Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

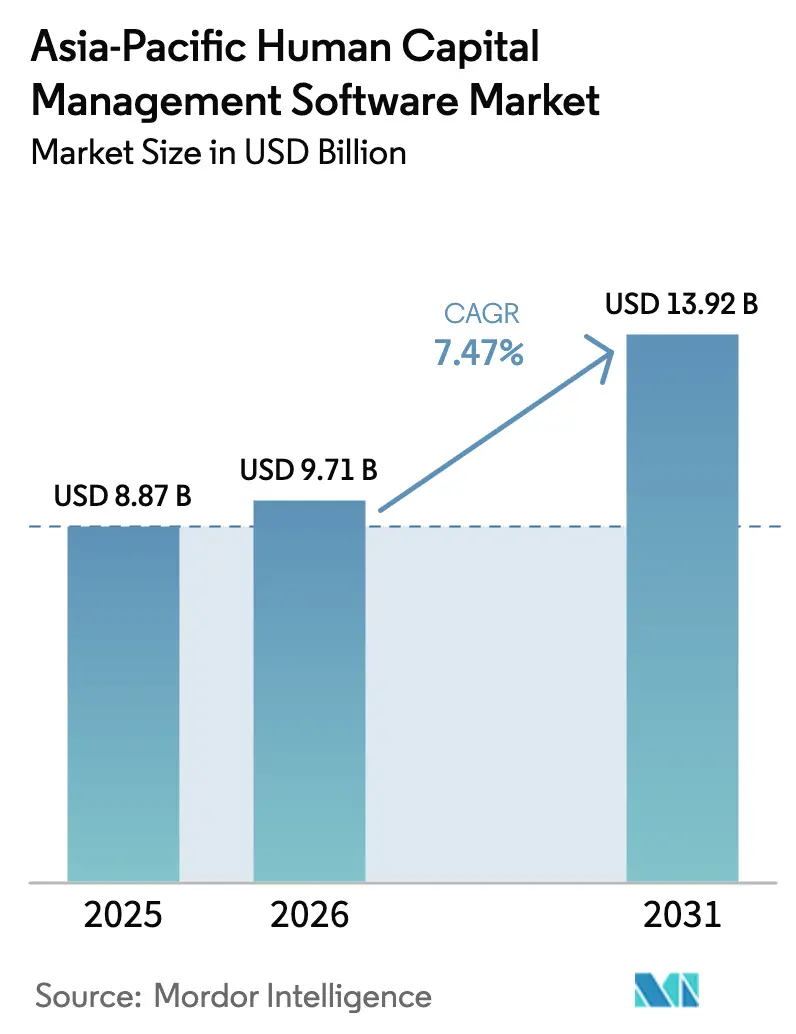

| Base Year Market Size (2025) | USD 8.87 Billion |

| Market Size (2026) | USD 9.71 Billion |

| Market Size (2031) | USD 13.92 Billion |

| Growth Rate (2026 - 2031) | 7.47% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Human Capital Management Software Market Analysis by Mordor Intelligence

The Asia-Pacific human capital management software market size is expected to grow from USD 8.87 billion in 2025 to USD 9.71 billion in 2026 and is forecast to reach USD 13.92 billion by 2031 at 7.47% CAGR over 2026-2031. Cloud-first strategies, fast regulatory change, and skills shortages are prompting enterprises to modernize HR platforms, while venture funding gives local vendors the balance-sheet strength to challenge global incumbents. Skills-based talent models, payroll digitalization mandates, and AI-powered employee-service chatbots are expanding demand beyond core HR into adjacent talent and analytics modules. At the same time, privacy rules that require in-country data storage are reshaping data-center footprints, fueling incremental spending on secure cloud regions. Competitive intensity remains moderate as regional specialists gain share by shipping statutory updates faster than monolithic global suites.

Key Report Takeaways

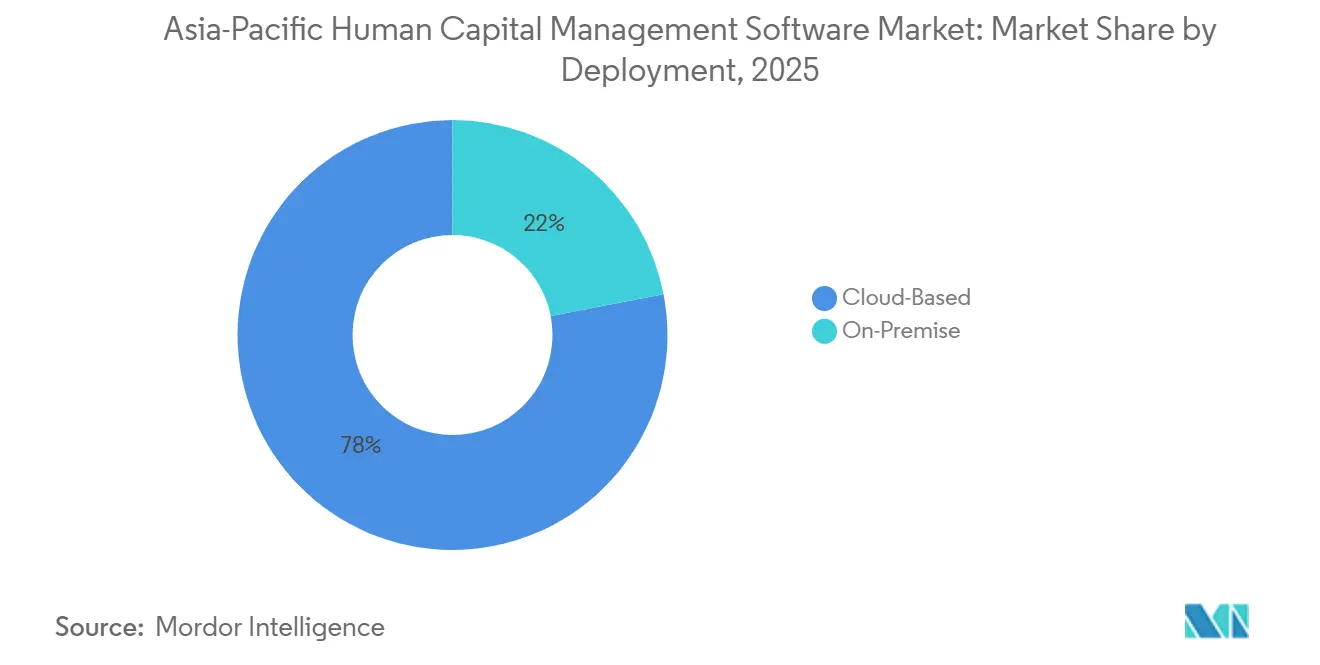

- By deployment, cloud-based solutions captured 78.03% share of Asia-Pacific human capital management software market's 2025 revenue, and this share is widening as the model advances at 7.51% CAGR through 2031.

- By organization size, large enterprises held 63.89% share of Asia-Pacific human capital management (HCM) software market's 2025 revenue, yet small and medium-sized enterprises are expanding the fastest at 7.91% CAGR to 2031.

- By application, core HR generated 29.77% of Asia-Pacific HCM software market's 2025 sales, while performance and talent management is the fastest-growing module at 7.84% CAGR through 2031.

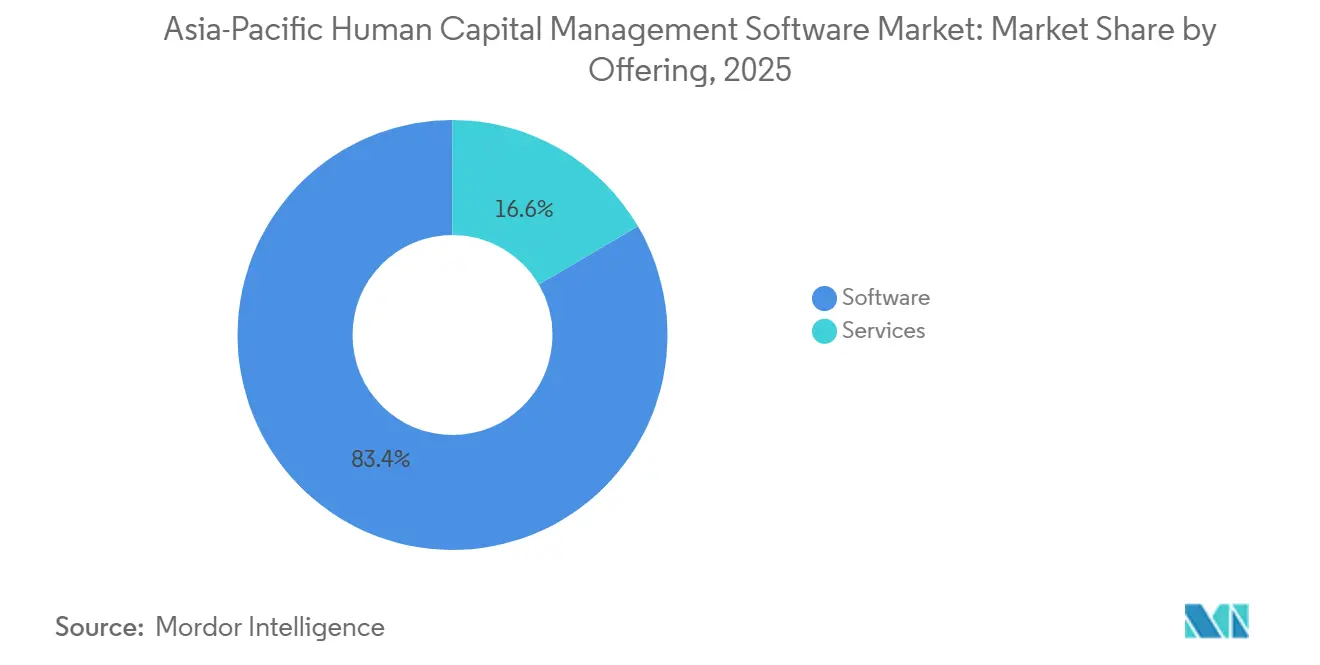

- By offering, software platforms represented 83.43% of 2025 spending, but services revenue is accelerating at 8.13% CAGR on the back of implementation demand.

- By end-user industry, banking, financial services, and insurance commanded 28.17% share in 2025, whereas retail and e-commerce will post the highest growth at 8.07% CAGR to 2031.

- By geography, China accounted for 31.23% of regional sales of APAC HCM Software amrket in 2025, yet India is the fastest-expanding market at 8.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Human Capital Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Cloud Adoption Across Asia-Pacific Enterprises | +1.8% | APAC core, Indonesia, Malaysia | Short term (≤ 2 years) |

| Growing Demand for Mobile HCM Applications | +1.2% | Singapore, Australia, Japan | Short term (≤ 2 years) |

| Regulatory Mandates for Digital Payroll Compliance | +1.3% | China, India, Japan, Australia, Singapore | Medium term (2-4 years) |

| Increase in Demand for Talent Mobility | +1.0% | China, India, Singapore | Medium term (2-4 years) |

| Localization of AI-Driven Multilingual HR Chatbots for Mid-Market Firms | +0.9% | India, Japan, South Korea, Southeast Asia | Medium term (2-4 years) |

| Integration of Cross-Border Gig-Workforce Platforms | +0.7% | Singapore, Hong Kong, Malaysia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Cloud Adoption Across Asia-Pacific Enterprises

Enterprises are replacing capital-intensive on-premise systems with subscription-priced cloud suites to reduce total cost of ownership and accelerate innovation cycles. Regional data-center expansions in Sydney, Singapore, Tokyo, and Mumbai allow vendors to address strict residency rules while offering modern micro-services architectures that shorten release cadences.[1]Workday Newsroom, “Workday Opens New Data Centers Across Asia Pacific,” workday.com Mid-market buyers benefit most because cloud deployments remove the need for dedicated IT staff and server rooms, supporting scale-as-you-grow head-count models. Even regulated industries that once demanded air-gapped environments now pilot hybrid stacks that pin sensitive master data on-premise but run analytics in the cloud. The ability to toggle workloads between private and public clouds without re-platforming has become a key selection criterion, favoring vendors with containerized services and stateless integration gateways.

Regulatory Mandates for Digital Payroll Compliance

Rapid-fire statutory changes, from Indonesia’s CORETAX rollout to Vietnam’s electronic social-insurance books, require payroll engines that ship quarterly content packs rather than annual upgrades.[2]Forvis Mazars, “APAC Payroll Newsletter 2025 Issue 1,” forvismazars.com Vendors with in-house compliance teams and country-specific roadmaps differentiate by offering “day-one readiness” whenever governments revise brackets, allowances, or contribution formulas. Hong Kong’s eMPF platform, launching in phases through 2025, is a case in point: providers must embed contribution-submission APIs and portfolio-switch workflows or risk client attrition. As more tax authorities demand real-time payroll reporting, cloud architectures that support micro-batch submissions and audit-quality data trails gain further momentum.

Localization of AI-Driven Multilingual HR Chatbots for Mid-Market Firms

Conversational agents that speak Mandarin, Japanese, Bahasa, and Hindi now resolve routine HR queries and process leave requests, cutting service-center workload by up to 70% in early pilots.[3]OCBC Bank, “OCBC Launches AI-Powered HR Chatbot,” ocbc.com Pre-trained language models, fine-tuned on regional HR policies, allow vendors to sell plug-and-play chatbots without costly client-side training data. OCBC’s deployment proves the model at enterprise scale, while Zoho and Darwinbox are productizing stripped-down assistants that target firms with fewer than 500 employees. Integration with core HR ensures that the bot can surface personalized balances and policy eligibility in real time. Wider adoption hinges on robust back-end security because the chatbot touches sensitive data, prompting vendors to certify ISO 27001 controls to clear procurement hurdles.

Integration of Cross-Border Gig-Workforce Platforms

The region’s platforms must now classify drivers, riders, and freelancers as employees in several jurisdictions, forcing enterprises to unify contingent-labor management on a single system of record. SAP Fieldglass and similar tools now ship jurisdiction-specific pay templates, audit trails, and algorithmic scheduling that comply with Australia’s new minimum-standards regime.[4]SAP SE, “SAP Fieldglass Vendor Management System,” sap.com For regional headquarters orchestrating talent across Hong Kong and Singapore, a harmonized contractor ledger reduces misclassification risk and simplifies cost allocations. Vendors that surface consolidated dashboards for employees, contractors, and platform workers create a compelling value proposition as hybrid workforces become the norm.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy and Security Concerns | -0.8% | China, India, Singapore, Japan, Australia | Short term (≤ 2 years) |

| Integration Complexity with Legacy ERP Stacks | -1.1% | Large enterprises across APAC, China SOEs | Medium term (2-4 years) |

| Fragmented Asia-Pacific Labor-Law Landscape | -0.6% | Multi-country operators, regional HQs | Long term (≥ 4 years) |

| Scarcity of HR-Analytics Talent Pool | -0.4% | India, Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity with Legacy ERP Stacks

Many banks and manufacturers run heavily customized SAP ECC or Oracle E-Business Suite instances that cannot be retired overnight. Synchronizing organizational hierarchies, cost centers, and custom payroll logic with a next-generation cloud suite often requires middleware, data-clean-up, and staged rollouts that stretch beyond 18 months. While Workday and SAP SuccessFactors publish starter connectors, niche local payroll engines and government submission portals still demand bespoke APIs, inflating project scope. Consulting-heavy engagements raise the total cost of ownership, deterring budget-constrained clients and slowing overall market conversion. Vendors that bundle migration accelerators and pre-mapped data models reduce this friction, but legacy complexity remains the single biggest drag on implementation velocity.

Privacy and Security Concerns

China’s Personal Information Protection Law and India’s Digital Personal Data Protection Act require in-country storage and stringent cross-border transfer approvals, restricting multinational roll-outs that rely on centralized data hubs. Breach-notification windows of 72 hours in Singapore and Japan compel platforms to embed real-time intrusion detection, encryption at rest, and immutable audit logs. Vendors lacking regional data centers face procurement disqualification in banking and healthcare tenders, limiting addressable market until they establish local points of presence. Compliance investments therefore divert resources that could fund new product innovation, moderating near-term margin expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Infrastructure Drives Scalability

Cloud-based solutions held 78.03% revenue share of the Asia-Pacific human capital management software market in 2025, and the segment is expanding at 7.51% CAGR through 2031. Vendors are adding sovereign cloud regions to satisfy residency laws, which removes the historical barrier that once forced sensitive industries to remain on-premise. Large banks still keep certain payroll engines inside regulated data centers, yet they increasingly pair this core with cloud analytics to model compensation scenarios in near real time. On-premise and hybrid footprints remain relevant, but their road-maps now emphasize API gateways that allow phased migration rather than full-stack upgrades.

Mid-market firms are the biggest beneficiaries because subscription pricing converts fixed hardware cost into variable operating expense, freeing budget for analytics and learning modules. Zoho’s expansion across the Gulf Cooperation Council and Darwinbox’s template-driven roll-outs in Southeast Asia demonstrate that pre-configured cloud stacks can go live in weeks instead of quarters. Vendors that offer single-tenant options for highly regulated entities while keeping a multi-tenant core for everyone else capture divergent buyer preferences within one code base, a strategy expected to propel cloud’s Asia-Pacific human capital management software market share beyond 80% by 2031.

By Application: Skills-Based Talent Systems Gain Traction

Core HR generated 29.77% of 2025 application revenue as every deployment begins with an employee master file and compliance workflows. Performance and talent management is set to be the fastest-growing application at 7.84% CAGR, driven by the pivot from job grids to skills graphs. Internal talent marketplaces built on Workday Skills Cloud or SAP Opportunity Marketplace let CFOs redeploy engineers to high-priority projects without external hiring fees, accelerating pay-back periods.

Payroll remains a regulatory must-have, but differentiation is shifting to adjacent analytics that predict overtime spikes or pay-equity gaps. Workforce-management modules integrate scheduling with point-of-sale data in retail, while learning stacks now embed micro-credentialing to verify upskilling ROI. As these formerly siloed applications converge on a common data model, the Asia-Pacific human capital management software market size allocated to best-of-breed point solutions is expected to shrink, consolidating spend inside unified suites.

By Organization Size: Mid-Market Acceleration Reshapes Buyer Mix

Large enterprises controlled 63.89% of 2025 revenue because complex hierarchies, global scale, and audit overlays necessitate full-function suites integrated with ERP and CRM backbones. However, small and medium-sized enterprises are expanding at a brisk 7.91% CAGR thanks to cloud pricing below USD 10 per employee per month and localized statutory rules that remove the need for in-house payroll experts.

Regional specialists such as SmartHR in Japan and Beisen in China tailor user interfaces and compliance packs for local buyers, lowering change-management friction and raising win rates against global mega-suites. As SMEs scale, they often add modules rather than re-platform, locking in lifetime value for vendors that sell modular licenses. This twin-track dynamic positions the Asia-Pacific human capital management software industry to diversify revenue across both enterprise and mid-market cohorts without cannibalization.

By Offering: Services Revenue Accelerates Amid Implementation Demand

Software still dominates at 83.43% of 2025 spending, yet services are on track to post the highest growth at 8.13% CAGR as clients seek data migration, change management, and ongoing statutory maintenance. System integrators such as Accenture and Infosys bundle accelerators that cut test-cycle time, while payroll outsourcers like Ramco guarantee touchless processing compliance, winning multiple 2025 HR Vendor of the Year awards.

Outcome-based contracts aligned to head-count or payslip volumes are replacing billable-hour arrangements, giving buyers predictable cost and vendors sticky, recurring revenue. As multi-country payroll consolidation projects proliferate, the Asia-Pacific human capital management software market size attributable to managed services is projected to rise, especially among mid-market firms lacking in-house compliance expertise.

By End-User Industry: Retail Automation Outpaces Financial Services

Banking, financial services, and insurance accounted for 28.17% of 2025 revenue because regulators mandate robust audit trails and certified workflow segregation. Retail and e-commerce, however, will clock the fastest expansion at 8.07% CAGR as omnichannel operators grapple with volatile seasonal hiring and gig-worker scheduling.

Manufacturers emphasize workforce-safety analytics and overtime controls, while healthcare providers adopt modules for credential tracking and shift bidding to combat nurse shortages. Government bodies remain cautious cloud adopters given sovereignty rules but increasingly pilot hybrid deployments for learning management. Vendors offering vertical templates shorten blueprint phases, capturing domain-specific demand without starting from scratch each time.

Geography Analysis

China led the Asia-Pacific human capital management software market with 31.23% revenue in 2025, anchored by large state-owned enterprises and technology firms digitizing HR at scale. Beisen’s launch of AI Family 2.0 embeds generative screening and competency assessment, giving domestic buyers a locally hosted, AI-native alternative to global suites. Beijing’s data-sovereignty regime forces foreign vendors to partner with Chinese cloud providers or establish joint ventures, raising both compliance cost and time-to-market. The phased extension of retirement ages that started in 2025 further boosts upgrade cycles as firms must recalibrate pension eligibility across millions of workers.

India, forecast to grow at 8.12% CAGR, is the most dynamic sub-market. Rapid formalization, digital payroll mandates, and venture-backed challengers such as Darwinbox are accelerating adoption, particularly among companies with 200-2,000 employees. The Digital Personal Data Protection Act elevates localization requirements, prompting global vendors to spin up Mumbai or Hyderabad data centers to stay in large-enterprise tenders. Ongoing debate over standing-orders regulations in Karnataka signals more legislative churn ahead, sustaining demand for platforms that ship compliance updates within weeks, not quarters.

Japan’s market is distinctive for its high SaaS penetration yet dominant local champion: SmartHR holds 45.8% share and is now pushing up-market into enterprises with AI-powered talent analytics funded by its USD 96 million November 2025 raise. Expanded social-insurance coverage for part-time staff effective October 2024 has already triggered fresh configurations across payroll engines. South Korea, Australia, Singapore, and the emerging group of Indonesia, Malaysia, and Thailand represent the next wave of high-growth jurisdictions as each introduces gig-worker protections, right-to-disconnect rules, and progressive wage frameworks that alter payroll logic.

Competitive Landscape

The market shows moderate concentration, with Workday, SAP, Oracle, ADP, and UKG forming the global top tier, while Darwinbox, SmartHR, Beisen, Ramco, and Zoho anchor the regional tier. Workday’s four new Asia-Pacific cloud regions and embedded Skills Cloud amplify its value proposition of secure residency plus AI-driven talent insights. Oracle is bundling hire-to-retire workflows inside its ME Cloud to cross-sell into its large financials install base, and the 25A release adds generative agents for onboarding and performance.

Regional specialists differentiate by rapid localization and mid-market pricing. SmartHR automates Japan’s complex social-insurance enrollment and has begun building enterprise-grade analytics with its November 2025 funding. Darwinbox, buoyed by USD 140 million from Partners Group and KKR, is rolling out pre-configured payroll packs across Southeast Asia, winning accounts that global suites previously ignored. Beisen’s profitability milestone in 2026 demonstrates that scale and localization can coexist, enabling sustained R&D on AI modules.

Disruptors such as HiBob, Rippling, and Gusto are entering via Singapore and Australia with cloud-native architectures that promise implementation in days, not months. ISG’s 2025 HRMS guide ranks these challengers high on user experience innovation, though they lack deep statutory packs outside English-speaking markets. Mergers and acquisitions are expected as private equity seeks roll-ups to build pan-regional scale, targeting firms that combine 40%+ growth with double-digit operating margins.

Asia-Pacific Human Capital Management Software Industry Leaders

Workday Inc.

SAP SE

Oracle Corporation

Automatic Data Processing, Inc. (ADP)

UKG Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Oracle released Cloud HCM 25A, adding AI agents for hiring, onboarding, and performance and deepening integration with Fusion Cloud ERP.

- November 2025: SmartHR raised USD 96 million from General Atlantic to expand enterprise sales and AI product development in Japan

- November 2025: Ramco Systems won 2 Gold, 1 Silver, and 1 Bronze at HR Vendors of the Year Awards 2025 in Malaysia and Singapore for its Payce payroll platform.

- March 2025: Darwinbox secured USD 140 million led by Partners Group and KKR to fund Southeast Asia and Middle East expansion.

Asia-Pacific Human Capital Management Software Market Report Scope

Human capital management (HCM) software, an enterprise application solution, has been needed across all enterprises as it automates the cumbersome clerical tasks related to employee data, payroll, and benefits administration. The APAC human capital management (HCM) market is defined based on the revenues generated through the sale of licensing and subscription of human capital management software offered by various market players to various end-user industries in the APAC region. Market analysis for Enterprise Governance, Risk, and Compliance (eGRC) solutions is included in the scope of the study as an individual segment. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting the growth of the market in terms of drivers and restraints.

The Asia-Pacific Human Capital Management Software Market Report is Segmented by Deployment (Cloud-Based, On-Premise), Application (Core HR, Payroll Management, Compensation Management, Workforce Management, Performance and Talent Management, E-Learning and E-Recruiting, Enterprise GRC), Organization Size (Small and Medium-Sized Enterprises, Large Enterprises), Offering (Software, Services), End-User Industry (BFSI, IT and Telecom, Retail and E-Commerce, Manufacturing, Healthcare and Life-Sciences, Government and Public Sector, Other End-User Industries), and Geography (China, Japan, India, South Korea, Australia, Singapore, Indonesia, Malaysia, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

By Deployment

| Cloud-Based |

| On-Premise |

By Application

| Core HR |

| Payroll Management |

| Compensation Management |

| Workforce Management |

| Performance and Talent Management |

| E-Learning and E-Recruiting |

| Enterprise GRC (eGRC) |

By Organization Size

| Small and Medium-Sized Enterprises (SMEs) |

| Large Enterprises |

By Offering

| Software | Core Platforms |

| Point Solutions and Add-Ons | |

| Services | Implementation and Integration |

| Support and Maintenance |

By End-User Industry

| Banking, Financial Services, and Insurance (BFSI) |

| IT and Telecom |

| Retail and E-Commerce |

| Manufacturing |

| Healthcare and Life-Sciences |

| Government and Public Sector |

| Other End-User Industries |

By Geography

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Singapore |

| Indonesia |

| Malaysia |

| Rest of Asia-Pacific |

| By Deployment | Cloud-Based | |

| On-Premise | ||

| By Application | Core HR | |

| Payroll Management | ||

| Compensation Management | ||

| Workforce Management | ||

| Performance and Talent Management | ||

| E-Learning and E-Recruiting | ||

| Enterprise GRC (eGRC) | ||

| By Organization Size | Small and Medium-Sized Enterprises (SMEs) | |

| Large Enterprises | ||

| By Offering | Software | Core Platforms |

| Point Solutions and Add-Ons | ||

| Services | Implementation and Integration | |

| Support and Maintenance | ||

| By End-User Industry | Banking, Financial Services, and Insurance (BFSI) | |

| IT and Telecom | ||

| Retail and E-Commerce | ||

| Manufacturing | ||

| Healthcare and Life-Sciences | ||

| Government and Public Sector | ||

| Other End-User Industries | ||

| By Geography | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Indonesia | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large will the Asia-Pacific human capital management software market be by 2031?

The market is forecast to reach USD 13.92 billion by 2031, expanding at 7.47% CAGR from 2026-2031.

Which deployment model is gaining the most traction in Asia-Pacific?

Cloud-based platforms held 78.03% share in 2025 and continue to outpace on-premise options thanks to lower upfront cost and regulatory-compliant data centers.

What is the fastest-growing application area for HCM suites?

Performance and talent management is advancing at 7.84% CAGR as firms pivot to skills-based workforce strategies.

Why are small and medium-sized enterprises adopting HCM software more quickly now?

Subscription pricing, localized statutory packs, and pre-configured workflows remove the need for in-house HRIT expertise, supporting a 7.91% CAGR through 2031.

Which country offers the highest growth outlook?

India is projected to lead regional growth at 8.12% CAGR due to digital-payroll mandates and strong mid-market demand.

How are vendors addressing privacy regulations across Asia-Pacific?

Leading platforms now operate multiple in-region data centers, embed encryption and role-based access controls, and provide geo-fencing features to meet data-localization laws.

Page last updated on: