Automotive Collision Repair Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

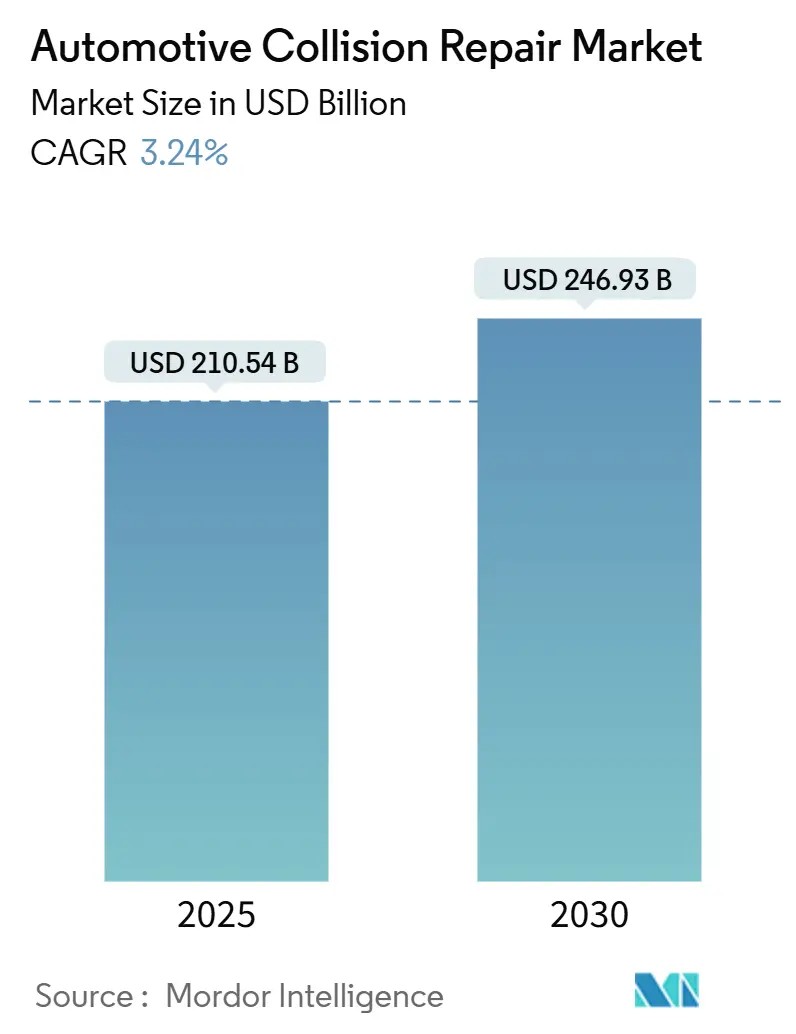

| Market Size (2025) | USD 210.54 Billion |

| Market Size (2030) | USD 246.93 Billion |

| Growth Rate (2025 - 2030) | 3.24% CAGR |

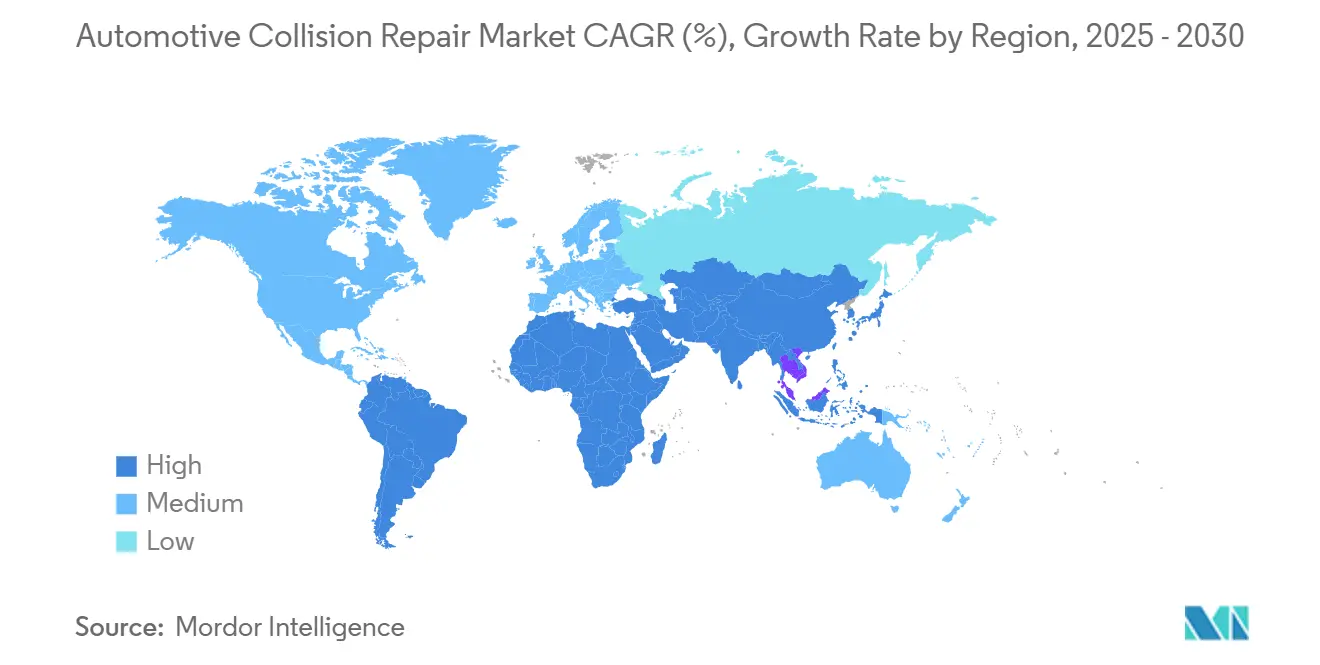

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Collision Repair Market Analysis by Mordor Intelligence

The automotive collision repair market reached USD 210.54 billion in 2025, and it is projected to expand to USD 246.93 billion by 2030 at a 3.24% CAGR. The automotive collision repair market size is underpinned by aging vehicle fleets that require more frequent interventions, the rapid spread of advanced driver-assistance systems (ADAS), and the rising penetration of electric vehicles that introduce new material combinations and repair protocols. While the segment historically relied on mechanical panel beating and repainting, it now revolves around sensor calibration, battery-safe structural work, and digital workflow integration. Technicians with ADAS and high-voltage credentials command premium wages, encouraging multi-site operators (MSOs) to consolidate for economies of scale. At the same time, tightening volatile organic compound (VOC) regulations and waste-management rules elevate compliance costs, producing barriers that favor larger, well-capitalized facilities. Insurers increasingly steer policyholders toward data-rich direct-repair programs, prompting shops to invest in automated parts procurement and real-time customer communication platforms to preserve volume.

Key Report Takeaways

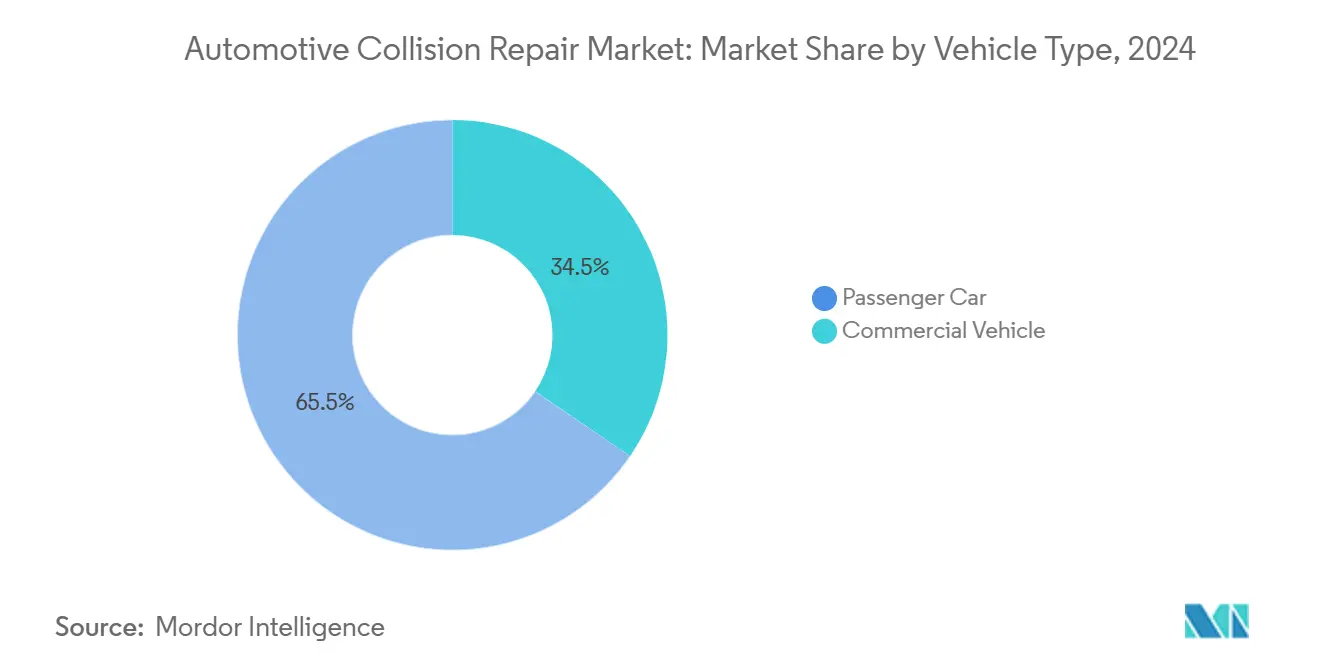

- By vehicle type, passenger cars led with 65.49% of the automotive collision repair market share in 2024, while commercial vehicles are poised to post a 6.95% CAGR to 2030.

- By product, paints and coatings accounted for 38.89% of the automotive collision repair market size in 2024; glass products are forecast to advance at a 7.08% CAGR through 2030.

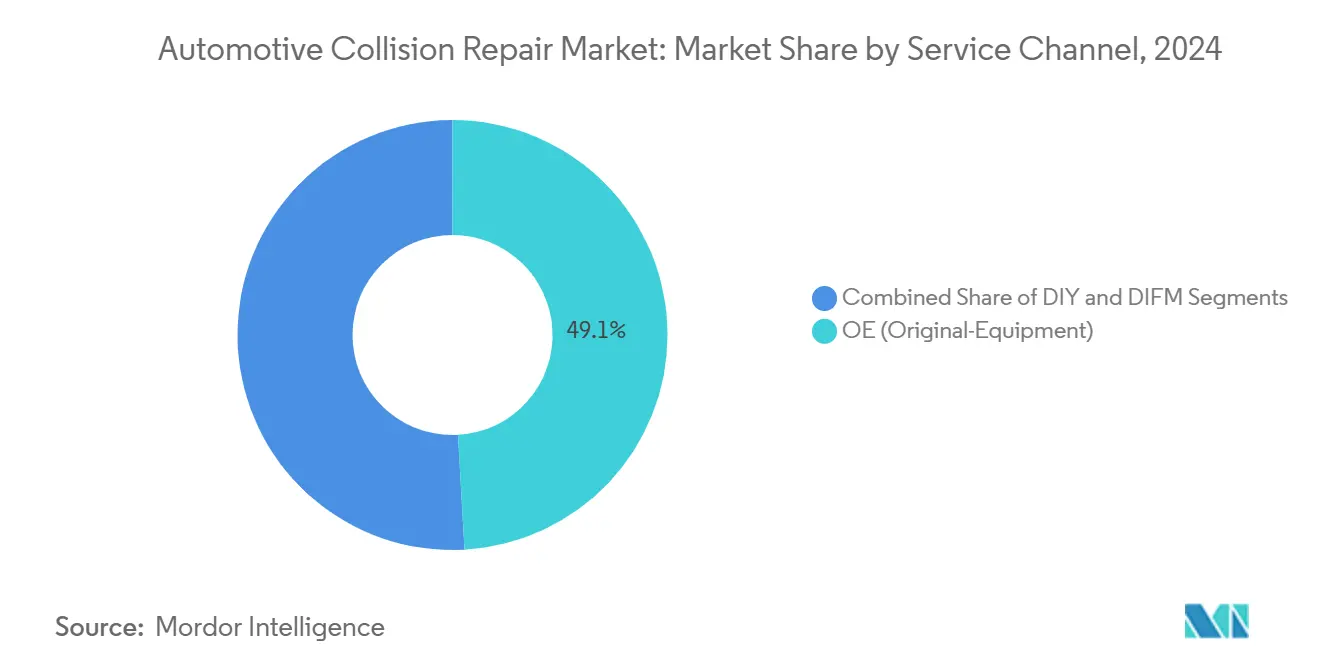

- By service channel, OE-certified outlets commanded 49.12% revenue in 2024, whereas do-it-for-me facilities will post the fastest 6.54% CAGR to 2030.

- By damage type, cosmetic and paint jobs represented 42.98% of repairs in 2024, but glass and ADAS calibration activities are projected to rise at a 9.41% CAGR over the same period.

- By geography, Europe held 32.75% of 2024 revenue, and Asia-Pacific is positioned to grow at a leading 7.67% CAGR to 2030.

Market Trends and Insights

Drivers Impact Analysis of Automotive Collision Repair Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADAS Sensor Calibration Demand | +1.8% | Global, with North America & Europe leading adoption | Medium term (2-4 years) |

| MSO Consolidation | +0.9% | North America core, expanding to Europe & APAC | Long term (≥ 4 years) |

| Specialized Repairing Demand | +0.7% | Global, concentrated in EV-adoption markets | Long term (≥ 4 years) |

| OEM-Certified Repair Networks | +0.6% | Asia-Pacific, Middle East, South America | Medium term (2-4 years) |

| Motor-Insurance Digital Claims | +0.5% | Global, with mature markets leading | Short term (≤ 2 years) |

| Vehicle Age and Accident Frequency | +0.4% | Global, particularly in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge In ADAS Sensor Calibration Demand

Mandatory recalibration following windshield or bumper work transforms collision repair into precision electronic service. Associations in Australia, Europe, and North America have published detailed calibration protocols, elevating equipment outlays and pushing shops toward certification programs[1]“ADAS Calibration Guidelines,” Australian Automotive Aftermarket Association, AAAA.COM.AU. ADAS work carries higher billable hours than traditional panel replacement, enabling facilities that master the procedures to lift margins. Parts manufacturers now pre-align camera brackets at the factory, but small fit variances still force in-shop verification, preserving service revenue. Supply constraints for multi-function calibration rigs occasionally delay job completion, reinforcing the value proposition of multi-bay MSOs that can share capital investments.

Private-Equity-Fuelled MSO Consolidation

Financial sponsors favor the automotive collision repair market for its nondiscretionary demand and fragmented ownership. Combining sites unlocks scale in paint procurement, labor scheduling, and claims data integration. Consolidators roll out centralized training academies that accelerate technician upskilling, mitigating labor shortages. Integrated management systems track key performance indicators in real time, shortening cycle times and improving insurer satisfaction. As multiples for single-site shops soften, acquisition pipelines remain robust, with owners aging out of the business and preferring cash exits over technology catch-up investments.

Lightweight EV Materials Requiring Specialized Repair

Battery-electric vehicles use aluminum, carbon fiber, and engineered thermoplastics that differ from steel in energy absorption and heat tolerance. The American Chemistry Council notes that adhesive bonding and rivet-bond hybrids replace traditional MIG welding on many models, compelling technicians to earn manufacturer-specific qualifications[2]“Advanced Materials Drive Electric Vehicle Innovation,” American Chemistry Council, AMERICANCHEMISTRY.COM. Faulty repairs risk galvanic corrosion or battery-pack heat transfer issues, raising liability. Repairers purchase new extraction systems to avoid airborne conductive dust and apply insulated tooling protocols. Early adopters market EV-ready credentials to fleets seeking to minimize downtime, capturing a profitable niche.

Expansion of OEM-certified Networks in Emerging Markets

Automakers view certification schemes as brand-protection tools and aftermarket revenue sources. Participation requires equipment purchases, annual audits, and use of genuine parts, creating de facto exclusivity. In Indonesia and the Gulf, dealership-attached body shops are expanding satellite locations to meet brand coverage targets. Certification signage reassures insurers of repair fidelity, channeling high-severity jobs toward approved sites. Yet rigorous standards raise breakeven thresholds, nudging unaligned independents toward parts and cosmetic niches instead of full-frame work.

Restraints Impact Analysis of Automotive Collision Repair Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Collision Technicians | -0.8% | Global, acute in developed markets | Long term (≥ 4 years) |

| VOC and Waste-Disposal Regulations | -0.6% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Declining Collision Rates | -0.4% | Developed markets with high ADAS penetration | Long term (≥ 4 years) |

| "Total-Loss" Design Economics | -0.3% | Global, varying by OEM strategy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Global Shortage of Certified Collision Technicians

Baby-boomer retirements and a perception of the trade as low-tech dampen enrollment in vocational programs. The National Institute for Automotive Service Excellence reported falling exam registrations in 2024 despite higher pay scales[3]“Certification Trends 2024,” National Institute for Automotive Service Excellence, ASE.COM. Shops jostle for talent through sign-on bonuses and tuition reimbursement, yet ADAS and EV skillsets demand additional classroom hours many candidates shy from. Labor scarcity lengthens cycle times, which frustrates insurers and drives work to networks with in-house academies. Automation is limited to paint mixing or parts logistics; hands-on panel and electrical work still require skilled humans.

Stringent VOC and Waste-disposal Regulations on Coatings

The U.S. Environmental Protection Agency enforces National Emission Standards for Hazardous Air Pollutants rules that mandate low-VOC formulations, specialized filtration, and cradle-to-grave solvent tracking[4]“Collision Repair—NESHAP Requirements,” Environmental Protection Agency, EPA.GOV. Waterborne paints improve compliance but require booth humidity control retrofits that cost significantly. Smaller independents struggle to recover that expense, accelerating consolidation. Inspectors in California and Germany fine noncompliant facilities heavily, incentivizing facilities to upgrade or outsource painting.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Automotive Collision Repair Market Segment Analysis

By Vehicle Type:

Commercial Fleets Drive ElectrificationPassenger cars led the automotive collision repair market holding 65.49% share in 2024, while commercial vehicles are projected to post a 6.95% CAGR through 2030 holding a smaller share than passenger cars. Commercial operators run data-driven replacement schedules and adopt electric vans faster because route predictability suits fixed charging patterns. For shops, fleet contracts guarantee repeat volume but require rapid turnaround and EV training. The automotive collision repair market size for the commercial segment will keep expanding as parcel and grocery delivery proliferate in urban centers. Fleet insurers insist on ADAS functionality checks after every structural repair, adding calibration revenue. Passenger cars remain the core of the automotive collision repair market, yet growth tempers as ADAS reduces minor impact frequency.

The automotive collision repair market’s commercial niche benefits from OEM telematics that immediately flag fault codes after a collision, allowing pre-repair parts ordering. Shops able to ingest over-the-air diagnostics lock in preferred-vendor status. Light-duty vans increasingly feature single-piece castings that are non-sectionable, steering severe damage toward full body replacement or total loss. Nevertheless, tire and wheel incidents keep routine work flowing. Medium-duty trucks still use repair-friendly ladder frames, providing steady structural business for facilities equipped with heavy pulling systems.

By Product:

Glass Segment Capitalizes on Sensor IntegrationPaints and coatings retained the dominant 38.89% slice of the 2024 automotive collision repair market size, yet glass products are forecast for a 7.08% CAGR as cameras, LiDAR windows, and heads-up displays migrate into windshields. ADAS calibration lifts average glass invoice values significantly, and insurers increasingly bundle glass and calibration approvals in a single claim, easing upsell conversations. Automotive collision repair market share shifts toward glazing suppliers that embed calibration targets directly into replacement panels to streamline set-ups.

Structural adhesives, seam sealers, and plastic repair sticks post mid-single-digit growth in tandem with multi-material bodies. Coating innovators push ultra-high-solid clears below 250 grams per liter VOC to stay ahead of regulation. However, glass garners the spotlight with acoustic laminated sidelites, solar-attenuating mid-laminates, and hydrophobic coatings. Circular-economy pilots recycle shattered windshields into glass-wool insulation, burnishing sustainability credentials.

By Service Channel:

OE Networks Maintain DominanceOE-certified centers preserved 49.12% of 2024 revenue by leveraging proprietary repair data, parts supply guarantees, and consumer trust in brand alignment. Insurers favor these outlets for high-value vehicles where repair integrity reduces liability. The do-it-for-me surge at 6.54% CAGR underscores consumer willingness to pay for convenience as vehicle systems surpass DIY skillsets. While the collision-only specialty shop remains viable, combined mechanical and body franchises win share through one-stop service.

The automotive collision repair market rewards OE participants with program rebates on bulk parts purchases, offsetting higher overhead. Network standards demand continuous technician education, benefiting customers with consistent quality. Independent fixed-site shops adapt by specializing in cosmetic quick-turn work or vintage model restoration, niches less reliant on factory scan tools. Mobile glass and paintless dent repair operators capture selective jobs but defer structural and electronic tasks to brick-and-mortar peers.

By Damage Type:

ADAS Calibration Commands Premium PricingCosmetic and paint jobs made up 42.98% of 2024 volume, yet glass and sensor calibration lines are rising at 9.41% CAGR, demonstrating the pivot from labor-intensive sanding toward data-centric diagnostics. The automotive collision repair market size generated by calibration already exceeds many traditional sub-segments and will multiply as Level-2+ autonomy spreads. Automotive collision repair market share gains tilt toward shops with ISO-validated calibration bays and brand-licensed tooling.

Structural aluminum fixes remain significant because EVs use larger castings that complicate sectional replacement. Carbon-fiber panels on premium models require vacuum-assisted resin bonding, another revenue-rich specialty. Interior electronic damage from airbag deployment creates secondary work streams in seatbelt pre-tensioner replacement and console wiring. The convergence of electronics and bodywork blurs historic trade divisions, favoring cross-trained technicians.

Geography Analysis

Germany and United Kingdom Automotive Collision Repair Market

Europe accounted for 32.75% of the automotive collision repair market in 2024 and is projected to register a modest 3.6% CAGR through 2030 as collision frequency trends downward. Strict type-approval laws obligate calibration after even minor structural work, elevating procedure counts and partially offsetting volume declines. Regulatory emphasis on low-VOC paints incentivizes early adoption of waterborne systems and infrared curing. Germany’s deep OEM supply chain eases access to genuine parts, whereas southern markets confront lengthier lead times that stretch cycle durations. Brexit-related customs checks continue to complicate U.K. parts flow, prompting distributors to expand continental warehouses to buffer shocks.

APAC Automotive Collision Repair Market

Asia-Pacific is the fastest-growing geography, expanding at a 7.67% CAGR. China’s rising electric-vehicle share adds complexity for independent repairers, who must invest heavily in battery isolation tools and fire-suppression facilities. India shows double-digit volume growth based on new-car sales and an aging low-end fleet still prone to mechanical failures. Japan’s advanced semiconductor content sets high calibration benchmarks, and its insurers are early to reimburse post-collision health checks for LiDAR sensors. Government-run vocational schools in Thailand and Vietnam collaborate with automakers to certify technicians, narrowing the skills gap.

North America and Mexico Automotive Collision Repair Market

North America delivers a steady 4.2% CAGR, fueled by MSO capital expenditures in ADAS bays and unified estimating platforms. U.S. carriers extend photo-estimate use, steering vehicles into aligned networks within hours of a claim. Canadian shops benefit from exchange-rate-driven parts arbitrage but face harsher winter damage profiles that raise glass and alignment revenue. Mexico sees growing interest from European OEMs that want certified networks near assembly plants to protect brand residual values; however, differences in regulatory oversight create accreditation challenges.

Mordor Intelligence provides coverage of the automotive collision repair market across other key regional markets, including North America, Europe, and Asia, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The automotive collision repair market exhibits fragmented characteristics, creating consolidation opportunities as scale advantages become increasingly crucial for technology deployment and operational efficiency. Parts distributor-repair hybrid LKQ Corporation exploits vertical integration to shorten parts lead times. Caliber Collision follows, leveraging proprietary workflow software that automates technician dispatch to balance bay utilization. Paint manufacturers PPG Industries, BASF, and Axalta compete via color-matching algorithms and low-VOC clearcoats that comply with the strictest jurisdictions.

Competitive priorities revolve around ADAS calibration capacity, EV battery isolation readiness, and real-time communication platforms. Early movers deploy cloud-based inventory systems that pair VIN decoding with live parts availability, reducing supplements. Intellectual property filings around sensor mapping and dynamic calibration are accelerating, underscoring a shift from pure mechanical craft toward software-anchored differentiation. Strategic alliances among coatings suppliers and workflow-platform developers aim to embed formulation data directly into repair planning, slashing prep time.

Private equity activity surges as investors chase roll-up synergies; well-run MSOs unlock purchasing clout that trims paint and parts cost of goods by 4-6 points. Smaller independents either join franchise banners for supply discounts or double-down on hyper-local relationships. EV-only repair franchises begin to appear in megacities, advertising factory-approved battery safing and non-intrusive dent removal. Meanwhile, insurers quietly pilot performance-based reimbursement that rewards shops meeting cycle-time and scan-report thresholds, reinforcing the benefits of data-rich operators.

Automotive Collision Repair Industry Leaders

LKQ Corporation

Caliber Collision

PPG Industries

BASF SE

Axalta Coating Systems

- *Disclaimer: Major Players sorted in no particular order

Automotive Collision Repair Market Companies Covered in this Report

- Caliber Collision

- Boyd Group/Gerber Collision & Glass

- Crash Champions

- Classic Collision

- Joe Hudson’s Collision Centers

- CollisionRight

- CARSTAR

- Maaco

- Fix Network

- Belron

- Steer Automotive Group

- Solus Accident Repair Centres

- AMA Group

- AutoNation Collision Centers

- LKQ Corporation

- PPG Industries

- BASF Coatings

- Axalta Coating Systems

- AkzoNobel

- 3M Automotive Aftermarket Division

Recent Industry Developments in Automotive Collision Repair Market

- June 2025: BASF Coatings and Toyota Motor Europe finalized a multi-year agreement to develop Body & Paint programs for Toyota and Lexus in Europe.

- May 2025: Kinetic collaborated with Chilton Auto Body to launch a digital repair hub serving the San Francisco Bay Area.

- May 2025: PPG introduced the DELTRON NXT DC7020 Premium Glamour Speed Clearcoat for high-volume collision centers in the United States.

Global Automotive Collision Repair Market Report Scope

Segmentation Overview

| Passenger Car |

| Commercial Vehicle |

| Paints and Coatings |

| Consumables |

| Spare Parts |

| Glass |

| Other Product |

| DIY |

| DIFM |

| OE |

| Structural Repair |

| Cosmetic and Paint |

| Glass and ADAS Calibration |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Car | |

| Commercial Vehicle | ||

| By Product | Paints and Coatings | |

| Consumables | ||

| Spare Parts | ||

| Glass | ||

| Other Product | ||

| By Service Channel | DIY | |

| DIFM | ||

| OE | ||

| By Damage Type | Structural Repair | |

| Cosmetic and Paint | ||

| Glass and ADAS Calibration | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the global revenue of the automotive collision repair market in 2025?

The automotive collision repair market generated USD 210.54 billion in 2025, supported by aging vehicles and more complex repair requirements.

How fast is the automotive collision repair market expected to grow through 2030?

It is forecast to record a 3.24% CAGR, reaching USD 246.93 billion by the decade’s end.

Which region will post the quickest growth?

Asia-Pacific leads with a projected 7.67% CAGR thanks to rising car ownership and growing EV penetration.

Why is ADAS sensor calibration important for body shops?

Windshield or bumper repairs disturb cameras and radar; mandatory recalibration adds high-margin revenue and requires specialized equipment.

How are environmental regulations affecting repair facilities?

Low-VOC rules and solvent-waste tracking force investment in compliant paint booths and filtration, raising operating costs but improving air quality.

What skills gap challenges the industry today?

A shortage of certified technicians, especially in ADAS and EV specialties, lengthens repair cycle time and elevates labor rates.

Page last updated on: