Enterprise WLAN Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 27.98 Billion |

| Market Size (2031) | USD 50.53 Billion |

| Growth Rate (2026 - 2031) | 12.55% CAGR |

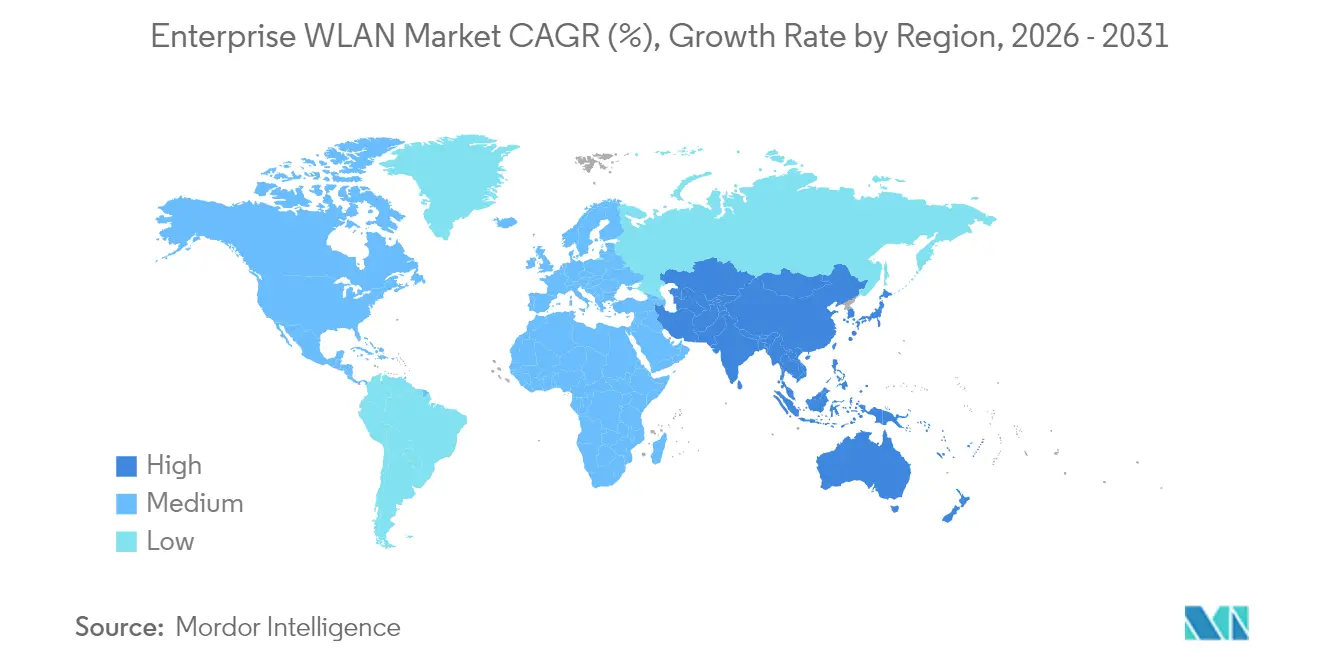

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise WLAN Market Analysis by Mordor Intelligence

The Enterprise WLAN Market size was valued at USD 24.86 billion in 2025 and estimated to grow from USD 27.98 billion in 2026 to reach USD 50.53 billion by 2031, at a CAGR of 12.55% during the forecast period (2026-2031).

Earlier supply constraints have largely receded, and procurement budgets are shifting toward next-generation wireless infrastructure that supports hybrid work, high-density IoT, and latency-sensitive video workloads. The rapid move to Wi-Fi 6E—and the first wave of Wi-Fi 7 trials—expands usable spectrum into the 6 GHz band, enabling multigigabit throughput and deterministic latency that legacy Wi-Fi 5 networks cannot match.[1]Pierre de Vries, “Drivers and Barriers to Wi-Fi 7 Deployment,” Electronics Weekly, electronicsweekly.comNorth America captured 38.9% of 2024 revenue on the strength of deep IT investments and favorable spectrum policy, while Asia Pacific is the fastest-growing region as digital-first agendas gain momentum. Hardware remains the largest spending category, yet AI-driven management and security software is climbing faster as enterprises prioritize automation, observability, and zero-trust controls. Market consolidation—illustrated by HPE’s USD 14 billion bid for Juniper Networks—aims to assemble full-stack portfolios capable of challenging Cisco’s roughly 40% share, according to NetworkWorld, but antitrust scrutiny may reshape timelines.

Key Report Takeaways

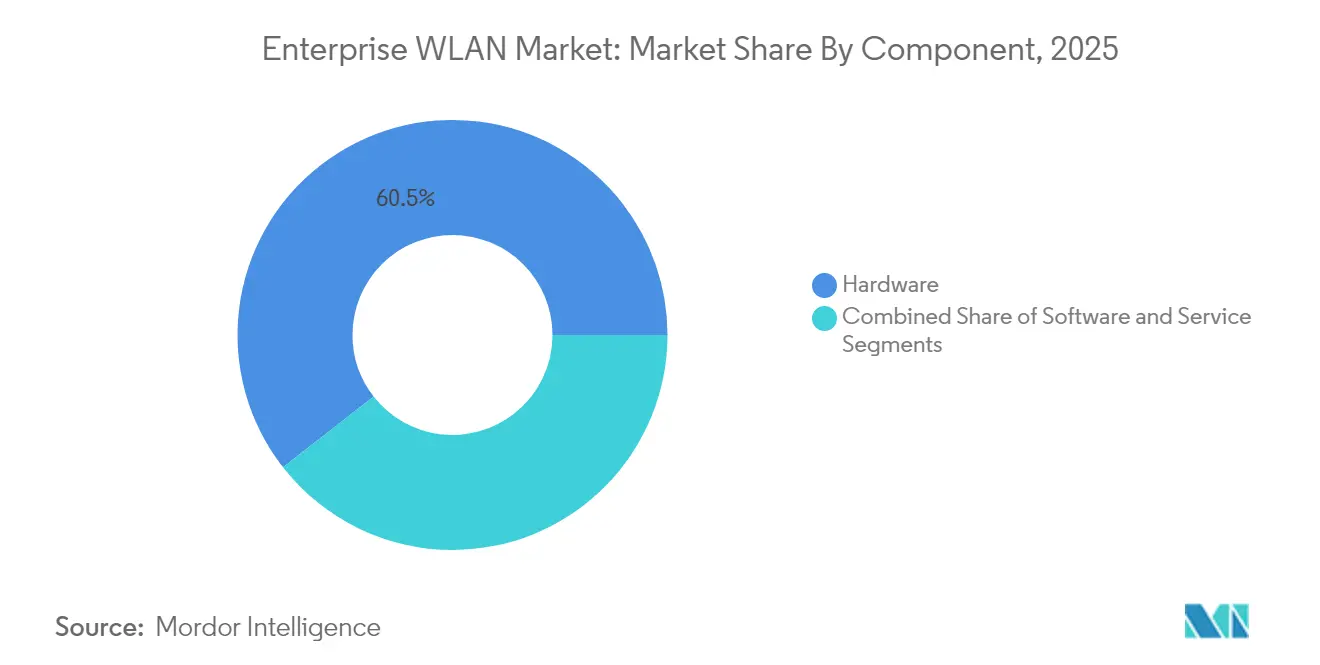

- By component, hardware led with 60.55% revenue share in 2025; software is expanding at a 13.75% CAGR through 2031.

- By organization size, large enterprises held 57.35% of the enterprise WLAN market share in 2025, while SMEs recorded the highest projected CAGR at 12.95% to 2031.

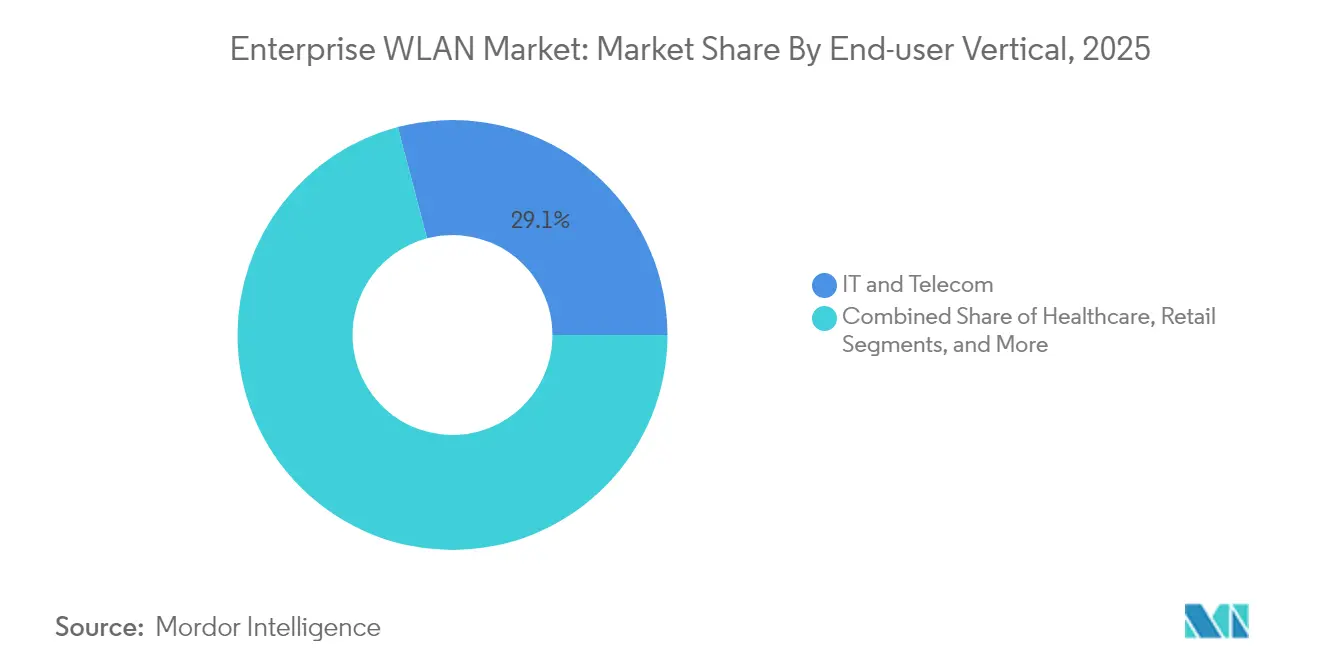

- By end-user vertical, IT and Telecommunications accounted for 29.10% of the enterprise WLAN market size in 2025; healthcare is set to advance at a 13.15% CAGR through 2031.

- By deployment mode, on-premises solutions retained a 65.50% share in 2025, yet cloud-managed WLAN is climbing at a 13.95% CAGR to 2031.

- By geography, North America led with 38.40% revenue share in 2025; Asia Pacific is forecast to grow at a 13.05% CAGR over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enterprise WLAN Market Trends and Insights

Drivers Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Wi-Fi 6/6E upgrade cycles | +3.2% | Global, earliest in North America & Western Europe | Medium term (2-4 years) |

| Rapid adoption of BYOD & hybrid work | +2.8% | Global, stronger in developed markets | Short term (≤2 years) |

| Exploding enterprise IoT node density | +2.5% | Global, heavy in manufacturing, healthcare, retail | Medium term (2-4 years) |

| Cloud-managed WLAN lowers TCO | +2.1% | Global, fastest in North America and Europe | Short term (≤2 years) |

| 6 GHz spectrum allocations | +1.4% | Regional, subject to regulator approval | Medium term (2-4 years) |

| Smart-building stimulus funds | +0.6% | Regional, visible in North America, Europe, developed APAC | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surge in Wi-Fi 6/6E Upgrade Cycles Drives Performance Leap

- Opening 1,200 MHz of 6 GHz spectrum gives enterprises the first contiguous stretch of ultra-wide channels for multigigabit WLAN, and multi-link operation in Wi-Fi 7 boosts throughput while trimming latency. Video collaboration, immersive training, and AR-assisted maintenance demand such deterministic performance, prompting 40% of large organizations to bring forward refresh schedules. Indian regulators value the 6 GHz allocation at USD 4,030 billion in cumulative economic activity for 2024-2034, underscoring its macro impact.[2]Kevin Robinson, “Economic Value of the 6 GHz Band for Unlicensed Use in India,” Dynamic Spectrum Alliance, dynamicspectrumalliance.orgYet higher power budgets and POE++ switches are prerequisites, nudging buyers to coordinate access-layer and switching upgrades in tandem.

Hybrid Work Models Demand Network Transformation

Hybrid work is now standard practice, requiring seamless roaming, granular access control, and application-level QoS across offices and homes. Enterprises allocate an average of USD 115.7 million over three years for advanced wireless projects to enable unified user experiences, VPN-grade security, and analytics-driven capacity planning. Passpoint (IEEE 802.11u) simplifies secure onboarding for employees and guests, lowering help-desk tickets while tightening identity assurance. The enterprise WLAN market benefits as CIOs align network modernization with workplace flexibility mandates

IoT Density Drives Network Architecture Evolution

By 2030, commercial smart buildings alone will host a significant number of IoT devices, pushing WLAN designs toward tri-radio APs and dynamic segmentation that isolates critical systems. Zero-trust architectures verify every device and flow, and blockchain-based identity schemes add tamper-resistant logs for compliance-sensitive environments. Complementary use of private 5G for latency-critical AGVs and Wi-Fi 6 for indoor sensors creates hybrid fabrics, broadening the enterprise WLAN market addressable scope.

Cloud Management Transforms Operational Economics

Cloud-hosted WLAN controllers eliminate onsite hardware, unify multisite operations, and embed AI for anomaly detection. Mist AI from Juniper flags root-cause issues before users notice, shrinking mean-time-to-repair and cutting truck rolls, which resonates with lean IT teams. Forty-two percent of professionals admit they devote excessive hours to manual troubleshooting tasks, according to NetworkComputing. Shifting CAPEX to OPEX, plus continuous feature updates, sustains a double-digit growth clip for cloud-managed platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chip-set supply-chain volatility | –1.8% | Global, sharper in emerging markets | Short term (≤2 years) |

| Skills gap in Wi-Fi design and security | –1.2% | Global, more pronounced in fast-growing economies | Medium term (2-4 years) |

| Enterprise private-5G substitution risk | –0.8% | Regional, intense in manufacturing, logistics, healthcare | Long term (≥4 years) |

| Rising cybersecurity insurance premiums | –0.5% | Global, larger burden in regulated industries | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Supply-Chain Disruptions Constrain Growth

Lead times for network ASICs stretch up to 52 weeks in some data-center SKUs, prompting buyers to postpone rollouts or adopt cloud alternatives that lessen hardware dependence. Vendors with diversified suppliers weather shortages better and capture displaced demand. Extreme Networks cites pandemic-era resilience that unlocked new sales in healthcare refits.

Cybersecurity Skills Gap Threatens Network Security

Ninety percent of breaches are tied partly to talent shortfalls, and wireless security expertise is especially scarce, according to Fortinet. Although Fortinet pledges to train one million specialists by 2026, 19% of enterprises already report a high risk of missing objectives due to a lack of skilled staff. AI-assisted policy engines help close gaps, but hiring lags remain a drag on enterprise WLAN market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominates, Software Accelerates

Hardware contributed 60.55% of 2025 revenue, powered by demand for high-density Wi-Fi 6E access points that safeguard application performance in auditoriums, factories, and hospitals. Vendors bundle tri-radio designs, integrated IoT radios, and advanced RF analytics that justify premium price points. The enterprise WLAN market is now cycling through switch upgrades that supply 2.5 Gbps or 5 Gbps multigig Ethernet plus 90 W POE to drive next-generation APs. The software category, though smaller, is climbing at a 13.75% CAGR as AI-native cloud control, assurance analytics, and threat-centric micro-segmentation become indispensable. Mist AI and Cisco DNA Center illustrate how controller logic, network data lakes, and machine learning converge into single-pane experiences.

Access point firmware and license subscriptions convert once-periodic capital spending into recurring revenue, enticing investors and compressing refresh intervals. Meanwhile, professional and managed services flourish because organizations lack in-house RF planning and zero-trust design skills. Consultants orchestrate site surveys, spectrum audits, and compliance validation, adding stickiness to vendor ecosystems

By Organization Size: Large Enterprises Lead, SMEs Accelerate

Large enterprises held 57.35% of the enterprise WLAN market share in 2025, reflecting multi-campus estates that demand scaled authentication, policy engines, and resiliency. SD-branch architectures feeding into SASE frameworks align well with Fortune 1000 security mandates. Yet SMEs post the strongest 12.95% CAGR, encouraged by subscription-based WLAN as a service that removes controller hardware and heavy upfront cost. Cloud onboarding and automated RF optimization free smaller IT teams from arcane CLI workflows, making enterprise-grade features accessible without hiring certified wireless engineers.

Vendors repackage enterprise functionality into tiered offerings that emphasize quick deployment, pay-as-you-grow licensing, and mobile-first dashboards. MSP channels bundle WLAN with broadband and VoIP, deepening penetration among retail, hospitality, and professional services. As talent shortages persist, SMEs turn to outsourced monitoring, driving a services layer that grows in lockstep with cloud-managed adoption.

By End-user Vertical: IT and Telecom Dominates, Healthcare Surges

The IT and Telecom sector accounts for 29.10% of the enterprise WLAN market size, acting as both a technology innovator and a showcase customer. Hyperscalers, colocation providers, and network operators rely on multitenant WLAN for visitor access, staging labs, and smart warehouse automation. Healthcare delivers the fastest 13.15% CAGR as hospitals digitize patient records, embrace telehealth, and deploy connected medical devices that require deterministic latency and strong isolation. Proposed HIPAA Security Rule updates place greater emphasis on encryption, access control, and continuous monitoring, triggering budget reallocations to WLAN refresh.

Retailers incorporate Wi-Fi analytics to map shopper paths and enable cashier-less checkout, while universities standardize next-gen Wi-Fi across dorms and classrooms to support e-learning platforms. Manufacturers invest in redundant WLAN meshes for AGVs and wireless programmable logic controllers, concluding that cabling impedes flexible retooling. Financial institutions seek branch transformation, deploying secure Wi-Fi for staff mobility and customer engagement while meeting stringent compliance.

By Deployment Mode: On-premises Persists, Cloud Accelerates

On-premises models still account for 65.50% of deployments, favored by government, finance, and healthcare entities that keep data planes local for compliance. Locally hosted controllers provide deterministic control paths and facilitate custom RF tuning. Nonetheless, cloud-managed solutions are expanding at a 13.95% CAGR owing to elastic scale and rapid feature rollouts. The enterprise WLAN market increasingly adopts hybrid control, where critical campuses remain on-premises and distributed sites move to SaaS dashboards.

AI-supported assurance modules in the cloud aggregate telemetry across thousands of APs, producing baseline performance fingerprints and auto-generating remediation scripts. This autonomy shortens problem resolution cycles and frees engineers for strategic tasks. Support for API-first operations allows DevNet teams to integrate WLAN events into IT service management suites, aligning networking with broader DevOps pipelines.

Geography Analysis

North America generated the highest revenue with a 38.40% share in 2025, buoyed by FCC-backed 6 GHz allocations that created an estimated USD 870 billion in economic value during 2023-2024. United States shipments swung sharply, down 30.6% year over year in Q2 2024, then rebounded 15.3% sequentially as backlogs cleared, according to InfotechLead. Federal broadband funding, smart-building incentives, and a vibrant managed services channel sustain spending across healthcare, education, and financial services.

Asia Pacific posts the fastest 13.05% CAGR between 2026 and 2031. China remains the biggest market, steered by industrial policies that favor digital factories and campus rollouts. India’s policy think tank values unlicensed 6 GHz at USD 4,030 billion in cumulative impact through 2034, further catalyzing enterprise WLAN market demand. ASEAN members expand manufacturing footprints and modernize airports, both requiring high-density Wi-Fi and zero-trust segmentation.

Europe shows mixed momentum. Shipments sank 22.3% year over year in Q2 2024 amid macro headwinds, then ticked up modestly in Q3 as inventory normalization progressed, according to InfotechLead. The European Vision for 6G Network Ecosystems prioritizes AI-native and integrated sensing features, and spectrum regulators push common frameworks to accelerate vendor innovation.These initiatives will shape enterprise WLAN upgrades because interoperability between 5G-Advanced and Wi-Fi 7 is a design goal for campus environments.

The Middle East and Africa remain smaller but record double-digit growth as governments invest in smart cities. United Arab Emirates ministries deploy converged Wi-Fi/IoT networks in federal buildings, while South African retailers adopt cloud-managed WLAN to support omnichannel commerce. Latin America, starting from a low base, registered 235% year-over-year growth in Q3 2023 after supply bottlenecks eased and currency stability improved. The region’s hospitality and mining sectors show particular interest in AI-assisted WLAN for guest services and remote site connectivity.

Regulatory Landscape

Enterprise WLAN deployments are shaped by spectrum policy and equipment conformity regimes that affect 6 GHz Wi-Fi 6E and Wi-Fi 7 configuration choices. In the United States, the Federal Communications Commission (FCC) expanded the 6 GHz unlicensed framework by authorizing geofenced variable power (GVP) devices in January 2026 (FCC-26-1), with final rules published in the Federal Register in February 2026 and an effective date of April 27, 2026. This adds a compliance path beyond Standard Power and Low Power Indoor (LPI) operation for U-NII-5 and U-NII-7.

In Europe, the regulatory posture for 6 GHz remains more restrictive, generally limiting operation to LPI and Very Low Power (VLP) modes. That constraint influences enterprise AP power profiles and outdoor or campus edge designs. On the conformity side, the European Commission continues to anchor Radio Equipment Directive (RED) compliance through harmonized standards, including Commission Implementing Decision (EU) 2025/893 referencing EN 303 687 V1.1.1, which manufacturers must account for while ETSI revisions progress. At the global standardization layer, IEEE 802.11be (Wi-Fi 7) publication (July 22, 2025) provides the technical baseline for multi-link operation and 320 MHz channel capability that vendors incorporate into certified enterprise WLAN product lines.

Value Chain Analysis

The enterprise WLAN value chain begins with RF and networking silicon, including Wi-Fi chipsets, switching ASICs, and memory, and extends through module makers and OEM/ODM manufacturers building access points, gateways, and controller hardware. Branded infrastructure vendors then add firmware, security features, and management planes before the products move to enterprises via distributors, value-added resellers, MSPs, and systems integrators. These channel partners handle site surveys, RF planning, installation, and ongoing operations for multi-site estates.

Software and services have gained share as cloud-managed WLAN and AIOps expand, pulling recurring licensing, analytics, and security subscriptions into the chain alongside hardware refreshes such as multi-gig switching and higher PoE budgets. Supply-side developments in 2026 point to two delivery patterns: open, interoperable stacks for service-provider-led rollouts (Edgecore Networks and Indio Networks completing production-ready OpenWiFi integration in January 2026), and converged wired-wireless offerings that reduce friction for enterprise access-layer modernization (RUCKUS Networks and Nokia announcing early access to an integrated Wi-Fi 7 plus fiber optical LAN solution managed via RUCKUS One in April 2026).

Competitive Landscape

Cisco maintains leadership with around 40% revenue share, yet revenue slipped 29.7% in Q2 2024 as backlog burn-down overshadowed new orders. HPE’s proposed USD 14 billion acquisition of Juniper Networks aims to fuse Aruba’s campus WLAN strength with Mist AI’s cloud automation. Regulators fear post-merger concentration could exceed 70% in the United States, and litigation threatens to delay integration. During the uncertainty, Extreme Networks positioned itself as a stable alternative, winning 164 deals above USD 1 million in FY 2024.

Product differentiation centers on AI-driven operations. Juniper’s Marvis virtual assistant processes telemetry to offer actionable insights, while Cisco embeds AI analytics inside the Catalyst Center. Fortinet unifies next-generation firewalls and Wi-Fi, creating a single security fabric that compares favorably in cyber insurance audits. HPE-Aruba leads in unified wired-wireless policy via ClearPass and EdgeConnect SD-WAN synergy.

White-space opportunities emerge in industry-specific packages: healthcare bundles that combine RTLS for medical assets, manufacturing kits tuned for Wi-Fi-based AGV handoffs, and education editions with cloud-native identity. Vendors also explore subscription tiers that add CBRS or private-5G radio modules, allowing campus operators to deploy converged networks under one license plan.

Early Wi-Fi 7 road-map visibility influences RFPs. Extreme has introduced AP4000 series units that handle 320 MHz channels with flexible power profiles, while Cisco’s Catalyst 9800E controller firmware already supports multi-link operation for select beta customers. Partners such as WWT compare vendor power budgets and heat dissipation to guide facilities teams on switch and cooling upgrades. Timely Wi-Fi 7 certification will become a land-grab moment for share shifts.

Enterprise WLAN Industry Leaders

Cisco Systems Inc.

Huawei Technologies Co. Ltd.

Alcatel Lucent Enterprises

Dell Inc.

Fortinet

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The 6 GHz transition continues to create actionable whitespace in global enterprise estates where spectrum policy and standards maturity support higher-performance WLAN designs. However, operational complexity and compliance constraints still limit full utilization. In the United States, the FCCs introduction of geofenced variable power (GVP) devices for 6 GHz, with rules effective April 27, 2026, creates an additional operating mode that can improve coverage and performance across more demanding enterprise layouts. This supports demand for access points with geofencing, location capabilities, and policy controls aligned to the new class.

A second opportunity set is packaging and platform integration that reduces total cost and deployment friction for distributed campuses and multi-building upgrades, particularly when enterprises coordinate Wi-Fi 7 access points with switching, power, and wired backbones. Vendor activity supports this direction: RUCKUS Networks and Nokia moved to early access availability for an integrated Wi-Fi 7 and fiber optical LAN solution (April 2026), positioning unified management to streamline refresh projects. OpenWiFi-oriented production integrations (Edgecore Networks and Indio Networks, January 2026) also expand options for MSP and telco-led enterprise deployments that want more flexibility across hardware and software choices. Across regions, the divergence between US 6 GHz modes (Standard Power, LPI, and GVP) and EU constraints (LPI/VLP) creates a design and services market for global enterprises that need region-specific SKUs, firmware governance, and standardized security posture under different radio rules.

Recent Industry Developments

- April 2026: RUCKUS Networks and Nokia announced early access availability for an integrated Wi-Fi 7 and fiber optical LAN solution managed through the RUCKUS One platform. The combined offer targets enterprises standardizing the access layer, pairing next-generation WLAN with fiber-based LAN to simplify operations and site upgrades.

- May 2025: Extreme Networks launched ExtremeCloud Universal Zero Trust Network Access and Extreme Platform ONE, consolidating networking and security workflows into an AI-powered control plane. The release supports enterprise moves toward unified policy, identity-aware access, and simplified operations across distributed environments.

- March 2024: Cisco introduced its Wi-Fi 7 portfolio with a focus on intelligent, secure, and assured connectivity for enterprise environments. The announcement advanced competitive positioning around higher-capacity access points and management capabilities aligned to new Wi-Fi 7 features.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the enterprise WLAN market covers spending by organizations on Wi-Fi networks used inside offices, campuses, and similar sites, including related hardware, software, and services that enable enterprise-grade connectivity.

Scope exclusions: We exclude consumer home Wi-Fi devices, public hot-spot networks, and private cellular systems (such as CBRS or private 5G) that are not delivered as enterprise Wi-Fi LAN.

Segmentation Overview

- By Component

- Hardware

- Access Points

- WLAN Controllers

- Wireless Hotspot Gateways

- Software

- WLAN Security

- WLAN Management

- WLAN Analytics

- Other Software

- Services

- Professional Services

- Managed Services

- Hardware

- By Organization Size

- Large Enterprises

- Small and Medium-sized Enterprises (SME)

- By End-user Vertical

- Banking, Financial Services and Insurance

- Healthcare

- Retail

- IT and Telecommunications

- Manufacturing

- Education

- Hospitality

- Other Verticals

- By Deployment Mode

- On-premises

- Cloud-managed

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Argentina

- Brazil

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with setting a clear boundary for what gets counted as enterprise WLAN revenue, and then collecting public signals that explain demand and refresh cycles. We referenced sources such as FCC spectrum and Wi-Fi rule updates, NIST cybersecurity publications, the IEEE 802.11 standards body documentation, and Wi-Fi Alliance public material on Wi-Fi 6E and Wi-Fi 7 adoption.

To make the model practical, we also reviewed company filings, investor decks, and earnings transcripts to understand shipment trends, pricing commentary, and subscription attach for enterprise networking offers. Supporting checks were taken from credible press, association websites, and patent databases to see whether feature releases and product cycles match the timing assumed in the forecast. For financial normalization and cross-checking, we used paid subscriptions focused on company financials and intelligence, news and financials, and patent coverage. The desk research sources listed above are illustrative, and many other public documents were used for data collection, clarification, and validation.

Primary Interviews and Surveys

Primary work was used to test what we saw in public data, especially around replacement cycles, cloud-managed adoption, and price movement across access points, controllers, and services. We spoke with manufacturers, channel partners, integrators, and enterprise buyers across major regions, so assumptions on volumes, typical deal structures, and support service intensity could be confirmed before final sizing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 15% | APAC: 39% |

| Mid tier: 49% | Functional/Unit leaders: 36% | EMEA: 34% |

| Smaller Players: 15% | Managers: 49% | Americas: 27% |

Market-Sizing & Forecasting

The core model uses a top-down approach where enterprise IT and networking spend is narrowed step by step into WLAN, and then split using adoption and refresh indicators by region. To keep the result grounded, we then corroborated it with selective bottom-up approximations, such as sampled access point shipments times typical selling prices, and channel feedback on services and subscription attach, and gaps were adjusted when the two views drifted.

Key inputs used in the model include installed base refresh timing tied to Wi-Fi 6E and Wi-Fi 7 migration, average access points per site by common enterprise environments, cloud-managed share progression, services intensity for design and ongoing support, and regional enterprise expansion signals that affect net new deployments. For forecasting, scenario analysis was applied, where driver paths were set using expert consensus and then tested for sensitivity, so the final curve did not rely on one aggressive adoption assumption. Where bottom-up checks were incomplete, the missing piece was bridged using conservative ranges from interviews and cross-checked against public product cycle milestones.

Data Validation & Update Cycle

Outputs are checked against independent market signals and simple sanity tests before sign-off, including year over year movement, implied unit volumes, and realistic pricing progression. When a line item looks off, we review the driver that caused it, re-check the source, and then re-contact relevant respondents if the variance remains large.

The report is refreshed annually, and interim updates are made when material events occur, such as sharp demand swings, major standard transitions, or notable supply changes. Before delivery, an analyst performs a final pass to confirm assumptions are still current and that the latest public information has been reflected in the numbers.

Mordor Intelligence's Enterprise Wlan Market Size Measured Against Other Published Estimates

Published enterprise WLAN numbers often differ because the market boundary is not set the same way, and the timing of the base year can also shift the result. Differences also come from whether services and software are included, and whether estimates are built from enterprise demand signals or mainly from reported equipment revenue.

Quarterly and full-year enterprise WLAN revenue trackers are used as an external reasonableness check, and those observed swings help keep Mordor Intelligence's estimate anchored to the combined hardware plus software plus services spending that enterprises actually budget for in Wi-Fi refresh cycles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 24.86 B (2025) | |

| Trade Journal A | USD 9.40 B (2024) | Tracks a narrower equipment revenue pool that is closer to access point and controller sales, so recurring software subscriptions and many professional or managed services are not fully counted in the total. |

| Industry Database B | USD 32.77 B (2025) | Applies a wider definition that can pull in adjacent enterprise networking items or broader WLAN software layers, and it can also assume faster ASP expansion across the cycle. |

The spread is largely explained by what sits inside the counted market scope, followed by differences in year timing and how pricing progression is applied. By keeping inclusions explicit and then validating totals through repeatable demand indicators and targeted bottom-up checks, we arrive at a number that is easier to trace and update over time.

Key Questions Answered in the Report

What is the current size of the enterprise WLAN market?

The enterprise WLAN market size is USD 27.98 billion in 2026.

How fast is the enterprise WLAN market expected to grow?

It is forecast to expand at a 12.55% CAGR, reaching USD 50.53 billion by 2031.

Which region is growing the fastest for enterprise WLAN deployments?

Asia Pacific is projected to post a 13.05% CAGR between 2026 and 2031.

Why are cloud-managed WLAN platforms gaining popularity?

They eliminate onsite controllers, reduce total cost of ownership, and embed AI for automated troubleshooting, appealing to organizations with lean IT teams.

How does Wi-Fi 6E improve enterprise network performance?

It adds 1,200 MHz of 6 GHz spectrum, enabling wider channels, higher throughput, and lower latency, which are essential for video collaboration, IoT, and AR/VR applications.

What impact will HPE’s proposed acquisition of Juniper Networks have?

If approved, the combined entity could control over 70% of the United States enterprise-grade WLAN market, potentially changing competitive dynamics and accelerating AI-driven innovation.

Page last updated on: