Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

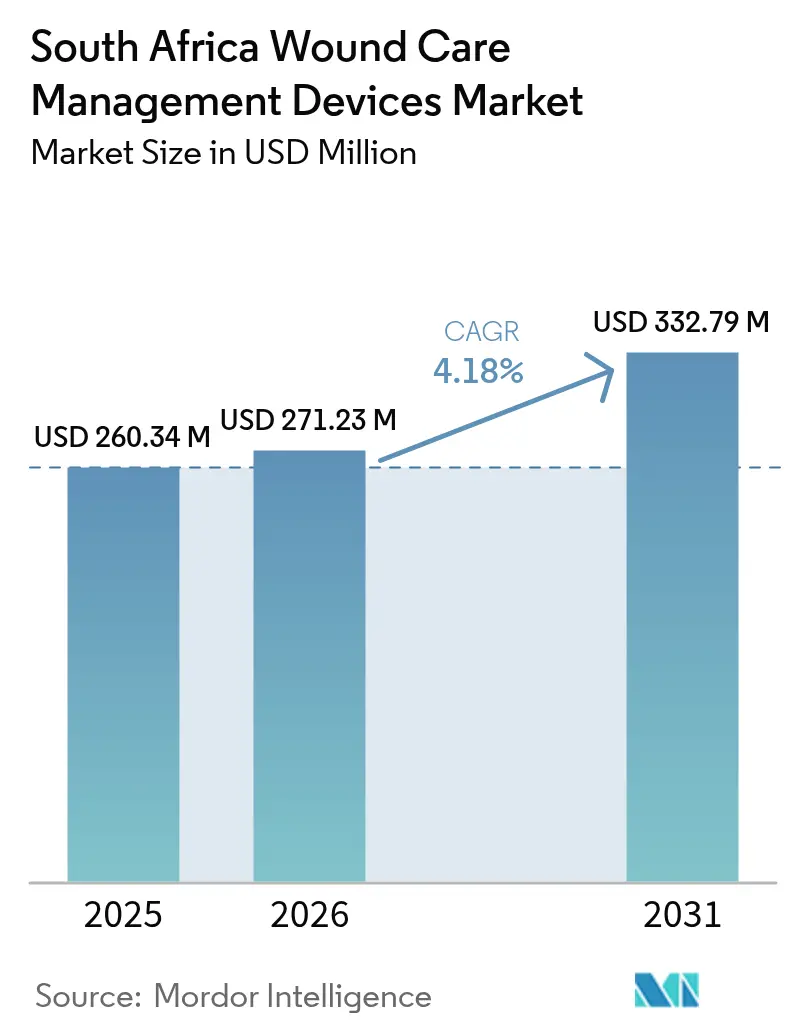

| Base Year Market Size (2025) | USD 260.34 Million |

| Market Size (2026) | USD 271.23 Million |

| Market Size (2031) | USD 332.79 Million |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Africa Wound Care Management Devices Market Analysis by Mordor Intelligence

The South Africa wound care management devices market size is expected to grow from USD 260.34 million in 2025 to USD 271.23 million in 2026 and is forecast to reach USD 332.79 million by 2031 at 4.18% CAGR over 2026-2031. This outlook rests on demographic pressure from an ageing and diabetic population, regulatory reform under the National Health Insurance Act, and rapid hospital modernisation that together lift demand for advanced dressings, closure tools, and portable negative-pressure systems. Import exposure remains pronounced, yet faster South African Health Products Regulatory Authority (SAHPRA) approvals cut device registration times to 68 days, improving speed-to-market for innovators. Chronic disease management accounts for a large share of national hospital beds, so providers increasingly view better wound healing as a route to lower length of stay and readmission risk. Industry players therefore position integrated portfolios that blend evidence-based therapies with home-compatible kits, tele-monitoring functions, and user training to match changing reimbursement norms under universal coverage [1]Jeanette K. Sams-Dodd, "Stable closure of acute and chronic wounds and pressure ulcers and control of draining fistulas from osteomyelitis in persons with spinal cord injuries: non-interventional study of MPPT passive immunotherapy delivered via telemedicine in community care," Frontiers in medicine, frontiersin.org.

Key Report Takeaways

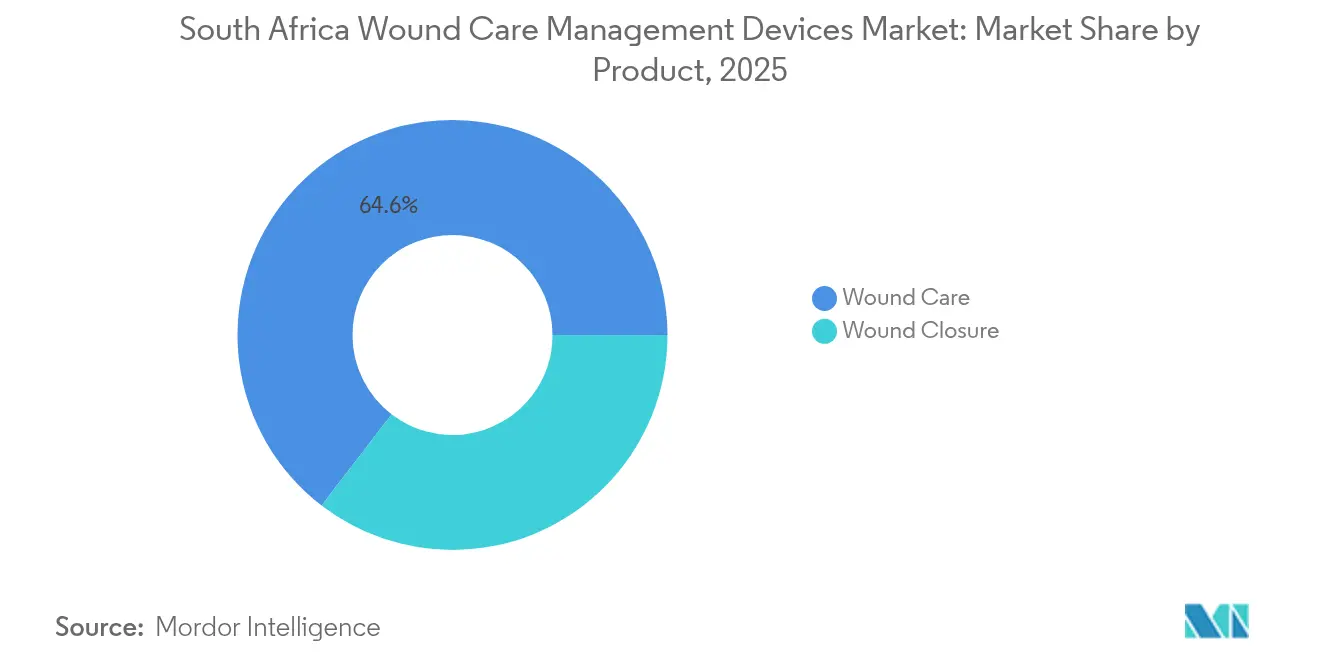

- By product category, wound care products led with 64.58% of the South Africa wound care management devices market share in 2025, while wound closure recorded the fastest CAGR at 4.64% through 2031.

- By wound type, chronic wounds accounted for 58.62% share of the South Africa wound care management devices market size in 2025, whereas acute wounds are projected to grow at 4.78% CAGR to 2031.

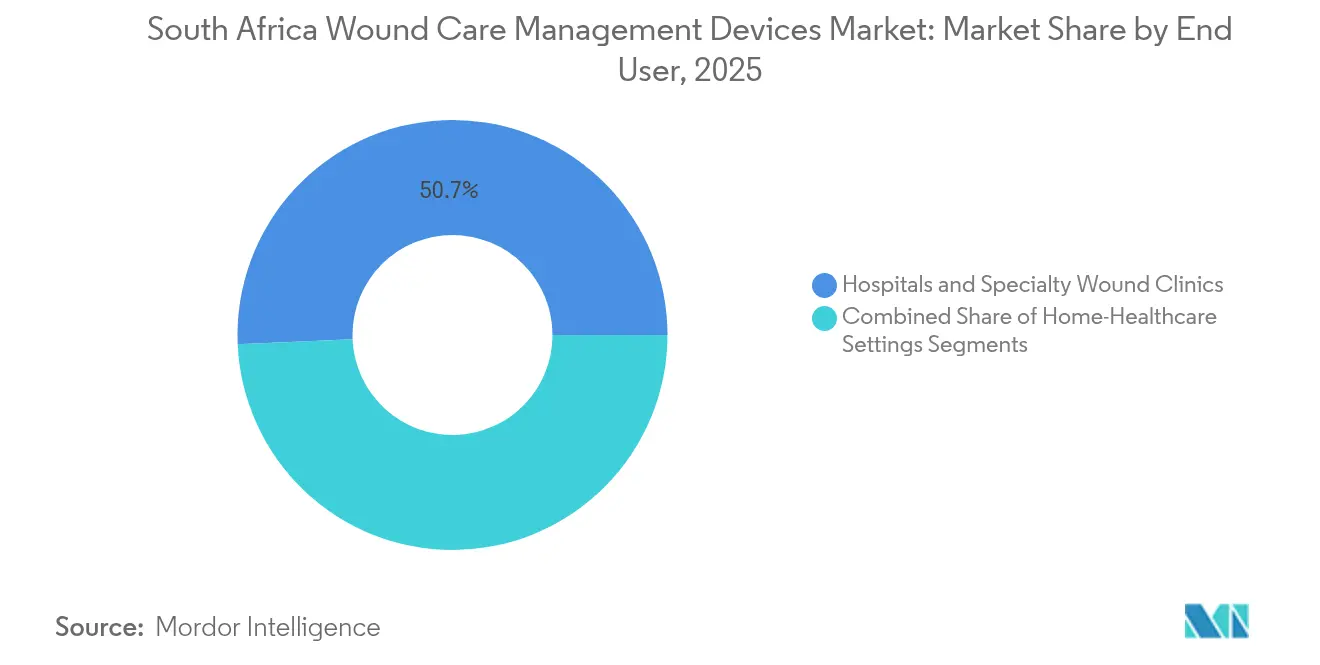

- By end user, hospitals and specialty wound clinics held 50.68% share of the South Africa wound care management devices market in 2025, but home healthcare settings are on track for a 4.83% CAGR during the same period.

- By mode of purchase, institutional procurement represented 60.88% share of the South Africa wound care management devices market in 2025, yet retail and over-the-counter channels are projected to expand at a 4.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of chronic wounds and surgical procedures | +1.2% | National, concentrated in urban provinces | Medium term (2-4 years) |

| Ageing and diabetic population boosting advanced dressings demand | +1.0% | National, higher impact in Western Cape and Gauteng | Long term (≥ 4 years) |

| Accelerating adoption of negative-pressure wound therapy devices | +0.8% | Urban centres, expanding to secondary cities | Short term (≤ 2 years) |

| Growing technology advancements in wound care devices | +0.6% | National, led by private facilities | Medium term (2-4 years) |

| SAHPRA fast-track incentives for local manufacturing | +0.4% | National, hubs in Gauteng and Western Cape | Long term (≥ 4 years) |

| Growth of inbound medical tourism for complex wound management | +0.3% | Cape Town, Johannesburg, Durban | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic Wounds and Surgical Procedures

Diabetes prevalence climbed from 5.5% in 2000 to an estimated 13.1–26.3% of South African adults by 2025, a surge that translates into higher rates of lower-limb amputation and prolonged ulcer care. Patient-level data show 0.73% of diabetes patients undergo new amputations each year. Chronic wound volume therefore rises while surgical backlogs persist, since specialist density per 100 000 population remains below World Health Organization benchmarks. Hospitals respond by adopting advanced dressings and portable negative-pressure systems that accelerate healing and curb inpatient costs.

Ageing and Diabetic Population Boosting Advanced Dressings Demand

Systematic reviews confirm diabetes prevalence reaches 26.3% in some provinces and intersects with population ageing, so complex ulcers and pressure injuries become more common. Older patients often face self-care difficulties, especially those managing both diabetes and hypertension, and risk intensifies among unmarried and low-income groups [2]Ghose Bishwajit, "Sociodemographic and health disparities in self-care difficulties among older individuals: Evidence from South Africa," BMC Geriatrics, bmcgeriatr.biomedcentral.com. Advanced hydro-fiber, foam, and antimicrobial dressings deliver moisture balance and bacterial control that shorten healing time relative to gauze. Providers weigh these clinical gains against budget pressure and increasingly prove value through real-world cost-offset studies.

Accelerating Adoption of Negative-Pressure Wound Therapy Devices

Clinical trials at Groote Schuur Hospital achieved 55% closure within 14 days when ultraportable negative-pressure wound therapy (NPWT) systems were used. Economic modelling shows each closed wound saves EUR 4,155.98 in downstream care despite higher device outlay. Single-use NPWT units facilitate safe discharge and home monitoring, a priority as the South Africa wound care management devices market shifts toward community care.

Growing Technology Advancements in Wound Care Devices

Artificial-intelligence roadmaps under the Draft National AI Plan aim for ZAR 70 billion investment by 2030 and include real-time wound imaging, biosensor patches, and predictive analytics. Johnson & Johnson’s Impact Ventures program supports African start-ups building AI platforms for remote diagnosis and prescription, reinforcing data-driven care pathways. Wearable pH and temperature sensors feed alerts to clinicians, helping prevent infection escalation in home settings and sustaining device utilisation outside hospitals [3]Dang-Khoa Vo, "Advances in Wearable Biosensors for Wound Healing and Infection Monitoring," MDPI, mdpi.com.

High Cost of Next-Generation Wound Devices and Biologics

Manufacturers spend up to 20% of revenue on supply chain services as freight and component prices rise, inflating retail cost for synthetic skin substitutes and enzymatic debriders. Public hospitals already operate under budget ceilings that tightened, so adoption of premium items remains selective. Private medical schemes cover only 16% of citizens, reinforcing inequity in access to high-priced therapies.

Limited Reimbursement Outside Large Urban Hospitals

Prescribed Minimum Benefits policies only reimburse advanced wound devices when prescribed by specialists, yet workforce ratios reveal 1 physiotherapist per 69 public ICU beds and just 2 state podiatrists for the entire KwaZulu-Natal department. Rural clinics thus struggle to secure funding for modern modalities, widening geographic disparity until telemedicine and the National Health Insurance Act extend specialist oversight.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wound Care Dominance Drives Market Foundation

Wound care products generated 64.58% of South Africa wound care management devices market revenue in 2025, establishing the primary revenue base as hospitals rely on modern dressings for diabetic foot and pressure ulcer control. The South Africa wound care management devices market size for wound care is forecast to track steady gains while negative-pressure systems and antimicrobial foams lift value per case. Traditional cotton gauze remains in public tenders because of low unit price, yet hidden costs linked to longer healing time spur gradual switch to foam and hydro-fiber. Portable NPWT kits post the highest uptake under evidence of 55% two-week closure rates.

Wound closure products climbed fastest at a 4.64% CAGR, mirroring surgical backlog reduction and growth in day surgery centres that favour absorbable tissue adhesives. Sealants and glues secure linear incisions and burn grafts, trimming operating room minutes and follow-up visits. Topical antimicrobials, enzymatic debriders, and skin substitutes keep consistent demand mainly in tertiary facilities. Device makers now bundle closure products with digital tracking apps to meet hospital key-performance metrics.

By Wound Type: Chronic Wounds Reflect Disease Burden Reality

Chronic wounds commanded 58.62% of South Africa wound care management devices market share during 2025, a proportion that mirrors diabetic foot prevalence and prolonged pressure ulcer cases among immobile elders. The South Africa wound care management devices market size tied to chronic wounds expands steadily as clinicians deploy moisture-retentive dressings, off-loading devices, and NPWT to avert costly amputations. Venous leg ulcer management remains complex in peri-urban districts where follow-up compliance is low.

Acute wounds grow quicker at a 4.78% CAGR because trauma centres upgrade trauma packs and burn units introduce advanced closure matrices. Urban violence, road traffic crashes, and elective cosmetic surgery contribute to procedure counts that raise closure device sales. Training modules on donor-site care and infection prevention lift uptake of silicone contact layers and silver-impregnated foams. Public-sector protocols now mandate single-use adhesive strips for caesarean incisions to lower stitch removal visits.

By End User: Home Healthcare Transformation Accelerates

Hospitals and specialised clinics represented 50.68% of South Africa wound care management devices market revenue last year thanks to bundled procurement and volume. Yet, home healthcare settings post 4.83% CAGR through 2031 as universal coverage encourages early discharge and community nursing. Portable NPWT and antimicrobial foam dressings suit domiciliary use, and smartphone-linked biosensors allow weekly tele-consult review. The South Africa wound care management devices market size generated by home settings is expected to double its 2025 base by the decade close, reflecting payer focus on total-cost reduction.

Long-term care centres sustain demand among bedridden elders where pressure ulcer prevention products run alongside continence care. Manufacturers therefore supply starter kits, staff training, and periodic stock replenishment, fostering long-term contracts. Tech firms integrate AI photo analytics that alerts clinicians to healing plateaus, bridging the specialist gap in provincial areas.

By Mode of Purchase: Retail Channel Democratisation Emerges

Institutional purchase controlled 60.88% of South Africa wound care management devices market value in 2025 because bulk tenders dominate public spending. Centralised procurement may intensify under the National Health Insurance Fund, yet retail and over-the-counter lines rise 4.88% a year as patients self-manage less complex wounds. Bandage ranges, hydro-colloid blister plasters, and single-use NPWT boxes now occupy pharmacy aisles where discount chains attract cash buyers.

The South Africa wound care management devices market share held by retail channels benefits from consumer education campaigns on early ulcer intervention. E-commerce supports refill orders for dressings and topical agents, especially in remote towns where clinic stock-outs persist. Manufacturers tailor smaller pack sizes and pictogram-based instructions to boost compliance.

Geography Analysis

Gauteng, Western Cape, and KwaZulu-Natal absorb most device sales because they house the largest hospital networks and host 70% of specialist surgeons. Western Cape private hospitals also cater to inbound medical tourists who seek reconstructive burn care, producing premium consumption patterns. Provincial household healthcare spend totalled ZAR 293 billion in 2022 and equalled 8–9% of GDP, but fiscal ability varies widely.

Rural provinces face double-digit diabetes prevalence yet fewer wound specialists, causing late presentation and higher amputation rates. Studies from district clinics in Eastern Cape note screening gaps where primary health nurses lack monofilament tools for foot checks. Such disparities broaden the addressable pool for tele-wound platforms that extend specialist reach.

The National Health Insurance Act, signed in May 2024 and slated for full roll-out by 2026, aims to standardise coverage and improve supply equity. Universal tariff schedules could lift baseline demand in under-served provinces once procurement aligns. Device producers already court provincial depots with locally assembled kits that side-step currency risk.

Competitive Landscape

International brands continue to dominate the South African wound care management devices market because of global portfolios and deep distributor ties, yet import reliance exposes supply to currency swings. B. Braun recently invested in Gauteng production lines that created 160 jobs and supplied neighbouring markets, signalling a localisation trend. Local capacity improves tender scoring and stabilises inventory during port delays.

Technology partnerships frame many recent moves. Johnson & Johnson supports AI imaging start-ups for early ulcer recognition, while Smith+Nephew’s Cape Town training centre certifies nurses on negative-pressure techniques. Firms now bundle education, remote monitoring software, and device servicing into contract bids, turning solutions into competitive moats.

White-space opportunities lie in home-care kits for diabetic foot ulcers, pressure ulcer prevention packs for long-term facilities, and digitally enabled dressing supplies targeted at remote clinics. Suppliers that align with National Health Insurance formularies and prove cost-offset potential through local studies are expected to gain tender preference.

South Africa Wound Care Management Devices Industry Leaders

-

Smith and Nephew PLC

-

Medtronic PLC

-

Coloplast Ltd

-

Convatec

-

Coloplast

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: ReDress Medical announced that ActiGraft is now reimbursed by Discovery Health for diabetic foot and pressure ulcer treatment under the Advanced Wound Care Framework.

- March 2024: Adcock Ingram Critical Care and Convatec signed a sales, marketing, and distribution agreement covering South Africa and neighbouring countries to expand ostomy and advanced wound portfolios.

- February 2024: Johnson & Johnson Impact Ventures partnered with Villgro Africa to support 10 African healthcare start-ups developing AI solutions for imaging and teleradiology, with applications in wound care triage.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the South Africa wound-care management devices market comprises all single-use and reusable medical devices that clean, close, or actively heal acute or chronic skin lesions, including advanced dressings, negative-pressure wound-therapy pumps, oxygen and electrical stimulation units, tissue adhesives, sutures, staplers, and related applicators. Devices sold only for cosmetic or dermatologic esthetic use are outside the study scope.

Scope exclusion: pharmaceutical topical agents and purely traditional cotton-based bandages were not valued.

Segmentation Overview

-

By Product

-

Wound Care

-

Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

-

Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Topical Agents

- Other Wound Care Products

-

Dressings

-

Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

-

Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical/Traumatic Wounds

- Burns

- Other Acute Wounds

-

Chronic Wounds

-

By End User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

-

By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

Detailed Research Methodology and Data Validation

Primary Research

Interviews were held with wound-care nurses, biomedical engineers, procurement heads at Gauteng and Western Cape hospitals, and private clinic buyers. Conversations helped refine typical device lifespan, price dispersion between imported and locally assembled systems, and the current penetration of NPWT versus conventional dressings across provinces. These insights filled secondary-data gaps before final model sign-off.

Desk Research

Our analysts began with public statistics from authorities such as Statistics South Africa for hospital procedure volumes, the National Department of Health for diabetic prevalence, SAHPRA device approvals, the International Diabetes Federation, and trade data portals like UN Comtrade that track NPWT pump imports. Company 10-Ks, local investor presentations, and peer-reviewed articles in the South African Medical Journal further framed demand drivers. Subscription resources, including D&B Hoovers for manufacturer revenue splits and Volza shipment logs for device inflows, supported volume cross-checks. The sources listed are illustrative; many additional references informed verification and clarification.

Market-Sizing & Forecasting

A top-down reconstruction anchored on 2024 in-patient surgical episodes, diabetic-foot ulcer incidence, and shipment-adjusted import values produced the first cut. Results were corroborated through selective bottom-up checks, sampled supplier revenues, and average selling price multiplied by unit volumes, then aligned through one round of top-down and bottom-up triangulation. Key variables tracked include: (1) diabetes prevalence trajectory, (2) annual major-surgery counts, (3) NPWT pump install base, (4) average ex-factory ASP trends, and (5) rand-to-USD exchange movement. Multivariate regression with scenario overlays on hospital modernization rates generated the 2025-2030 forecast, and gaps in bottom-up inputs were bridged using weighted regional proxies validated by local experts.

Data Validation & Update Cycle

Outputs undergo anomaly checks, senior-analyst peer review, and variance benchmarking versus independent health-system metrics. The model refreshes every 12 months, with interim revisions triggered by policy or currency shocks. A last-minute pass ensures clients receive the freshest view.

Why Mordor's South Africa Wound Care Management Baseline Commands Reliability

Published values often differ because researchers pick dissimilar device mixes, pricing bases, and refresh cadences.

Key gap drivers here include the inclusion of OTC dressings by some publishers, different inflation deflators, and whether pharmaceutical topicals are blended with device revenue. Mordor's disciplined scope, province-level variables, and annual update rhythm anchor a balanced baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 260.34 M (2025) | Mordor Intelligence | - |

| USD 176.6 M (2024) | Regional Consultancy A | Includes OTC dressings and lacks device sub-segmentation; older base year |

| USD 1.5 B (2024) | Global Consultancy B | Merges consumables, biologics, and services; upward currency-inflation mark-ups |

In sum, our transparent variable selection, dual validation steps, and device-only scope give decision-makers a dependable view that bridges optimism and conservatism while remaining traceable for future audits.

Key Questions Answered in the Report

What is the current value of the South Africa wound care management devices market?

The market stands at USD 271.23 million in 2026 and is projected to reach USD 332.79 million by 2031.

Which product category dominates revenue?

Wound care products including advanced dressings hold 64.58% of 2025 revenue, while wound closure devices grow fastest at 4.64% CAGR.

How will home healthcare influence demand?

Home settings post a 4.83% CAGR as portable NPWT and tele-monitoring tools enable safe discharge and self-care, lowering hospital stays.

What role does the National Health Insurance Act play?

Universal coverage is set to standardise procurement and extend advanced wound care to rural clinics, lifting baseline demand after full roll-out by 2026.

Why is negative-pressure wound therapy gaining traction?

Local trials achieved 55% closure within 14 days and each healed case saved EUR 4,155.98 in downstream costs, driving adoption in both hospital and home care.

Which provinces drive medical tourism related to wound management?

Western Cape, Gauteng, and KwaZulu-Natal attract regional patients seeking complex reconstructive surgery and advanced closure solutions.

Page last updated on: