Europe Automotive Collision Repair Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

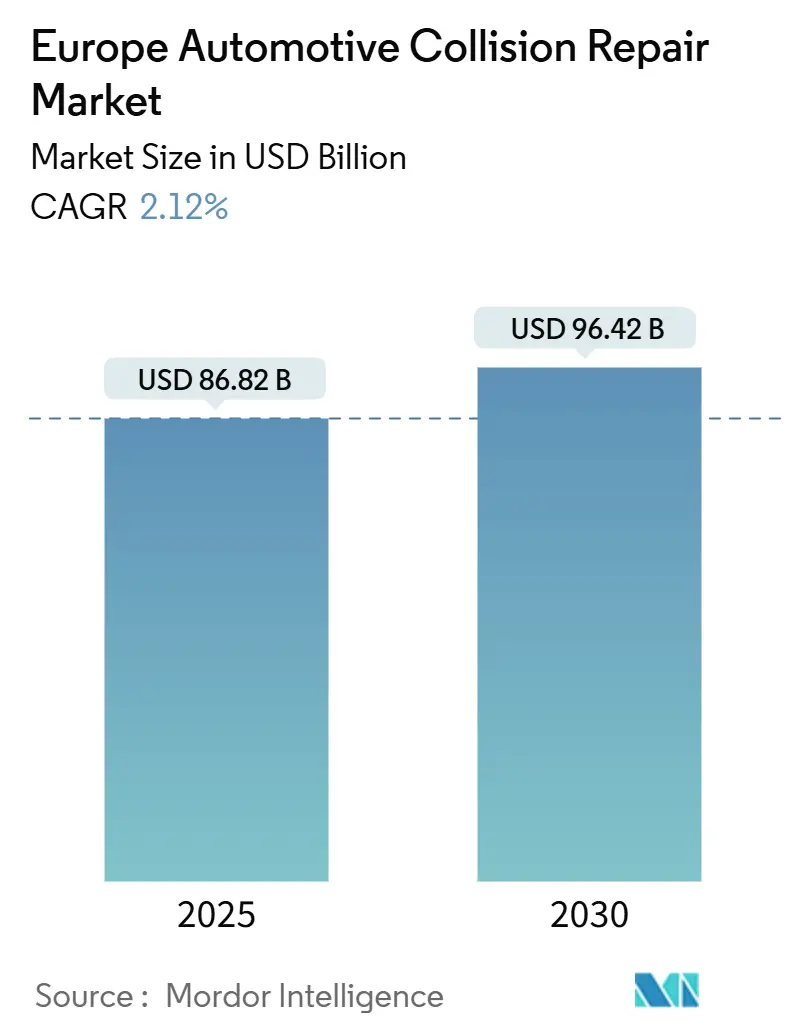

| Market Size (2025) | USD 86.82 Billion |

| Market Size (2030) | USD 96.42 Billion |

| Growth Rate (2025 - 2030) | 2.12% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automotive Collision Repair Market Analysis by Mordor Intelligence

The European automotive collision repair market size is USD 86.82 billion in 2025 and is forecast to reach USD 96.42 billion by 2030, reflecting a 2.12% CAGR over the period. The measured expansion mirrors a maturing yet resilient landscape shaped by stringent environmental regulations, digital insurance ecosystems, and growing ADAS penetration. Water-borne refinish systems gain ground as EU VOC limits push body shops to invest in compliant spray-booth upgrades. At the same time, the aging vehicle parc lifts repair frequency, especially in Western Europe[1]“Average age of the European vehicle fleet,”, European Environment Agency, eea.europa.eu. Glass replacement and calibration revenue accelerate because advanced driver-assistance sensors are now embedded in almost every new windshield, raising technical complexity and ticket value. DIFM channels dominate today, but rising e-commerce adoption nudges a steady DIY uptick as consumers secure professional-grade parts directly online. Competitive intensity stays high as regional consolidators pursue scale to fund technology, training, and sustainability initiatives, even as battery-electric power-trains begin to trim mechanical claim volumes.

Key Report Takeaways

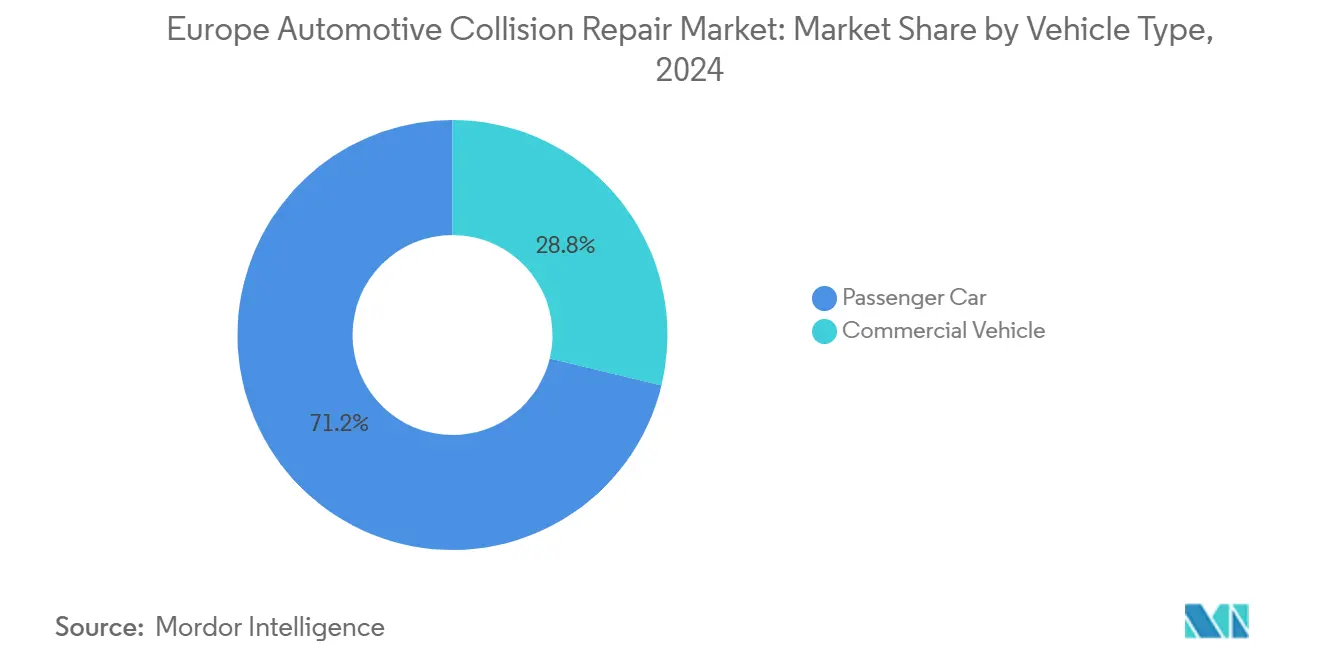

- By vehicle type, passenger cars held 71.22% of Europe automotive collision repair market share in 2024, while commercial vehicles are projected to expand at a 3.21% CAGR through 2030.

- By product, spare parts accounted for 43.41% of the Europe automotive collision repair market in 2024; glass components are advancing at a 3.37% CAGR between 2025 and 2030.

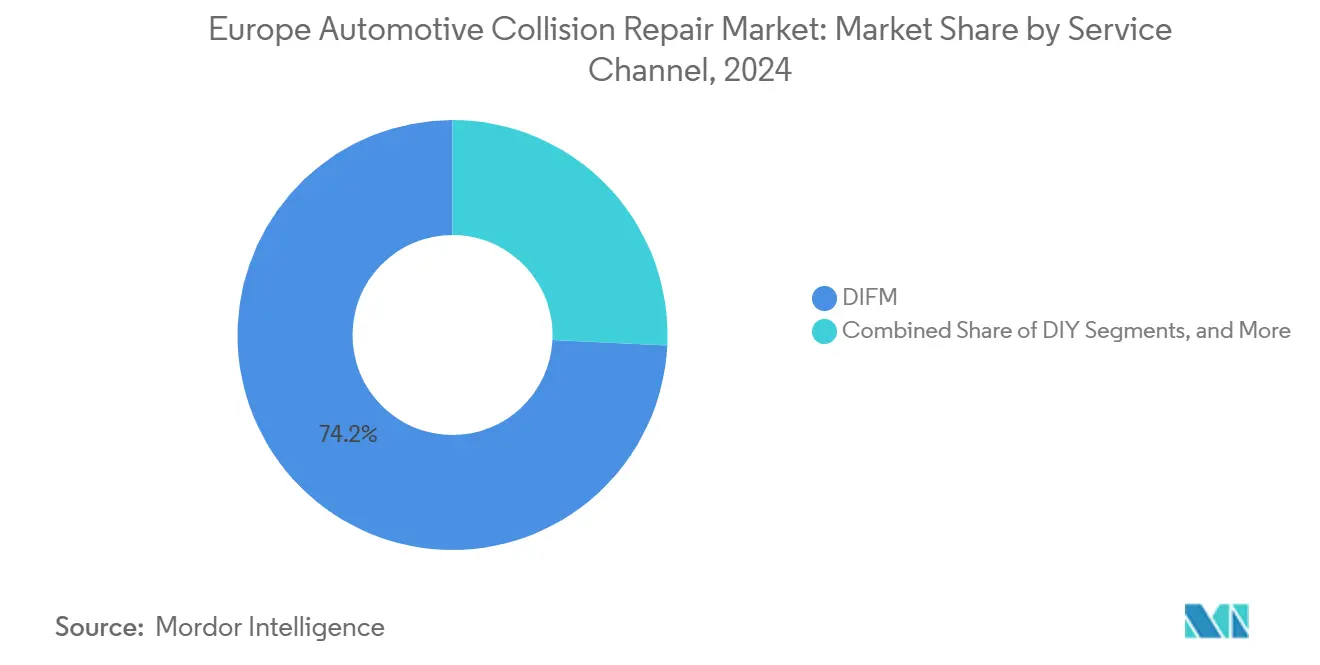

- By service channel, DIFM commanded a 74.22% share of the Europe automotive collision repair market in 2024, and DIY is set to grow at a 3.83% CAGR through 2030.

- By damage type, cosmetic and paint repairs captured a 44.32% share of the Europe automotive collision repair market in 2024, whereas glass and ADAS calibration services are posting a 3.98% CAGR to 2030.

- By country, Germany led with a 28.28% share of the Europe automotive collision repair market in 2024, while Spain is on track for a 3.76% CAGR during the forecast window.

Europe contributes to a system defined not by any single geography but by the interaction of many. The global automotive collision repair market data by Mordor Intelligence represents that combined structure.

Europe Automotive Collision Repair Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADAS-Equipped Windshields Boost Calibration Revenue | +0.8% | Germany, United Kingdom, France, Scandinavia | Short term (≤ 2 years) |

| Aging Vehicle Parc Increases Repair Frequency and Parts Demand | +0.6% | Western Europe core, spillover to Eastern Europe | Long term (≥ 4 years) |

| E-Commerce Parts Portals Improve Access and Price Transparency | +0.5% | Global with early adoption in United Kingdom, Germany | Medium term (2-4 years) |

| EU VOC Limits Accelerate Water-Borne Refinish Adoption | +0.4% | Europe-wide, strongest in Germany, France, Netherlands | Medium term (2-4 years) |

| Digital Claims Platforms Speed Up Repair Authorization | +0.3% | United Kingdom, Germany, Netherlands, Nordic countries | Short term (≤ 2 years) |

| OEM Captive-Parts Monetization Raises Repair Ticket Size | +0.2% | Germany, France, Italy, Spain | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in ADAS-Equipped Windshields Drives Calibration Revenue

Windshields now house cameras, radar, and lidar modules that require post-repair calibration within tight tolerance brackets. Equipment from Hofmann delivers OEM-level accuracy, and independent shops gain data access through Euro 5 PassThru standards [2]“ADAS Calibration Solutions,”, Hofmann, hofmann-equipment.com. Smaller operators without the capital to acquire calibration rigs face rising barriers to entry, accelerating a technology-driven consolidation wave.

Aging Vehicle Parc Raises Repair Frequency and Parts Demand

In Europe, as passenger cars age, they increasingly suffer from wear issues like corrosion and paint failures, leading to a surge in repair demand. The cross-border trade of used cars, particularly in Eastern Europe, not only extends the lifespans of these vehicles but also amplifies the demand for discontinued parts. This trend, bolstered by supply delays from the pandemic, has boosted repair shops and aftermarket suppliers. Additionally, the aging vehicle fleet across the region has created opportunities for manufacturers to innovate and supply high-quality replacement parts, while repair shops are expanding their service offerings to cater to the growing demand. The aftermarket sector is also witnessing increased investments in technology and logistics to address these evolving needs effectively.

E-Commerce Parts Portals Widen Access and Price Transparency

LKQ Europe blends a vast warehouse network with a daily-accessed online catalog serving thousands of workshops. Its acquisition of Uni-Select/GSF Car Parts adds significant UK branch coverage, strengthening its hybrid model of digital storefronts and localized delivery—enhancing speed, reach, and service depth across the aftermarket ecosystem. Instant inventory checks, VIN-matched search, and next-day shipping allow even micro-garages to source OEM-grade or tier-one alternatives at wholesale prices. Consumers also capitalize, fueling DIY repair growth despite collision work remaining heavily technical. Heightened transparency compresses margins for traditional distributors but increases overall efficiency across the European automotive collision repair market.

Stringent EU VOC Limits Accelerate Shift to Water-Borne Refinish Systems

EU rules cap solvent emissions at 200 g/L for pre-cleaning and 840 g/L for special finishes, forcing many body shops to retrofit ventilation, drying, and mixing rooms. Large repair networks absorb these costs more effectively than small independents, which drives consolidation. Compliance also enables premium pricing as insurers and corporate fleets prefer environmentally verified suppliers. Paint manufacturers such as Axalta cut VOC emissions by up to 50% while retaining color-match precision [3]“Water-borne Refinish Portfolio,”, Axalta, axalta.com. Exemptions for classic vehicles open a niche for specialists still using solvent-based products, creating a dual-track market inside the broader regulatory framework.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-Material Inflation Squeezing Body-Shop Margins | -0.4% | Europe-wide, particularly affecting smaller operators | Short term (≤ 2 years) |

| BEV Simplicity Reducing Mechanical Collision Claims | -0.3% | Norway, Netherlands, Germany, United Kingdom | Medium term (2-4 years) |

| Skilled-Labor Shortage Limiting Peak Repair Capacity | -0.2% | Germany, United Kingdom, France, Scandinavia | Long term (≥ 4 years) |

| Right-to-Repair Uncertainty Hindering IAM Investment | -0.1% | Europe-wide with country-specific implementation variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Raw-Material Inflation Squeezes Body-Shop Margins

EU antidumping tariffs added EUR 0.25-0.74 per kg to titanium dioxide, a pigment used in many refinish products [4]“Titanium Dioxide Market Update,”, Axalta, axalta.com. Rising energy costs and geopolitical trade shifts magnify input inflation. Paint makers experiment with bio-based binders, though scale economics remain nascent. Insurance labor-rate negotiations lag these material spikes, compressing gross profit until yearly contracts adjust. Larger chains leverage volume agreements to buffer volatility, but single-site operators feel the margin pinch immediately.

BEV Power-Train Simplicity Cuts Mechanical Collision Claims

Battery-electric vehicles tend to be involved in fewer accidents and insurance claims compared to conventional cars. However, when incidents occur and the battery pack is affected, the cost of repairs or claims tends to be significantly higher. Thermal-event risk demands quarantined zones and specialist PPE, raising overhead for collision shops. Limited supply of certified EV technicians inflates wages and drags repair cycle times. Some insurers route high-voltage repairs exclusively to OEM franchised centers, diverting revenue from independents inside the European automotive collision repair market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Electrification Momentum

Europe automotive collision repair market size is attributed to passenger cars still accounting for 71.22% share in 2024. Still, commercial fleets account for growing parts and labor spending because battery-electric delivery vans require specialized tooling. Employer-funded maintenance bundles further lock in recurring revenue streams for certified centers. Commercial vehicles contributed a smaller volume yet posted the swiftest 3.21% CAGR through 2030. Fleet operators measure downtime in lost revenue minutes, thus pushing repair shops for standardized, rapid-turn processes that integrate battery diagnostics and ADAS calibration in a single visit. LKQ Europe launched Elitek mobile units to meet this need, underscoring how convenience intertwines with technical depth.

Fleet electrification amplifies the risk of high-voltage contact, so insurers mandate proof of technician certification. This drives investment in insulated tooling, battery lifts, and containment pods. Independent garages unable to certify quickly cede contracts to national chains. Meanwhile, passenger-car owners display brand-loyal behavior, raising expectations for OEM finishes and digital service tracking. As a result, the European automotive collision repair market witnesses parallel service models: cost-optimized fleet agreements on one side, premium retail experiences on the other.

By Product: Glass Components Accelerate Through ADAS Integration

Spare parts held a 43.41% share of the Europe automotive collision repair market in 2024, anchored by bumpers, lamps, and sheet-metal panels. Yet glass leads growth at 3.37% CAGR through 2030 because every ADAS sensor embedded in a windshield must be recalibrated after replacement. Europe's automotive collision repair market share for glass rose in urban corridors with the highest autonomous emergency braking adoption. Belron capitalizes by bundling replacement with OEM-specified calibration, commanding higher margins than commodity side-panel sales.

Sustainability pressures push paint and consumables suppliers to innovate around low-solvent formulas and recycled plastics. Raw-material volatility complicates pricing, making just-in-time inventory tools from 3M’s RepairStack more critical. Within metal parts, supply constraints on micro-alloy steels can cause temporary gaps that favor salvage and refurbished components, introducing a circular-economy dimension to the European automotive collision repair market.

By Service Channel: DIFM Dominance Faces DIY Digital Disruption

DIFM channels kept 74.22% command of the Europe automotive collision repair market share in 2024, reflecting insurance steering and the complexity of structural alignment, paint blending, and electronic coding. However, DIY is rising at a 3.83% CAGR through 2030, as digital platforms supply repair tutorials, VIN-matched parts, and one-click tool rentals. Younger drivers often tackle mirror caps, minor bumper scuffs, and sensor covers themselves, consuming aerosol blends that comply with EU VOC caps.

Large chains respond by enhancing convenience. Mobile glass vans, pick-up-and-deliver programs, and same-day express bays create compelling value over at-home fixes. Subscription-based maintenance gives buyers peace of mind through unlimited cosmetic touch-ups for a flat monthly fee, locking customers into the European automotive collision repair market ecosystem. Right-to-repair legislation reduces OEM exclusivity on visible parts, but manufacturers counter with warranties tied to certified installs, retaining a slice of business even as independents gain legal access.

By Damage Type: ADAS Calibration Commands Premium Pricing

Cosmetic and paint jobs remained the volume leader, with a 44.32% share of the Europe automotive collision repair market in 2024, yet glass and ADAS calibration climbed fastest, at a 3.98% CAGR through 2030. Ultra-thin camera housings and embedded radar modules require millimeter-level alignment. Calibration bays equipped with static targets and dynamic road-test rigs see utilization spikes, pushing ROI on these assets well ahead of schedule.

Structural repairs decline in frequency thanks to improved crumple-zone engineering and automated braking, but when heavy hits occur, exotic materials like boron steel and aluminum raise complexity. To stay competitive, shops invest in multi-metal welders, non-destructive testing, and ultrasound. At the same time, cosmetic work benefits from the aging fleet, where clear-coat fade and micro-dents erode resale value. Water-borne color systems paired with digital spectrophotometers cut process time and VOC output, giving compliant facilities an edge across the European automotive collision repair market.

Geography Analysis

By Geography: Germany Anchors, Spain Surges, East Expands

Germany contributed 28.28% of Europe automotive collision repair market share in 2024, underpinned by the continent’s largest vehicle parc and an average age of over 10 years. TÜV inspection data shows rising fault incidences, propelling stable workshop volumes. Multi-site networks dominate high-value ADAS and EV work because they can carry the cost of specialized rigs.

Spain is forecast to grow at a 3.76% CAGR to 2030 as economic revival and infrastructure upgrades boost mobility. Seasonal tourism peaks trigger collision spikes that benefit coastal repair clusters. The UK and France exhibit mature insurer-steered ecosystems where digital claims platforms slash approval cycles. Italy’s fragmented workshop landscape offers a consolidation opportunity for acquisitive groups seeking regional density.

Eastern Europe stretches vehicle lifespans to 28 years, creating enduring demand for legacy parts and refurbishment services. Cross-border flows of Western used cars sustain volumes, while cost-sensitive owners opt for non-OEM spares sourced via pan-European portals. Nordic states lead EV adoption, forcing repairers to meet battery isolation standards sooner than their southern counterparts. This geographic diversity shapes a multifaceted European automotive collision repair market that rewards scale and localized specialization.

The automotive collision repair market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for North America and Asia.

Competitive Landscape

Fragmentation persists, yet consolidation accelerates as regulatory compliance and technology needs raise entry hurdles. Belron owns the glass niche, leveraging 1,300 centers and a fleet of mobile vans for on-site calibration. Paint giants Axalta and PPG battle on sustainability claims, digital color-match platforms, and rapid-cure chemistries.

Investment in AI damage recognition gains pace. 3M’s RepairStack automates consumable restocking, ensuring line-side availability and data-driven cost tracking. Independent shops adopt these tools to stay within insurer referral networks, mitigating the scale advantage of chains.

Design-protection reform also alters playing fields. OEMs shift to captive-parts monetization and brand-certified shop programs to retain share. Meanwhile, labor shortages in Germany and France raise wages, prompting chains to partner with vocational schools to secure talent pipelines. Overall, intense yet rational competition defines the European automotive collision repair market.

Europe Automotive Collision Repair Industry Leaders

Belron Group

LKQ Corporation

Steer Automotive Group

Axalta Coating Systems, LLC

Mondofix Inc. (Fix Auto)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Axalta acquired three European distributors and is integrating them into its Axalta Axcess network. Axalta Axcess serves as Axalta's direct-to-customer sales and distribution platform, streamlining ordering, delivery, and aftersales support for its European clientele.

- October 2024: After a decisive vote from the Council of the EU, the European Union has officially adopted a repair clause. This new clause grants the freedom to choose visible repair spare parts. The harmonized European repair clause has been integrated into the EU Design Directive and the Design Regulation.

Europe Automotive Collision Repair Market Report Scope

| Passenger Car |

| Commercial Vehicle |

| Paints and Coatings |

| Consumables |

| Spare Parts |

| Glass |

| Other Product |

| Do-It-Yourself (DIY) |

| Do-It-For-Me (DIFM) |

| Original Equipment (OE) |

| Structural Repair |

| Cosmetic and Paint |

| Glass & ADAS Calibration |

| United Kingdom |

| Germany |

| Spain |

| Italy |

| France |

| Russia |

| Rest of Europe |

| By Vehicle Type | Passenger Car |

| Commercial Vehicle | |

| By Product | Paints and Coatings |

| Consumables | |

| Spare Parts | |

| Glass | |

| Other Product | |

| By Service Channel | Do-It-Yourself (DIY) |

| Do-It-For-Me (DIFM) | |

| Original Equipment (OE) | |

| By Damage Type | Structural Repair |

| Cosmetic and Paint | |

| Glass & ADAS Calibration | |

| By Country | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected value of the Europe automotive collision repair market by 2030?

The market is forecast to reach USD 96.42 billion by 2030, reflecting a 2.12% CAGR across the period.

Which product category is growing fastest in European collision repair?

Glass components, driven by ADAS-ready windshields and required calibration, are advancing at a 3.37% CAGR.

Why does Germany command the largest share of European collision repair spending?

Germany’s large, aging vehicle parc and high technology adoption rate generate consistent repair demand, securing 28.28% share in 2024.

How are EU VOC regulations affecting repair shops?

Strict solvent limits push shops toward water-borne coatings, triggering capital upgrades but enabling premium pricing for compliant service.

What impact do battery-electric vehicles have on collision repair revenue?

EVs reduce mechanical claim frequency but increase average repair cost due to battery safety protocols and specialized technician needs.

Page last updated on: