Democratic Republic Of Congo Automotive Engine Oil Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

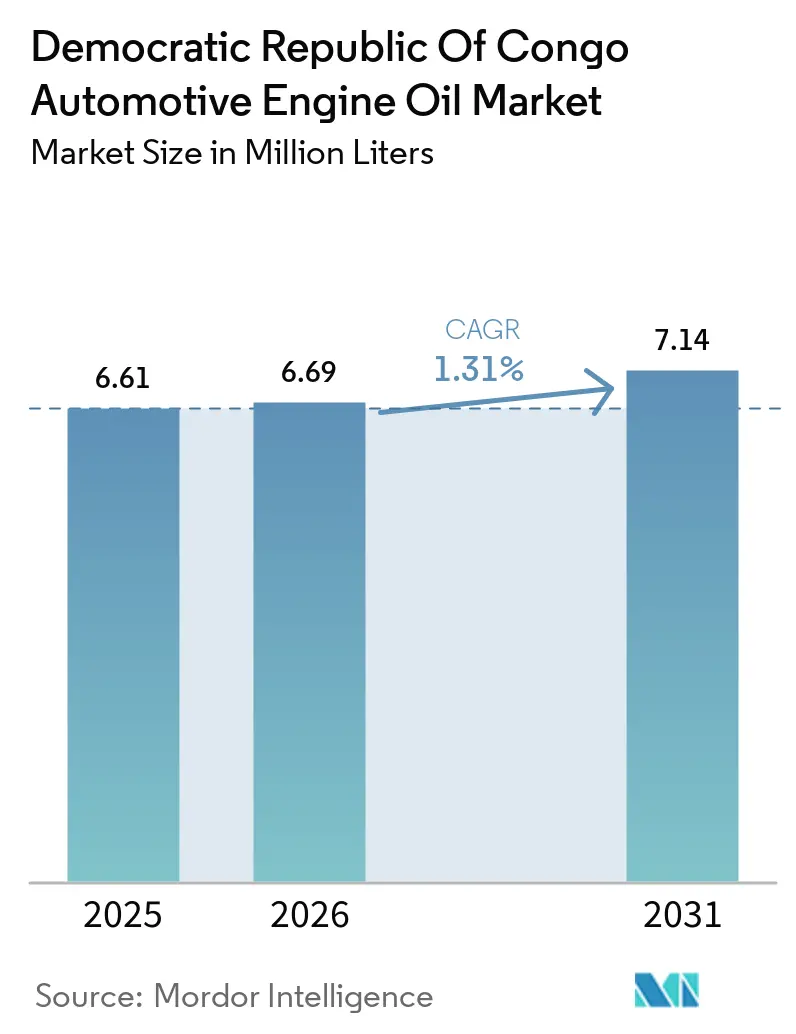

| Base Year Market Size (2025) | 6.61 Million liters |

| Market Volume (2026) | 6.69 Million liters |

| Market Volume (2031) | 7.14 Million liters |

| Growth Rate (2026 - 2031) | 1.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Democratic Republic Of Congo Automotive Engine Oil Market Analysis by Mordor Intelligence

The Democratic Republic of Congo Automotive Engine Oil Market size is expected to increase from 6.61 million liters in 2025 to 6.69 million liters in 2026 and reach 7.14 million liters by 2031, and is expected to grow at a CAGR of 1.31% over 2026-2031. For decades, the nation’s sole refinery has been entirely shut down, leading to a continued dependence on imported petroleum products. Coupled with the fact that a significant portion of the road networks remains unpaved, this situation has stunted growth and concentrated distribution primarily in Kinshasa and a select few provincial hubs. The average age of vehicles on the road is considerably high, resulting in heightened lubricant consumption per vehicle. However, the market grapples with challenges as counterfeit lubricants and informal oil recycling undermine legitimate sales. Meanwhile, mining activities in the Katanga copper-cobalt belt are driving up demand for heavy-duty and synthetic lubricant grades. Additionally, reforms aimed at fuel subsidies, driven by efficiency, are prompting fleets to extend their drain intervals. Looking ahead, stricter regulations on used-vehicle imports, set to take effect in the near future, promise to rejuvenate a segment of the fleet. Yet, it also means a prolonged reliance on older engines, which will necessitate higher-viscosity multigrades for optimal protection.

Key Report Takeaways

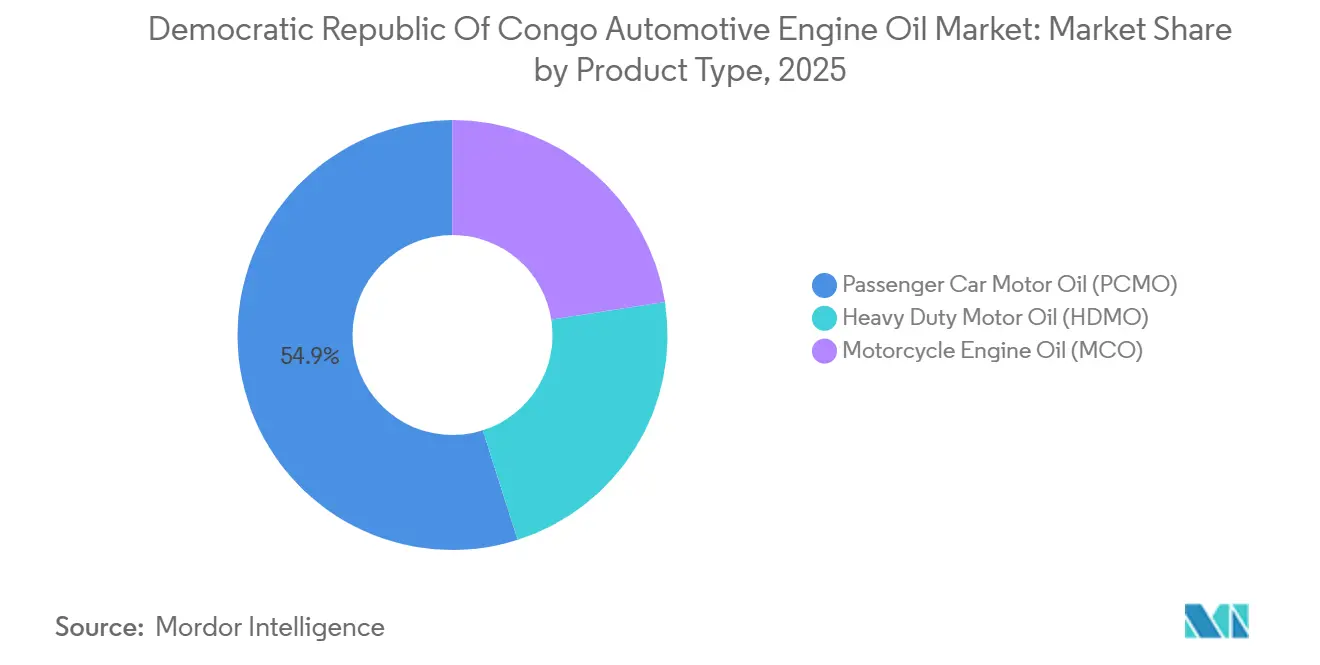

- By product type, passenger car motor oil led with 54.91% of the Democratic Republic of Congo automotive engine oil market share in 2025, while motorcycle engine oil is forecast to expand at a 3.12% CAGR through 2026 to 2031.

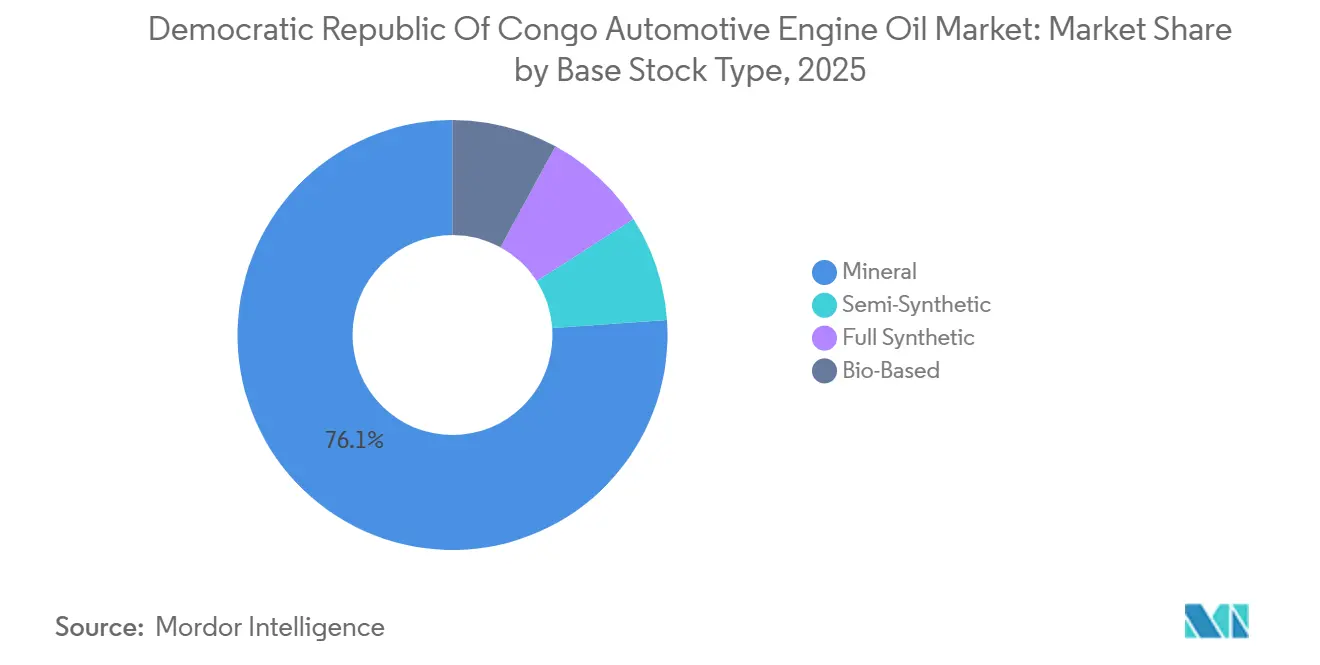

- By base stock, mineral oils accounted for 76.12% of the 2025 Democratic Republic of Congo automotive engine oil market size, whereas full synthetics are projected to grow at a 4.08% CAGR through 2026 to 2031.

- By viscosity grade, 15W-XX captured 47.42% of the 2025 Democratic Republic of Congo automotive engine oil market share, and 5W-XX grades are expected to advance at a 3.92% CAGR over 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Democratic Republic Of Congo Automotive Engine Oil Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising average vehicle age necessitates more frequent engine oil consumption | +0.40% | National, concentrated in Kinshasa, Lubumbashi, Goma | Medium term (2-4 years) |

| Expansion of the vehicle parc, supported by increasing imports of used vehicles | +0.30% | National, with early gains in Kinshasa, Matadi, and Boma | Short term (≤ 2 years) |

| Growth in mining and logistics activities is driving higher demand for commercial vehicle lubricants | +0.30% | Katanga (Lubumbashi, Kolwezi), Kasaï, eastern provinces | Long term (≥ 4 years) |

| Gradual transition toward synthetic and high-performance engine oils | +0.20% | Lubumbashi, Kinshasa, mining corridors | Long term (≥ 4 years) |

| Increasing adoption of on-demand mobile oil-change services | +0.10% | Kinshasa, Goma, and Lubumbashi urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Average Vehicle Age Necessitating More Frequent Engine Oil Consumption

In the Democratic Republic of Congo, the automotive parc primarily expands through imports of used vehicles, with only a small fraction being new passenger cars. Older engines, due to worn seals and rings, tend to consume more oil as they experience increased blow-by. Recent regulations reduced the import age ceiling and mandated stringent technical inspections, posing a risk of immobilization for non-compliant vehicles. Cars that pass these inspections may require more frequent oil changes, thereby bolstering the demand for lubricants. Enforcement efforts, particularly robust in Kinshasa, have seen authorities actively impounding unsafe vehicles. Consequently, these developments have led to a moderate uptick in the country's automotive engine oil market.

Expansion of the Vehicle Parc Supported by Imports of Used Vehicles

Matadi and Boma, despite facing high customs duties that can reach a significant percentage of the cost, insurance, and freight value, managed to process a greater portion of arrivals. This was largely due to stricter fuel-marking measures that effectively reduced smuggling and significantly increased fiscal revenues[1]Authentix, “Fuel Marking Program,” authentix.com. Every new car or motorcycle leads to consistent lubricant purchases over its lifetime. Motorcycle taxis have become a significant mode of urban transport, positioning two-wheelers as the swiftly growing segment. The integration of moto-taxi fleets into ride-hailing platforms like Yango is steering riders towards branded lubricants and regular maintenance, boosting sales in Kinshasa, Matadi, and Boma.

Growth in Mining and Logistics Activity Driving Higher Demand for Commercial Vehicle Lubricants

Heavy-duty trucks operate continuously at large mines in the Katanga copper-cobalt belt, such as Glencore's Kamoto project and China Molybdenum Company's Tenke Fungurume, which depend on long-life oils to reduce downtime[2]Glencore, “Kamoto Copper Company,” glencore.com . United Petroleum (UP-RDC) has become a key supplier, providing Shell-partnered synthetics that meet the East Africa Standard 177:2019 to more than ten mining groups. Fuel consumption in the Western corridor has significantly increased, indicating a notable rise in the use of heavy-duty motor oil. This trend is further supported by logistics fleets transporting copper and cobalt to export gateways, particularly in Lubumbashi, Kolwezi, and on extended routes to Angola and Tanzania.

Gradual Transition Toward Synthetic and High-Performance Engine Oils

Full synthetics are becoming more popular as the benefits of extended drains start to outweigh their higher purchase prices. COBIL made a significant move into premium formulations by launching SuperSyn and other certified product lines, marking the first state-backed initiative in this domain. TotalEnergies is promoting its Quartz INEO and Quartz 9000 products, both of which have received multiple approvals from original equipment manufacturers. Auto Lubumbashi, with its in-house laboratory, conducts oil analyses enabling fleets to safely extend their service intervals. Mining clients who have transitioned to synthetics report reduced downtime and decreased fuel consumption, further emphasizing the rising value of these products per liter.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and adulterated engine oils | -0.30% | National, concentrated at borders (Kasumbalesa, YEMA, Goma) | Short term (≤ 2 years) |

| Fuel-subsidy linked efficiency norms lowering volumes | -0.20% | National, excluding mining fuels (Katanga exempted Oct 2025) | Medium term (2-4 years) |

| Informal oil-recycling reducing fresh demand | -0.20% | National, concentrated in Kinshasa, Lubumbashi informal garages | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Adulterated Engine Oils

Authorities in Angola and Tanzania intercepted significant quantities of counterfeit products from major brands like Castrol, Total, and Shell, all of which were destined for the Democratic Republic of Congo. While the Office Congolais de Contrôle is tasked with overseeing standards, its limited resources hinder its ability to monitor every shipment. This gap in oversight has allowed subpar blends to infiltrate the market, appealing to consumers lured by lower prices. Such counterfeits not only accelerate engine wear but also erode brand trust and undermine legitimate sales. A national fuel-marking initiative has demonstrated that traceability can effectively combat fraud. However, while there is potential in extending this system to lubricants, challenges such as funding, laboratory capacity, and ensuring importer compliance remain significant obstacles.

Fuel-Subsidy Linked Efficiency Norms Lowering Volumes

Government spending on fuel subsidies significantly decreased over time, with mining fuels eventually being removed from the subsidy list. As fuel prices increased, transport operators, most of whom manage small fleets of three trucks or fewer, began extending oil drain intervals or switching to more affordable mineral grades. Some informal operators even mixed used oil with diesel to reduce costs, despite the technical risks involved. While the value per liter has risen due to the growing use of synthetic oils, the overall growth in volume has slowed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PCMO Dominates, MCO Accelerates

Passenger car motor oil generated 54.91% of 2025. Due to a predominantly imported fleet, the Democratic Republic of Congo's automotive engine oil market is expected to maintain a significant share over the forecast period. The consistent replacement rate from minibusses and small cars, commonly used for private ride-hailing, supports this trend. Furthermore, adherence to original equipment manufacturer warranties among newer imports continues to drive the demand for multigrade oils.

Motorcycle engine oil, however, is projected to grow at a 3.12% CAGR over 2026 to 2031, with ride-hailing becoming more formalized and urban trips heavily reliant on moto-taxis, branded suppliers such as TotalEnergies and UNICOIL are introducing two-wheeler synthetics. These synthetics promise cooler running temperatures and longer drain intervals, successfully capturing market share from informal blends.

Volumes of heavy-duty motor oil are closely tied to mining activities and cross-border logistics. Even with subsidy reforms, the demand remains robust, supported by expansions in copper and cobalt output. Suppliers based in Lubumbashi are providing advanced motor oil formulations, and there is a growing trend of predictive-maintenance contracts among large truck fleets.

By Base Stock Type: Mineral Prevails, Synthetic Gains

Mineral oils held 76.12% of the 2025 Democratic Republic of Congo automotive engine oil market share because low landed cost remains crucial in an economy with limited per-capita purchasing power. Imported Group I base stocks still dominate blender recipes.

Synthetic Lubricants, forecast at a 4.08% CAGR over 2026 to 2031, Mining clients, operating around the clock, rely on uninterrupted equipment function. In the Democratic Republic of Congo, while the market for synthetic automotive engine oils is currently modest, it is expected to grow. This is largely driven by promotions of extended-drain economics from industry players like Congolaise des Hydrocarbures, TotalEnergies, and United Petroleum of the Democratic Republic of Congo. Meanwhile, semi-synthetic blends cater to mid-tier urban fleets, delivering partial performance enhancements at competitive price points.

Bio-based lubricants, sourced from palm, raphia, and safou oils, have entered local forestry operations. These lubricants are gradually gaining traction, marking them as a promising, albeit niche, segment in the market.

By Grade: 15W-XX Leads, 5W-XX Rises

Fifteen-weight multigrades such as 15W-40 took 47.42% of 2025 demand, reflecting the prevalence of older, high-clearance engines running in tropical heat. They will continue to shoulder nearly half of the Democratic Republic of Congo automotive engine oil market size through mid-forecast.

Lower-viscosity 5W-XX oils are expected to grow at a 3.92% CAGR from 2026 to 2031. In Lubumbashi and Kinshasa stores, engine oils recommended for many imported vehicles carry specifications such as 5W-30. TotalEnergies Quartz INEO and Quartz 9000, which meet these original equipment manufacturer specifications, have become widely available. While monograde oils and specialty blends like 20W-50 are used for generators and older sport utility vehicles, oils with 0W specifications remain limited to a niche market.

Geography Analysis

Kinshasa, with its numerous COBIL stations, the Ango-Ango storage hub, and the highest vehicle population in the country, dominates the Democratic Republic of Congo's automotive engine oil market. The capital's reliance on motorcycle-taxis, rapid urbanization, and stricter technical inspections support the demand for passenger car motor oil and motorcycle oil.

Fuel demand in the western provinces, reliant on Matadi and Boma ports, experienced substantial growth. This increase followed the implementation of a fuel-marking program that enhanced tax compliance. With a steady influx of newer vehicle imports, these corridors remain crucial for multigrade engine oils.

High-value synthetic and heavy-duty engine oil sales are driven by the Katanga copper-cobalt belt, located around Lubumbashi and Kolwezi. The exemption of mining fuels from subsidies ensures price stability, enabling operators to allocate budgets for premium lubricants. Border towns like Goma, situated on the eastern frontier, are benefiting from a newly commissioned terminal to address persistent shortages. Meanwhile, interior centers such as Kamina, Kalemie, Bunia, and Tshikapa, with limited station availability, present untapped opportunities. Companies are focusing on these areas for mobile services and small-format pack sales.

Competitive Landscape

The Democratic Republic of Congo Automotive Engine Oil Market is moderately concentrated. Auto Lubumbashi and UNICOIL vie for dominance, offering technical services, oil analysis, and digital marketing to cater to a significant number of fleet and retail clients. UP-RDC, capitalizing on its partnership with Shell, supplies synthetic oils to several mining operations along the Katanga corridor.

Democratic Republic Of Congo Automotive Engine Oil Industry Leaders

TotalEnergies

Shell plc

Puma Energy

BP p.l.c. (Castrol)

Engen Petroleum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: At Kinshasa’s Molendé station, COBIL SA had unveiled its inaugural series of in-house, API-certified lubricants: Amatis, Omnia, HD Coolant, SuperSyn, and ATF. This launch marked COBIL's strategic pivot into the realms of blending and packaging. With these certified lubricants, COBIL strengthened the domestic supply, reduced the nation's dependence on imports, and influenced the dynamics of the DRC’s automotive engine oil market.

- April 2025: TotalEnergies Marketing RDC hosted a seminar aimed at lubricant distributors. The event had spotlighted Quartz lubricants, offering special promotions and gifts. This initiative broadened service capabilities and deepened customer engagement within TotalEnergies' retail network in the Democratic Republic of Congo. Through distributor training and Quartz promotions, TotalEnergies reinforced lubricant distribution channels, fostered customer loyalty, and enhanced its competitive stance in the DRC’s automotive engine oil arena.

Democratic Republic Of Congo Automotive Engine Oil Market Report Scope

Democratic Republic of Congo Automotive Engine Oil refers to lubricants specifically formulated for vehicles operating in the DRC’s diverse climate and road conditions. It reduces friction, prevents wear, and enhances engine performance while ensuring durability under heavy use. Widely used across passenger cars, trucks, and industrial vehicles, it supports fuel efficiency, reliability, and long-term maintenance of engines in the Congolese automotive sector.

The Democratic Republic of Congo Automotive Engine Oil Market is segmented by product type, base stock type, and grade. By product type, the market is segmented into Passenger Car Motor Oil (PCMO), Heavy Duty Motor Oil (HDMO), and Motorcycle Engine Oil (MCO). By base stock type, the market is segmented into mineral, semi-synthetic, full synthetic, and bio-based oils. By grade, the market is segmented into 0W-XX, 5W-XX, 10W-XX, 15W-XX, monogrades, and other grades. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

| Passenger Car Motor Oil (PCMO) |

| Heavy Duty Motor Oil (HDMO) |

| Motorcycle Engine Oil (MCO) |

| Mineral |

| Semi-Synthetic |

| Full Synthetic |

| Bio-Based |

| 0W-XX |

| 5W-XX |

| 10W-XX |

| 15W-XX |

| Monogrades |

| Other Grades |

| By Product Type | Passenger Car Motor Oil (PCMO) |

| Heavy Duty Motor Oil (HDMO) | |

| Motorcycle Engine Oil (MCO) | |

| By Base Stock Type | Mineral |

| Semi-Synthetic | |

| Full Synthetic | |

| Bio-Based | |

| By Grade | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

Key Questions Answered in the Report

What is the size of the Democratic Republic of Congo Automotive Engine Oil Market?

The Democratic Republic of Congo Automotive Engine Oil Market size is expected to increase from 6.61 million liters in 2025 to 6.69 million liters in 2026 and reach 7.14 million liters by 2031, and is expected to grow at a CAGR of 1.31% over 2026-2031.

Which product segment leads consumption?

Passenger car motor oil captured 54.91% of the 2025 volume and remains the largest segment.

Why are synthetics growing faster than mineral oils?

Mining fleets and large urban operators adopt synthetics for longer drain intervals and lower downtime, driving a 4.08% CAGR for full synthetics through 2026 to 2031.

How is the used-vehicle import rule affecting demand?

The new 15-year age cap refreshes part of the fleet yet preserves a sizable pool of older cars, sustaining demand for both 15W and 5W multigrades.

What is the main challenge for legitimate lubricant suppliers?

Counterfeit and adulterated oils entering through border points undercut pricing and erode consumer trust.

Page last updated on: