Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

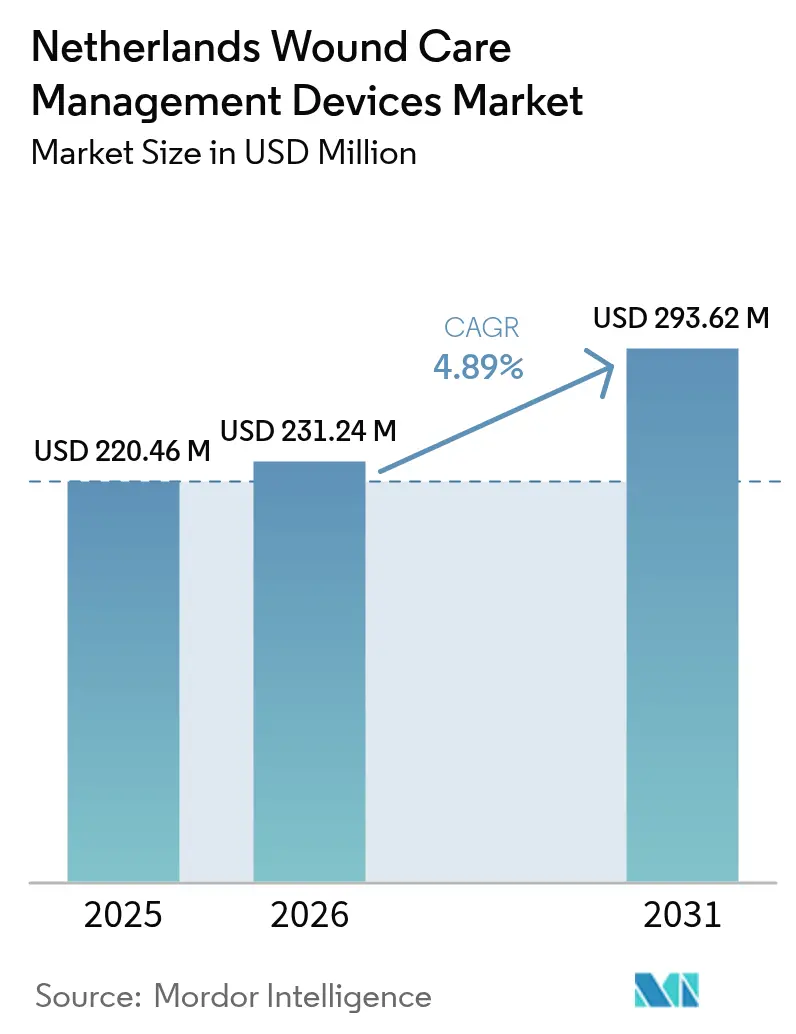

| Base Year Market Size (2025) | USD 220.46 Million |

| Market Size (2026) | USD 231.24 Million |

| Market Size (2031) | USD 293.62 Million |

| Growth Rate (2026 - 2031) | 4.89% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Netherlands Wound Care Management Devices Market Analysis by Mordor Intelligence

The Netherlands wound care management devices market size was valued at USD 220.46 million in 2025 and estimated to grow from USD 231.24 million in 2026 to reach USD 293.62 million by 2031, at a CAGR of 4.89% during the forecast period (2026-2031). Demand growth is fueled by a rising elderly population, wider use of negative-pressure and sensor-enabled therapies, and the national Fast-Track protocol that has compressed specialist referral times and redirected resources toward higher-value technologies. Hospitals are moving from volume-based purchasing to outcome-focused procurement, prompting manufacturers to emphasize total cost-of-care propositions rather than product features. Retail channels are gaining traction as self-management products and e-commerce platforms make professional-grade dressings accessible to patients. Sustainability mandates, especially restrictions on single-use plastics, are accelerating innovation in bio-based materials and encouraging circular business models for devices and packaging.

Key Report Takeaways

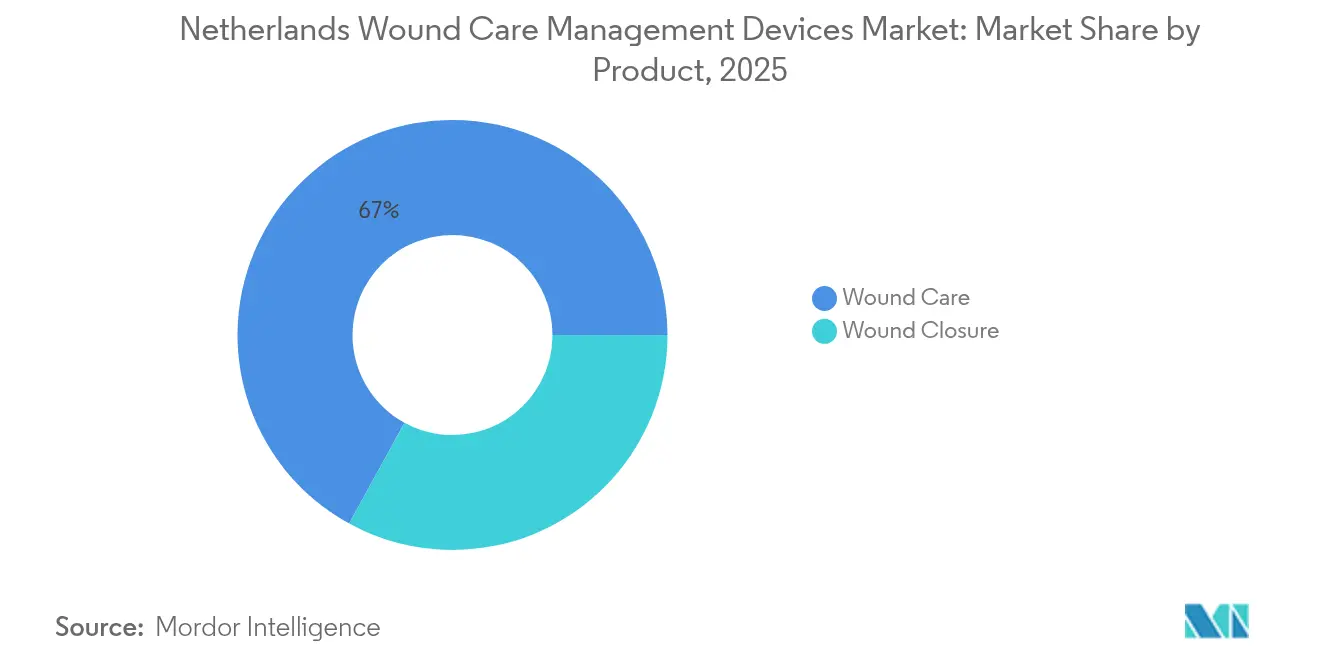

- By product, wound care devices led with 67.02% of the Netherlands wound care management devices market share in 2025, while wound closure products are forecast to grow at 5.11% CAGR through 2031.

- By wound type, chronic wounds accounted for 60.42% of the Netherlands wound care management devices market size in 2025, but acute wounds represent the fastest growth at 5.55% CAGR to 2031.

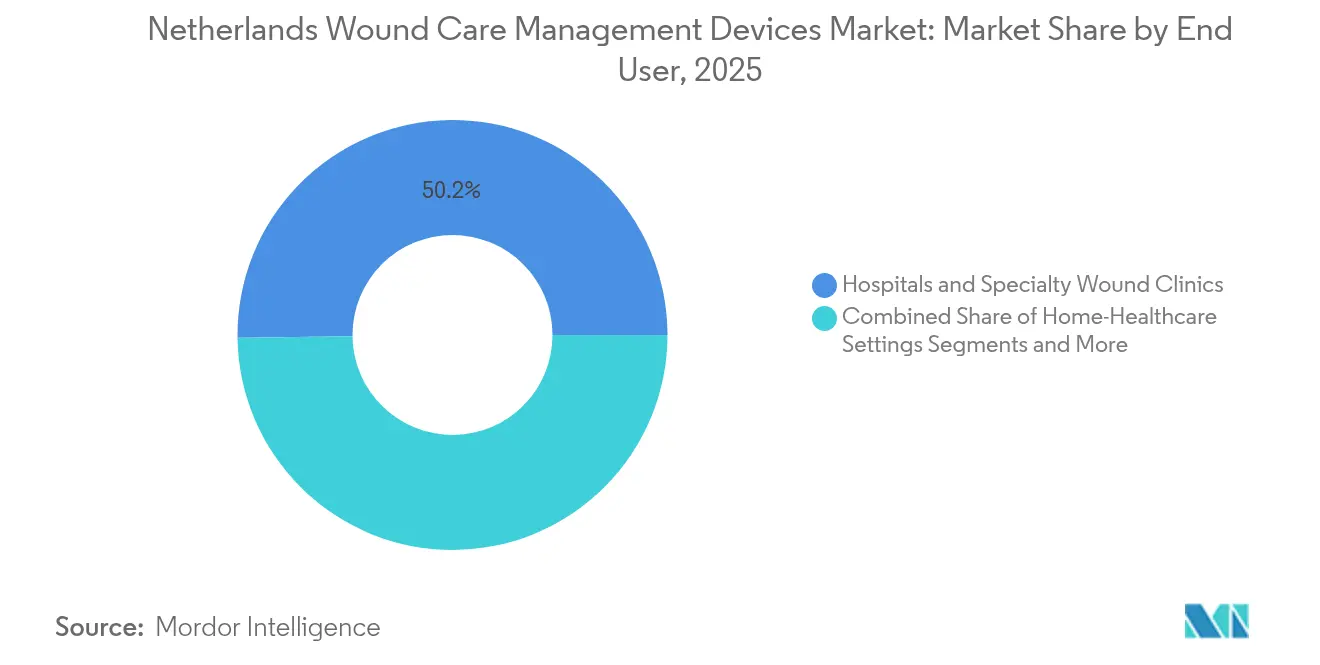

- By end user, hospitals and specialty clinics held 50.20% of the Netherlands wound care management devices market share in 2025; home healthcare settings exhibit the highest projected CAGR at 5.58% through 2031.

- By mode of purchase, institutional procurement captured 62.71% of the Netherlands wound care management devices market size in 2025, whereas retail and OTC channels are advancing at 5.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing incidence of chronic wounds & diabetic ulcers | +1.2% | National, concentrated in urban centers | Medium term (2-4 years) |

| Rising surgical procedure volumes | +0.8% | National, hospital-centric | Short term (≤ 2 years) |

| Rapidly expanding ageing population | +1.5% | National, rural areas disproportionately affected | Long term (≥ 4 years) |

| Uptake of negative-pressure & smart-sensor wound-therapy devices | +0.9% | National, early adoption in academic medical centers | Medium term (2-4 years) |

| National "Fast-Track" protocol accelerating specialist referrals | +0.4% | National, primary care integration | Short term (≤ 2 years) |

| Sustainability push for bio-based, compostable dressings | +0.3% | National, hospital procurement focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing incidence of chronic wounds & diabetic ulcers

Lower diabetic-foot-ulcer incidence of 0.34% among Dutch diabetes patients coexists with a growing elderly population whose frailty pushes chronic wound numbers upward. Pressure ulcers affect 4.2% of nursing-home residents, with more than one-fifth infected, sustaining demand for antimicrobial dressings. Multidisciplinary centers achieve 69% closure rates for recurrent diabetic ulcers within 75 days, extending ulcer-free periods beyond 350 days through reconstructive surgery. Frailty assessments show 83% prevalence among elderly leg-ulcer patients, underscoring technology needs that address complex comorbidities. Advanced monitoring solutions that adapt to individual healing trajectories are therefore gaining clinical traction.

Rising surgical procedure volumes

Higher surgical throughput has multiplied demand for both prophylactic and therapeutic wound solutions. Closed-incision negative-pressure therapy cut infection rates to 24% from 51% in complex abdominal repairs. In femoral endarterectomy, single-use NPWT lowered complication incidence from 50.8% to 8% while reducing average costs per patient by EUR 588. Burns in patients over 85 years carry a 23.8% mortality rate, pushing hospitals to adopt specialized dressings that accelerate re-epithelialization. As value-based reimbursement gains ground, hospitals increasingly view surgical-wound performance as a determinant of financial health.

Rapidly expanding ageing population

Amputation rates among diabetic patients fell, reflecting earlier intervention and better wound-care protocols. Long-term-care spending plans show a funding surplus, enabling wider deployment of advanced therapies in institutional settings. Government investments [1]Dutch health Authority, "February letter on the use of the Wlz 2025 budgetary framework," puc.overheid.nl in additional nursing-home beds from 2027 will drive purchases of devices configured for continuous monitoring and remote clinician oversight. AI-enabled lifestyle sensors in care facilities allow earlier detection of skin breakdown, converting reactive treatment into proactive prevention [2]Sjors Groeneveld, "The Cooperation Between Nurses and a New Digital Colleague AI-Driven Lifestyle Monitoring in Long-Term Care for Older Adults: Viewpoint," JMIR Publications, nursing.jmir.org.

Uptake of negative-pressure & smart-sensor wound-therapy devices

Smith+Nephew’s RENASYS EDGE system, CE-marked in 2024, highlights the shift toward portable NPWT units that improve patient mobility. Cost-effectiveness analyses reveal EUR 4,156 savings per closed wound despite higher acquisition costs because of shorter healing times [3]Apelqvist J, "Negative Pressure Wound Therapy An update for clinicians and outpatient care givers," EWMA, journals.cambridgemedia.com.au. Smart dressings that track pH, temperature, and moisture enable early identification of complications; academic prototypes such as the iCares bandage are demonstrating predictive accuracy that could guide therapy adjustments. Machine-learning algorithms underpinning these platforms promise individualized care plans that maximize closure probabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High total treatment cost for advanced modalities | -0.7% | National, cost-sensitive segments | Medium term (2-4 years) |

| Stringent reimbursement approval in Dutch basic-insurance system | -0.5% | National, regulatory bottlenecks | Short term (≤ 2 years) |

| Shortage of certified wound-care nurses | -0.4% | National, rural areas more affected | Long term (≥ 4 years) |

| Environmental restrictions on single-use plastics in hospitals | -0.2% | National, institutional procurement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High total treatment cost for advanced modalities

Although NPWT accelerates closure, its initial device cost of EUR 2,035 per patient exceeds the EUR 1,919 outlay for conventional care, pressuring hospital budgets. Dutch basic-insurance reimbursement demands rigorous cost-effectiveness evidence before new modalities are listed, slowing adoption for premium innovations. Rising monthly insurance premiums have heightened public scrutiny of medical-device expenditures, leading payers to prioritize solutions with proven economic returns. Outpatient wound-clinic studies indicating EUR 2,621 annual savings per patient therefore focus on care-setting optimization rather than higher-priced technology upgrades.

Stringent reimbursement approval in Dutch basic-insurance system

Nederlandse Zorgautoriteit classification rules require detailed clinical and economic dossiers, extending market-entry timelines for novel devices. Although the 2025 national health budget allocates EUR 109.4 billion to care delivery, regulators emphasize cost containment and equitable access over rapid innovation. Surplus capacity in long-term-care finances can support advanced devices but procurement teams remain conservative until outcome data reach threshold levels. The elevated evidence bar thus favors incumbents with resources for longitudinal trials, reducing near-term opportunities for start-ups.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Broad Device Portfolios Command the Premium Tier

Wound care devices retained 67.02% share of the Netherlands wound care management devices market in 2025, led by foam dressings, hydrofibers, and negative-pressure platforms that provide superior exudate management and infection control. Smith+Nephew’s NPWT line contributed to 3.8% underlying revenue growth in its Advanced Wound Management division during Q1 2025. Clinical studies that position advanced dressings as cost-neutral over an episode of care are sustaining hospital demand even amid reimbursement scrutiny. Wound closure products account for smaller revenue but are expanding at 5.11% CAGR as staplers, sealants, and bioabsorbable clips gain favor in minimally invasive surgery. Sensor-integrated dressings that transmit temperature or pH data to clinicians are blurring category boundaries, enabling hybrid products that both close and monitor wounds.

The Netherlands wound care management devices market size for wound closure solutions is set to climb as procedure volumes rise and surgeons seek devices that limit operative time while improving cosmetic results. Incorporation of antimicrobial coatings into sutures is lowering post-operative infection risk, aligning with hospital quality metrics. Biodegradable adhesives promise avoidance of removal procedures, adding patient convenience. In parallel, developers are embedding microelectronics into adhesives to create intelligent closures capable of reporting tension or moisture in real time, a capability valued by surgical teams pursuing enhanced recovery protocols.

By Wound Type: Chronic-Care Complexity Sustains Advanced Therapy Demand

Chronic wounds captured 60.42% of Netherlands wound care management devices market share in 2025, reflecting the cumulative effects of aging, vascular disease, and diabetes. Prevalence of pressure ulcers in institutionalized elderly patients drives perpetual consumption of foam and antimicrobial dressings, while NPWT shortens closure timelines for recalcitrant diabetic ulcers. Frailty assessments reveal higher-than-expected care complexity, necessitating technologies that simplify dressing changes and enable caregivers with limited wound expertise. The Netherlands wound care management devices market size for chronic wounds is projected to grow steadily as the population aged 65 + rises and comorbid conditions accumulate.

Acute wounds are forecast to expand faster at 5.55% CAGR, riding on surgical volume growth and improved trauma survival rates. Prophylactic NPWT has demonstrated infection reductions of more than 50% in complex abdominal procedures, encouraging routine use in high-risk surgeries. Burns treatment for older adults remains resource-intensive, reinforcing demand for dressings that speed re-epithelialization while minimizing pain. The Netherlands wound care management devices industry increasingly couples acute-wound therapies with digital monitoring, allowing early intervention when complications emerge.

By End User: Home Healthcare Emergence Reshapes Care Delivery

Hospitals and specialty clinics retained 50.20% revenue share in 2025, yet the home-care channel grows 5.58% CAGR as digital monitoring underpins safe decentralisation. Luscii’s remote-care platform has already lowered cardiology outpatient visits by 19%; OMRON’s January-2025 takeover signals strategic intent to embed similar functionality in wound care workflows. Portable NPWT units approved for patient self-management enable same-day discharge, lowering inpatient bed-days and amplifying Netherlands wound care management devices market penetration beyond hospital walls.

Institutional facilities remain indispensable for complex or surgically intensive cases. AI-powered imaging tools have analysed 50 million wounds to date, supplying clinicians with healing-trajectory forecasts that refine treatment choice. As ageing deepens, long-term-care operators pilot sensor carpets and chair-pressure maps that alert nurses to shear or moisture risk, integrating wound prevention into everyday elder care.

By Mode of Purchase: Retail Growth Signals Patient Empowerment

Institutional procurement contributed 62.71% of 2025 revenue, mirroring strict professional oversight for advanced modalities. Value-based tenders now score bids on healing time, total cost and environmental footprint, lifting barriers for suppliers ready with lifecycle analyses. The Fast-Track protocol standardises triage, nudging GPs toward products with published algorithms and validated outcomes.

Retail and OTC channels climb at 5.72% CAGR as educated patients order silicagel sheets, hydrocolloids and smart dressings through e-commerce. Integrated tele-consultation services help customers photograph wounds and receive guidance, reinforcing adherence while shrinking travel costs. This consumer pivot enlarges the Netherlands wound care management devices market and forces manufacturers to package professional-grade performance in user-friendly formats.

Geography Analysis

Urban teaching hospitals in Amsterdam, Utrecht, and Rotterdam spearhead adoption of advanced wound care systems, enabled by research grants and robust clinical-trial infrastructure. These centers often pilot smart dressings and predictive analytics platforms before nationwide rollout, anchoring early revenue streams for innovators. Rural regions, by contrast, face shortages of certified wound-care nurses, prompting investment in telehealth to bridge expertise gaps. Implementation of the Fast-Track referral model nationwide has harmonized treatment pathways, yet rural clinics still confront longer travel times for specialist consultations, reinforcing the appeal of home-based NPWT units.

Government funding of EUR 600 million to expand nursing-home capacity beginning 2027 will concentrate new demand for institutional wound-care technologies outside the Randstad corridor. Facilities built under this program are being designed with sensor-enabled care suites, positioning them as early adopters of continuous monitoring systems. Recycling mandates appear most stringent in university hospitals, where sustainability offices track packaging waste as a procurement criterion, indirectly shaping supplier portfolios. Cross-border care agreements with Germany and Belgium facilitate knowledge exchange and joint clinical studies, benefiting Dutch suppliers that can prove efficacy in broader European populations.

The Netherlands wound care management devices market registers near-uniform reimbursement rules across provinces, yet local procurement collaboratives negotiate separate supply contracts that favor vendors able to guarantee just-in-time logistics. The national electronic-health-record backbone simplifies data collection for outcomes-based purchasing, giving device makers that offer integrated digital dashboards an advantage. Overall, regulatory coherence, high digital maturity, and demographic headwinds combine to create a fertile test bed for novel wound-management ecosystems.

Competitive Landscape

Multinational incumbents such as Smith+Nephew, ConvaTec, and Mölnlycke hold leading positions in the Netherlands wound care management devices market by coupling broad portfolios with established key-account teams. Smith+Nephew’s RENASYS EDGE rollout and 3.8% Q1 2025 revenue uptick demonstrate the resilience of premium NPWT lines. ConvaTec’s 2024 clinical study results showcased faster closure for its collagen-alginate dressings, reinforcing evidence-based marketing tactics. Mölnlycke leverages its Safetac silicone technology to secure formularies that prioritize atraumatic dressing removal.

Digital-health entrants, often spin-outs from Dutch universities, target gaps in real-time monitoring and predictive analytics. Plasmacure’s cold-plasma PLASOMA device, able to close wounds 2.5 times faster in clinical studies, positions the firm as a challenger with a differentiated modality. The acquisition of Luscii by OMRON Healthcare underscores rising interest from consumer-health giants in remote monitoring, potentially widening distribution channels for sensor-embedded dressings. Regulatory hurdles under the EU Medical Device Regulation favor well-capitalized players that can finance post-market surveillance and clinical evidence generation, but cloud-based software companies circumvent some hardware burdens, accelerating their go-to-market path.

Competitive battlegrounds increasingly coalesce around sustainability credentials and outcome-based pricing. Suppliers that reclaim NPWT pumps for refurbishment, or offer bio-based dressings that satisfy plastic-reduction targets, are gaining tender advantages. Hospitals award multi-year contracts contingent on healing-rate guarantees, prompting vendors to bundle devices, consumables, and analytics in integrated platforms. White-space opportunities include machine-learning wound-scoring engines, compostable absorbent layers, and end-to-end logistics services that reduce caregiver workload while improving healing trajectories.

Netherlands Wound Care Management Devices Industry Leaders

-

ConvaTec

-

Smith & Nephew

-

Medtronic

-

Solventum

-

Coloplast

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Plasmacure signed a development and distribution agreement with Venture Medical for its PLASOMA cold-plasma chronic-wound system.

- December 2024: UMC Utrecht and TU Delft unveiled WOCA, a low-cost portable NPWT device built on Arduino technology for trials in low-resource settings.

- September 2024: Plasmacure reported clinical data showing PLASOMA closes 2.5 times more wounds than standard care.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Netherlands wound-care management devices market as every single-use or reusable device, negative-pressure systems, advanced sensor dressings, debridement tools, and closure instruments designed to clean, protect, or close chronic and acute skin lesions in Dutch clinical or home settings.

Scope Exclusion: first-aid plasters sold solely as over-the-counter consumer goods are not included.

Segmentation Overview

-

By Product

-

Wound Care

-

Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

-

Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Other Wound Care Products

-

Dressings

-

Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

-

Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical/Traumatic Wounds

- Burns

- Other Acute Wounds

-

Chronic Wounds

-

By End User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

-

By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

Detailed Research Methodology and Data Validation

Primary Research

Our analysts held structured interviews with Dutch wound-care nurses, hospital procurement heads, and home-care coordinators across Randstad, North Brabant, and Friesland. These discussions validated average selling prices, NPWT penetration, and regional stock-outs that desk material alone could not surface.

Desk Research

We reviewed freely available tier-1 sources such as the Netherlands Central Bureau of Statistics surgical files, RIVM prevalence dashboards, Eurostat hospital-discharge data, International Diabetes Federation disease registers, and European Wound Management Association guidance. Patents from Questel and company statements in D&B Hoovers highlighted technology diffusion and pricing. Tenders Info notices plus EU-MDR filings confirmed installed base numbers. The sources named illustrate the breadth of our desk work; many additional references supported data checks.

Market-Sizing & Forecasting

We anchored 2025 value using a top-down prevalence-to-treated-cohort model, then corroborated totals with selective bottom-up supplier roll-ups. Core variables, diabetes incidence, elective surgery trends, geriatric population growth, NPWT adoption rates, and device replacement cycles feed a multivariate regression that extends forecasts to 2030. Where bottom-up numbers were patchy, we aligned outputs to hospital invoice audits before applying scenario analysis for reimbursement shifts.

Data Validation & Update Cycle

Model outputs face peer review and variance checks; anomalies trigger re-interviews. Reports refresh annually, with interim updates when material regulatory or recall events emerge.

Why Mordor's Netherlands Wound Care Management Baseline Commands Reliability

Published estimates vary because firms differ on scope, base year, and assumption depth. By focusing strictly on devices, selecting a 2025 anchor, and grounding inputs in Dutch usage metrics, Mordor Intelligence offers a balanced lens.

Key gap drivers elsewhere include mixing consumer dressings with devices, relying on global revenue splits, or isolating only advanced sub-segments.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 220.46 m (2025) | Mordor Intelligence | - |

| USD 349 m (2023) | Regional Consultancy A | Combines dressings, biologics, OTC items; older base year and revenue-share split model |

| USD 165 m (2025) | Trade Journal B | Counts export-import dressings only; excludes hospital devices |

| USD 182.85 m (2028) | Global Consultancy C | Looks solely at advanced segment; limited survey sample without national calibration |

The comparison shows how Mordor Intelligence delivers a reproducible, transparent baseline rooted in current data and continuous validation, giving decision-makers a dependable starting point.

Key Questions Answered in the Report

What is the current size of the Netherlands wound care management devices market?

The market stands at USD 231.24 million in 2026 and is set to reach USD 293.62 million by 2031.

Which product category holds the largest share?

Wound care devices, including advanced dressings and NPWT systems, hold 67.02% share of the Netherlands wound care management devices market.

How fast are home-healthcare applications growing?

Home-care use of wound devices is expanding at a 5.58% CAGR as telehealth and single-use NPWT enable safe treatment outside hospitals.

What is driving acute wound segment growth?

Rising surgical volumes and enhanced trauma care protocols are pushing the acute segment to a 5.55% CAGR through 2031.

How are sustainability rules affecting device procurement?

EU and Dutch bans on single-use plastics are pressuring hospitals to shift toward bio-based dressings and reusable NPWT pumps, reshaping supplier selection criteria.

Why are reimbursement approvals challenging for new devices?

The Dutch basic-insurance system demands strong clinical and economic evidence, extending timelines and raising the bar for advanced technologies seeking coverage.

Page last updated on: