Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.16 Billion |

| Market Size (2026) | USD 1.28 Billion |

| Market Size (2031) | USD 2.08 Billion |

| Growth Rate (2026 - 2031) | 10.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Pet Insurance Market Analysis by Mordor Intelligence

The Germany Pet Insurance Market size in terms of premium value is expected to grow from USD 1.16 billion in 2025 to USD 1.28 billion in 2026 and is forecast to reach USD 2.08 billion by 2031 at 10.20% CAGR over 2026-2031.

The growth reflects a decisive shift in consumer attitudes as German households increasingly treat pets as family members, prompting wider adoption of financial protection for veterinary care. Product innovation, regional economic disparities, and the rapid rise of digital distribution each deepen demand, while the low penetration rate of roughly 20% highlights sizable headroom for expansion. Higher disposable incomes in Bavaria and Baden-Württemberg anchor spending on comprehensive policies, whereas accelerating uptake in East Germany signals that price-conscious regions are also closing the protection gap. Policy design is evolving toward customizable packages that bundle illness, accident, and preventive coverage, supported by IoT wearables, AI-driven underwriting, and flexible caps that mirror human healthcare standards. Competitive intensity is increasing as traditional insurers leverage brand trust while insurtech entrants compete on speed, transparency, and lower cost of service delivery.

Key Report Takeaways

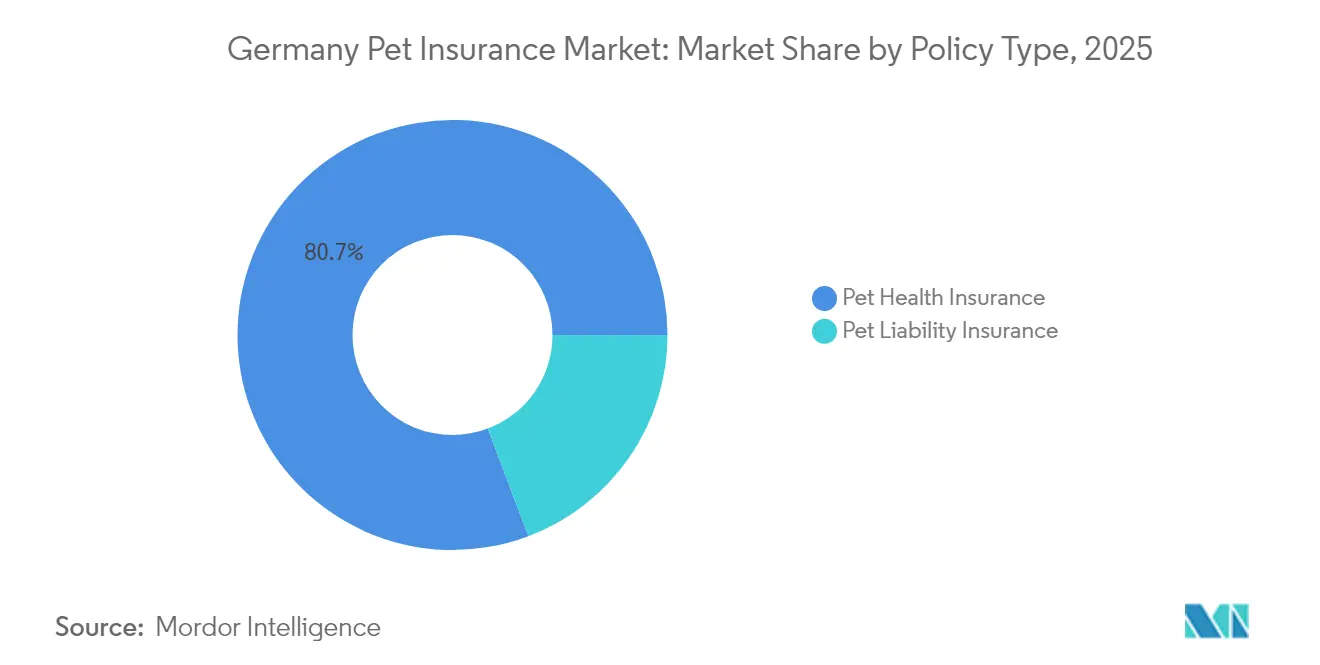

- By policy type, pet health insurance held 80.74% of the Germany pet insurance market share in 2025, while pet liability insurance recorded the highest CAGR at 11.55% through 2031.

- By animal type, dogs led with 63.92% revenue share in 2025; cat coverage is advancing at a 13.19% CAGR to 2031.

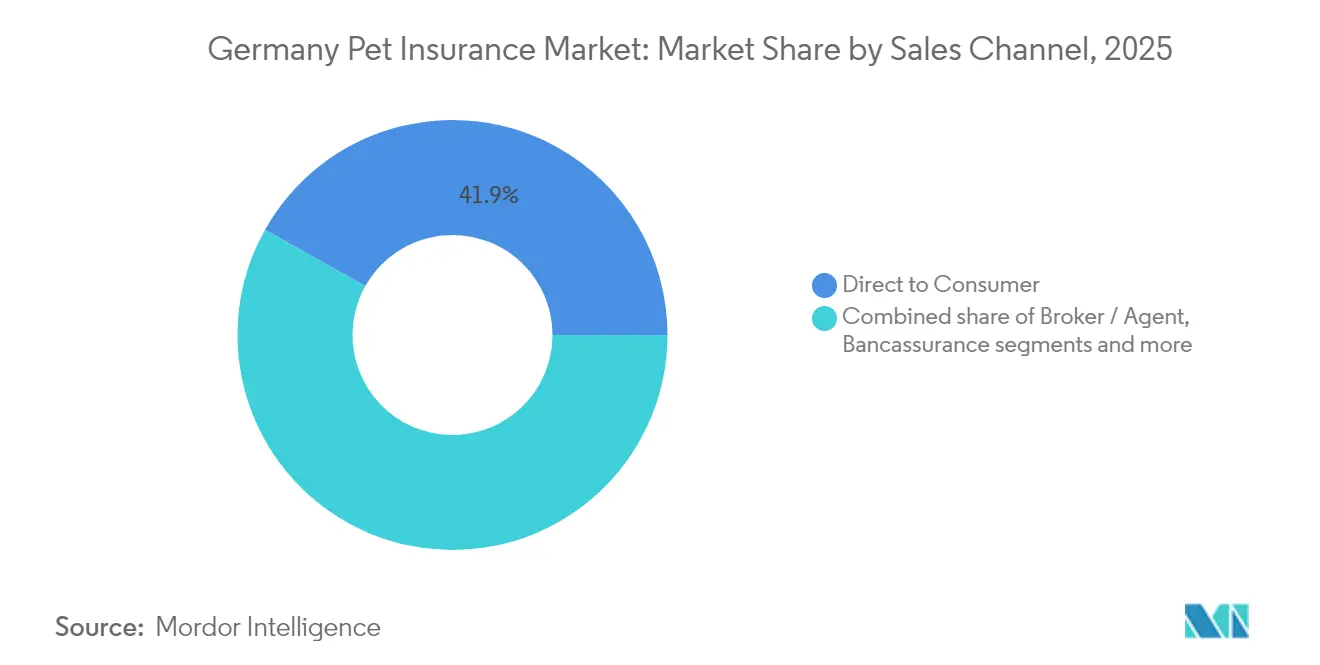

- By sales channel, direct-to-consumer accounted for 41.86% of the Germany pet insurance market size in 2025, yet online aggregators and insurtech platforms are expanding at 14.5% CAGR.

- By coverage level, standard plans (≤ €5,000 cap) captured 44.82% of the Germany pet insurance market size in 2025, while comprehensive plans posted the fastest 12.29% CAGR.

- By region, South Germany commanded a 29.85% revenue share in 2025; East Germany shows the quickest 11.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Pet Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pet humanisation and willingness to spend | +2.8% | National, stronger in South and West Germany | Long term (≥ 4 years) |

| Higher post-COVID pet adoption | +1.9% | Urban hubs: Berlin, Munich, Hamburg | Medium term (2-4 years) |

| Rising veterinary costs | +2.1% | National, strongest in metropolitan areas | Short term (≤ 2 years) |

| Flexible, customisable policy design | +1.6% | Tech-savvy regions nationwide | Medium term (2-4 years) |

| Integration of IoT pet-wearables enabling risk-based pricing | +0.8% | Urban centers, tech-forward demographics | Long term (≥ 4 years) |

| State-level debate on mandatory pet health cover | +1.2% | Regional, varying by state legislation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Humanization & Willingness to Spend on Health

Nearly 73% of German owners identify pet parenting as central to their lifestyle, and spending priorities now emphasize welfare over cost[1]Zentralverband Zoologischer Fachbetriebe, “Der Heimtiermarkt in Zahlen,” zzf.de. The result is a sustained preference for broad medical cover, preventive services, and even alternative therapies that mirror human care models. Emotional attachment reduces price sensitivity, encouraging insurers to launch premium tiers with unlimited caps, dental benefits, and travel extensions. In response, carriers have started loyalty programs that refund unused wellness budgets, reinforcing a perception of tangible value. Expanded public discussion around animal rights further normalizes the idea that quality veterinary care is a moral obligation, solidifying long-run demand in the Germany pet insurance market.

Increasing Pet Adoption Post-COVID

Remote work extended daily time spent at home, prompting many urban professionals to acquire pets for companionship. Household pet ownership reached 45% in 2024, totalling 34.3 million animals. New owners, unfamiliar with veterinary bills, view insurance as a straightforward budgeting instrument and respond well to educational content on accident-cost scenarios. Insurers now lead onboarding campaigns at breeder sites, shelters, and e-commerce checkout pages, converting first-time owners at the decision point. As flexible work patterns persist, continued inflow of puppies and kittens supports a longer-term policy pipeline, while social-media storytelling from satisfied claimants amplifies peer-to-peer influence.

Rising Veterinary Costs Due to Advanced Treatments

A 25% uplift in the German Fee Schedule for Veterinarians (GOT) since 2022 has raised the price of routine procedures and magnified the risk of catastrophic out-of-pocket bills[2]VIN News Service, “Germany Revamps Veterinary Fee Schedule,” vin.com. Emergency surgery can exceed USD 10,800, dwarfing several years of average premiums and underscoring insurance value. Urban clinics deploy CT scanners and laser therapy to differentiate services, intensifying cost inflation. Owners of pedigree dogs and aging cats are disproportionately exposed, pushing average claim severity higher each year. Faced with mounting invoices, many clinics now promote insurance at the point of payment, effectively becoming unpaid distribution allies for insurers.

Expansion of Flexible, Customisable Policy Products

Tiered packages such as bronze, silver, and gold allow owners to align caps, deductibles, and wellness budgets with pet age, breed risk, and financial tolerance[3]Lassie, “Product Overview,” lassie.co. Real-time policy editing via mobile apps lets users upgrade caps ahead of planned procedures or add dental riders without a full policy reboot. Personalization also enables age-adjusted rates and partial cover for pre-existing conditions, closing access gaps for older pets. Data from wearables feeds dynamic pricing that rewards healthy behavior, deepening customer engagement. Rising consumer expectation for Netflix-style subscription control means policies that cannot be altered instantly risk falling behind in the Germany pet insurance market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High premium cost versus perceived need | -1.4% | Entire market, stronger in East Germany | Short term (≤ 2 years) |

| Limited cover for senior pets | -0.9% | Nationwide, affects ageing pet population | Medium term (2-4 years) |

| Fragmented data standards | -0.6% | National | Medium term (2-4 years) |

| Growth of vet direct-payment wellness plans | -0.8% | Urban clinics with strong client bases | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Premium Cost vs Perceived Need

Monthly charges ranging from USD 14.5 to USD 94.7 remain a hurdle for price-sensitive households, especially those that have never faced large veterinary bills. East German consumers retain cautious spending habits, slowing uptake despite improving purchasing power. Entry-level plans, installment billing, and clearer claim-probability calculators are helping narrow the perception gap, but many owners still weigh premiums against routine vaccination costs instead of worst-case scenarios. Rising inflation in household energy and food costs competes for disposable income, compounding reluctance. Insurers experimenting with micro-deductibles and mileage-style caps aim to offer just enough protection at a lower monthly price point.

Limited Cover for Senior Pets & Pre-Existing Conditions

As pets age, most providers halt new enrolments after 6–8 years, often excluding pre-existing ailments. This practice leaves older and chronically ill pets without coverage, even as their veterinary needs grow significantly. The lack of coverage during this critical period creates a gap in the market, as pet owners face rising medical expenses for their aging companions. Senior citizen affinity groups are now advocating for more lenient underwriting, especially for long-lived pets like indoor cats, to address this underserved segment. In response, some insurance carriers are testing "legacy plans." These plans feature reimbursement levels that increase as the pet ages, aiming to strike a balance between risk and affordability. These plans are designed to provide meaningful support for pet owners while managing the financial risks for insurers. However, broader acceptance hinges on actuarial evidence proving that this staged pricing model can sustain itself while offering substantial benefits to both parties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Policy Type: Health Insurance Dominates Liability Growth

Pet health insurance generated 80.74% of 2025 premiums, underscoring how direct exposure to medical bills outweighs liability concerns for most owners. The Germany pet insurance market size for liability coverage is smaller but expands at 11.55% CAGR as more states mandate third-party protection for dogs. Liability premiums, starting at USD 3.49 monthly, serve as an entry product that familiarises price-sensitive owners with insurance. Cross-sell strategies convert liability clients into combined medical packages, elevating average revenue per policy and improving retention. Carriers are also exploring bundled discounts that attach liability cover automatically to mid and top-tier health plans, reducing friction for owners and simplifying compliance updates as regulations evolve.

Legislation mandating coverage is consistently driving up volumes, positioning liability as the primary growth engine for the industry. This trend highlights the increasing importance of liability insurance as a structural driver for sustained market expansion. Health insurance, bolstered by cutting-edge claims processing and an array of enticing add-ons, continues to serve as the industry's cornerstone. These advancements enhance customer satisfaction and streamline operational efficiency for insurers. Owners, already equipped with liability plans, are increasingly drawn to high-deductible health plans. This choice safeguards their budget and mitigates risks associated with major surgeries, offering a balanced approach to cost management and coverage. With dog ownership plateauing and cat adoption on the upswing, insurers foresee a further shift in the liability ratio. This anticipation is fueled by ongoing political discussions aiming to extend mandatory third-party coverage beyond just canines, potentially broadening the market and creating new growth opportunities for insurers.

By Animal Type: Dogs Lead While Cats Accelerate

Dogs contributed 63.92% of written premiums in 2025 because higher average treatment costs and liability obligations compel owners to seek protection. The Germany pet insurance market size for cats escalates faster at 13.19% CAGR as urbanization and smaller households favor feline companions. Cat policies generally price 20–30% below dog equivalents, broadening affordability without eroding margins thanks to lower average claim costs. Younger owners are also more willing to buy multi-pet packages, combining cat and dog cover under one discount, improving overall spending per household. Marketing content now includes breed-specific health tips that double as risk-mitigation tools, lowering claim frequency while increasing perceived insurer expertise.

Breed-linked orthopedic risks keep dog premiums elevated, while indoor lifestyle-related illnesses such as obesity and renal disease drive the cat claims mix. Insurers tailor underwriting formulas to each species, refining risk selection and sustaining profitability. Gene-testing add-ons, offered at a reduced price for policyholders, identify hereditary disorders early and build data insights. Growth in cat coverage also helps close the penetration gap among metropolitan renters, expanding overall policy counts in the Germany pet insurance market.

By Sales Channel: Digital Transformation Accelerates

Direct-to-consumer outlets held a 41.86% share in 2025, reflecting decades-long reliance on the agent networks of leading carriers. Yet online aggregators and insurtech apps outpace all other channels with a 14.5% CAGR as tech-native owners browse, compare, and bind policies on mobile devices. Instant quotes, simplified KYC, and chat-based claims settlement form the core value proposition that fuels channel migration. Aggregators also upsell add-ons using in-journey nudges, raising the average policy premium by up to 12% without human intervention. Data collected on click-through paths feeds machine-learning models that forecast churn, triggering retention offers before cancellation requests surface.

Traditional brokers retain relevance in rural areas and among older demographics who favor advice-led sales. Hybrid models where agents guide purchases on insurer platforms are emerging to preserve relationship equity while capturing digital efficiencies. Bancassurance partnerships exploit existing KYC data in retail banking apps to pre-fill application forms, cutting purchase time to under three minutes. Improved user journeys lower acquisition costs over time, even if initial marketing spending surges. Data gathered from aggregator funnels also feeds dynamic pricing engines, sharpening competitiveness across the Germany pet insurance market.

By Coverage Level: Premium Migration Emerges

Standard caps up to USD 5,207.8 per year attracted 44.82% of buyers in 2025, balancing affordability with realistic risk transfer. However, comprehensive plans offering unlimited annual benefits show a 12.29% CAGR, mirroring consumer readiness to safeguard pets against extreme procedures. Rising GOT tariffs and broader acceptance of MRI, endoscopy, and advanced oncology push owners toward higher caps. Loyalty schemes that roll unused annual limits into the next policy year heighten appeal, especially for young, healthy pets. Premium financing through monthly installments further eases cash-flow impact, mitigating sticker shock that once discouraged top-tier adoption.

Basic policies with USD 1,041.5 limits remain popular starter products but face attrition when claims exceed payout ceilings. Carriers actively upsell at renewal, citing concrete examples of cost escalation to justify cap increases. Meanwhile, premium-tier plans embed tele-vet subscriptions at no extra charge, adding perceived value and reducing claim frequency through early triage. Digital claim submissions now pay within 48 hours, cementing trust in unlimited-cap products. The premiumization trend deepens average policy value, reinforcing revenue growth in the Germany pet insurance market.

Geography Analysis

South Germany maintains leadership due to robust economic indicators, dense veterinary infrastructure, and cultural propensity to treat pets as household dependents. Bavaria’s urban hubs frame a consumer base willing to pay for preventive dental work, physiotherapy, and emergency surgery, all of which are indexed above the national average. Strong local reputations of Allianz and Munich Re subsidiaries support cross-selling into motor and home lines, embedding multi-policy relationships that curb churn within the Germany pet insurance market.

East Germany exhibits the fastest expansion as Berlin, Dresden, and Leipzig benefit from tech-driven employment growth that boosts disposable income. Pension purchasing power exceeds West German averages once cost-of-living indices are applied, making pet coverage affordable to retirees who favor low-maintenance cats. Digital sign-up journeys from insurtechs such as Getsafe eliminate branch visits, aligning well with the online banking habits prevalent in the region. Government discussion around mandatory canine health cover could trigger a step-change in policy counts if adopted by 2027. Regional e-commerce platforms also bundle introductory pet insurance offers with food subscriptions, widening reach among new adopters.

The West and North regions sustain steady growth underpinned by mature broker networks and stable household incomes. Hamburg’s logistics clusters yield a pet-friendly workforce, yet market saturation tempers the headline pace. Liability-focused incremental gains dominate in rural Lower Saxony and Schleswig-Holstein, where working dogs prompt third-party cover. Cross-border tourism has also spurred insurers to add temporary EU travel riders, popular among vacationers from coastal towns. Across these areas, insurers emphasize hybrid wellness-plus-accident bundles to maintain relevance as veterinary clinics push their subscription plans. Collectively, geographic variances require nuanced pricing, product configuration, and channel strategies to unlock full value for the Germany pet insurance market.

Competitive Landscape

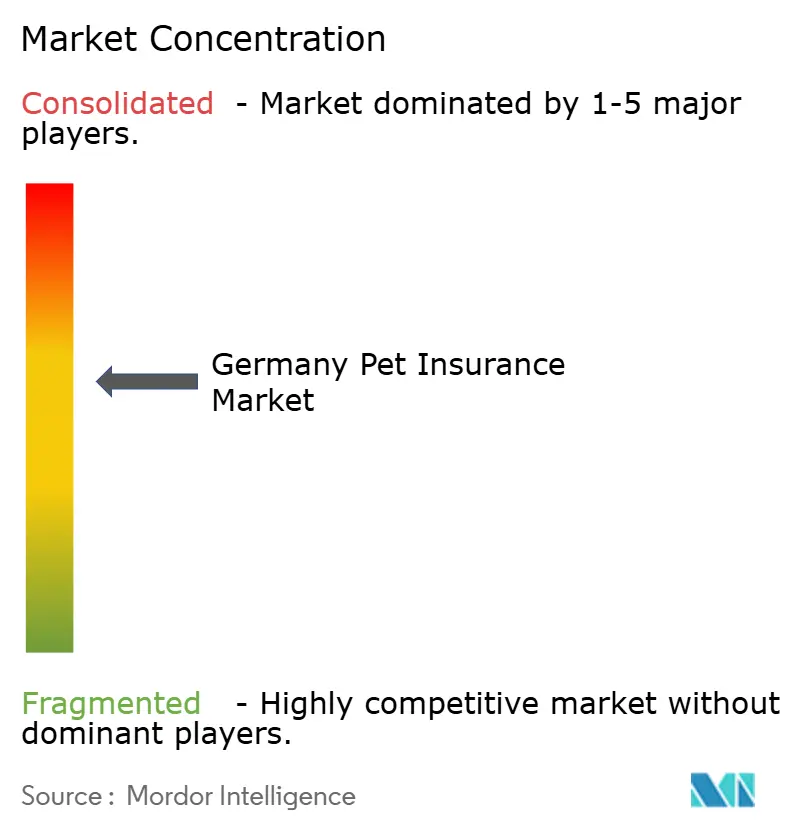

The Germany pet insurance market exhibits moderate fragmentation, with traditional insurers competing alongside emerging insurtech platforms, creating a dynamic competitive environment where established players leverage brand recognition while digital entrants offer superior customer experience and pricing transparency. Market concentration remains relatively low, with no single player commanding a dominant market share, though Allianz Group (through AGILA and Petplan subsidiaries) maintains a significant presence alongside established carriers like Uelzener, HanseMerkur, and ERGO. The competitive intensity has increased substantially as insurtech platforms like Getsafe, Feather, and Lassie challenge traditional distribution models through digital-first approaches and streamlined product offerings. Strategic patterns reveal a clear divide between relationship-based traditional insurers and transaction-focused digital platforms, with customer acquisition costs and retention strategies varying significantly between these approaches.

Technology adoption has become the primary competitive differentiator, with companies like Munich Re developing AI-driven underwriting tools through their REALYTIX ZERO CoPilot platform to enhance automation and reduce product development timelines. White-space opportunities exist in senior pet coverage, IoT integration for risk-based pricing, and regional market penetration in underserved East German territories. Emerging disruptors focus on customer experience optimization, transparent pricing, and value-added services like telemedicine and preventive care programs that extend beyond traditional claims processing. The competitive landscape evolution suggests consolidation potential as smaller players struggle with customer acquisition costs while larger insurers seek digital capabilities through partnerships or acquisitions, similar to Chubb’s acquisition of Healthy Paws in the broader pet insurance market.

Strategic differentiation pivots on value-added services. Tele-vet consultations, 24/7 chat, and wellness dashboards cultivate loyalty while lowering claim costs through early intervention. Senior-pet products and partial coverage for pre-existing illnesses represent white space still thinly served but likely to see new product launches over the next two years. As insurers bundle liability, medical, and wellness into single contracts, the Germany pet insurance market is moving closer to the holistic framework that characterizes Scandinavian benchmarks.

Germany Pet Insurance Industry Leaders

Allianz Versicherungs-AG

AGILA Haustierversicherung AG

Uelzener Allgemeine Versicherungs-Gesellschaft

HanseMerkur Krankenversicherung AG

Getsafe Digital GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ELEMENT Insurance AG entered insolvency, impacting 320,000 contracts and creating takeover opportunities.

- January 2025: Generali unveiled the “Lifetime Partner 27” plan, pledging AI investments and protection-gap initiatives, including pet cover.

- May 2024: Munich Re launched REALYTIX ZERO CoPilot, an AI underwriting platform enabling faster, customised pet products.

- April 2024: Chubb finalized the acquisition of Healthy Paws, signaling ongoing pet insurance consolidation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the German pet insurance market as all premium revenue earned from policies that cover veterinary treatment or legally mandated third-party liability for companion animals kept in households across Germany. Policies purchased online, through agencies, banks, or directly from insurers are included, while revenue is recorded in constant 2025 U.S. dollars.

Scope Exclusions: Travel-only pet cover, embedded micro-insurance offered free with loyalty cards, and livestock or equine policies are outside this scope.

Segmentation Overview

- By Policy Type

- Pet Health Insurance

- Pet Liability Insurance

- By Animal Type

- Dogs

- Cats

- By Sales Channel

- Direct to Consumer

- Broker / Agent

- Bancassurance

- Online Aggregators & Insurtech Platforms

- By Coverage Level

- Basic (≤ €1 000 annual cap)

- Standard (≤ €5 000 annual cap)

- Comprehensive (Unlimited / higher caps)

- By Region

- North

- West

- South

- East

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed underwriting heads at multi-line insurers, digital brokers, veterinary association board members, and insurtech founders across Bavaria, North Rhine-Westphalia, Berlin, and Saxony. These discussions clarified average premium ladders, claim frequency by breed, and emerging embedded insurance pilots, which in turn grounded the assumptions drawn from secondary material.

Desk Research

We began by mapping the demand pool with publicly available series such as pet population counts from the German Pet Trade Association (ZZF), average veterinary invoice data published under the federal fee schedule (GOT), and state-level dog liability mandates collated by the Federal Ministry of Justice. Additional context came from European Insurance and Occupational Pensions Authority dashboards, scholarly articles in the Journal of Veterinary Science, and company filings sourced via Dow Jones Factiva and D&B Hoovers. Select shipment-level insights from Volza and patent trends from Questel helped verify innovation intensity. The sources listed are illustrative; many more datasets and documents guided validation and clarification.

Market-Sizing & Forecasting

A blended top-down and bottom-up approach underpins the model. Top-down reconstruction starts with household pet stocks, overlays species-wise policy penetration, adjusts for mandatory dog liability uptake, and multiplies by validated average annual premiums. Supplier roll-ups of sampled insurtech gross written premiums provide a bottom-up sense check before totals are finalized. Key variables include: 1) annual change in companion animal population, 2) mean veterinary cost index, 3) disposable income per capita, 4) penetration differentials between urban and rural states, and 5) average premium inflation. A multivariate regression, cross-checked through scenario analysis, projects these drivers to 2030. Gaps in granular insurer disclosures are bridged using weighted averages from primary interviews.

Data Validation & Update Cycle

Outputs pass successive peer reviews, automated variance flags, and reconciliation with independent premium collections from BaFin. Reports refresh each year, and interim revisions are triggered when legislation, catastrophic outbreaks, or large M&A events materially alter baselines. Before delivery, an analyst reruns the model so clients receive the most current view.

Why Our Germany Pet Insurance Baseline Commands Trust

Published estimates often diverge because firms choose different policy mixes, penetration assumptions, and currency bases. Understanding those levers is vital for decision-makers.

Key gap drivers include whether liability-only policies are counted, how fast veterinary costs are assumed to rise, the refresh cadence of pet population data, and the year used for currency conversion. Mordor Intelligence aligns scope precisely with market realities and refreshes inputs annually, which curbs over or under-statement.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.16 B (2025) | Mordor Intelligence | - |

| USD 1.34 B (2025) | Global Consultancy A | Higher penetration assumptions, omission of liability-only policies, aggressive veterinary cost escalator |

| USD 1.40 B (2024) | Industry Analyst B | Mixes accident-only and wellness add-ons, uses constant 2022 € exchange |

| USD 0.72 B (2023) | Trade Journal C | Excludes surgical cover, counts broker sales only, limited regional scope |

Taken together, the comparison shows that Mordor's disciplined selection of scope, annually refreshed inputs, and dual-path validation delivers a balanced, transparent baseline that stakeholders can replicate and trust.

Key Questions Answered in the Report

What is the current value of the Germany pet insurance market?

The market is valued at USD 1.28 billion in 2026 and is projected to reach USD 2.08 billion by 2031.

How fast is the Germany pet insurance market growing?

It is expanding at a 10.20% CAGR over the 2026-2031 period.

Which region leads the Germany pet insurance market?

South Germany, particularly Bavaria and Baden-Württemberg, leads with 29.85% revenue share as of 2025.

Which sales channel is growing the quickest?

Online aggregators and insurtech platforms are advancing at a 14.5% CAGR through 2031.

Why are comprehensive plans gaining popularity?

Rising veterinary costs and greater willingness to invest in unlimited protection are driving a 12.29% CAGR for comprehensive coverage options.

What is the biggest challenge for wider adoption?

High premium cost relative to perceived need remains the chief barrier, especially among price-sensitive households in East Germany.

Page last updated on: