Very Small Aperture Terminal (VSAT) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

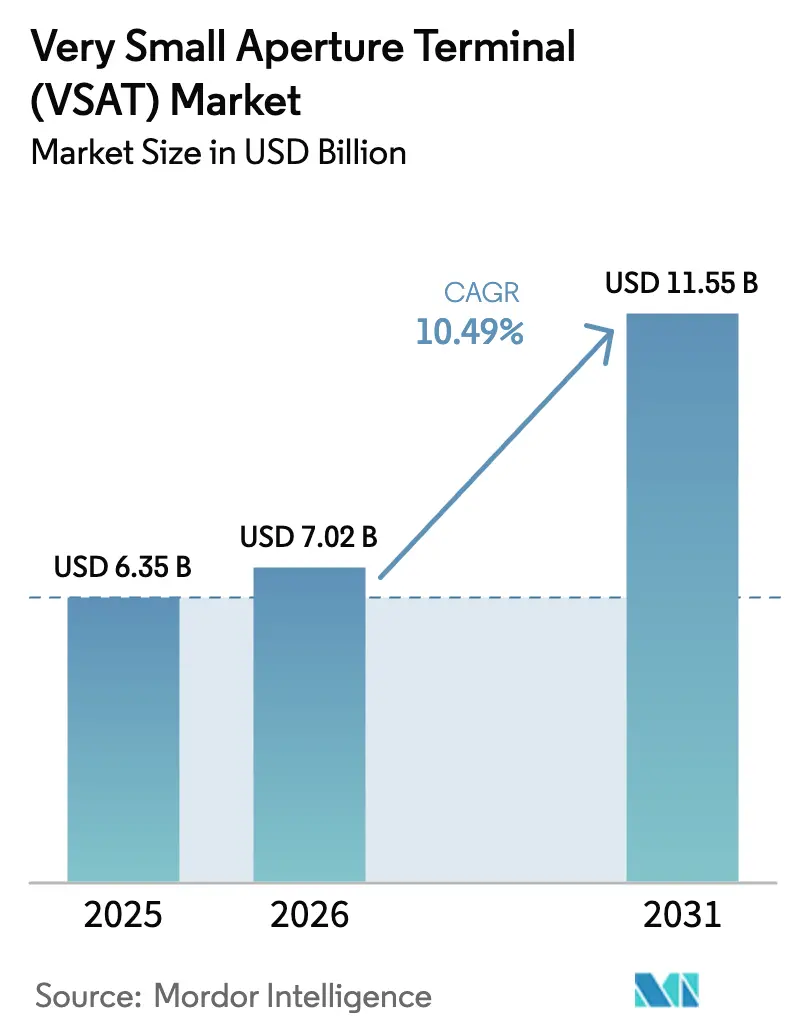

| Market Size (2026) | USD 7.02 Billion |

| Market Size (2031) | USD 11.55 Billion |

| Growth Rate (2026 - 2031) | 10.49% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Very Small Aperture Terminal (VSAT) Market Analysis by Mordor Intelligence

The VSAT market size was valued at USD 6.35 billion in 2025 and estimated to grow from USD 7.02 billion in 2026 to reach USD 11.55 billion by 2031, at a CAGR of 10.49% during the forecast period (2026-2031). Momentum comes from high-throughput satellite launches, growing maritime digitalization mandates, energy-sector automation, and large-scale rural-broadband programs in Asia. Competitive intensity is rising as vertically integrated LEO providers disrupt traditional GEO economics, forcing incumbents to accelerate hybrid-orbit strategies. Capacity upgrades at Ku- and Ka-band, coupled with advances in flat-panel antennas, are widening addressable use cases while helping operators counter supply-chain shocks related to gallium-based amplifiers. Although regulatory delays and price compression weigh on margins, sustained multi-orbit innovation and public-sector funding continue to underpin expansion across the VSAT market.

Key Report Takeaways

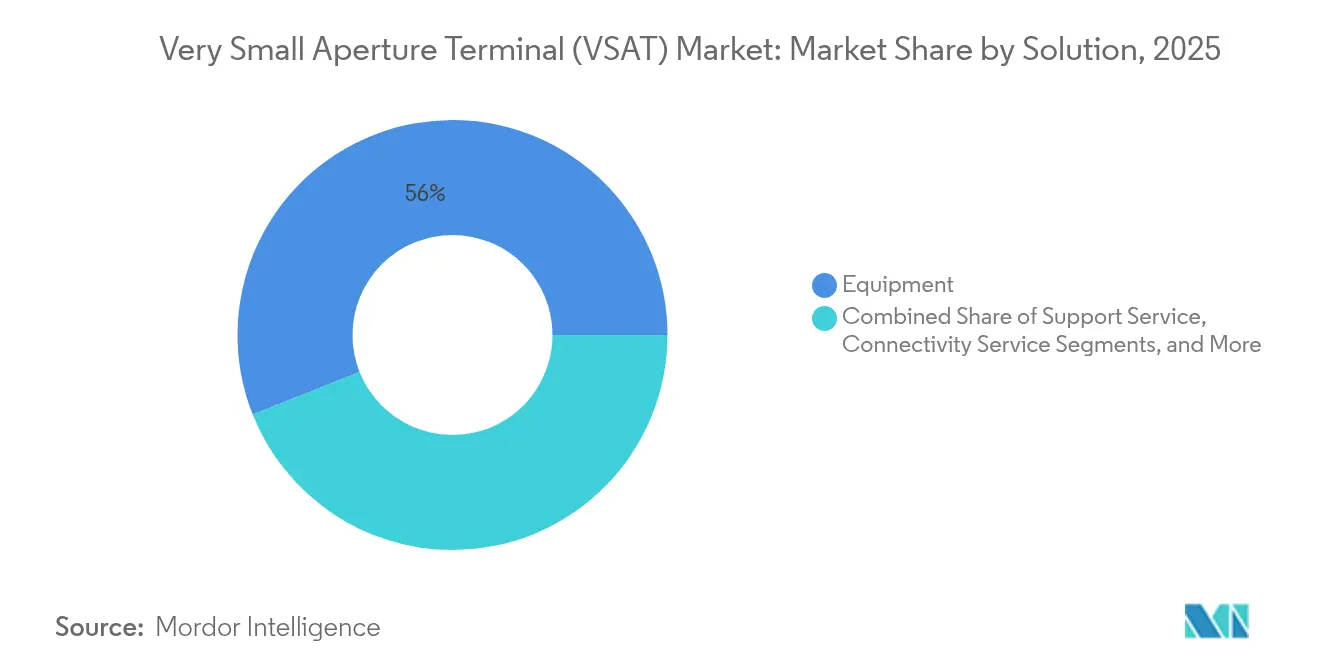

- By solution, equipment captured 56.02% VSAT market share in 2025, while connectivity services are projected to expand at an 11.6% CAGR through 2031.

- By platform, land systems held 47.35% of the VSAT market size in 2025; maritime platforms are advancing at the fastest 11.6% CAGR through 2031, propelled by IMO e-Navigation compliance.

- By frequency, Ku-band led with 41.22% revenue share in 2025; Ka-band is set to grow at 14.02% CAGR on the back of spot-beam deployments.

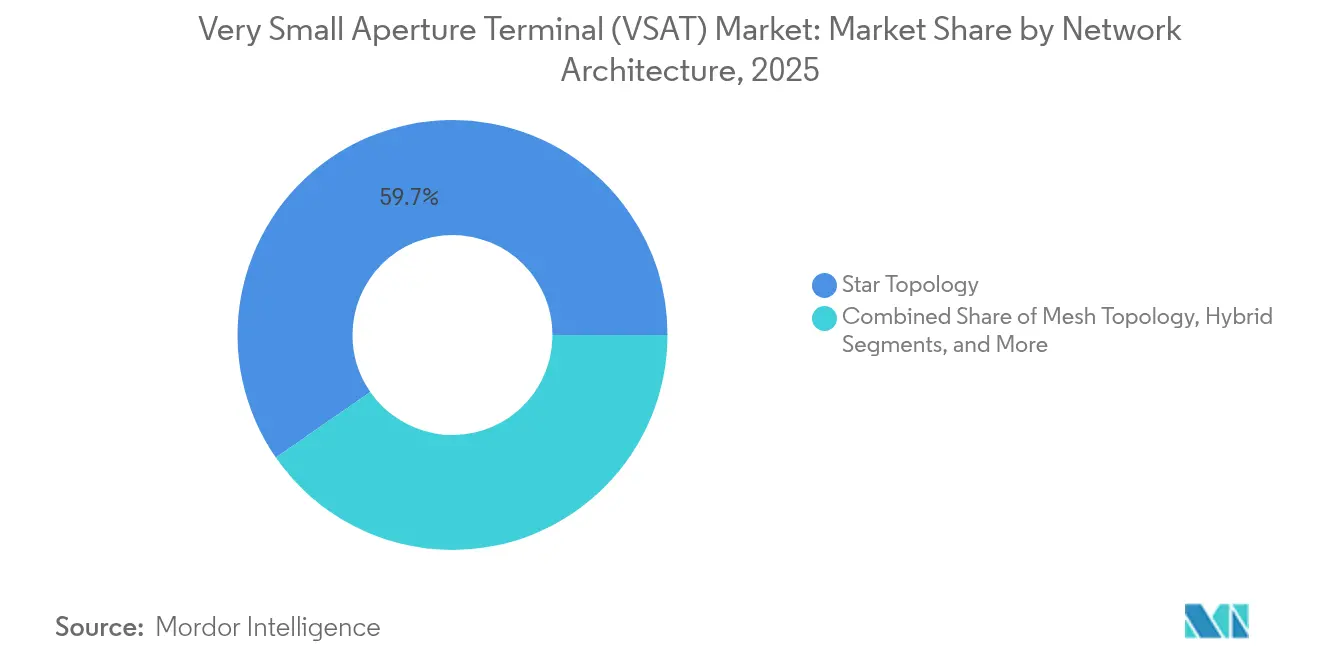

- By network architecture, star topology accounted for 59.65% VSAT market share in 2025, while mesh networks are projected to rise at 10.78% CAGR.

- By type, standard VSAT commanded 72.34% of the AT market size in 2025; micro VSAT is growing fastest at 11.95% CAGR.

- By design, commercial-grade terminals generated 35.16% revenue in 2025, whereas ruggedized units are set to climb at 10.66% CAGR.

- By antenna, parabolic dishes delivered 62.05% revenue share in 2025; flat-panel electronically steered units are forecast to expand at 13.01% CAGR.

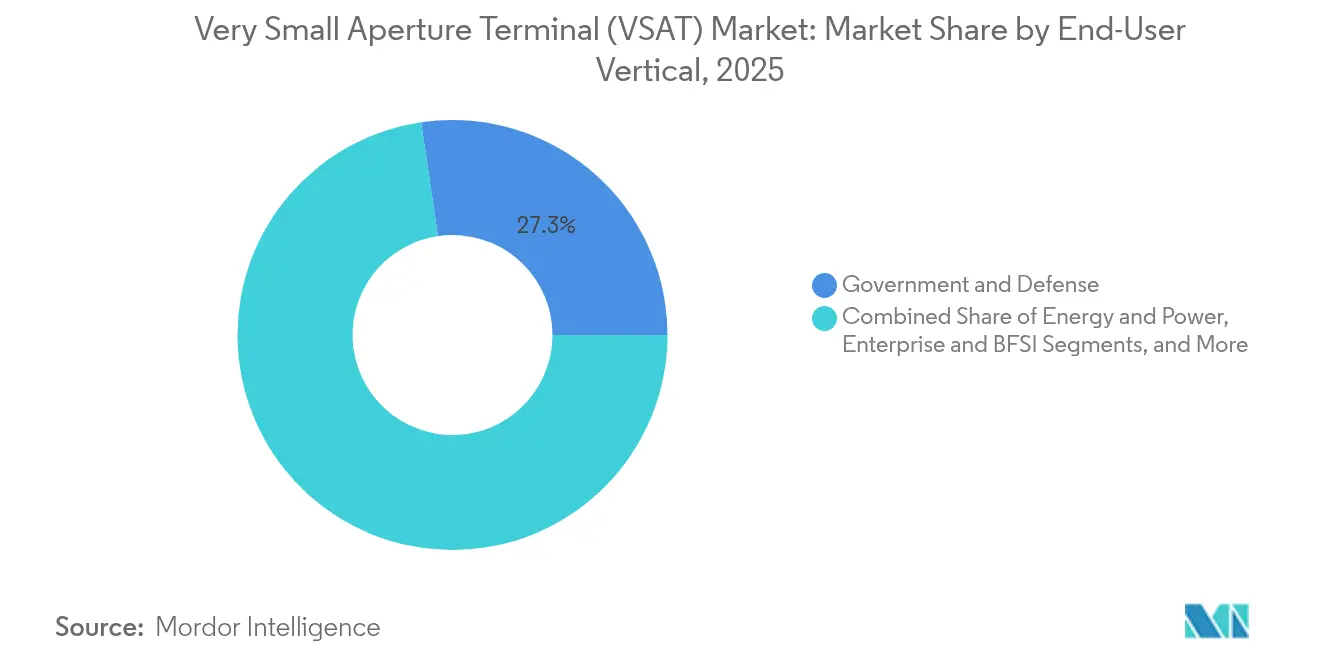

- By end-user, government and defense led with 27.33% share, while aviation IFC is projected to log a 14.45% CAGR through 2031.

- By application, data networks held 46.88% VSAT market share in 2025; IoT/M2M backhaul is slated for a 14.96% CAGR.

- By geography, North America dominated at 31.22% revenue share in 2025, whereas Asia-Pacific is expected to post the highest 11.84% CAGR on government-funded rural broadband.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Very Small Aperture Terminal (VSAT) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of HTS and LEO constellations enabling sub-USD 1/GB backhaul in Africa | +2.1% | Africa and wider MEA | Medium term (2-4 years) |

| Rising maritime digitalization and IMO e-Navigation mandates | +1.8% | Global shipping lanes | Short term (≤ 2 years) |

| Energy super-majors’ remote-field automation in the Middle East | +1.5% | Middle East & North Africa | Medium term (2-4 years) |

| Government-funded rural broadband in Asia | +1.9% | Core Asia-Pacific | Long term (≥ 4 years) |

| Airline IFC retrofit wave in North America and Asia | +1.6% | Major aviation hubs | Short term (≤ 2 years) |

| NATO-aligned procurement of man-packable VSATs | +1.3% | Allied defense markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of HTS and LEO constellations enabling sub-USD 1/GB backhaul in Africa

High-throughput satellites and proliferating LEO fleets are lowering bandwidth costs in rural Africa, where Starlink-driven subscriber numbers in Zimbabwe surged fivefold within a year.[1]Space in Africa, “Starlink Drives 500% Growth in VSAT Subscriptions in Zimbabwe,” spaceinafrica.com LEO systems cut latency and shrink deployment times, allowing mobile operators to extend 4G coverage into regions lacking fiber. Aggressive consumer pricing, including rental hardware models, is dismantling affordability barriers and fostering cross-border telecom partnerships. Regulators are equally supportive as Lesotho and other governments issue decade-long landing rights that view satellite connectivity as a catalyst for economic inclusion. The result is accelerating VSAT roll-outs that position the VSAT market for durable growth across underserved African geographies.

Rising maritime digitalization and IMO e-Navigation mandates

The Facilitation Convention now requires single-window data exchange, pushing shipping companies to upgrade from legacy L-band links to Ku- and Ka-band VSAT for primary communications.[2]Maritime Executive, “IMO: The Regulatory Framework for Maritime Data Sharing,” maritime-executive.com Upcoming IMO strategies covering AI-enabled navigation aim for a fully interconnected fleet by 2027, further spurring bandwidth demand. Vessel operators are embracing high-capacity GEO and NGSO paths to support just-in-time routing that cuts fuel burn by 14%. Flat-panel antennas ease deck-space constraints and drive adoption among mid-size vessels. Collectively, mandated digital reporting and efficiency targets reinforce Ku/Ka hardware refresh cycles across the global VSAT market.

Energy super-majors’ remote-field automation in the Middle East

Oil and gas operators estimate that advanced connectivity could unlock USD 250 billion in upstream value by 2030 through predictive analytics and robotics. Aramco’s investment in OneWeb links signals growing preference for LEO-enabled low-latency control in desert fields where fiber is unviable. Presently, only 5% of offshore sites use VSAT, leaving vast expansion headroom as digital twins and edge analytics gain traction. Multi-orbit terminals that blend GEO breadth with LEO responsiveness are becoming standard in drilling packages. This automation imperative propels equipment upgrades that enlarge the VSAT market footprint in energy corridors.

Government-funded rural broadband accelerating VSAT roll-outs in Asia

India’s BharatNet III allocates USD 16.7 billion to link 650,000 villages by 2025, with VSAT bridging terrain that fiber cannot economically reach.[3]ET Telecom, “Government to invest $13 billion more in BharatNet,” telecom.economictimes.indiatimes.com Policy incentives include viability-gap funding that offsets capital costs for private ISPs adopting satellite backhaul. Domestic Ku-band gateways operated by BSNL underscore the push for sovereign infrastructure. Competing LEO entrants like Starlink and Kuiper are negotiating access, hinting at hybrid fiber-satellite models to maximize coverage. Similar subsidy programs in Indonesia and the Philippines reinforce long-run demand visibility for the VSAT market throughout Asia-Pacific.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price compression from Starlink’s 50% cheaper bandwidth | -1.4% | Global GEO markets | Short term (≤ 2 years) |

| Supply-chain shortage of GaN high-power amplifiers | -0.8% | Worldwide manufacturing | Medium term (2-4 years) |

| Stringent ECC ESIM licensing delays in Europe | -0.5% | European Union | Short term (≤ 2 years) |

| High cap-ex for Ka-band gateways in emerging economies | -0.7% | Africa and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price compression from Starlink’s 50% cheaper bandwidth in GEO markets

Starlink delivers more than 102 Tbit/s of capacity and has struck headline airline deals that undercut legacy GEO pricing by half. Operators such as Hughes lost over 500,000 consumer subscribers within 15 months, highlighting elasticity in price-sensitive segments. To remain competitive, GEO incumbents are merging to unlock scale, as evidenced by the Viasat-Inmarsat and pending SES-Intelsat combinations. Meanwhile, enterprise buyers leverage LEO quotes to negotiate lower renewal rates. This margin squeeze dampens near-term revenue growth across the VSAT market.

Supply-chain shortage of GaN high-power amplifiers post-2024

China controls 98% of global gallium output, and new export restrictions heighten risks for RF component availability. A 30% disruption could erase USD 602 billion from the U.S. economy, prompting ESA to launch the GREAT2 program that seeds European foundries. VSAT manufacturers face longer lead times and rising amplifier costs, delaying terminal deliveries. Some operators now dual-source silicon-based alternatives, but efficiency losses complicate Ka-band system design. Unless diversification accelerates, supply tightness may curb equipment shipments and slow the VSAT market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Equipment Anchors Revenue While Services Drive Growth

The equipment slice generated more than half of total VSAT market revenue in 2025, reflecting high upfront spending on terminals, hubs, and gateways. Connectivity services, however, are delivering the fastest 11.6% CAGR as operators pivot to recurrence-based models that bundle capacity, security, and analytics. Heightened demand for multi-orbit resilience is prompting enterprises to outsource network management, allowing service providers to stack value-added offerings atop baseline bandwidth. This strategic shift balances hardware cycles and provides steadier cash flows, elevating investor confidence in the VSAT market.

HuBS and baseband refresh programs continue to lift equipment outlays as operators prepare infrastructure for Ka-band and LEO payloads. Market incumbents differentiate through terminal designs featuring integrated Wi-Fi, advanced SD-WAN, and edge computing. Meanwhile, support services benefit from mission-critical SLAs covering continuous monitoring and preventive maintenance. Together, these interlocking layers sustain a diverse revenue mix that keeps the VSAT market resilient amid pricing volatility.

By Platform: Land VSAT Dominates While Maritime Accelerates

Land deployments captured 47.35% of VSAT market share in 2025, powered by enterprise branch connectivity and public-sector digitization programs. Government tenders for community Wi-Fi and border-patrol surveillance keep demand stable, while remote-asset monitoring drives incremental links across mining and utilities. Despite land’s dominance, maritime connections are compounding fastest as ship operators adopt broadband for route optimization, crew welfare, and regulatory reporting. Antenna vendors are launching low-profile Ku/Ka solutions that withstand salt spray and vibration, facilitating retrofits across existing fleets.

Airborne applications add another high-growth dimension, especially as airlines upgrade cabins to maintain brand loyalty on long-haul routes. Portable and man-pack systems target defense users who need broadband in austere theaters. These complementary niches expand the addressable universe and help diversify the VSAT market away from any single platform category.

By Frequency Band: Ku-Band Leadership Challenged by Ka-Band Innovation

Ku-band continues to hold the largest slice of VSAT market revenue at 41.22%, buoyed by mature ground networks and global beam coverage. Yet Ka-band is posting a 14.02% CAGR thanks to spot-beam architectures that deliver 10- to 100-fold capacity gains and lower USD per GB costs. New Ka satellites feature digital payloads that allocate bandwidth dynamically, improving spectral efficiency. Rain fade still poses design hurdles, so integrators add adaptive coding and dual-band terminals to maintain uptime.

C-band remains indispensable for broadcast and high-power uplinks in equatorial rain zones, while X-band supports defense missions requiring encrypted payloads. Multi-band packages that blend these layers are gaining favor among energy majors and governments that value flexibility. This spectrum diversity safeguards capacity across multiple markets and keeps the VSAT market on a sustainable growth trajectory.

By Network Architecture: Star Topology Dominance Faces Mesh Challenge

Star networks accounted for 59.65% VSAT market size in 2025 because centralized hubs simplify management and enable easy multicast distribution. However, mesh architectures are rising at 10.78% CAGR as IoT and critical-infrastructure users demand site-to-site paths that bypass potential hub failures. Regenerative satellites and on-orbit routers accelerate adoption by reducing round-trip latency. Operators also deploy hybrid topologies that switch dynamically between star and mesh depending on application traffic.

Dedicated SCPC links endure where point-to-point capacity must remain deterministic, such as television contribution feeds or military gateways. Software-defined networking in the cloud orchestrates these varied paths, ensuring application SLA compliance. Architectural optionality thus becomes a competitive differentiator across the VSAT market.

By Type: Standard VSAT Leads While Micro Solutions Gain Momentum

Conventional terminals with apertures of 1 meter or larger contributed 72.34% of revenue in 2025, underscoring their reliability in enterprise WANs and government backbones. Micro VSAT units below 0.6 meter are, however, growing at 11.95% CAGR, propelled by rental models for retail outlets, ATMs, and disaster-response teams. Miniaturization lowers shipment costs and simplifies rooftop installs, creating new customer profiles that had previously considered VSAT impractical.

Standard terminals still dominate high-throughput links that support HD video, cloud backup, and VoIP trunking. They are now shipping with multi-band radios that auto-switch between GEO and LEO beams, shielding end-users from link degradation. This tiered product lineup secures both legacy and emerging use cases for the VSAT market.

By Design: Commercial-Grade Volume Meets Ruggedized Reliability

Commercial-grade enclosures delivered 35.16% of 2025 sales due to cost advantages in benign settings such as corporate campuses and retail outlets. Ruggedized designs, featuring sealed electronics and vibration-damped mounts, are advancing at 10.66% CAGR as militaries, maritime fleets, and energy firms deploy links in harsh environments. Defense buyers now insist on mil-spec radios with integrated interference-mitigation and stealth profiles, pushing average selling prices higher.

Vendors are borrowing thermal-management techniques from the automotive sector, improving reliability in desert or polar extremes without adding bulk. As a result, rugged systems penetrate commercial mining and construction markets that once settled for less capable gear. This design bifurcation diversifies supplier revenue streams inside the VSAT market.

By Antenna Technology: Parabolic Dominance Challenged by Flat-Panel Innovation

Parabolic dishes captured 62.05% revenue in 2025, prized for high gain and economical production. Flat-panel electronically steered antennas are enlarging their footprint at 13.01% CAGR as mobility customers value low drag and zero moving parts. Unit costs remain a headwind, yet economies of scale are improving with volume programs for aircraft and land vehicles.

Deployment kits now package phased-array panels with modems in a single enclosure, slashing install times. Hybrid arrays combine mechanical tilt with electronic azimuth, offering a cost bridge while full digital beamforming prices drop. These innovations position flat-panels to erode parabolic share gradually, reshaping hardware mix within the VSAT market.

By End-User Vertical: Defense Leadership Faces Aviation Growth

Defense agencies held 27.33% VSAT market share in 2025 after ramping SATCOM spending for ISR platforms, border security, and allied coalition operations. Aviation is the breakout vertical with a forecast 14.45% CAGR, driven by passenger experience imperatives and airline fleet modernization. Energy companies follow closely, equipping offshore rigs and desert pipelines with multi-orbit links for real-time analytics.

Maritime lines strengthen as decarbonization targets require continuous performance monitoring. Enterprise and BFSI segments maintain baseline demand for corporate VPN extensions and disaster recovery circuits. These diversified verticals cushion revenue swings, ensuring broad-based advancement of the VSAT market

By Application: Data Networks Lead While IoT Backhaul Accelerates

Data networks and broadband internet services controlled 46.88% revenue in 2025, reflecting universal demand for basic connectivity across government, enterprise, and consumer realms. IoT/M2M backhaul, expanding at 14.96% CAGR, leverages VSAT to link sensors on pipelines, power grids, and agriculture machines. Edge devices relay telemetry for predictive maintenance, lowering OPEX for asset-heavy operators.

Voice circuits still underpin mission-critical dispatch and defense channels, while private networks satisfy security-sensitive sectors. Video contribution benefits as HD and UHD streaming proliferate. The growing mix of bandwidth profiles sharpens the value proposition and enlarges the VSAT market size across diverse application stacks.

Geography Analysis

North America commanded 31.22% of global revenue in 2025, supported by government programs and early LEO adoption that embed redundancy across corporate and defense networks. Contracts such as NASA’s USD 4.8 billion Near Space Network keep public-sector volumes buoyant, while commercial airlines adopt simultaneous multi-orbit terminals to ensure gate-to-gate connectivity over polar routes. Canada’s resource sector and Mexico’s cross-border logistics further underpin steady demand, anchoring the region’s leading role in the VSAT market.

Asia-Pacific is the fastest-growing hub at a 11.84% CAGR through 2031, propelled by BharatNet in India, rural extension projects in Indonesia, and high-capacity Chinese payloads like ChinaSat-27 slated for launch in 2025. Governments co-fund VSAT gateways to close digital-divide gaps, and regional airline expansions fuel IFC upgrades. Starlink and Kuiper have already signed channel deals with Indian integrators, signaling deeper penetration of NGSO services that will raise the regional VSAT market size materially.

Europe advances steadily despite ECC ESIM licensing lags, thanks to entrenched GEO operators and Arctic coverage priorities for Nordic states. SES and Eutelsat leverage extensive teleports to address government and maritime users, while the Middle East and Africa experience robust energy-sector spending that could exceed USD 1.1 billion in annual SATCOM revenue by 2031. Latin America rounds out global growth as public Wi-Fi concessions and universal-service projects in Peru and Brazil tap VSAT to reach remote communities.

Competitive Landscape

Competition is intensifying as vertically integrated LEO constellations compress bandwidth prices and prompt legacy GEO operators to consolidate. The completed Viasat-Inmarsat deal and the proposed SES-Intelsat merger exemplify scale-seeking moves designed to pool spectrum and ground assets. Starlink’s end-to-end model challenges wholesale capacity sellers by bundling hardware, capacity, and cloud APIs, forcing incumbents to accelerate multi-orbit offerings.

Technology has become the primary differentiator. Hughes launched Mission Connect for defense agencies, combining GEO capacity with software-defined networking to secure tactical data links. Gilat’s USD 98 million acquisition of Stellar Blu provides phased-array know-how for aviation IFC, targeting USD 150 million incremental revenue in 2025. Operators also secure niche advantages in Arctic coverage or energy IoT to avoid direct price wars and keep margins defensible.

Strategic partnerships round out the competitive toolkit. Viasat integrated Telesat Lightspeed capacity to deepen Ka-band resources for mobility customers. Amazon Kuiper and Starlink forged early reseller accords with Indian VSAT integrators, ensuring local compliance and channel reach. As hybrid satellite-terrestrial platforms mature, ecosystem strength, rather than satellite count alone, will define long-term leadership inside the VSAT market.

Very Small Aperture Terminal (VSAT) Industry Leaders

Orbit Communications Systems Ltd.

Viasat Inc.

L3Harris Technology Inc.

Gilat Satellite Networks Ltd.

EchoStar Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Viasat integrated Telesat Lightspeed LEO capacity into its multi-orbit network, strengthening SLA-backed mobility offerings.

- June 2025: Starlink and Amazon Kuiper signed commercial distribution deals with VSAT operators in India.

- April 2025: Hughes became a Managed Service Provider within Airbus’ HBCplus IFC ecosystem.

- April 2025: Gilat secured more than USD 15 million in orders for VH-TS constellation terminals.

- March 2025: Delta Airlines chose the Hughes Fusion multi-orbit solution for A350 and A321neo fleet.

- February 2025: Gilat launched its dedicated Defense Division to meet rising tactical SATCOM demand.

- January 2025: Viasat won a USD 4.8 billion ceiling contract for NASA Near Space Network services.

Global Very Small Aperture Terminal (VSAT) Market Report Scope

A very small aperture terminal (VSAT) is a small-sized earth station used in the transmit or receive of data, voice and video signals over a satellite communication network, excluding broadcast television. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The very small aperture terminal (VSAT) market is segmented by solution (Equipment, Support Services and Connectivity Services), by platform (Land VSAT, Maritime VSAT, and Airborne VSAT), by application (Data Transfer, Voice Communications, Private Network, Broadcasting and Other Applications) and by geography (North America, Europe, Asia Pacific, South America, Middle East, and Africa). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Equipment |

| Support Services |

| Connectivity Services |

| Ground Infrastructure (Hub/Gateway) |

| Land VSAT |

| Maritime VSAT |

| Airborne VSAT |

| Portable/Man-pack VSAT |

| C-Band |

| Ku-Band |

| Ka-Band |

| X-Band |

| Multi-Band/HTS |

| Star Topology |

| Mesh Topology |

| Point-to-Point/SCPC |

| Hybrid |

| Standard VSAT |

| Ultra-Small Aperture Terminal (USAT/Micro VSAT) |

| Ruggedized |

| Commercial-Grade |

| Parabolic Dish |

| Flat-Panel Electronically Steered |

| Deployable/Fly-Away |

| Government and Defense |

| Energy and Power (Oil, Gas, Mining) |

| Maritime and Offshore |

| Aviation (Commercial and Business) |

| Enterprise and BFSI |

| Telecom Cellular Backhaul |

| Media and Broadcasting |

| Agriculture and Natural Resources |

| Emergency and Disaster Relief |

| Data Networks/Broadband Internet |

| Voice Communications |

| Private Network Services (VPN/MPLS) |

| Video Broadcasting and Streaming |

| IoT/M2M Backhaul |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Solution | Equipment | ||

| Support Services | |||

| Connectivity Services | |||

| Ground Infrastructure (Hub/Gateway) | |||

| By Platform | Land VSAT | ||

| Maritime VSAT | |||

| Airborne VSAT | |||

| Portable/Man-pack VSAT | |||

| By Frequency Band | C-Band | ||

| Ku-Band | |||

| Ka-Band | |||

| X-Band | |||

| Multi-Band/HTS | |||

| By Network Architecture | Star Topology | ||

| Mesh Topology | |||

| Point-to-Point/SCPC | |||

| Hybrid | |||

| By Type | Standard VSAT | ||

| Ultra-Small Aperture Terminal (USAT/Micro VSAT) | |||

| By Design | Ruggedized | ||

| Commercial-Grade | |||

| By Antenna Technology | Parabolic Dish | ||

| Flat-Panel Electronically Steered | |||

| Deployable/Fly-Away | |||

| By End-User Vertical | Government and Defense | ||

| Energy and Power (Oil, Gas, Mining) | |||

| Maritime and Offshore | |||

| Aviation (Commercial and Business) | |||

| Enterprise and BFSI | |||

| Telecom Cellular Backhaul | |||

| Media and Broadcasting | |||

| Agriculture and Natural Resources | |||

| Emergency and Disaster Relief | |||

| By Application | Data Networks/Broadband Internet | ||

| Voice Communications | |||

| Private Network Services (VPN/MPLS) | |||

| Video Broadcasting and Streaming | |||

| IoT/M2M Backhaul | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the VSAT market?

The VSAT market is valued at USD 7.02 billion in 2026 and is forecast to reach USD 11.55 billion by 2031.

Which segment is growing fastest within the VSAT market?

Connectivity services are expanding at an 11.6% CAGR as operators emphasize recurring revenue.

Why is Asia-Pacific the fastest-growing region?

Government-funded rural broadband programs such as India’s BharatNet drive large-scale deployments, pushing the region toward a 11.84% CAGR through 2031.

How are LEO constellations affecting VSAT pricing?

Providers like Starlink offer bandwidth at roughly half traditional GEO rates, prompting incumbents to adopt multi-orbit strategies and reduce prices.

Which frequency band is gaining traction for high-capacity applications?

Ka-band is recording the strongest 14.02% CAGR because spot-beam satellites can deliver 10-100 times the throughput of legacy Ku-band systems.

What factors limit VSAT growth despite strong demand?

Price compression, GaN amplifier shortages, and European ESIM licensing delays create near-term headwinds that operators must navigate.

Page last updated on: