Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

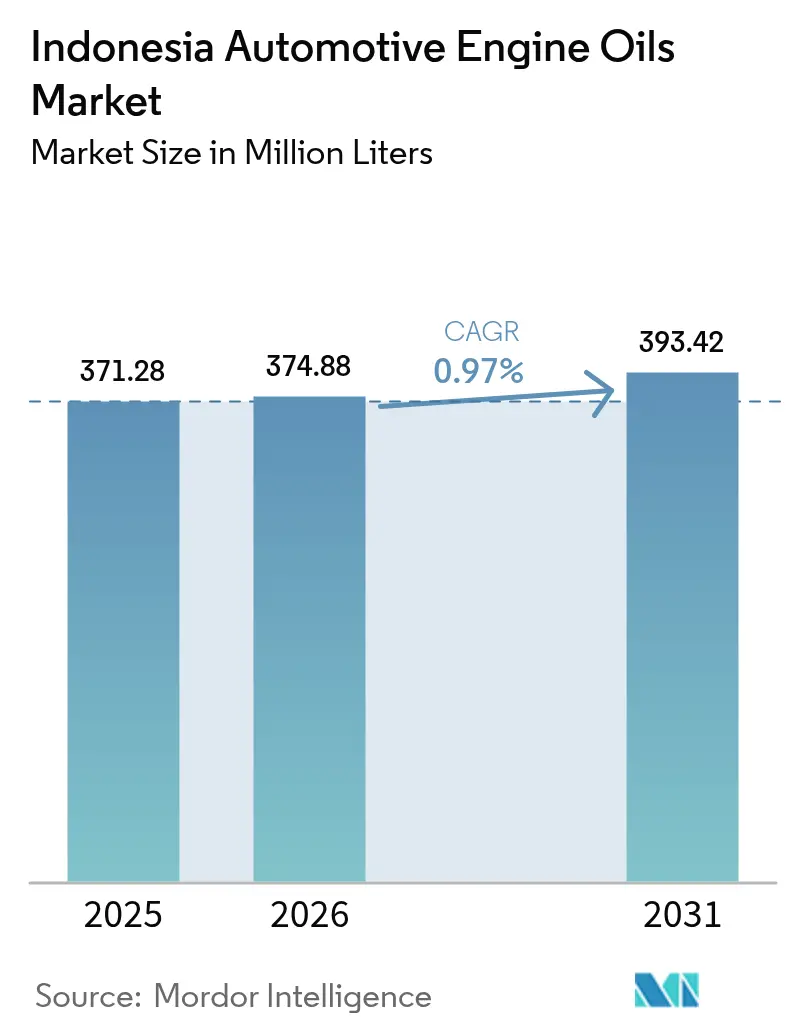

| Base Year Market Size (2025) | 371.28 Million liters |

| Market Volume (2026) | 374.88 Million liters |

| Market Volume (2031) | 393.42 Million liters |

| Growth Rate (2026 - 2031) | 0.97% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Automotive Engine Oils Market Analysis by Mordor Intelligence

The Indonesian Automotive Engine Oils Market size was valued at 371.28 million liters in 2025 and estimated to grow from 374.88 million liters in 2026 to reach 393.42 million liters by 2031, at a CAGR of 0.97% during the forecast period (2026-2031). Persistent population growth, accelerating urbanization, and a vehicle parc that already exceeds 138 million units continue to underpin baseline demand despite macro-economic volatility. Motorcycles remain the backbone of personal mobility, while rising middle-class incomes foster gradual passenger-car penetration. OEM specifications are moving toward low-viscosity synthetic formulations, spurring product mix upgrades even as overall volumes advance at a measured pace. Simultaneously, mandatory Indonesian National Standard (SNI) compliance and the planned Euro 4 fuel transition are elevating the technical threshold for suppliers, rewarding firms that can deliver rapid formulation updates. Competitive intensity is shaped by Pertamina’s cost-advantaged refining base, Shell’s and ExxonMobil’s technology portfolios, and the emergence of Chinese brands that leverage price positioning.

Key Report Takeaways

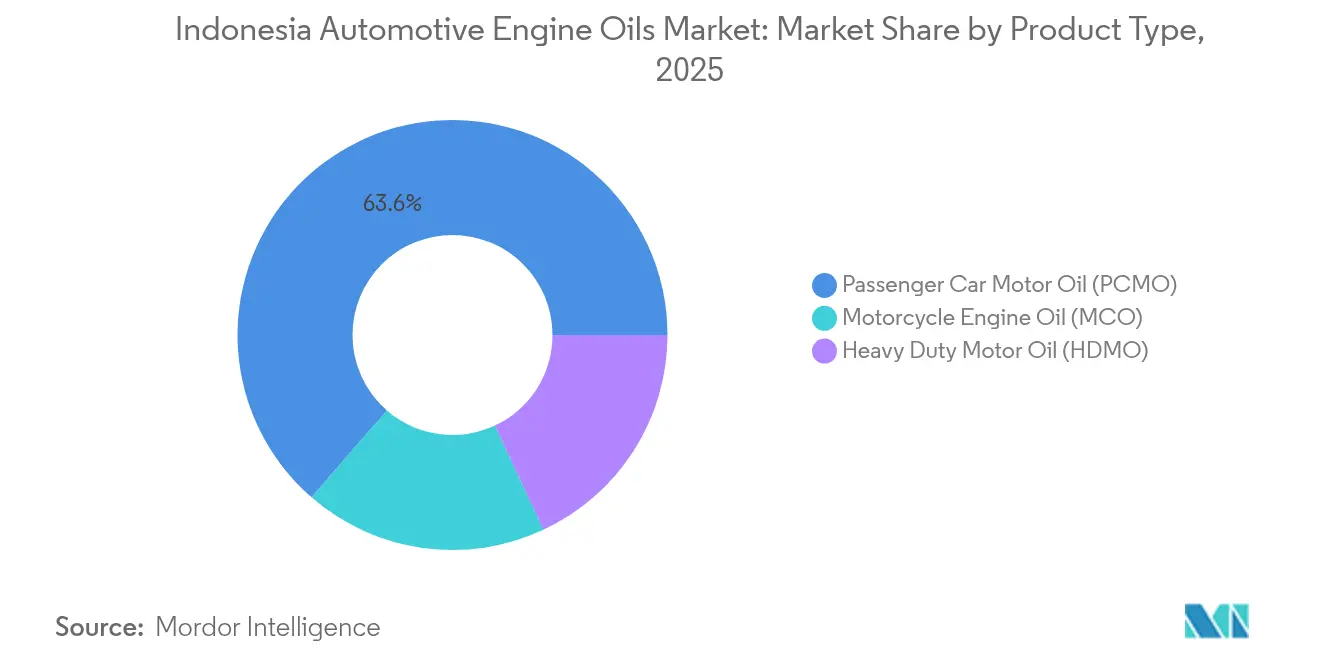

- By product type, passenger car motor oil captured 63.62% of Indonesia automotive engine oil market share in 2025, while motorcycle engine oil is set to expand at a 1.14% CAGR through 2031, the fastest among all resin segments.

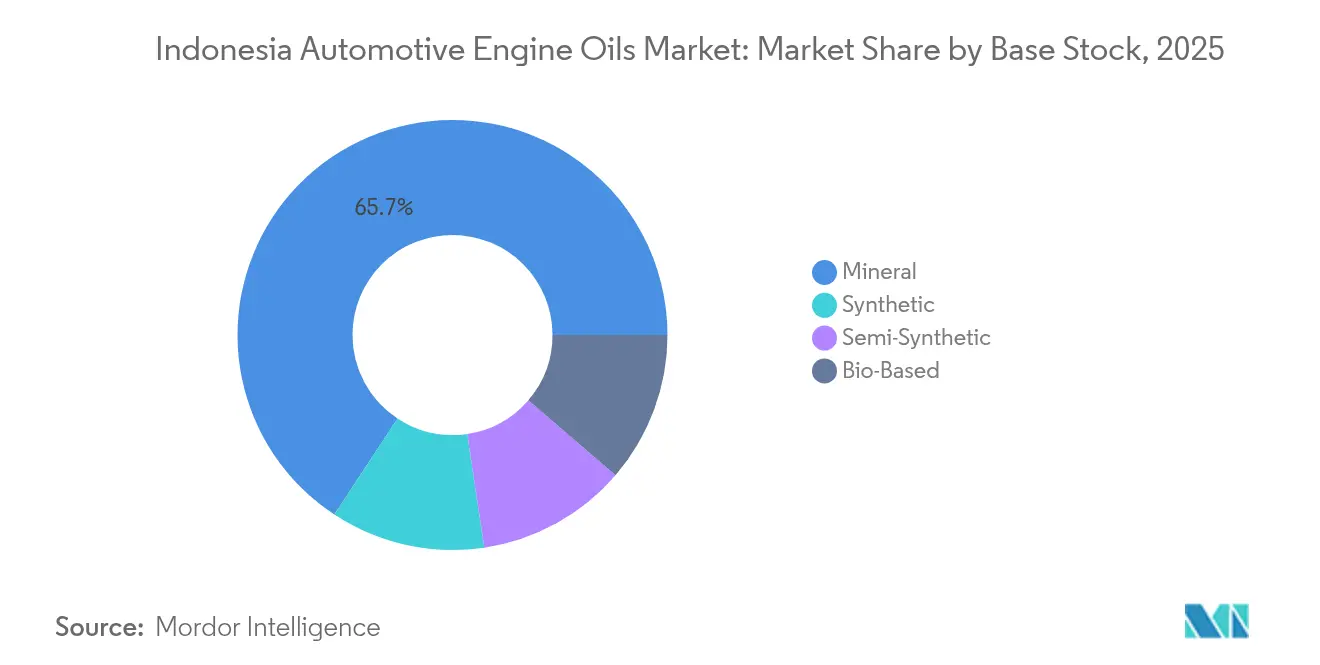

- By base stock, mineral oils commanded 65.74% share of the Indonesia automotive engine oil market size in 2025, while synthetic base stocks are forecast to grow at a 1.21% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth of vehicle parc | +0.4% | Java and Sumatra lead, national influence | Medium term (2-4 years) |

| OEM push toward low-viscosity oils | +0.2% | Jakarta and Surabaya concentrate early adoption | Long term (≥ 4 years) |

| Rising motorcycle ownership | +0.3% | Urban centers plus emerging cities | Short term (≤ 2 years) |

| Government incentives for cleaner engines | +0.1% | Initial uptake in major metropolitan areas | Long term (≥ 4 years) |

| Ride-hailing fleet expansion | +0.1% | Jakarta, Surabaya, Bandung and tier-2 spillovers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Vehicle Parc Drives Base Demand

Indonesia’s 138 million-unit vehicle population, including 113 million motorcycles, produces an unmatched aftermarket lubricant opportunity. Government tax incentives propelled car sales to 81,230 units in February 2022, a 65% year-on-year jump[1]Coordinating Ministry for Economic Affairs, “Encouraging the National Automotive Industry to Become a Global Player,” ekon.go.id . More cars and two-wheelers translate directly into higher lubricant change frequencies, while new toll roads lengthen average kilometers traveled. These factors shift the Indonesian automotive engine oil market from pure replacement to incremental volume expansion as new vehicle additions consistently outrun fleet retirements.

OEM Specifications Shift Toward Advanced Formulations

Global and local automakers are standardizing on API SP or higher for gasoline engines and advocating 0W or 5W grades to optimize thermal management and fuel economy[2]Motor Plus-Online, “API SP Adoption,” motorplus-online.com. Motorcycle applications lag at API SN but are expected to follow by 2027. Motul and other premium brands already promote 10W-30 and 10W-40 synthetics for future-proofing against tighter emission norms. Suppliers enjoying early-mover advantage in synthetic technology can achieve double-digit margin premiums while educating workshops on viscosity migration. Consumers gravitate toward better cold-start protection and extended service intervals, accelerating the premiumization of the Indonesia automotive engine oil market.

Rising Motorcycle Ownership Sustains Volume Growth

Two-wheelers generated 6.91 million units of domestic production and 6.33 million units of sales in 2024, reinforcing Indonesia’s status as Southeast Asia’s largest motorcycle hub. Automatic transmission bikes command over 90% of purchases, necessitating JASO MB-compliant oils engineered for CVT systems. Frequent oil-change intervals caused by high-temperature urban stop-and-go riding maintain robust baseline demand. Exports of 572,000 completely built motorcycles further drive production utilization and pull through lubricant requirements aligned with international OEM standards.

Government Incentives Accelerate Technology Adoption

The state offers 3% PPnBM DTP for hybrids and 10% VAT relief for battery electric vehicles that achieve 40% local content. Electric car sales hit 37,619 units in 2024, yet still represent just 6.25% of passenger-vehicle volume. Euro 4 fuel implementation, set for 2027–2028, will mandate lower sulfated ash formulations to safeguard catalytic converters. B40 biodiesel from January 2025 already requires oxidation-stable diesel lubricants, spurring ExxonMobil’s release of Mobil Delvac 1™ B40 variants. These regulations reward suppliers with agile research and development and certification capabilities.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthening drain intervals | −0.2% | Higher in urban centers with newer vehicles | Medium term (2-4 years) |

| Uptake of electric two-wheelers | −0.1% | Jakarta, Surabaya, Bandung subsidy clusters | Long term (≥ 4 years) |

| Counterfeit/adulterated lubricants | −0.1% | Price-sensitive rural markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lengthening Drain Intervals Reduce Consumption Frequency

Synthetic oils support 10,000-kilometer service intervals versus 5,000 kilometers for conventional blends. Newer low-cost green cars employ tighter tolerances and smaller sumps that cut per-service volumes. Fleet managers favor higher-priced synthetics because lifetime cost per kilometer falls, trimming absolute liters consumed even as revenue per liter rises. Motorcycles adopt improved circulation that extends oil life, yet congestion-induced stop-start driving partly offsets the interval expansion.

Electric Two-Wheelers Introduce Long-Term Displacement Risk

Government subsidies covering 35,714 battery-electric motorcycles create early-stage momentum, but electric units still form just 0.05% of the national fleet. High upfront costs and sparse charging infrastructure impede rapid adoption, according to ITB research. Yet policy support and falling battery prices could accelerate uptake beyond conservative forecasts, posing a structural headwind to the Indonesian automotive engine oil market in the long run.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Passenger cars lead while motorcycles pace growth

The Indonesia automotive engine oil market size for passenger car motor oil accounted for 63.62% of the total volume in 2025. API SP upgrades and 0W-20 viscosity adoption underpin premiumization. OEM factory-fill contracts provide early volume security and brand loyalty that extend into the aftermarket. Heavy-duty motor oil serves logistics and agriculture, with B40-ready formulations becoming a prerequisite.

Motorcycle engine oil volume is projected to climb at a 1.14% CAGR through 2031. Continuous city riding elevates lubricant stress, supporting higher change frequencies. JASO MB specifications for automatic clutch designs create differentiation opportunities, illustrated by Shell Advance City Scooter’s full-synthetic launch in June 2025. As disposable income rises, riders shift from mineral 20W-50 to semi-synthetic 10W-40, lifting average revenue per liter.

By Base Stock: Mineral holds volume but synthetics capture value

Mineral formulations accounted for 65.74% of Indonesia automotive engine oil market share in 2025, driven by state-owned Pertamina’s integrated refining economics. Large-scale depots and 5,000 fuel stations guarantee nationwide availability, reinforcing consumer trust. Semi-synthetics act as a price-performance bridge, appealing to cost-sensitive fleets that still require API SP compliance.

The synthetic segment posted a 1.21% CAGR toward 2031, supported by OEM low-viscosity mandates and extended drain-interval economics. Pertamina’s Group III base-oil JV in Dumai and Shell’s USD 12 million grease plant in Marunda localize supply chains, reducing import costs and lead times. Bio-based lubricants leveraging domestic palm oil remain nascent but align with future sustainability mandates.

Geography Analysis

Java anchors the Indonesian automotive engine oil market through dense vehicle ownership, OEM assembly hubs, and high ride-hailing penetration. Jakarta’s Jabodetabek megacity concentrates 30% of national passenger cars and 25% of motorcycles, driving workshop demand for both mineral and synthetic grades. The completed Trans-Java Toll Road has lengthened trip distances, lifting per-vehicle lubricant consumption. Pertamina’s Plumpang depot and Shell’s Marunda plant ensure same-day fulfillment across Greater Jakarta.

Sumatra is buoyed by palm-oil plantations and logistics corridors that utilize heavy-duty diesel engines. Mining expansion in South Sumatra and Riau accelerates the uptake of high-performance synthetics that can withstand abrasive particulates and B40 fuel blends. Meanwhile, Kalimantan’s coal and nickel operations present concentrated industrial demand clusters that favor suppliers offering on-site lubrication management.

Infrastructure gaps inflate logistics costs, so suppliers with regional warehouses and distributor partnerships gain a service-level edge. Government plans for new mining smelters and the planned Batang Toru hydropower project will increase heavy equipment fleets, creating additional pull for diesel engine oils.

Competitive Landscape

The market is highly consolidated in nature. Shell Indonesia operates a local blending plant that produces 99% of its domestic portfolio and is completing a USD 12 million grease expansion aimed at 12 million liters per year. Digital platforms are becoming a battleground. Shell’s Value Improvement Program offers data analytics on oil condition, while Pertamina’s RFID inventory tracking enhances reseller transparency. These service extensions lock in workshops and fleets, raising switching costs and intensifying competition within the Indonesia automotive engine oil market.

Indonesia Automotive Engine Oils Industry Leaders

BP plc

Chevron Corporation

Exxon Mobil Corporation

PT Pertamina

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Shell Indonesia launched Shell Advance City Scooter full-synthetic oil in 10W-40 and 10W-30 grades priced at USD 4.23 to 4.83 per liter.

- March 2024: Pertamina Lubricants relaunched Meditran Series commercial oils meeting Mercedes-Benz 228.3 and Volvo VDS-3 specifications.

Indonesia Automotive Engine Oils Market Report Scope

By Product Type

| Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Heavy Duty Motor Oil (HDMO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Motorcycle Engine Oil (MCO) | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades |

By Base Stock

| Mineral |

| Synthetic |

| Semi-Synthetic |

| Bio-Based |

| By Product Type | Passenger Car Motor Oil (PCMO) | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Heavy Duty Motor Oil (HDMO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Motorcycle Engine Oil (MCO) | 0W-XX | |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| By Base Stock | Mineral | |

| Synthetic | ||

| Semi-Synthetic | ||

| Bio-Based | ||

Key Questions Answered in the Report

What is the current volume of engine oil consumed in Indonesia?

The market reached 374.88 million liters in 2026 and is forecast to grow to 393.42 million liters by 2031.

Which resin segment accounts for the largest share?

Passenger car motor oil led with 63.62% of total volume in 2025.

Which base stock is growing fastest?

Synthetic formulations are expected to register a 1.21% CAGR through 2031 due to OEM low-viscosity mandates.

How significant is electric-vehicle impact on lubricant demand?

EVs formed just 0.05% of Indonesia's fleet in 2024, so displacement risk remains limited near term.

Who commands the largest domestic share?

State-owned Pertamina Lubricants controls 36% of national volume.

How will Euro 4 fuel standards affect formulations?

Suppliers must reduce sulfated ash and enhance oxidation stability to protect aftertreatment systems when Euro 4 is implemented by 2028.

Page last updated on: