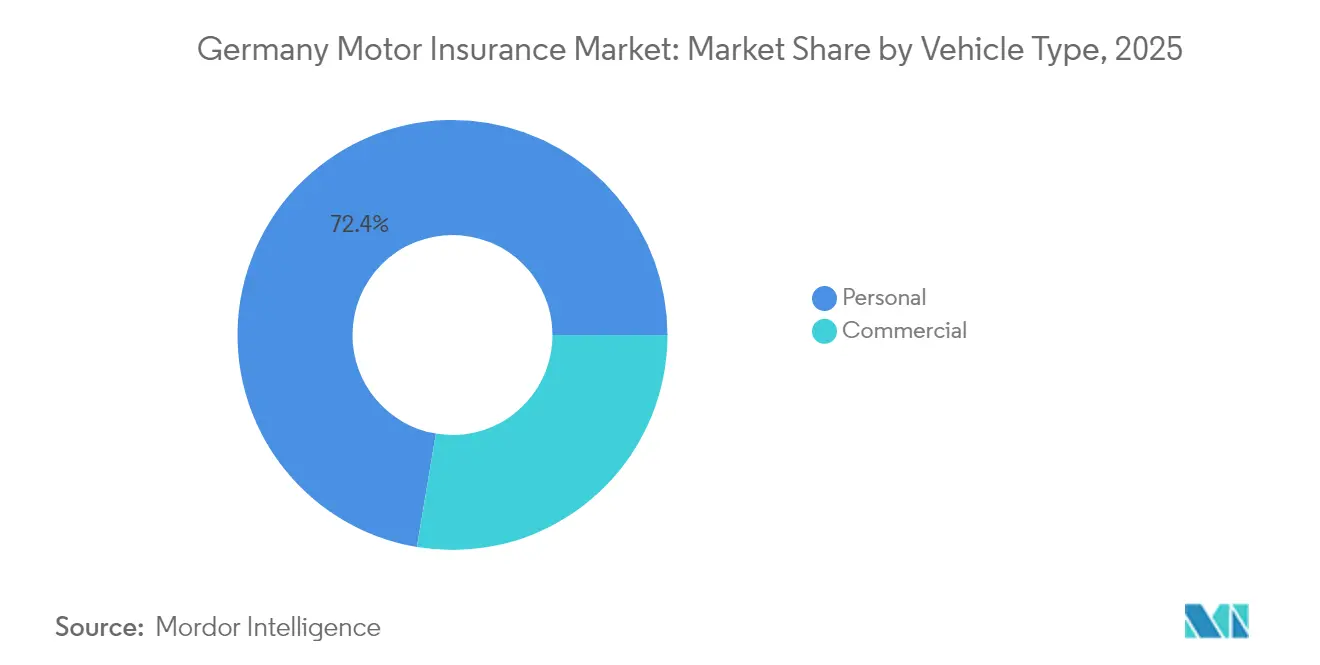

- By vehicle type, commercial vehicles retained 27.65% of Germany's motor insurance market share in 2025, while expanding at the fastest 3.39% CAGR through 2031.

- By insurance type, comprehensive policies represented 32.90% of Germany's motor insurance market size in 2025 and are accelerating at a 3.76% CAGR to 2031.

- By distribution channel, direct digital sales booked a 3.98% CAGR between 2026 and 2031, as agents still controlled a 41.65% premium share in 2025 but ceded momentum to mobile-first alternatives.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Motor Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-linked repair-cost catch-up pricing boom | +1.2% | National, most acute in dense urban corridors | Short term (≤ 2 years) |

| EV-specific loss-frequency gap vs ICE | +0.4% | Nationwide, led by Bavaria and Baden-Württemberg EV clusters | Medium term (2-4 years) |

| Telematics-driven pricing sophistication | +0.3% | Country-wide, particularly commercial fleets | Medium term (2-4 years) |

| Aggregator-fuelled customer churn cycle | +0.2% | Country-wide, skewed to price-sensitive demographics | Short term (≤ 2 years) |

| OEM subscription partnerships | +0.3% | Premium-vehicle segments, leasing portfolios | Long term (≥ 4 years) |

| Usage-based micro-policies for last-mile fleets | +0.1% | Urban logistics hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inflation-Linked Repair-Cost Catch-Up Pricing Boom

Workshop hourly rates averaged EUR 188 (USD 204) in 2024, an 8.6% surge that eclipsed headline inflation and triggered immediate tariff adjustments. Rising wage expectations for certified technicians, complex ADAS calibration labor, and intermittent parts shortages have driven average repair invoices from EUR 2,700 in 2017 to EUR 4,000 in 2023. German insurers booked over EUR 3 billion underwriting losses in 2023, prompting a 20% premium uplift in 2024 and another 8-11% slated for 2025. Because these increases merely recapture margin erosion rather than add new profit pools, carriers now deploy granular claims-data analytics and negotiated-rate preferred-supplier networks to contain future shocks. The pricing boom, therefore, supplies near-term revenue lift for the German motor insurance market while spotlighting the urgency of structural claims-expense reform.

EV-Specific Loss-Frequency Gap vs ICE

Insurance Europe reported that EVs register 5-10% lower third-party liability claim frequency yet incur 30-35% higher average repair costs, a duality rooted in sophisticated safety tech that prevents crashes but requires specialized fixes when incidents occur[1]Insurance Europe, “Electric Vehicle Insurance Risk Analysis,” insuranceeurope.eu. German carriers have responded by creating EV-specific rating factors that account for kilowatt-hour battery size, thermal-runaway risk, and certified repair-shop scarcity. Early adopting regions such as Bavaria and Baden-Württemberg already concentrate warranty-extension add-ons covering battery degradation and high-voltage system diagnostics. While frequency benefits temper aggregate exposure, severity inflation compresses combined ratios unless premiums keep pace. Consequently, insurers with accurate EV segmentation models secure profitable footholds as the German motor insurance market electrifies.

Telematics-Driven Pricing Sophistication

HUK-Coburg’s Telematik Plus offers up to 30% discounts for safe driving, relying on smartphone sensors to evaluate acceleration, braking, cornering, and nighttime mileage. This behavior-based approach lowers adverse-selection risk and nurtures a feedback loop that encourages defensive driving through gamified scorecards. Commercial fleets integrate dash-cam video and engine-control-unit data into risk dashboards, tying corporate safety KPIs directly to insurance costs. BaFin permits such dynamic rating, provided data privacy and anti-discrimination standards are met, giving carriers room to expand pay-how-you-drive propositions. Telematics, therefore, strengthens customer stickiness and enhances actuarial precision, underpinning margin improvement across the Germany motor insurance market.

Aggregator-Fueled Customer Churn Cycle

Comparison portals Check24 and Verivox enable consumers to retrieve dozens of quotes within minutes, pushing annual switching rates beyond 30% in the most price-elastic segments. The resulting commoditization pressures insurers to refine lifetime-value analytics, launch loyalty points, and bundle roadside assistance to deter defection. High churn elevates acquisition costs, but it also disciplines underwriters to eliminate cross-subsidies and rationalize pricing as aggregator algorithms incorporate telematics and coverage-feature filters; carriers that excel in risk-based tariffing and transparent communication climb search rankings. The Germany motor insurance market thereby evolves toward a more contestable equilibrium where price remains pivotal yet service experience can still differentiate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising spare-parts monopolistic pricing power | -0.8% | National, acute in luxury brands | Medium term (2-4 years) |

| Claims-inflation profit squeeze | -0.6% | Nationwide, comprehensive segment | Short term (≤ 2 years) |

| ADAS repair complexity outpacing technical skills | -0.3% | Country-wide, rural workshops | Medium term (2-4 years) |

| Climate-driven hail-event clustering risk | -0.2% | Bavaria, Hesse, central storm belts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Spare-Parts Monopolistic Pricing Power

Original-equipment makers continue to enforce design patents that restrict aftermarket access to bumpers, hoods, fenders, and headlamps, allowing them to maintain double-digit mark-ups on many high-volume parts. These mark-ups translate directly into higher loss severity because body-shop invoices must reflect both the expensive component and the labor time needed to fit it. The 2024 EU repair-clause legislation seeks to foster competition by legalizing replica visible parts and could unlock up to EUR 720 million in consumer savings once fully implemented[2]European Commission, “EU Repair Clause Implementation,” ec.europa.eu. Insurers, however, must first vet new suppliers, set up certification protocols, and negotiate quality guarantees, which introduces near-term administrative overhead. Luxury marques retain broader intellectual-property protections, meaning policyholders with premium vehicles will see limited price relief even after the rule change. Until a robust aftermarket emerges, high parts costs will continue to widen combined ratios and force carriers to push through tariff increases to protect solvency margins.

Claims-Inflation Profit Squeeze

Total claim outlays have been rising faster than earned premium for three consecutive years, driving most German motor insurers to combined ratios above 100% in 2023. Workshop labor inflation, elevated rental-car prices, and longer repair-cycle times linked to supply bottlenecks all compound the problem. Although insurers imposed an average 20% tariff increase in 2024, the lag between pricing and loss emergence means many carriers will not feel the full benefit until late 2025. Reinsurers have responded by lifting attachment points, shifting more attritional volatility back onto primary balance sheets, and intensifying capital pressure. Companies are beefing up loss-adjustment reserves, automating low-complexity claims, and renegotiating supplier contracts, yet return on equity remains well below the pre-pandemic norm. Persistent cost creep therefore threatens to undermine strategic-investment budgets even as topline revenue continues to grow.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Personal Segment Dominance

Personal cars remain the backbone of Germany’s motor-insurance portfolio, capturing 72.35% of premiums in 2025 because nearly every one of the country’s 48 million passenger vehicles must, by law, carry at least third-party liability cover. Most owners also upgrade to comprehensive policies that reimburse glass breakage, hail dents, vandalism, and theft—risks that resonate in densely parked urban streets and along storm-prone southern corridors. Persistently high ownership rates, stable household incomes, and inexpensive credit keep policy volumes large, yet structural headwinds are emerging. Younger city dwellers lean toward subscription mobility and car-sharing fleets that eliminate the need for an individual policy, while local governments expand low-emission zones and public-transport incentives that further depress private-car mileage. Insurers, therefore, see slower top-line growth in personal lines and are testing usage-based add-ons, instant deductible adjustments, and in-app reward programs to keep digitally minded drivers engaged.

Commercial motor, by contrast, is the growth engine, projected to advance at a 3.39% CAGR through 2031 as parcel-service vans, ride-hail fleets, and electrified last-mile cargo bikes multiply across Germany’s logistics hubs. E-commerce giants, supermarket chains, and pharmaceutical distributors now operate data-rich telematics dashboards that log every acceleration spike and charging session, feeding insurers a continuous risk signal they can price in near real time. Fleet managers tap these insights to reroute around congestion, schedule predictive maintenance, and coach drivers toward safer habits, collectively shrinking accident frequency and lowering loss ratios. Battery warranties, depot-charging liability, and cross-border Green Card extensions have become standard riders, while specialized wording now covers autonomous-driving pilots on closed industrial campuses. Together, these product tweaks show how commercial lines are evolving from a simple indemnity purchase into a broader risk-management partnership between carriers and corporate mobility operators.

By Insurance Type: Comprehensive Coverage Momentum

Third-party liability accounted for 67.10% Germany's motor insurance market share in 2025 due to a statutory mandate, yet comprehensive policies are tracking the steeper 3.76% CAGR through 2031. Elevated vehicle MSRP and intricate sensor arrays magnify repair bills for minor fender-benders, nudging owners to upgrade protection. Hail-related losses, particularly the EUR 2.0 billion event in 2023, highlight weather-peril exposure that only comprehensive policies address [GDV.DE]. Moreover, leasing contracts increasingly stipulate fully comprehensive cover, tightening penetration in higher-value car cohorts.

Insurers enhance comprehensive offerings with variable deductibles, new-car value protection, and storm-shelter parking-advisory alerts delivered via mobile push notifications. Integration of glass-repair reservations and instant photo-estimate tools shortens claims cycles and improves customer satisfaction. As ADAS adoption lowers collision frequency, carriers weigh premium rebates tied to verified lane-keeping-assist engagement. These product tweaks maintain relevance and reinforce retention within the Germany motor insurance market.

By Distribution Channel: Digital Channel Expansion

Agents retained 41.65% premium share in 2025, reflecting consumer reliance on personalized advice for coverage nuances and claims handholding. Nonetheless, direct digital channels chart the swiftest 3.98% CAGR to 2031, propelled by smartphone-native quote journeys, instant document upload, and open-banking payment links. Acquisition cost in direct can fall below 5% of premium versus 12-15% via agencies, furnishing pricing headroom.

Insurtech newcomers like Friday and Neodigital guarantee policy issuance under 90 seconds and month-to-month cancellation rights, resonating with digital-native cohorts. Banks leverage auto-loan touchpoints to cross-sell motor policies, while brokers specialize in vintage-auto and expat segments. Hybrid incumbents integrate video consultations, click-to-policy frameworks, and branch-based advisory to preserve omnichannel continuity. Such a model blending caters to heterogeneous buying preferences and supports steady conversion within the German motor insurance market.

Geography Analysis

Bavaria and Baden-Württemberg together contributed 34.80% of the national premium in 2025, buoyed by high disposable income, luxury-car density, and a concentration of automotive manufacturing. Munich recorded claims 15% above the national mean due to congestion, premium vehicle mix, and elevated labor rates. Hamburg’s maritime climate fosters corrosion-related claims on commercial fleets, while Lower Saxony’s rural corridors register higher wildlife-collision incidents.

Eastern Länder such as Saxony and Thuringia feature older vehicle fleets with lower average sums insured, translating into higher price sensitivity and a preference for entry-level liability cover. Yet these regions show above-average uptake of aggregator channels, signaling latent digital-conversion potential. Hail-exposed districts in Bavaria and Hesse experienced EUR 2.0 billion comprehensive losses in 2023, driving localized tariff surges and retentions. Catastrophe models now layer micro-cell thunderstorm analytics, enabling postcode-level pricing that aligns risk with premium in the Germany motor insurance market.

Urban centers face emerging mobility paradigms where car-sharing, e-scooters, and integrated public-transport passes diminish private-car reliance among sub-35 demographics. Conversely, logistics-hub cities like Leipzig and Frankfurt benefit from warehouse expansion and e-commerce parcel flows that swell light commercial-vehicle counts. Regional universities in North-Rhine-Westphalia incubate telematics and autonomous-vehicle startups, fostering knowledge spillovers into insurer innovation labs. The geographic mosaic thus creates uneven growth pathways that sophisticated underwriters exploit for portfolio diversification inside the Germany motor insurance market.

Competitive Landscape

The German motor insurance market exhibits moderate concentration yet an intense innovation race, with legacy giants and digital entrants vying for customer mindshare across pricing, service, and ecosystem integration. HUK-Coburg leads on policy count, insuring over 14 million vehicles through a mutual structure that channels surplus into tariff rebates and loyalty bonuses[3]HUK-Coburg, “Company Facts and Figures,” huk.de. Its direct sales arm grows double digits annually by leveraging brand equity, while Telematik Plus cements a reputation for fair-use discounts that resonate with younger drivers. Allianz positions itself as a broad-based financial-services orchestrator, bundling motor with home, legal-expenses, and travel covers inside a single dashboard; its Insurance Copilot generative-AI platform slashes claim-file handling time by 30%, freeing adjusters for complex cases. AXA Germany focuses on modular contracts that let customers add glass-breakage, battery-damage, or private-car-sharing endorsements in a few clicks, emphasizing flexibility as a retention lever.

Digital-only challengers such as Friday, Neo digital, and Getsafe rely on headless architectures and API-first product catalogs that integrate seamlessly into dealership portals, neobank apps, or mobility-as-a-service platforms. Their value proposition centers on transparent pricing, monthly cancellation, and instant claims payments via SEPA transfers. While policy volumes remain modest compared with incumbents, their superior customer-satisfaction scores force established insurers to recalibrate service benchmarks. OEM-aligned insurers like Volkswagen Financial Services and BMW Insurance leverage embedded telematics feeds to monitor driving patterns, battery health, and over-the-air software updates. Such real-time data enhances risk scoring and enables proactive maintenance nudges that curtail breakdown-related claims. Reinsurers, led by Munich Re and Hannover Re, support primaries with structured quota shares covering hail volatility and large-loss clusters; they also incubate insurtech subsidiaries that commercialize AI underwriting engines. Consulting alliances with cloud hyperscalers deliver scalable policy-admin platforms, further democratizing digital capabilities.

Brokerage conglomerates Marsh and Aon focus on corporate fleets and captive leasing entities, offering self-insured retention layers and loss-prevention analytics. Niche players like OCC target classic-car aficionados with agreed-value policies and event-road-risk extensions, safeguarding margins through specialty underwriting expertise. Overall, strategic advantage in the German motor insurance market now rests less on asset scale and more on data fluency, frictionless claims journeys, and multi-channel customer intimacy.

Germany Motor Insurance Industry Leaders

Allianz

HUK-Coburg

AXA Germany

R+V Versicherung

DEVK

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Allianz, BlackRock, and T&D Holdings completed the acquisition of German life insurer Viridium from Cinven in a EUR 3.5 billion transaction. Although a life-focused deal, the partnership amplifies Allianz’s capital flexibility that could be redirected toward motor-line technology upgrades.

- February 2025: Allianz implemented the Insurance Copilot generative AI solution for claims management, initially deployed for automotive claims processing with expansion plans across operating entities. Early results show faster triage and improved customer satisfaction, reinforcing insurer commitment to AI-driven efficiency.

- January 2025: HUK-COBURG announced sustainability initiatives as part of its strategic positioning in the German motor insurance market. The program prioritizes carbon-neutral claims logistics and eco-screened supplier networks, signaling rising ESG expectations in underwriting portfolios.

- October 2024: The European Union adopted repair clause legislation, breaking OEM monopolies on visible spare parts, with implementation affecting German motor insurance repair-cost dynamics. Market participants anticipate gradual claims-severity relief once the certified aftermarket supply stabilizes.

Germany Motor Insurance Market Report Scope

Car insurance safeguards individuals financially in case of a car accident or related incidents. It commonly includes coverage for vehicle repair or replacement costs and medical expenses resulting from accidents. The German car insurance market is in size forecast and is segmented by insurance type and distribution channel. The market is segmented by insurance type into accident, third-party liability, and comprehensive. In distribution channels, the market is segmented into agents, brokers, online, banks, and other distribution channels. The reports offer the market sizing and forecasts for the German car insurance market in value (USD) for all the above segments.

By Vehicle Type (Value)

| Personal |

| Commercial |

By Insurance Type (Value)

| Third-Party |

| Comprehensive |

By Distribution Channel (Value)

| Direct |

| Agents |

| Brokers |

| Banks |

| Other Distribution Channels |

| By Vehicle Type (Value) | Personal |

| Commercial | |

| By Insurance Type (Value) | Third-Party |

| Comprehensive | |

| By Distribution Channel (Value) | Direct |

| Agents | |

| Brokers | |

| Banks | |

| Other Distribution Channels |

Key Questions Answered in the Report

How large is the Germany motor insurance market in premium terms for 2026?

Total written premiums reached USD 58.86 billion in 2026 and are forecast to hit USD 67.43 billion by 2031.

What growth rate is expected for the sector through 2031?

The market is projected to expand at a 2.75% CAGR, reflecting steady premium increases amid structural cost pressures.

Which vehicle segment is expanding fastest?

Commercial vehicle cover shows the highest 3.39% CAGR as e-commerce and logistics fleets proliferate.

Why are comprehensive policies gaining momentum?

Hail-storm losses, higher vehicle values, and intricate sensor arrays raise potential repair bills, encouraging drivers to opt for broader cover.

How are digital aggregators reshaping competition?

Platforms like Check24 heighten price transparency and elevate switching rates, compelling insurers to refine retention tactics and dynamic pricing.

What role do OEM subscription programs play?

Automakers embed full insurance in bundled leasing fees, securing multi-year retention for insurers and leveraging vehicle-data streams for smarter underwriting.

Page last updated on: