Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

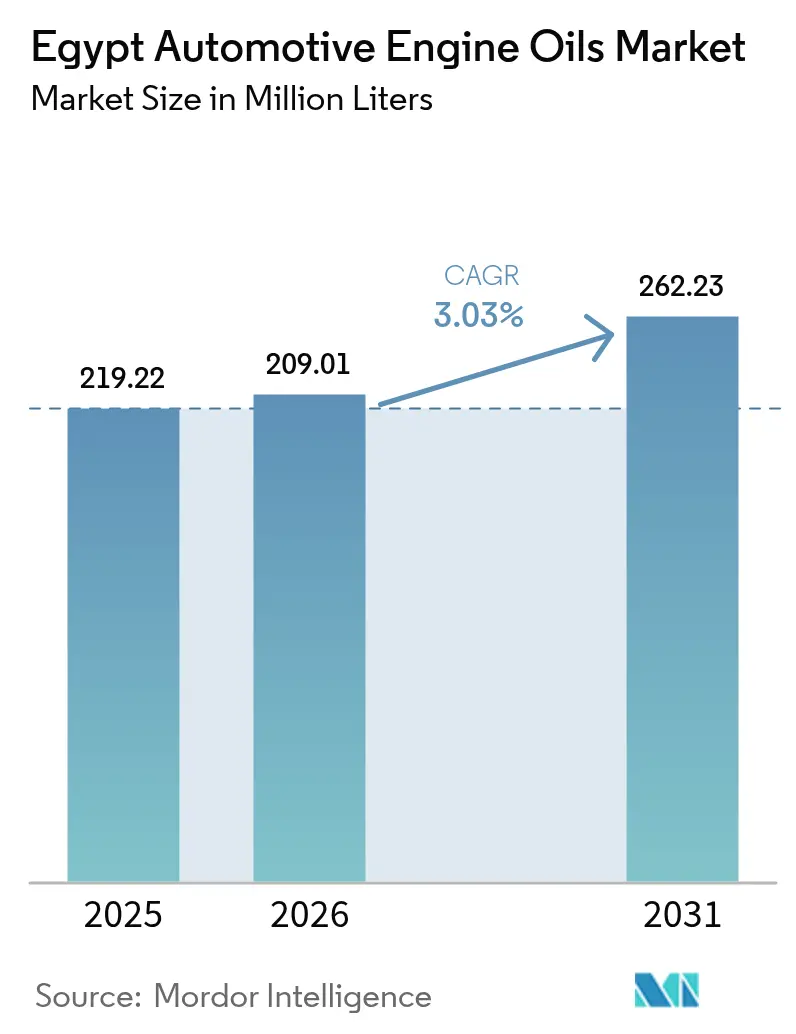

| Base Year Market Size (2025) | 219.22 Million liters |

| Market Volume (2026) | 209.01 Million liters |

| Market Volume (2031) | 262.23 Million liters |

| Growth Rate (2026 - 2031) | 3.03% CAGR |

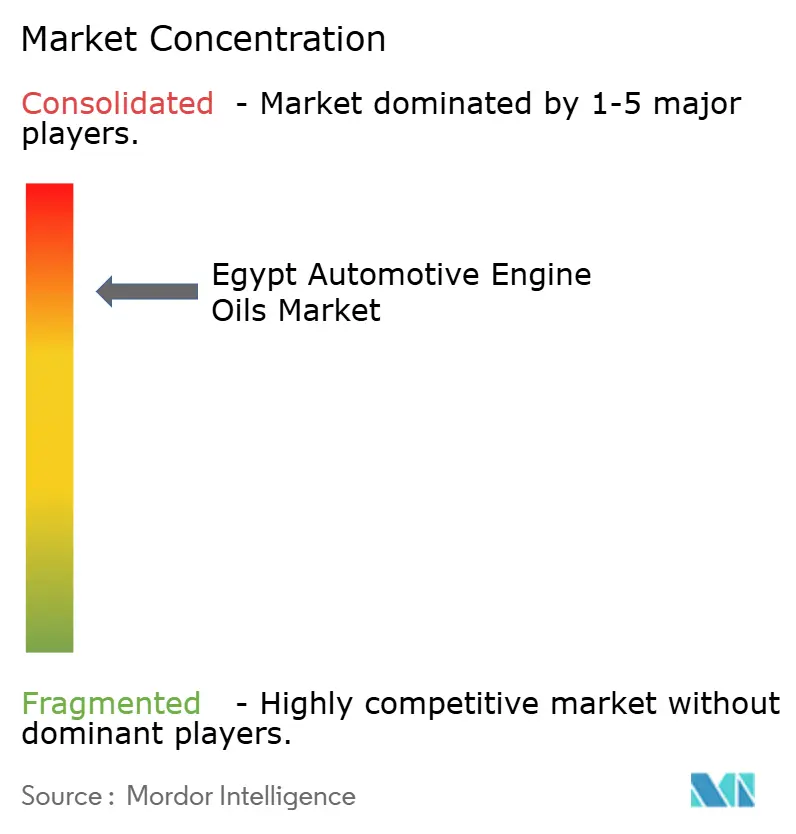

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Automotive Engine Oils Market Analysis by Mordor Intelligence

The Egypt Automotive Engine Oils Market size is projected to be 219.22 Million liters in 2025, 209.01 Million liters in 2026, and reach 262.23 Million liters by 2031, growing at a CAGR of 3.03% from 2026 to 2031. The egypt automotive engine oils market is expanding because economic activity is rebounding, infrastructure spending is rising, and the country is investing in alternative-fuel programs that keep internal-combustion vehicles in circulation. Market growth is also tied to local refinery upgrades that secure base-oil supply, the steady renewal of Egypt’s large passenger-car fleet, and increasing demand from commercial vehicles that undergo more frequent service cycles. Competitive pressure has intensified as multinational and regional formulators add synthetic and semi-synthetic grades tailored for hot-climate performance while guarding against counterfeit products. Currency volatility and additive import restrictions temper near-term volume growth, yet investment in quality control and domestic blending capacity shields the egypt automotive engine oils market from severe supply shocks. The industry’s evolving product mix and supportive energy policy framework create measured opportunities for premium lubricants through 2030.

Key Report Takeaways

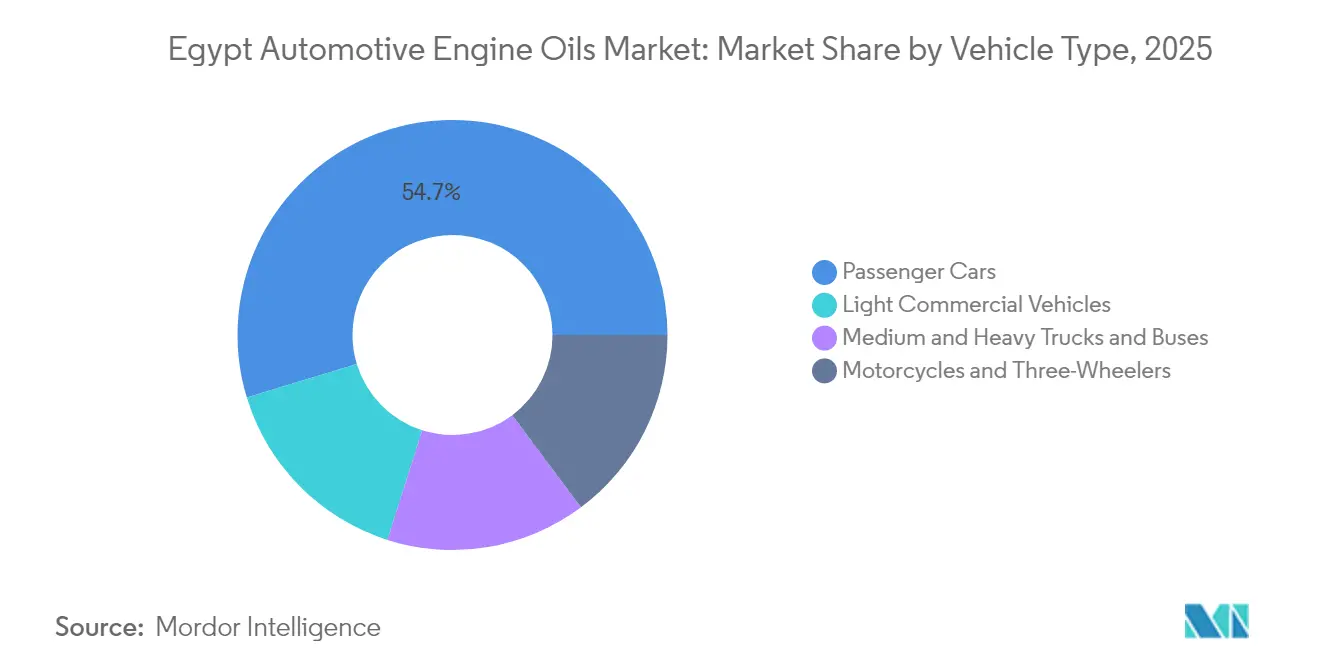

- By vehicle type, passenger cars held 54.70% of the egypt automotive engine oils market share in 2025, whereas light commercial vehicles are projected to expand at a 3.47% CAGR through 2031.

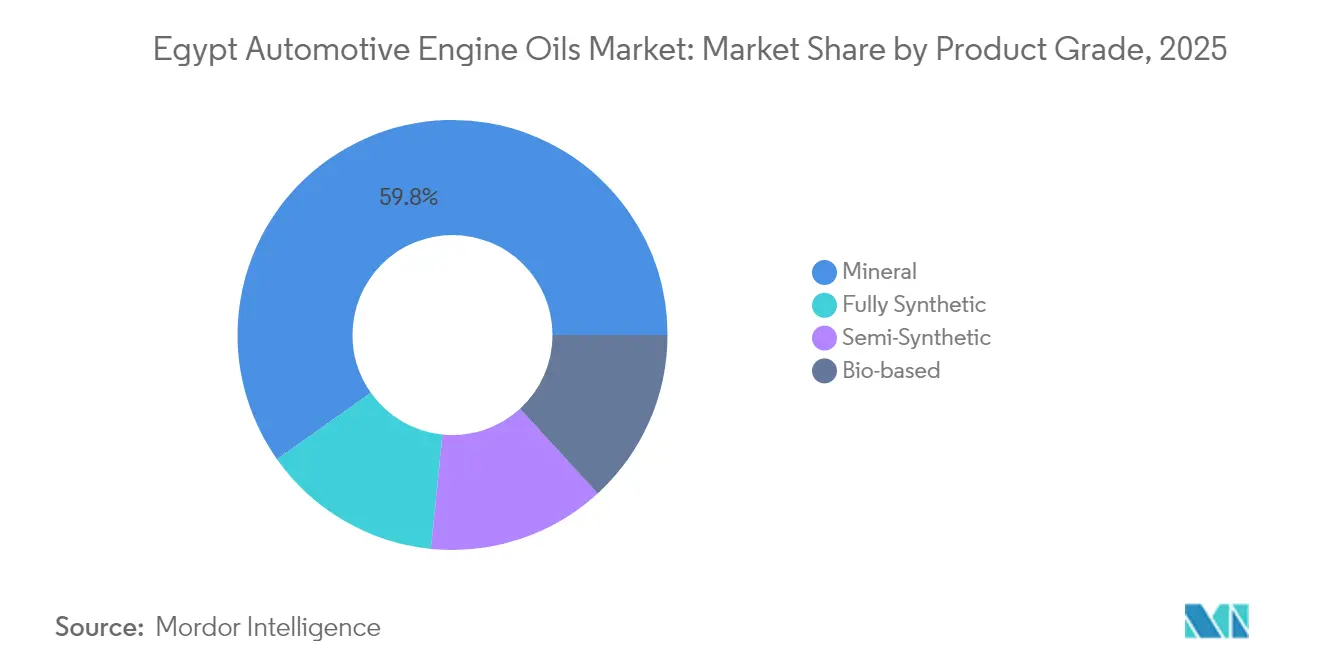

- By product grade, mineral accounted for 59.80% of the egypt automotive engine oils market size in 2025, and fully synthetic is advancing at a 3.55% CAGR during the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Automotive Engine Oils Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Vehicle Parc | +0.8% | National, concentrated in Greater Cairo and Alexandria | Medium term (2-4 years) |

| Rising Penetration of Synthetic and Semi-Synthetic Oils | +0.6% | Urban centers with newer vehicle concentrations | Long term (≥ 4 years) |

| Government CNG-Conversion Targets Boosting Oil Change Frequency | +0.4% | National rollout with priority corridors | Short term (≤ 2 years) |

| Local Refinery Upgrades Enabling Higher-Quality Base-Oil Supply | +0.3% | National supply chain benefits | Medium term (2-4 years) |

| Nano-Additive R&D for Hot-Climate Performance | +0.2% | Desert regions and high-temperature applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Vehicle Parc

Egypt’s registered private-car fleet reached 5.23 million in 2023, and fleet growth parallels a 7.1% rise in manufacturing output that lifts commercial transport demand. Public investment of EGP 115 billion in green transportation has multiplied vehicle kilometers traveled across highways, bus corridors, and ride-hailing services. Higher urbanization and a 104 million population unlock sustained car ownership, which raises lubricant demand per maintenance cycle. Fleet expansion also drives service-network density, prompting distributors to increase egypt automotive engine oils market coverage in secondary cities.

Rising Penetration of Synthetic and Semi-Synthetic Oils

Fully synthetic grades grow faster than the overall egypt automotive engine oils market because late-model engines need tighter viscosity stability and extended drain intervals. Local research shows nano-additive packages that improve thermal conductivity by 10.4%, which addresses Egypt’s high-ambient temperatures. Assembly plants that partner with global OEMs are publishing service-fill specifications that elevate end-user preference for premium oils, while semi-synthetics offer a cost bridge for older vehicles making the transition[1]MDPI, “Thermal Conductivity Enhancement of Engine Oils with Carbon-Nanotube Additives,” mdpi.com .

Government CNG-Conversion Targets Boosting Oil-Change Frequency

A national program finances 80,000 vehicle conversions at a 3% fixed interest rate, backed by the build-out of 1,000 CNG stations. Dual-fuel engines require shorter oil-change intervals to mitigate fuel dilution, increasing per-vehicle lubricant consumption even as gasoline usage decelerates. Taxi and delivery fleets dominate early adoption, reinforcing engine-oil volumes among high-mileage units in the egypt automotive engine oils market.

Local Refinery Upgrades Enabling Higher-Quality Base-Oil Supply

Alexandria Mineral Oils Company lifted quarterly output to 335,000 tons, while the Mostorod refinery adds 4.7 million t/y of finished products that include Group I/II base stocks. Reduced dependence on imports stabilizes blending margins and supports locally tailored formulations. Domestic supply also insulates the egypt automotive engine oils industry from global freight disruptions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FX Volatility and Import Restrictions on Additives/Base Oils | -0.5% | National supply chain impacts | Short term (≤ 2 years) |

| Proliferation of Low-Grade/Re-Refined Counterfeit Oils | -0.3% | Urban markets with price-sensitive segments | Medium term (2-4 years) |

| Gradual EV and Hybrid Uptake Reducing Long-Term Demand | -0.2% | Urban centers with early EV adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FX Volatility and Import Restrictions on Additives/Base Oils

Exchange-rate swings widened raw-material costs and created letter-of-credit delays worth USD 7-8 billion before mid-2024 reforms. Blenders face higher working-capital demands when sourcing specialty antioxidants and viscosity improvers. Price jumps ripple through retailers, delaying synthetic-grade adoption in the egypt automotive engine oils market[2]International Monetary Fund, “Arab Republic of Egypt Article IV Consultation 2024,” imf.org.

Proliferation of Low-Grade/Re-Refined Counterfeit Oils

Counterfeit volumes undercut authentic brands by 20-40% in retail price and can damage engines, eroding consumer trust. Color, odor, and tamper-evidence-seal checks are adopted as counter-measures, yet distribution reach of informal sellers remains extensive. Substandard products squeeze legitimate suppliers’ market share and constrain the premiumization trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Fleets Drive Service Intensity

Light commercial vehicles posted a 3.47% CAGR, pacing ahead of passenger cars because freight, construction, and last-mile delivery sectors surged after private investment jumped 30% to EGP 133.1 billion. The egypt automotive engine oils market size for commercial fleets will approach 101.2 million liters by 2031, fueled by higher mileage accumulation per unit. Commercial buyers contract bulk supplies, which encourages synthetic formulations that lower downtime, while CNG conversions magnify change-frequency multipliers. Passenger cars keep a 54.70% egypt automotive engine oils market share but record slower expansion owing to an aging parc and tighter household budgets. Still, population growth keeps absolute volumes rising, securing a baseline for aftermarket sales and service workshops.

In motorcycles and three-wheelers, a policy that bans fully built-unit imports sustains localized assembly lines and contains category growth. Heavy trucks and buses benefit from the USD 3.6 billion savings in fuel imports after natural-gas production recovered, which redirects government spending toward road-fleet renewal. Fleet owners adopt long-drain interval oils with higher TBN values to minimize workshop visits—an emerging niche that multinational formulators address through CK-4 and FA-4 viscosity grades. Combined, these interactions ensure a broad, durable customer base across all vehicle categories, maintaining a resilient foundation for the egypt automotive engine oils market through 2031.

By Product Grade: Premium Shift Amid Mineral Dominance

Mineral oils retain a 59.80% share because over half the national fleet is more than 12 years old and favors low-cost 20W-50 viscosity. The segment, totaling 179.9 million liters in 2025, grows below the market average. Meanwhile, fully synthetic volumes expand at 3.55% CAGR, pushing the egypt automotive engine oils market size for synthetics to nearly 48 million liters by 2031. High-temperature shear-stability and detergency benefits meet OEM warranty requirements for turbocharged gasoline direct-injection engines. Semi-synthetics bridge price gaps and help modernize lube bays, while high-mileage blends with seal conditioners tap the 1.4 million vehicles above 200,000 kilometers.

Nano-additive R&D supports a local premium pivot. Prototype SN Plus 5W-30 products using dispersed graphene platelets cut wear by 17% in dynamometer tests under 45 °C ambient conditions. Domestic blenders exploit upgraded base-oil streams from Mostorod and AMOC refineries, ensuring shorter lead times and lower landed cost relative to imports. The premium shift improves gross margins and encourages multinational licensors to approve Egyptian blend plants, broadening the range of specification-compliant oils in retail channels. Overall, a steady climb in quality grades keeps the egypt automotive engine oils market balanced between affordability and performance.

Geography Analysis

Economic output is heavily concentrated in Greater Cairo and Alexandria, which together account for nearly half of registered vehicles and anchor distribution warehousing for imported additives and packaging. The egypt automotive engine oils market size in these metro regions exceeds 152.7 million liters in 2025. Dense traffic and ridesharing platforms escalate drain intervals, feeding brisk demand for fast-fit centers. Alexandria’s seaport throughput sustains logistics fleets and marine-adjacent workshops that favor bulk containers and metered dispensing systems.

Secondary cities—such as Mansoura, Tanta, and Assiut—gain share as industrial corridors expand. A USD 10 billion solar-manufacturing hub in the New Administrative Capital and the 1,000-km highway revamp drive lubricant needs for construction machinery and transport fleets. Distribution companies respond with regional depots and digital ordering portals that cut delivery times to 48 hours. Rural highways experience higher dust loading, steering fleet operators toward higher-viscosity, high-TBN oils with superior particulate suspension capacity.

Desert and Red Sea governorates register low volumes but premium per-unit revenue, because mining and petroleum service vehicles operate in 50 °C ambient conditions that necessitate synthetic 10W-60 or 5W-40 formulations. Seasonal tourism peaks also draw long-haul buses along the Red Sea corridor, enlarging Q3 lubricant sales. Enhanced logistics corridors through Suez and Port Said continue to improve supply resilience, supporting a nationwide footprint for the egypt automotive engine oils market.

Competitive Landscape

Global suppliers such as Shell, ExxonMobil, BP, Chevron, and TotalEnergies dominate branded shelf space, yet face growing rivalry from Saudi and Emirati portfolio entrants that seize upstream integration advantages. Shell leverages technical partnerships with OEM aftersales networks to maintain product approval lists, while ExxonMobil expands franchise-workshop packages for independent garages. BP’s possible divestiture of Castrol could realign supply contracts and open white-label gaps for regional blenders.

Domestic manufacturers use refinery proximity to launch competitive SKUs. AMOC markets Group II-based blends under its Delta brand, offering 15-40% lower ex-gate prices than imports. Counterfeit risk compels leading brands to embed QR code traceability. Some distributors pilot subscription models bundling oil changes with roadside assistance, stimulating customer stickiness in the egypt automotive engine oils market.

Strategic investments focus on environmental stewardship. TotalEnergies pilots closed-loop used-oil collection with cement kilns for energy valorization, and Castrol’s MoreCircular program coordinates with Safety-Kleen to re-refine waste oil. LabWare’s LIMS deployment at EGPC labs raises test throughput by 25%, improving quality audits. Nano-additive R&D alliances between Cairo University and local blenders promise performance differentiation. Competitive intensity will remain moderate as scale economies balance with growing niche specialization.

Egypt Automotive Engine Oils Industry Leaders

ExxonMobil Corporation

Misr Petroleum

TotalEnergies

Shell plc

BP plc (Castrol)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ADNOC Distribution partnered with TotalEnergies Marketing Egypt (TEME) to launch ADNOC Voyager lubricants in Egypt. The selected ADNOC Voyager products are manufactured at TEME's blending facility in Borg El Arab, supporting Egypt's industrial growth, creating employment opportunities, enhancing local supply chains, and reducing reliance on imports.

- February 2025: Alexandria Company for Petroleum Additives (ACPA) formed a partnership with Amalie, an American company, to manufacture and distribute Amalie lubricants across Egypt. The collaboration, formalized through a Memorandum of Understanding, includes plans for the production and marketing of synthetic oil.

Egypt Automotive Engine Oils Market Report Scope

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Trucks and Buses |

| Motorcycles and Three-Wheelers |

By Product Grade

| Mineral |

| Semi-Synthetic |

| Fully Synthetic |

| Bio-based |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium and Heavy Trucks and Buses | |

| Motorcycles and Three-Wheelers | |

| By Product Grade | Mineral |

| Semi-Synthetic | |

| Fully Synthetic | |

| Bio-based |

Key Questions Answered in the Report

What is the forecast volume for egypt automotive engine oils by 2031?

The market is projected to reach 262.23 million liters by 2031, growing at a 3.03% CAGR.

Which vehicle category is growing fastest in egypt automotive engine oils consumption?

Light commercial vehicles lead with a 3.47% CAGR thanks to higher mileage and CNG conversion incentives.

Which product grade is gaining share in Egypt’s lubricant sector?

Fully synthetic oils expand at a 3.55% CAGR as OEMs demand premium performance in newer engines.

How do CNG conversions affect engine-oil demand in Egypt?

Dual-fuel engines require more frequent oil changes, adding incremental volume on top of fleet growth.

Page last updated on: