Europe Car Wash Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2019 - 2024 |

| Market Size (2026) | USD 11.01 Billion |

| Market Size (2031) | USD 14.12 Billion |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

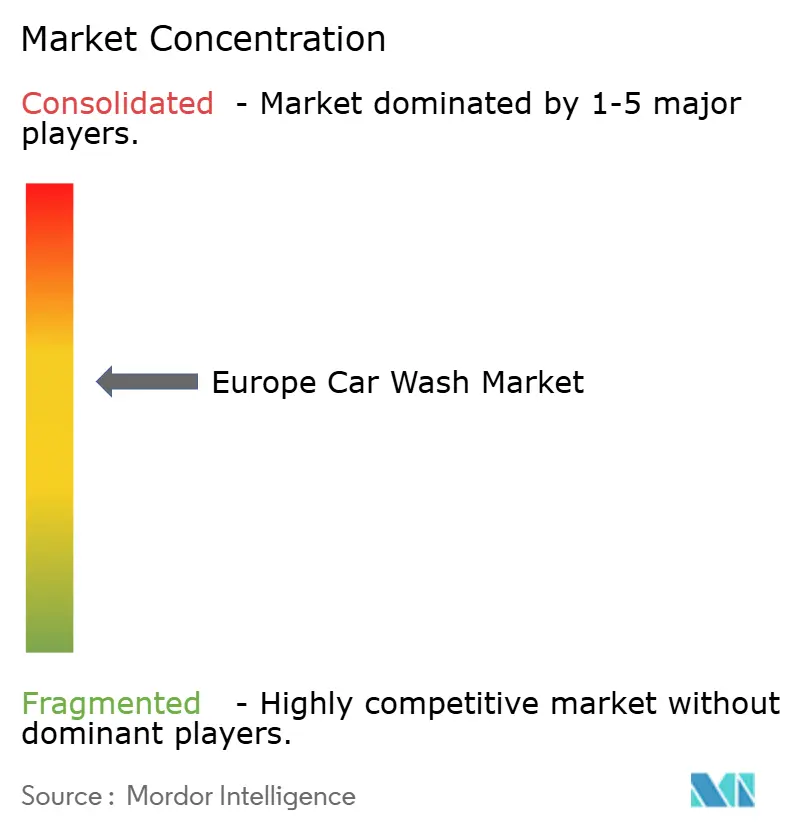

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Car Wash Market Analysis by Mordor Intelligence

The European car wash market size stood at USD 11.01 billion in 2026 and is projected to reach USD 14.12 billion by 2031, advancing at a 5.10% CAGR during the forecast period. Subscription programs have driven significant growth in recurring revenue, while one-off transactions have declined. This shift underscores a new strategy in the European car wash market: prioritizing customer loyalty over mere footfall. Germany commands a leading share of the market's value, bolstered by the region's densest network of professional wash sites. Meanwhile, Spain is witnessing the quickest growth, fueled by the late adoption of tunnel washes and a shift to cashless payments. While automatic tunnels dominate the market, manual bays are making a comeback. This resurgence is driven by the demand for higher-pressure, touch-free options, especially for commercial vehicles and paint-protection-film constraints. Cashless transactions are on a growth trajectory, driven by app features that reduce queue times and enable dynamic pricing. The competitive landscape remains fragmented. Leading equipment vendors—WashTec, Kärcher, and Istobal—collectively service a minority of installed sites, allowing local independents to carve out a niche by emphasizing speed, uptime, and retrofit financing.

Key Report Takeaways

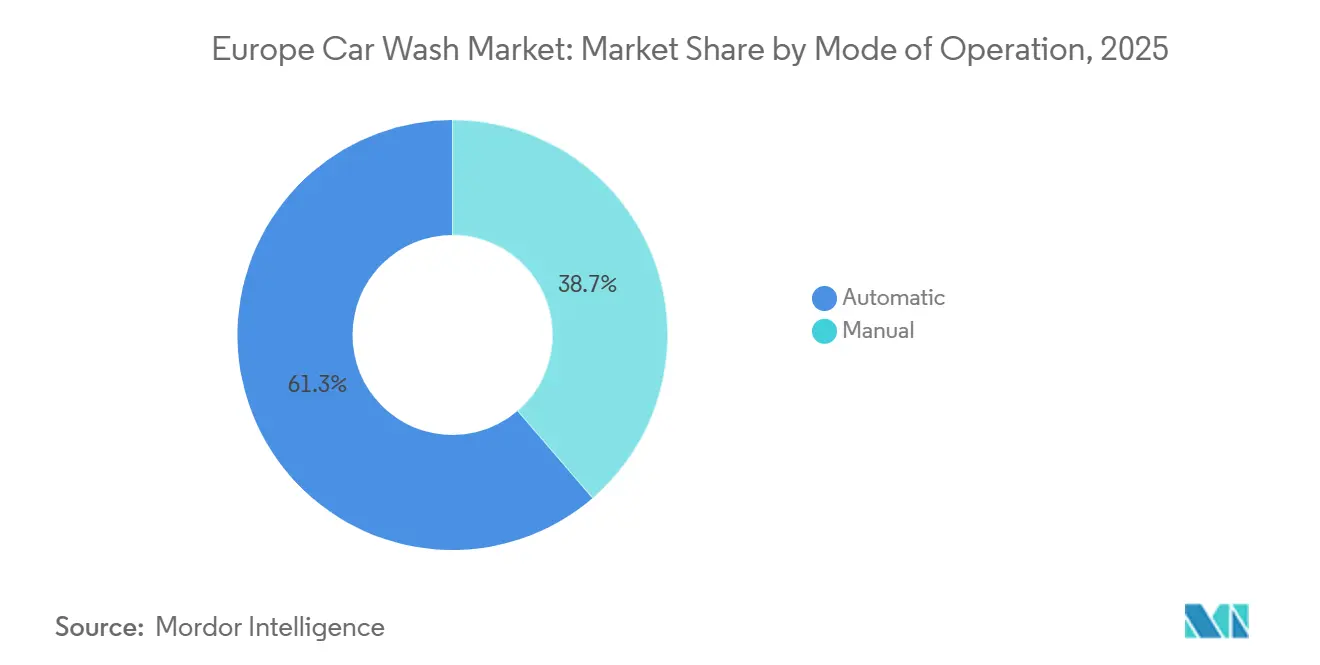

- By mode of operation, automatic systems held 61.25% of the European car wash market share in 2025; manual bays expand the fastest at a 6.33% CAGR through 2031.

- By payment mode, cash accounted for 66.14% of the European car wash market share in 2025, while cashless transactions are forecast to rise at a 7.42% CAGR through 2031.

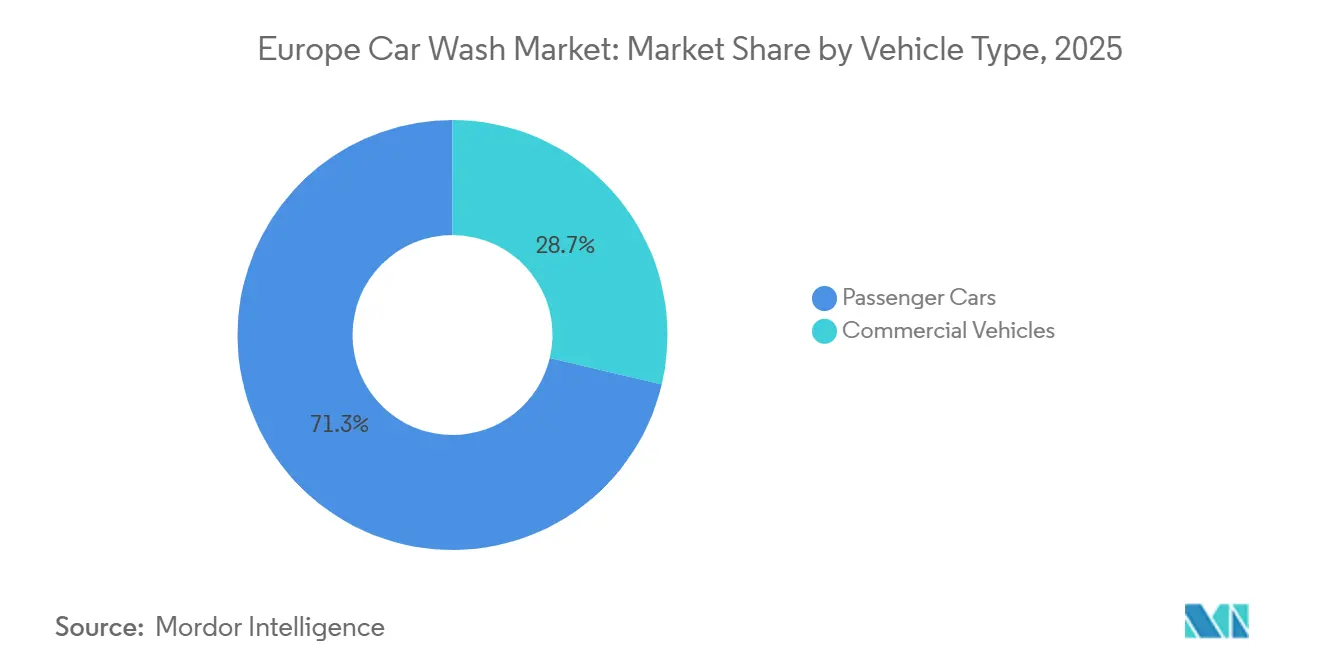

- By vehicle type, passenger cars accounted for 71.26% of the European car wash market in 2025; commercial vehicles posted the highest 5.87% CAGR to 2031.

- By end user, individual consumers accounted for 76.11% of the European car wash market share in 2025, whereas fleet operators grew at an 8.13% CAGR through 2031.

- By country, Germany led the European car wash market with a 30.25% share in 2025; Spain recorded the steepest CAGR of 6.74% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on car wash market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Car Wash Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subscription "Wash-Club" Models | +1.4% | United Kingdom, Germany, France; emerging in Spain, Italy | Short term (≤ 2 years) |

| Shift to Automatic Car Washes | +1.2% | Germany, United Kingdom, Netherlands; slower in Southern Europe | Short term (≤ 2 years) |

| Regulations Favor Professional Services | +0.9% | EU-wide; strongest in Germany, Netherlands, Denmark | Long term (≥ 4 years) |

| Rising Vehicle Ownership/Car Parc | +0.8% | Germany, France, Italy, Spain; moderate in United Kingdom | Medium term (2-4 years) |

| App-Based Digital Payments | +0.6% | Urban hubs in Germany, United Kingdom, France, Nordics | Medium term (2-4 years) |

| OEM–Dealer Wash-Bay Integrations | +0.5% | Germany, United Kingdom, France | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Subscription-Based “Wash-Club” Models Accelerating Repeat Business

In 2024, recurring memberships grew significantly, while walk-up sales declined. This shift bolstered overall operator revenue, driven by increased visit frequency, even as ticket sizes stabilized. Average monthly fees remain consistent, and the projected lifetime value supports equipment upgrades. In February 2024, WashTec partnered with Superoperator, enabling a portion of its European clientele to redeem services across sites. This move, aimed at curbing churn, is especially beneficial for customers on the move. The International Carwash Association noted that many members who canceled still frequent the same site, underscoring the effectiveness of trial subscriptions as acquisition tools. In Southern Europe, operators are testing tiered plans to address affordability concerns. Additionally, to counter churn driven by expired cards, operators are now automating prompts to update credit cards.

Shift Toward Convenience-Oriented Automatic Washes

While automatic tunnels lead in volume, their adoption is influenced by labor costs. In Northern Europe, high labor costs drive a shift towards automation. Conversely, in Southern Europe, lower wages allow traditional hand-washing methods to thrive. WashTec's SmartCare Connect, unveiled in May 2025, harnesses machine learning to optimize brush pressure and chemical dosing [1]“SmartCare Connect Product Sheet,” WashTec, washtec.de. This innovation not only reduces wash cycles significantly but also improves water efficiency. Kärcher's TB redesign, also launched in May 2025, features eco! efficiency recirculation, a nod to fleet operators keen on meeting environmental standards. However, the financial hurdle remains significant: automatic tunnels require a much higher investment compared to manual bays. This disparity, especially in regions with limited equipment financing, hampers the shift towards automation. Meanwhile, innovation thrives, with Otto Christ's NOVA articulated brushes, recognized with the 2025 busplaner award, leading the charge in commercial-vehicle systems.

Stricter Water-Use Regulations Favoring Professional Washes

By 2030, the Urban Wastewater Treatment Directive 2024/3019 will tighten effluent standards, indirectly leading to higher municipal tariffs for at-home washing. In contrast, professional sites that invest in closed-loop systems and achieve high throughput stand to gain. Kärcher’s WRP biological plant significantly recycles process water, reducing freshwater usage and offering substantial cost savings for operators. In Germany and the Netherlands, water-recycling prerequisites are mandatory for new permits, effectively sidelining single-pass designs and directing volume to compliant chains. Many municipalities are now mirroring the EU Water Reuse Regulation 2020/741 as a guiding framework. Operators with deep pockets are reaping the most benefits, further tilting the competitive landscape in favor of chains over independent entities.

Rising Vehicle Ownership and Expanding Car Parc

Europe counted roughly 249 million passenger cars in 2023, the oldest fleet on record at 12.5 years, a dynamic that elevates maintenance spend on exterior cleaning to protect residual value [2]“The Vehicle Fleet in the EU 2023,” European Automobile Manufacturers Association, acea.be. Battery-electric vehicles, though still a minority, are prompting more frequent washes to maintain their aerodynamic range. Germany's automotive retail and repair turnover has grown, highlighting robust aftermarket activity closely tied to wash demand. To address the reduced spending power of older car owners, operators have introduced tiered pricing, steering budget-conscious consumers towards basic subscription plans. Seasonal trends are apparent as vehicle-repair activities in France typically lead to an uptick in wash visits during specific periods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Utility Costs Pressure Margins | -0.9% | Germany, Netherlands, Belgium; Spain, Portugal | Medium term (2-4 years) |

| CAPEX for Tunnel Systems | -0.7% | EU-wide; acute in Southern and Eastern Europe | Short term (≤ 2 years) |

| Urban Zoning Restricts New Sites | -0.4% | Major metros in Germany, France, United Kingdom | Long term (≥ 4 years) |

| Protection Films Reduce Frequency | -0.3% | Germany, United Kingdom, Nordics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Utility (Water and Energy) Costs Pressuring Margins

In H1 2025, non-household electricity prices varied significantly across regions, with some countries experiencing notably higher rates than others, resulting in an apparent margin disparity. In drought-affected areas like Spain and Portugal, water tariffs continue to rise steadily each year. While larger chains manage their exposure through strategies such as fixed-price power contracts or on-site solar solutions, independent businesses face challenges from fluctuating spot prices, which significantly impact profitability. Investing in advanced recycling platforms, such as those capable of reclaiming a substantial portion of process water, helps mitigate tariff-related pressures but requires a considerable initial investment.

High Upfront CAPEX for Tunnel Systems

Installing a tunnel requires significant investment in equipment and civil works. This substantial barrier fragments the European car wash market and extends the return on investment (ROI) period for independent operators. In 2024, Istobal introduced a leasing program that allows payments to be spread over an extended period. However, this program has seen a concentrated uptake in Germany and France, where access to credit is more liberal. In contrast, operators in the United Kingdom continue to depend on low-capex hand-wash models. These models, while cost-effective, are now under scrutiny due to evolving labor laws, highlighting the delicate balance between capital expenditure and labor considerations. Otto Christ’s modular EVO STAR offers the flexibility of staged brush additions, enabling operators to reduce their initial investment. Yet the demand for this innovation is predominantly limited to multi-site groups, which can effectively spread the costs of training and engineering across multiple locations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Operation: Automation Leads but Manual Bays Regain Momentum

Automatic formats delivered 61.25% of the European car wash market share in 2025, underscoring the scale advantage that tunnel throughput confers on the European car wash market. Manual bays, however, chart a 6.33% CAGR, beating overall growth as fleet customers and PPF-equipped premium cars require high-pressure touch-free cleaning. Otto Christ’s NOVA articulated brushes now serve bus and truck profiles once exclusive to manual stalls, while WashTec’s SmartCare Connect slashes cycle times under three minutes [3]“NOVA Commercial Vehicle Wash,” Otto Christ, christ-carwash.com. In Southern Europe, where labor is cheaper than Northern benchmarks, manual operations remain cost-effective and help preserve a fragmented landscape.

Automatic tunnels integrate seamlessly with subscription programs that demand 24/7 uptime, while manual sites attract price-sensitive users willing to trade speed for lower ticket prices. Equipment leaders are responding with hybrid models combining rollover and jet bays on a single footprint, blurring the lines between categories. Paint-protection-film constraints favor touchless options, while aging commercial fleets drive demand for oversized bays. As a result, the European car wash market size tied to manual formats could expand its slice despite automation’s headline share.

By Mode of Payment: Cash Dominates but Cashless Scales Fast

Cash closures still secured 66.14% of the European car wash market share in 2025, reflecting embedded consumer habits in Southern and Eastern Europe and retrofit inertia among site operators. Cashless volume, though smaller, grows at a 7.42% CAGR, outpacing every other payment mode in the European car wash market. Mobile apps reduce dwell time and enable preauthorizations, boosting average ticket size.

Germany and the United Kingdom already have a notable share of cashless transactions, fueling price differentiation through surge and off-peak promotions. The European Central Bank’s near-universal contactless infrastructure eases migration, but legacy wash-controller integrations delay adoption. Subscription programs inherently demand stored credentials, creating a virtuous cycle in which membership growth drives cashless usage. Southern Europe’s cash culture and limited smartphone penetration temper progress, making payment mode a key segmentation lens for Pan-EU strategies.

By Vehicle Type: Passenger Cars Rule as Commercial Fleets Accelerate

Passenger cars accounted for 71.26% of the European car wash market share in 2025, yet commercial vehicles expanded at a 5.87% CAGR, steadily increasing their share of the European car wash market. Euro 7 emissions rules push logistics fleets toward greater aerodynamic efficiency, while corporate ESG audits scrutinize water and chemical use, steering operators toward professional sites. Automation breakthroughs such as Kärcher’s TB and Otto Christ’s NOVA now enable high-roof vans and articulated lorries to be washed in under five minutes, eroding manual monopoly.

Passenger-car wash habits differ by segment: mass-market owners lengthen wash cycles as the fleet ages, whereas PPF-equipped premium cars shift to gentler, touch-free processes at lower frequency. Although small in share, battery-electric vehicles require frequent washing to maintain range, offering a niche upside. Dealer-integrated bays target passenger units during servicing but are increasingly expanding into light-commercial fleets, embedding wash activity within the OEM maintenance ecosystem.

By End-User: Consumers Dominate, Fleets Drive Incremental Growth

Individual customers accounted for 76.11% of the European car wash market share in 2025. Yet, fleet contracts posted an 8.13% CAGR through 2031, well above the European car wash market average, as logistics, rental, and corporate owners bundle washes into centralized service agreements. Fleet vehicles visit 24-36 times annually versus 6-10 for private cars, offsetting discounted prices through high volume.

Subscription plans pivot primarily to consumers but are now migrating to fleets through modules like Kärcher’s Charlie Fleet, delivering spend visibility and ESG reporting. Operators balance two value propositions: convenience and speed for households, compliance and cost for fleets. Chains with national footprints gain an edge as fleet buyers demand multi-site coverage, a trend that accelerates consolidation and undercuts single-site independents.

Geography Analysis

Germany accounts for 30.25% of 2025 revenue in the European car wash market, supported by a vast network of professional wash points and the region's highest per-capita frequency of car washes. However, elevated power tariffs are compressing margins, prompting operators to focus on upselling premium subscriptions to maintain profitability. WashTec leverages its domestic network to pilot IoT diagnostics before expanding across the EU, reinforcing Germany's leadership in technology.

In the United Kingdom, the car wash market is substantial, but hand washes dominate due to historically low labor costs and financing challenges that limit the adoption of tunnel washes. A recent acquisition by a United States investor has introduced institutional capital, accelerating refurbishment programs to improve operational efficiency and encouraging manual users to transition to subscription-based tunnel washes.

Spain reveals the fastest 6.74% CAGR through 2031, as operators leapfrog legacy cash systems and move directly to digital payments, with tunnel equipment manufactured domestically by Istobal. Water-scarce conditions and rising tariffs propel closed-loop investment, further professionalizing the landscape. In France, a leading equipment manufacturer has strengthened its local presence to meet the high service demands of national petrol retailers and hypermarkets. Nordic countries lead in cashless adoption, while Eastern Europe remains reliant on manual, cash-based systems due to economic constraints, reflecting the varied levels of maturity across the European car wash market.

Mordor Intelligence provides coverage of the car wash market across other key regional markets, including North America, Middle East, and Asia Pacific, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Fragmentation remains a hallmark of the market: the leading trio of OEMs—WashTec, Kärcher, and Istobal—account for a minority share of European sites. This opens the door for mid-tier regional builders and local independents to carve out a significant presence. WashTec recently unveiled its SmartCare Connect, a solution that integrates predictive maintenance with remote firmware updates. This innovation aims to minimize downtime, a move designed to prevent subscription churn, underscoring the growing importance of connectivity as a key service differentiator.

Otto Christ, with a significant operational scale and advanced manufacturing capabilities, adeptly fulfills the majority of its orders through an online configurator. This tool not only slashes lead times but also accommodates custom tunnel designs tailored for buses, trucks, and dealer retrofits. Meanwhile, Istobal, with a strong global presence, operates multiple subsidiaries and plants across several continents. This footprint allows for regional assembly, significantly reducing freight costs and expediting after-sales service. The trend is unmistakable: vendors are increasingly bundling hardware, chemicals, payment terminals, water recycling solutions, and cloud analytics. This strategy creates comprehensive ecosystems that effectively lock operators into their proprietary platforms.

Private-equity firms are signaling a potential roll-up cycle in the industry. Franchise Equity Partners' strategic move into IMO not only mirrors the consolidation trends seen in North America but also hints at a likely surge in competitive bidding for smaller chains. There are untapped opportunities in areas like dealer-integrated bays and app-driven loyalty programs, both of which stand to benefit from leveraging underutilized data. While mobile on-demand washing services pose a challenge to urban market share, they face hurdles in lowering unit costs. This limitation curtails their scalability, especially outside of densely populated metropolitan areas.

Europe Car Wash Industry Leaders

WashTec AG

Alfred Kärcher SE & Co. KG

Istobal S.A.

Otto Christ AG

Tammermatic Oy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Tommy’s Express launched its first French site in Allonne, offering a three-minute tunnel with water-reclamation technology.

- May 2025: Preen partnered with sector investors to deploy “T1 powered by Preen,” a United Kingdom network of premium touch-free tunnels starting in Ipswich.

- May 2025: WashTec introduced SmartCare Connect, integrating digital services with intelligent machines to position itself as a one-stop solutions provider.

- July 2024: Repsol Klin rolled out a monthly subscription offering daily washes across its Spanish network and up to 10% extra savings through Energy Plan linkage.

Europe Car Wash Market Report Scope

The scope includes segmentation by mode of operation (automatic and manual), mode of payment (cash and cashless), vehicle type (passenger and commercial), and end-user (individual consumers and fleet operators). The analysis also covers country-level segmentation, including Germany, the United Kingdom, France, Italy, Spain, and the rest of Europe. Market size and growth forecasts are presented by value in USD.

| Automatic |

| Manual |

| Cash |

| Cashless |

| Passenger Cars |

| Commercial Vehicles |

| Individual Consumers |

| Fleet Operators |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Mode of Operation | Automatic |

| Manual | |

| By Mode of Payment | Cash |

| Cashless | |

| By Vehicle Type | Passenger Cars |

| Commercial Vehicles | |

| By End-User | Individual Consumers |

| Fleet Operators | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe car wash market in 2026?

The sector generated USD 11.01 billion in 2026 and is projected to reach USD 14.12 billion by 2031.

What is the forecast CAGR for European car wash revenue?

Aggregate revenue is expected to advance at a 5.10% CAGR between 2026 and 2031.

Which country contributes the most value?

Germany leads with 30.25% of 2025 turnover thanks to the densest professional wash network in the region.

Which segment grows fastest by payment mode?

Cashless transactions rise at a 7.42% CAGR, the quickest among all payment channels.

Page last updated on: