Asia Pacific Automotive Collision Repair Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

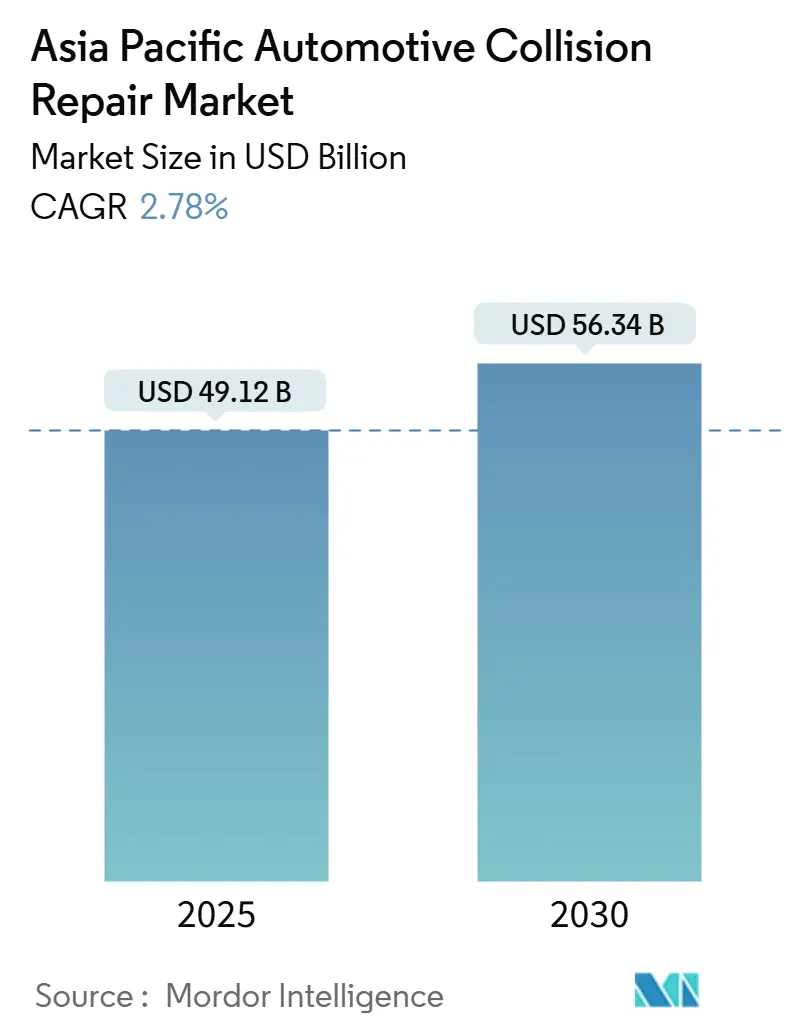

| Market Size (2025) | USD 49.12 Billion |

| Market Size (2030) | USD 56.34 Billion |

| Growth Rate (2025 - 2030) | 2.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Automotive Collision Repair Market Analysis by Mordor Intelligence

The Asia Pacific automotive collision repair market size is valued at USD 49.12 billion in 2025 and is forecast to reach USD 56.34 billion by 2030, advancing at a 2.78% CAGR during the forecast period. This growth reflects the shift from volume‐driven business to higher-margin, technology-intensive services such as advanced driver assistance systems (ADAS) calibration and electronic diagnostics. Repair complexity now offsets the decline in accident frequency accompanying improved vehicle safety technologies. Paints and coatings remain the leading product category, but glass repair and calibration services are expanding fastest as integrated cameras and sensors push up ticket values. China preserves scale leadership thanks to its vast vehicle parc and strict environmental mandates, while India records the highest growth as personal mobility and aftermarket spending accelerate. Competitive advantage increasingly hinges on digital diagnostic capabilities, technician certification, and regulatory compliance.

Key Report Takeaways

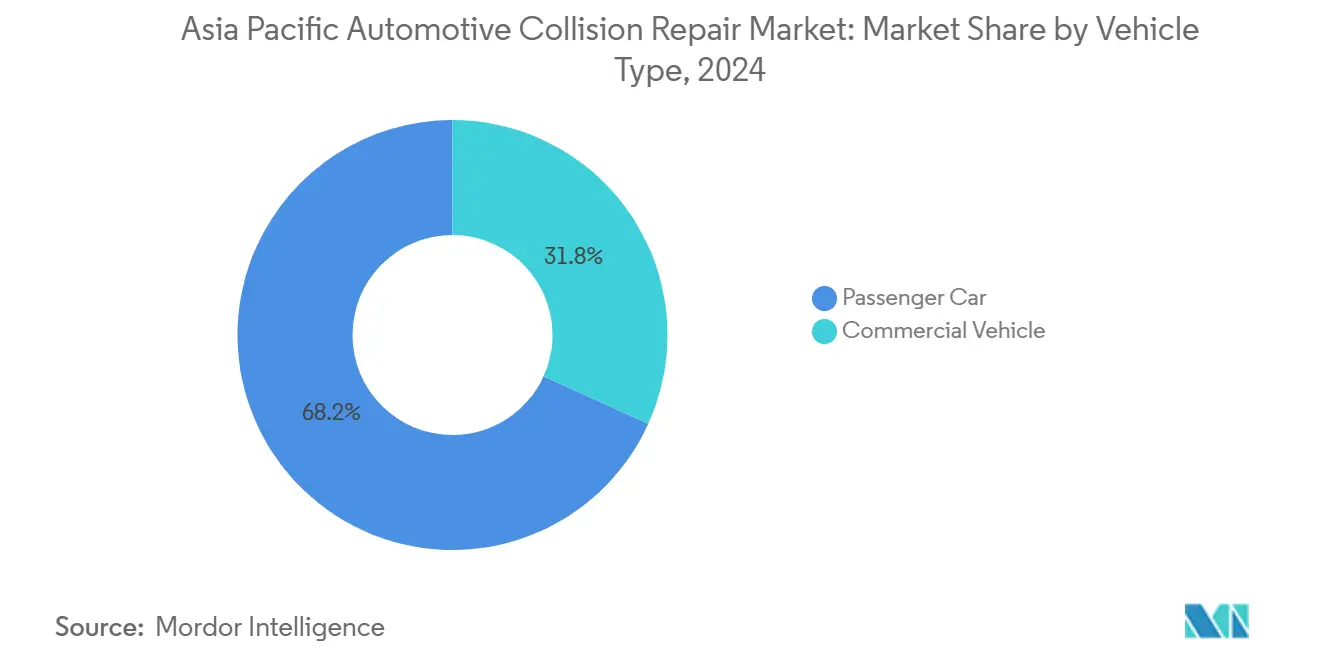

- By vehicle type, passenger cars accounted for 68.22% share of the Asia Pacific automotive collision repair market size in 2024, and commercial vehicles are advancing at a 3.32% CAGR through 2030.

- By product, paints and coatings led the Asia Pacific automotive collision repair market with 45.41% of the share in 2024, while glass is projected to expand at a 3.98% CAGR through 2030.

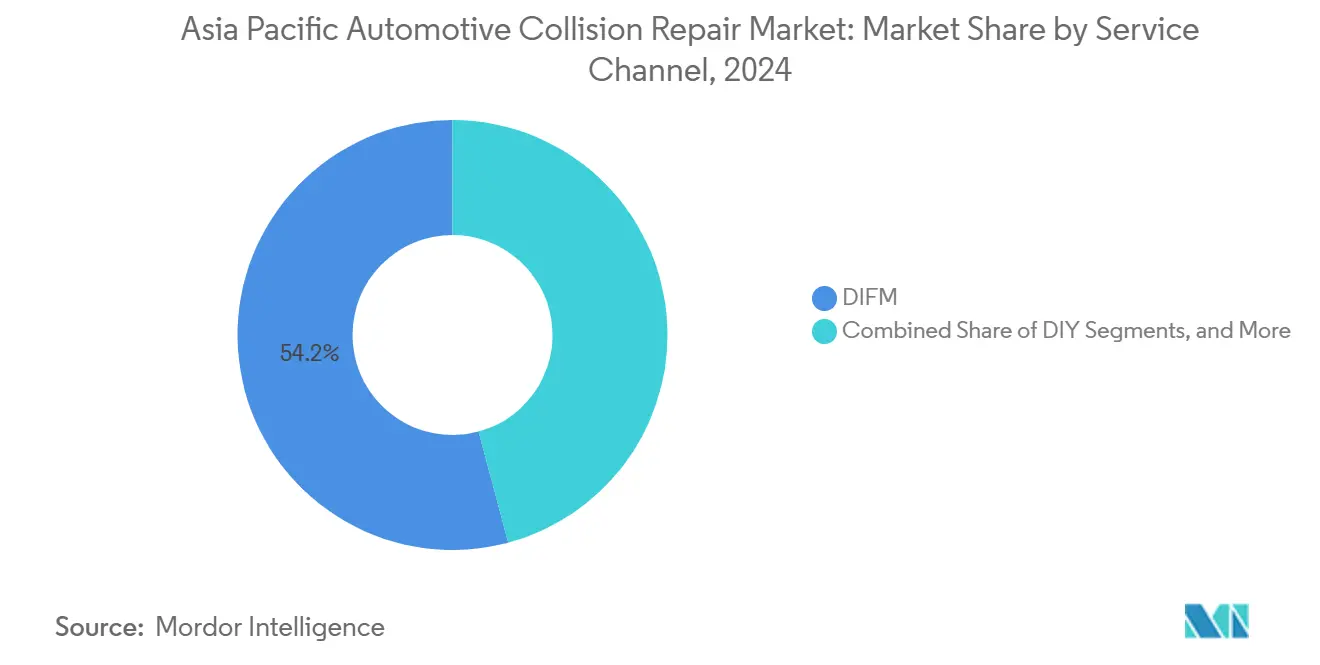

- By service channel, the DIFM segment held 54.18% of the Asia Pacific automotive collision repair market share in 2024, whereas OE networks record the highest projected CAGR at 3.83% to 2030.

- By damage type, cosmetic and paint repairs dominated with a 56.92% share of the Asia Pacific automotive collision repair market size in 2024, while glass and ADAS calibration services are forecast to grow at a 4.74% CAGR to 2030.

- By country, China commanded a 48.28% share of the Asia Pacific automotive collision repair market in 2024, whereas India is set to post the fastest 4.84% CAGR over the forecast period.

Global valuation is built by aggregating outputs from multiple regions, with Asia forming one of the important contributors. Mordor Intelligence's global automotive collision repair market size report represents that cumulative total.

Asia Pacific Automotive Collision Repair Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ADAS Calibration Demand Rising Rapidly | +0.7% | Japan, South Korea, Australia | Short term (≤ 2 years) |

| Growing Vehicle Parc and Accident Rates | +0.6% | India, Indonesia, Southeast Asia | Long term (≥ 4 years) |

| Shift to Water-Borne and Low-VOC Coatings (Regulatory) | +0.5% | China, Japan, South Korea | Short term (≤ 2 years) |

| Cosmetic Repairs Driven by Rising Incomes | +0.4% | India, Indonesia, Vietnam | Medium term (2-4 years) |

| Insurance-Backed Repair Franchise Expansion | +0.3% | China, Indonesia, Thailand | Medium term (2-4 years) |

| Sustainability Push for Recycled Polymer Parts | +0.2% | Japan, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of ADAS Calibration Demand Post-Collision

Modern windshields, bumpers, and grilles house cameras and radar that need recalibration after every repair. Static calibration rigs with target boards and dynamic road-test procedures elevate job complexity and price points. South Korea’s “minor damage repair standards” specify repair parameters for ADAS-equipped vehicles to sustain sensor performance. Bosch’s DAS 3000 rig offers multi-brand compatibility and laser alignment, illustrating capital barriers for small shops [1]“DAS 3000 Calibration Solution,”, Bosch Diagnostics, boschdiagnostics.com. Limited capacity enables early adopters to command premium rates and lock in dealer partnerships across the Asia Pacific automotive collision repair market.

Growing Vehicle Parc and Accident Rates

India’s vehicle population is expected to climb from 333 million units to 430-435 million by 2030, a 29% increase that sustains repair demand as older vehicles need more frequent attention[2]“Indian Auto Components Aftermarket Outlook 2025,”, India Brand Equity Foundation, ibef.org. Indonesia’s status as Southeast Asia’s largest car market amplifies the trend, with local manufacturing hubs spawning dense service networks. Rapid urbanization raises vehicle utilization and accident exposure, especially in congested megacities. An expanding two-wheeler base adds volume for body-panel and paint refinish work. These dynamics underpin steady throughput at collision centers even as safety technology improves.

Regulatory Shift to Water-Borne and Low-VOC Coatings

China’s Three-year Environmental Protection Plan enforces volatile-organic-compound (VOC) caps, forcing Shanghai, Shenzhen, and Tianjin repairers to switch entirely to water-borne coatings. Similar directives in Japan and South Korea accelerate the adoption of low-VOC formulations. Compliance raises material costs but allows shops to charge green premiums and attract OEM-approved business. Established suppliers with advanced chemistries gain share, while small independents struggle with spray-booth retrofits and skills training. The regulation, therefore, re-orders supplier power and speeds technology migration across the Asia Pacific automotive collision repair market.

Expansion of Insurance-Backed Repair Franchise Networks

Insurers integrate downstream to cut claims outlays and control quality. Sompo Holdings opened the AUTOGLAD facility near Jakarta, which has a capacity of 400 cars per month, embedding Japanese process controls in a local franchise model[3]“AUTOGLAD Body Repair Center Launch,”, Sompo Holdings, sompo-hd.com. Such alliances promise faster approvals, standardized parts sourcing, and digital estimation platforms that shrink cycle time. Customers receive warranty-backed workmanship, while insurers secure predictable cost structures. Franchise proliferation pressures stand-alone workshops unless they join networks or upgrade capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Improved Safety Systems Reducing Collision Volume | -0.9% | Japan, South Korea, Australia | Medium term (2-4 years) |

| High VOC and Environmental Compliance Costs | -0.8% | China, Japan, South Korea | Short term (≤ 2 years) |

| Shortage of Skilled Technicians for ADAS and Multi-Material Repairs | -0.6% | Australia, Japan | Long term (≥ 4 years) |

| Electronic Parts Shortages Causing Repair Delays | -0.5% | Australia, remote APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Improved Vehicle Safety Systems Reducing Collision Frequency

Regions such as Australia, Europe, and China are witnessing a notable decline in rear-end collisions, thanks to the implementation of Autonomous Emergency Braking (AEB) systems. AEB technology, which automatically applies brakes to prevent or mitigate collisions, has become a critical feature in modern vehicles, enhancing road safety. With fewer minor accidents, traditional body shops are seeing a reduced demand for panel repairs. In response, these shops are pivoting towards electronics-centric services, such as sensor calibration and diagnostics, striving to sustain revenue in an increasingly safety-conscious market.

Electronic Parts Shortages Delaying Repair Turnaround

Due to ongoing semiconductor shortages, access to crucial components such as sensors and control modules has been delayed. These shortages have disrupted the supply chain, causing significant bottlenecks in the availability of essential parts. As a result, some vehicle repairs are left waiting for months. These prolonged delays have led insurers to declare total losses on vehicles that might have been repairable. This diminishes revenue for workshops and hampers the market's overall growth, as prolonged repair times impact customer satisfaction and operational efficiency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Service Premiumization

Passenger cars still hold 68.22% of the Asia Pacific automotive collision repair market size in 2024, and commercial vehicles are set to expand at a 3.32% CAGR through 2030. Fleet operators budget for preventive maintenance and prefer certified centers to safeguard uptime and regulatory compliance. High-mileage duty cycles accelerate wear on bumpers, lighting, and telematics hardware, translating to larger invoices. At the same time, ride-hailing businesses outsource accident repairs to multi-shop operators, adding predictable workstreams and introducing OEM telematics data into scheduling algorithms.

Fleet electrification adds complexity. Battery enclosures demand structurally sound benches and insulated tools. Thailand sees rising electric light-truck registrations, requiring collision centers to invest in isolation kits and fire-suppression protocols. Such capital intensiveness tilts shares toward chains with manufacturer or insurer backing, reinforcing consolidation in the Asia Pacific automotive collision repair market.

By Product: Glass Segment Accelerates Through ADAS Integration

Paints and coatings held 45.41% of the Asia Pacific automotive collision repair market size in 2024, underlining their ubiquity for scratch and dent restoration. Yet glass services lead in growth at 3.98% CAGR through 2030 because windshields now house lane-keep cameras and rain sensors. Complete glass replacement often triggers static and dynamic calibration, adding USD 200-USD 400 labor premiums and specialized target kits.

Consumables, including adhesives and masking films, scale indirectly with paint jobs. Low-VOC thinners and fast-dry clearcoats gain popularity amid stricter booth emissions limits. Spare mechanical parts show muted expansion as OEM engineering lengthens component lifecycles, but recycled plastic bumper skins gain traction under circular-economy pledges by assemblers.

By Service Channel: OE Networks Expand Market Reach

DIFM commanded 54.18% of the Asia Pacific automotive collision repair market size in 2024, illustrating the continued preference for professional service as vehicle systems grow more intricate. Original-equipment (OE) networks post the fastest 3.83% CAGR through 2030 because automakers realize the lifetime value in parts and data analytics. Dealer-affiliated shops capture warranty work and leverage telematics alerts for predictive offers. 3M’s RepairStack platform automates parts ordering and blueprinting, giving OE facilities real-time visibility on cost of goods sold. Independent DIY activity diminishes, limited to minor touch-ups, as proprietary software locks consumers out of diagnostic menus.

By Damage Type: ADAS Calibration Commands Premium Pricing

Cosmetic and paint work holds 56.92% of the Asia Pacific automotive collision repair market size in 2024. Conversely, glass and ADAS calibration lines are forecast to advance at a 4.74% CAGR to 2030, reflecting their labor intensity and liability stakes. Regulatory clauses in Japan require proof-of-calibration certificates for continued roadworthiness, reinforcing the need for specialized rigs. Structural repairs on multi-material chassis also call for induction welders and rivet guns, but see slower growth because crash-energy management designs minimize severe deformation.

Geography Analysis

China retained 48.28% of the Asia Pacific automotive collision repair market share in 2024. Strict VOC directives encourage water-borne coating investments that lift ticket margins, while huge BEV sales inject high-voltage repair demand. PPG’s investment in the battery-pack coating center exemplifies the supplier's commitment to evolving OEM platforms.

India delivers the region’s highest 4.84% CAGR through 2030, underpinned by a fast-expanding vehicle parc and an aftermarket poised to grow by 2026. Used-car sales, scrappage incentives, and higher safety-rating awareness funnel cars into paint and parts replacement lines. Japan and South Korea show modest growth but host the most advanced ADAS penetration and rigorous repair specs. Korea’s guidelines for repairing rather than replacing plastic bumpers on sensor-equipped cars preserve sustainability while controlling costs.

Australia faces skilled-labor shortages that impede capacity expansion. Southeast Asian nations such as Indonesia enjoy insurer-driven consolidation, exemplified by Sompo’s AUTOGLAD rollout, which signals a shift toward franchise formats and centralized parts procurement.

Coverage of the automotive collision repair market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for North America and Europe.

Competitive Landscape

The Asia Pacific automotive collision repair market is moderately fragmented. Top global coatings suppliers (BASF, PPG, Axalta), diagnostic giants (Bosch, Snap-on), and insurer-backed franchises compete with thousands of independents. Capital requirements for ADAS rigs, low-VOC spray booths, and technician training tilt share toward large chains and OE-affiliated workshops. BASF’s “Sustainability Future Target Picture” aligns refinish offerings with circular-economy goals, giving it a tender advantage in environmentally sensitive municipalities.

Technology integration defines winners. Shops deploying inventory automation, AI-based estimating, and remote diagnostic platforms cut cycle times by up to 20% and lower parts obsolescence. Insurance partnerships deliver guaranteed volumes in exchange for fixed pricing structures.

White-space opportunities lie in recycled-parts brokerage, mobile calibration vans, and EV battery-case refurbishment. Midsize players form buying groups to secure sensor modules amid global shortages. Talent scarcity remains the chief bottleneck, with apprenticeship programs and e-learning portals emerging as retention tools.

Asia Pacific Automotive Collision Repair Industry Leaders

PPG Industries Inc.

3M Company

Axalta Coating Systems LLC

Robert Bosch GmbH

Denso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BASF Coatings introduced its Sustainability Future Target Picture at refinish sites throughout the Asia Pacific, embedding circular-economy metrics into its product roadmaps. This initiative aims to align with the company's broader sustainability goals by promoting resource efficiency, reducing environmental impact, and fostering innovation in sustainable coatings solutions.

- August 2024: Bosch Diagnostics unveiled its ADS X V6.0 firmware, boasting quicker scans for Asian brands and a broader range of ADAS features. The latest update enhances coverage for model year 2024 and introduces over 2,000 new special tests and system applications for ADAS calibrations.

Asia Pacific Automotive Collision Repair Market Report Scope

| Passenger Car |

| Commercial Vehicle |

| Paints & Coatings |

| Consumables |

| Spare Parts |

| Glass |

| Other Product |

| Do-It-Yourself (DIY) |

| Do-It-For-Me (DIFM) |

| Original Equipment (OE) |

| Structural Repair |

| Cosmetic and Paint |

| Glass and ADAS Calibration |

| India |

| China |

| Japan |

| South Korea |

| Rest of Asia Pacific |

| By Vehicle Type | Passenger Car |

| Commercial Vehicle | |

| By Product | Paints & Coatings |

| Consumables | |

| Spare Parts | |

| Glass | |

| Other Product | |

| By Service Channel | Do-It-Yourself (DIY) |

| Do-It-For-Me (DIFM) | |

| Original Equipment (OE) | |

| By Damage Type | Structural Repair |

| Cosmetic and Paint | |

| Glass and ADAS Calibration | |

| By Country | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific |

Key Questions Answered in the Report

What is the current value of the Asia Pacific automotive collision repair market?

It is valued at USD 49.12 billion in 2025.

How fast is the market expected to grow?

The forecast CAGR is 2.78% through 2030.

Which product segment is expanding the quickest?

Glass repair and ADAS calibration services are projected to grow at 3.98% CAGR.

Why are OE repair networks gaining traction?

Automakers seek to capture aftermarket revenue and ensure quality by expanding authorized facilities equipped for ADAS and EV repairs.

What is the main challenge facing repair shops?

A shortage of technicians certified for multi-material and electric-vehicle repairs is limiting capacity.

Page last updated on: