Medical Device And MedTech Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

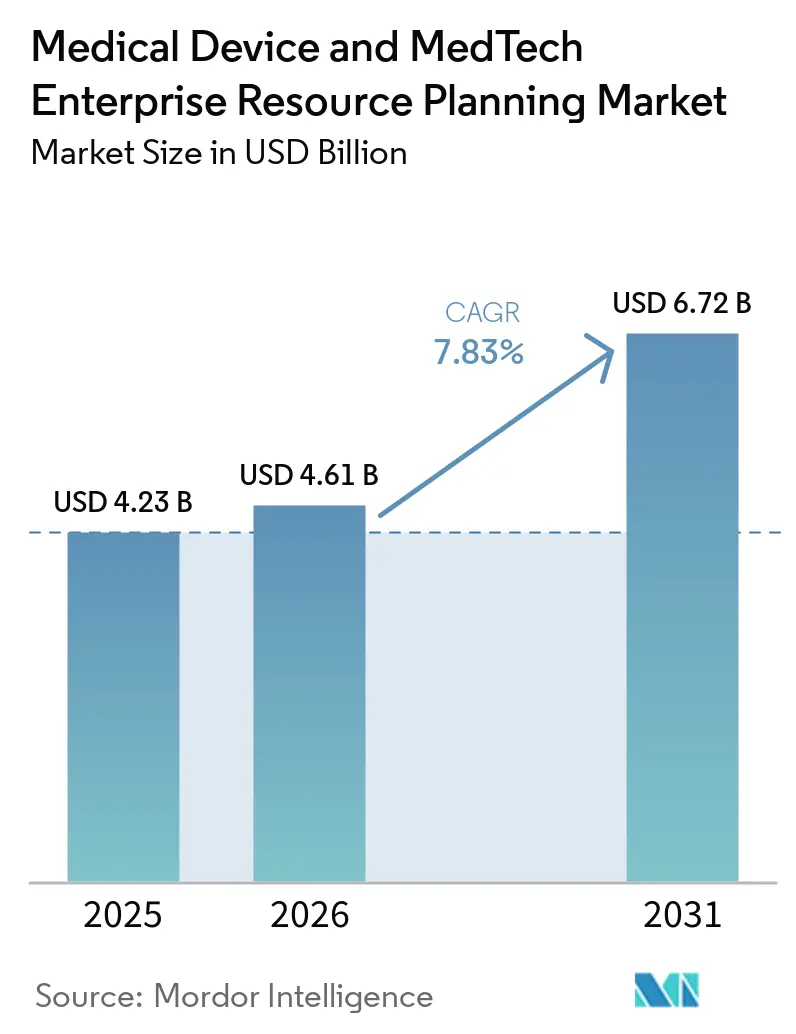

| Market Size (2026) | USD 4.61 Billion |

| Market Size (2031) | USD 6.72 Billion |

| Growth Rate (2026 - 2031) | 7.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Device And MedTech Enterprise Resource Planning Market Analysis by Mordor Intelligence

The Medical Device and MedTech enterprise resource planning market size is projected to expand from USD 4.23 billion in 2025 and USD 4.61 billion in 2026 to USD 6.72 billion by 2031, registering a CAGR of 7.83% between 2026 and 2031. The market’s trajectory reflects a decisive migration away from aging on-premise suites toward cloud-native platforms that automate quality compliance and embed AI forecasting. Cloud deployment already dominates current implementations, and the accelerating pace of EUDAMED and FDA deadlines is compressing buying cycles for validated, software-as-a-service offerings. Vendors are recasting roadmaps around pre-configured regulatory connectors, while buyers weigh validation costs against the flexibility of quarterly feature releases. Competitive intensity is rising as vertical-first challengers offer out-of-the-box UDI, lot-traceability, and post-market surveillance modules, pressuring enterprise resource planning incumbents to emphasize regulatory readiness over generic functionality. At the same time, cybersecurity incidents continue to temper pure-cloud enthusiasm, steering a subset of manufacturers toward hybrid architectures that retain sensitive device records on local servers.

Key Report Takeaways

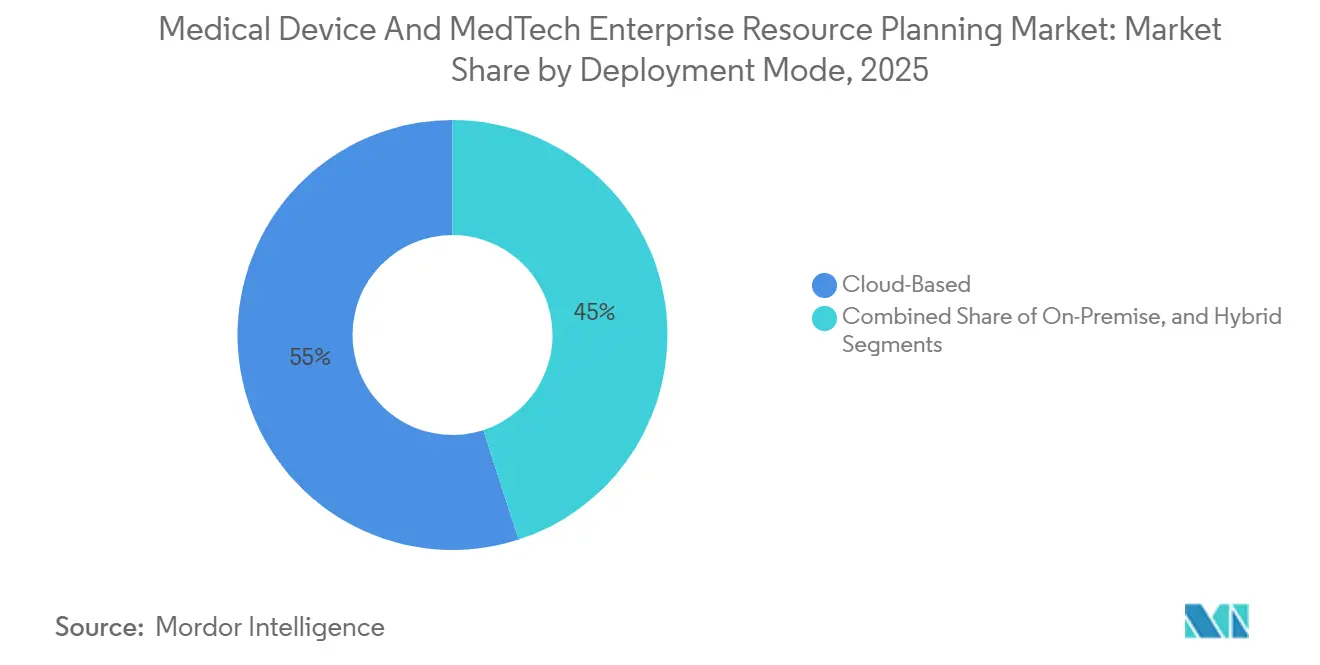

- By deployment mode, cloud-based systems led the Medical Device and MedTech Enterprise Resource Planning market with 54.98% market share in 2025 and are advancing at an 8.43% CAGR through 2031.

- By component, software commanded 69.77% revenue share in 2025, whereas services are the fastest-growing element at an 8.23% CAGR to 2031.

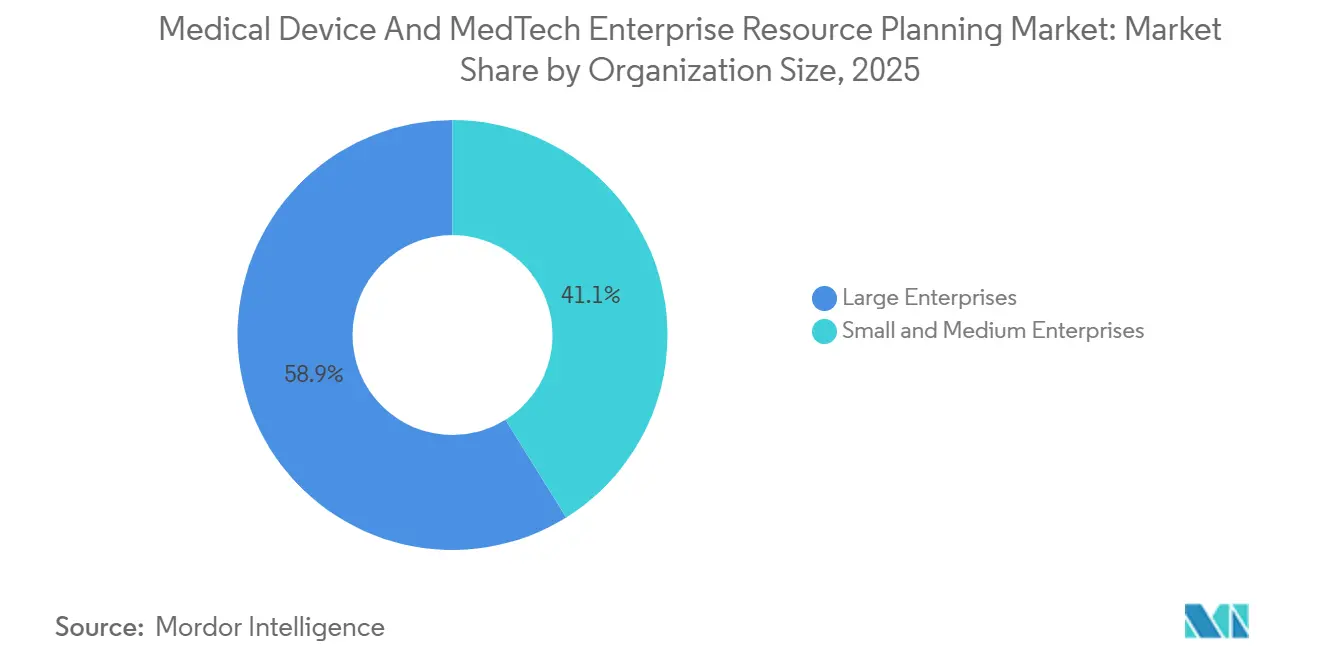

- By organization size, large enterprises accounted for 58.87% of 2025 spend, while small and medium enterprises are expanding at an 8.46% CAGR in the Medical Device and MedTech ERP market through 2031.

- By end user, medical device manufacturers accounted for 45.23% of outlays in 2025, while MedTech service providers are projected to expand at a 8.63% CAGR through 2031.

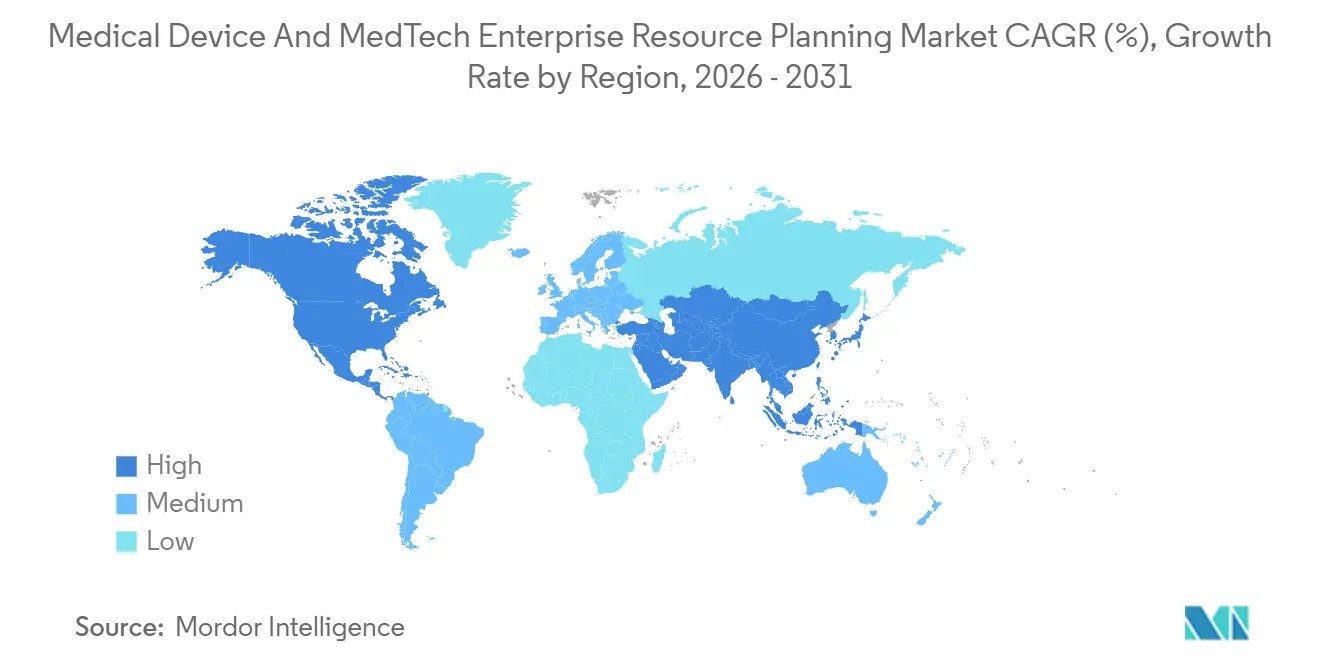

- By geography, North America dominated with a 38.39% share in 2025, yet Asia-Pacific is the fastest-growing region, with an 8.83% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Medical Device And MedTech Enterprise Resource Planning Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Regulatory Pressure for UDI and Quality Compliance | +1.8% | Global, with peak intensity in North America and Europe | Short term (≤ 2 years) |

| Shift Toward Cloud-native SaaS ERP Among Mid-sized MedTech Firms | +1.5% | Global, led by North America and Asia-Pacific | Medium term (2-4 years) |

| Rising Demand for Real-time Traceability in Globalized Supply Chains | +1.3% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Integration of IoT-enabled Shop-floor Data with ERP Platforms | +1.1% | Asia-Pacific core, spillover to North America | Medium term (2-4 years) |

| Surge in Post-merger System Consolidations in Medical Device Sector | +0.9% | North America and Europe | Short term (≤ 2 years) |

| Increasing Adoption of AI-driven Demand Forecasting Modules | +0.7% | North America and Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Regulatory Pressure for UDI and Quality Compliance

The May 28, 2026, deadline for mandatory EUDAMED submissions obliges manufacturers to load device master data, operator registrations, and vigilance reports into a central European database, prompting ERP vendors to release native connectors that populate serial numbers and certificates directly from product lifecycle modules. In the United States, the Quality Management System Regulation, which took effect on February 2, 2026, aligns computer system validation with ISO 13485:2016 and intensifies scrutiny of AI modules embedded in ERP quality workflows.[1] U.S. Food and Drug Administration, “Quality Management System Regulation,” fda.gov Oracle responded with a Health Device Validation Program that ships pre-validated scripts, cutting in half the installation qualification cycles for Class III device makers. Japan’s PMDA harmonization with ISO 13485 likewise boosts demand for multi-region templates capable of segregating FDA, EU, and Japanese establishment identifiers within a single master-data hierarchy. Collectively, these mandates nudge procurement decisions toward platforms that guarantee regulator-ready upgrades on a quarterly cadence.

Shift Toward Cloud-Native SaaS ERP Among Mid-Sized MedTech Firms

Subscription pricing that begins at USD 150 per user per month slashes the USD 2 million-plus capital outlay historically required for on-premise rollouts, bringing the Medical Device and MedTech enterprise resource planning market within reach of firms with USD 50 million to USD 500 million in annual sales. Microsoft’s Dynamics 365 deployments during 2025 embedded electronic batch records and deviation workflows, enabling 21 CFR Part 11 compliance without custom code. European mid-sized manufacturers closed go-lives in as little as 9 months by leveraging pre-configured lot-traceability templates, while Asia-Pacific firms favored hybrid clouds that keep intellectual property data in local data centers in deference to China’s Data Security Law. Rapid regulatory patching is an added lure: SaaS vendors can push new UDI formats or ISO revisions every quarter, whereas on-premises customers often defer upgrades to 3-year intervals. Even so, data-localization statutes continue to sustain hybrid demand, compelling providers to perfect low-latency synchronization between local quality systems and cloud financial ledgers.

Rising Demand for Real-Time Traceability in Globalized Supply Chains

Global supply chains spanning up to seven tiers leave device makers vulnerable to component genealogy gaps that frustrate recall execution. FDA guidance issued in 2025 obliges Class II and Class III manufacturers to maintain electronic links between finished-goods serial numbers and supplier lot numbers. SAP partnered with Fresenius in January 2026 to embed AI that cross-references temperature readings from in-transit sensors against historical defect rates, issuing pre-emptive alerts when environment excursions jeopardize sterility. Oracle’s Life Sciences AI Data Platform launched later that month to ingest supplier quality metrics from multiple ERP instances and flag high-risk vendors before nonconforming material reaches assembly lines. Blockchain-anchored ledgers and IoT telemetry now underpin audit trails that shrink recall window lengths from weeks to hours, a benefit that resonates as the European Commission moves toward 48-hour adverse-event reporting.

Integration of IoT-Enabled Shop-Floor Data With ERP Platforms

Manufacturing execution islands historically captured machine-cycle metrics but did not feed them to enterprise resource planning engines in real time. MachineMetrics released connectors for Infor and Epicor in March 2025, streaming sensor data straight into cost-of-goods calculations and automated quality holds. Siemens upgraded its Opcenter solution to push digital-twin-based process adjustments back into scheduling engines, improving first-pass yield for orthopedic implant lines. Asia-Pacific governments magnify adoption: South Korea budgeted KRW 500 billion in grants for small and medium enterprises deploying IoT sensors and cloud ERP, reimbursing up to 50% of project costs. The resulting convergence allows manufacturers to trigger automated recalibrations, rebalance labor, and update variance accounts within minutes of detecting drift on the factory floor.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Validation and FDA Computer System Validation Costs | -0.9% | North America and Europe | Short term (≤ 2 years) |

| Cybersecurity Concerns Slowing Cloud ERP Adoption | -0.7% | Global, with acute sensitivity in North America | Medium term (2-4 years) |

| Skills Gap in ERP Data Governance within MedTech SMEs | -0.5% | Global, most pronounced in Asia-Pacific and South America | Medium term (2-4 years) |

| Legacy MES-ERP Integration Complexities in Brownfield Plants | -0.4% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Validation and FDA Computer System Validation Costs

Despite the FDA’s 2024 shift to risk-based Computer Software Assurance, Class III device makers still budget around USD 1.2 million per ERP module for installation, operational, and performance qualification testing. Each quarterly cloud update triggers regression scripts, impact assessments, and archival of executed test evidence, prolonging release timelines and inflating consulting fees. The European Union mirrors these demands by requiring audit trails to remain accessible for up to 15 years, driving parallel validation costs. Cloud vendors now market validation-as-a-service bundles, and Acumatica’s turnkey documentation package costs USD 150,000; yet site-specific workflows and third-party integrations still mandate bespoke evidence generation. For a USD 50 million manufacturer, the expense equals 2.4% of annual revenue, underscoring why many SMEs postpone full-suite adoption.

Cybersecurity Concerns Slowing Cloud ERP Adoption

The February 2024 ransomware attack on Change Healthcare disrupted claims for 100 million U.S. patients and highlighted vulnerabilities in healthcare cloud stacks.[2]U.S. Department of Health and Human Services, “Change Healthcare Cyberattack,” hhs.gov In response, the FDA issued 2025 guidance advocating zero-trust architectures, multi-factor authentication, and encryption, but it stopped short of mandating a uniform framework, obliging vendors to self-certify. ISO 27001 certification now operates as table stakes for ERP providers, adding USD 200,000–USD 500,000 in annual overhead that smaller vendors struggle to absorb. Hybrid deployment models that keep UDI and clinical-trial data on-premise while hosting financial modules in the cloud have emerged as a mitigation strategy. However, synchronization latency extends the month-end close by 2 to 3 days, undermining one of the chief advantages of cloud upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Matures While Hybrid Bridges Data-Residency Gaps

Cloud deployments accounted for 54.98% of the Medical Device and MedTech enterprise resource planning market share in 2025 and are forecast to grow at an 8.43% CAGR through 2031, bolstered by mid-sized firms avoiding data-center investments of USD 2 million or more. Vendors are pulling end-of-support levers, SAP’s 2027 sunset for ECC and Oracle’s 2030 retirement of E-Business Suite, to prod customers toward SaaS subscriptions. The market size for on-premises instances will nonetheless persist among multinationals that prefer full control over software versioning and bespoke validation scripts. Hybrid architectures serve as a compromise for organizations subject to China’s Data Security Law or the European Union’s GDPR, allowing quality records to reside locally while planning engines run in global clouds.

Oracle’s process-manufacturing connectors synchronize shop-floor batch data every few minutes, addressing latency anxieties that once hampered hybrid rollouts. Microsoft and third-party quality consultants package risk-based validation templates that reduce go-live by 40%, shrinking perceived disadvantages of SaaS release cadences. Even so, quarterly feature pushes force manufacturers to maintain evergreen validation teams, while on-premise customers can bundle changes into a single multi-year retrofit. Across all deployment types, buyers now elevate cybersecurity posture and regulator-ready audit trails above generic functionality checklists, shifting evaluation scorecards toward compliance automation.

By Component: Services Outpace Software as Validation Demands Deepen

Software licenses and subscriptions accounted for 69.77% of market revenue in 2025, yet the services category is growing at an 8.23% CAGR as validation complexity increases. Implementation projects consume 12-18 months, with validation tasks accounting for up to 40% of billable hours, pressuring manufacturers to outsource Computer Software Assurance documentation to life-sciences specialists. The market for managed services is expanding as clients adopt continuous-compliance contracts that bundle quarterly validation, patch management, and regulatory monitoring services.

Infosys and Tricentis now automate regression testing during SAP S/4HANA migrations, reducing test-case generation by 40% and trimming overall project budgets. Data-migration consultancies likewise flourish as manufacturers cleanse decades of lot-traceability records before moving to multi-tenant clouds. Training engagements are another bright spot; quality engineers and supply-chain planners require upskilling to interpret AI-generated forecasts without violating validation protocols. With AI modules increasingly embedded at no extra software charge, revenue shifts downstream to advisory, training, and application-management add-ons that keep systems audit-ready.

By Organization Size: SMEs Leverage Modular SaaS for Rapid Compliance

Large enterprises retained 58.87% revenue share in 2025, propelled by multi-site consolidations such as Boston Scientific’s USD 120 million SAP S/4HANA rollout following its Axonics acquisition. Yet SMEs are the market’s fastest-growing cohort, with an 8.46% CAGR, thanks to modular subscriptions that convert capital outlays into operating expenses. Rootstock reports that 78% of its medical device customers deploy standard configurations with fewer than ten custom fields, sidestepping coding altogether. That approach minimizes validation scope and accelerates go-live timelines to as little as six months.

The skills gap remains a hurdle. SMEs often lack dedicated compliance officers and must re-skill quality engineers to manage electronic batch records and UDI submissions within ERP screens. Still, subscription bundles that package validation-as-a-service and managed hosting allow smaller firms to clear regulatory bars they once considered unattainable. Large enterprises will continue to dominate spending on complex integrations, such as linking SAP financials with Siemens digital-twin MES, but SMEs represent the locus of incremental cloud volume for the remainder of the decade.

By End-User: Service Providers Capture Share on Traceability Demands

Device manufacturers accounted for 45.23% of 2025 outlays, yet MedTech service providers, sterilization, calibration, repair, and reprocessing specialists are expanding at an 8.63% CAGR. The market share for contract manufacturing organizations, while smaller, is rising as sponsors demand real-time batch genealogy and electronic device history records for investigational exemptions. Service centers need warranty management, installed-base tracking, and mobile remote-service apps to streamline turnaround times and demonstrate compliance during customer audits.

Platforms such as Plex Systems report 25% shorter warranty-claim cycles after automating serial-number lookups and parts availability inside unified workflows.[3]Plex Systems, “Medical Device Industry Solutions,” plex.com Contract manufacturers favor multi-tenant architectures that let each sponsor maintain segregated quality data while sharing equipment utilization metrics. Implementation speed is paramount; Rootstock can onboard a newly acquired entity in roughly 30 days by cloning validated templates, giving private-equity roll-ups a repeatable playbook for bolt-on acquisitions.

Geography Analysis

North America accounted for 38.39% of the market in 2025, propelled by stringent FDA oversight and a dense population of multinational device makers. The new Quality Management System Regulation obliges firms to re-validate ERP controls, spurring a wave of validation-as-a-service contracts. Post-merger consolidations, such as Boston Scientific’s Axonics integration, underscore how acquisitions catalyze full-suite S/4HANA migrations that unify 16 or more manufacturing sites under a single global ledger. Canada and Mexico are emerging as nearshore contract-manufacturing hubs that install cloud ERP systems to meet the real-time traceability requirements of U.S. sponsors.

Asia-Pacific is the fastest-growing region, expanding at an 8.83% CAGR through 2031. China’s phased UDI rollout for Class III devices in 2024 and Class II in 2025 obliges domestic factories to deploy serial-number and EUDAMED-style connectors, steering investment toward platforms that can align with both European and U.S. identifiers. India’s Production Linked Incentive scheme reimburses up to 5% of incremental sales for plants equipped with IoT-enabled ERP, accelerating adoption among greenfield projects.[4]Government of India, “Production Linked Incentive Schemes,” investindia.gov.in South Korea subsidizes sensor-driven smart factories, while Japan’s Society 5.0 agenda incentivizes IoT-ERP convergence among Tier 2 suppliers seeking ISO 13485 harmonization.

Europe maintains substantial share, anchored by the Medical Device Regulation and the May 2026 EUDAMED deadline that effectively forces ERP modernization for any exporter. Manufacturers racing to meet the 48-hour adverse-event reporting proposal now view real-time traceability as a must-have, sparking demand for AI modules that correlate shipment conditions with defect probabilities. South America and the Middle East and Africa remain nascent but show steady uptake as local plants aim to mirror parent-company quality systems and gain preferred-supplier status with global brands.

Competitive Landscape

The Medical Device and MedTech ERP market remains moderately fragmented. SAP, Oracle, and Microsoft vie with vertical-specialist challengers such as QAD, Epicor, and Plex, while cloud-native upstarts Rootstock, Acumatica, and Priority Software target mid-market buyers demanding pre-validated templates. Differentiation hinges on compliance automation: Oracle’s February 2026 Health Device Validation Program ships pre-validated scripts, while SAP’s January 2026 alliance with Fresenius embeds AI analytics that correlate cold-chain sensor data with defect rates. Hybrid-cloud mastery is another battleground, as multinationals seek low-latency synchronization that straddles China’s data-residency rules without fragmenting global financial visibility.

Salesforce-native ERPs leverage the customer relationship platform’s vast ecosystem to bolt on field-service, commerce, and analytics without custom middleware. Dassault Systèmes pursues an end-to-end digital-thread strategy by linking design, simulation, and ERP within a single platform, enabling the instant propagation of engineering changes into supplier purchase orders. Siemens embeds digital twin models within execution systems that feed real-time parameters back to scheduling modules, automating corrective actions before nonconformances reach finished goods.

AI-driven demand forecasting marks the next frontier; Microsoft’s EDGE for Operations applies reinforcement learning to rebalance inventories dynamically, while Oracle’s Life Sciences AI Data Platform flags high-risk suppliers days before delivery. Growing cybersecurity expectations raise the bar for new entrants. ISO 27001 certification and zero-trust blueprints have become gating criteria, eliminating vendors unable to prove SOC 2-type controls. At the same time, escalating validation costs incentivize buyers to favor vendors that bundle turnkey Computer Software Assurance, shrinking time-to-value for regulatory sign-off.

Medical Device And MedTech Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Infor Inc.

QAD Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Oracle launched its Health Device Validation Program, providing pre-validated installation and operational qualification scripts that cut validation timelines from 18 months to nine months for Class III manufacturers.

- February 2026: Infosys partnered with Tricentis to automate regression testing during SAP S/4HANA migrations, promising a 40% reduction in validation cycles.

- February 2026: Oracle released process-manufacturing enhancements that use generative AI to draft production schedules based on equipment and material constraints.

- January 2026: Oracle unveiled the Life Sciences AI Data Platform to flag supplier quality risks in real time.

- January 2026: SAP entered a partnership with Fresenius to embed AI analytics that correlate sensor data with defect rates inside SAP S/4HANA.

Global Medical Device And MedTech Enterprise Resource Planning Market Report Scope

The market refers to the market for enterprise resource planning solutions specifically designed to support the operational, manufacturing, regulatory, and supply chain management needs of organizations in the medical device and broader medical technology (MedTech) industry. These ERP systems integrate critical business functions such as production planning, inventory management, quality control, regulatory compliance, financial management, and product lifecycle tracking into a unified platform, enabling organizations to streamline operations, maintain regulatory compliance, and improve operational visibility across the value chain.

The Medical Device and MedTech Enterprise Resource Planning Market Report is Segmented by Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Component (Software, and Services), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-user (Medical Device Manufacturers, MedTech Service Providers, Contract Manufacturing Organizations, and Clinical Research Organizations), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Based |

| On-Premise |

| Hybrid |

| Software |

| Services |

| Large Enterprises |

| Small and Medium Enterprises |

| Medical Device Manufacturers |

| MedTech Service Providers |

| Contract Manufacturing Organizations |

| Clinical Research Organizations |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Deployment Mode | Cloud-Based | ||

| On-Premise | |||

| Hybrid | |||

| By Component | Software | ||

| Services | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-user | Medical Device Manufacturers | ||

| MedTech Service Providers | |||

| Contract Manufacturing Organizations | |||

| Clinical Research Organizations | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will medical device and medtech enterprise resource planning market become by 2031?

The medical device and medtech enterprise resource planning market size is expected to reach USD 6.72 billion by 2031, growing at a CAGR of 7.83% over 2026-2031.

Which region presents the fastest growth opportunity for Enterprise Resource Planning vendors?

Asia-Pacific leads with an 8.83% CAGR, propelled by China’s UDI mandate, India’s Production Linked Incentive subsidies, and South Korea’s smart-factory grants.

What challenges most deter small manufacturers from adopting full-suite Enterprise Resource Planning?

High Computer System Validation costs, which can reach USD 1.2 million per module, and a limited pool of compliance talent remain the biggest barriers for SMEs.

Why are service revenues growing faster than software licenses?

Validation, data-migration, and managed-services engagements now account for a rising share of project budgets as firms outsource continuous compliance tasks.

How are vendors addressing regulatory deadlines such as EUDAMED?

Leading providers embed native connectors and ship pre-validated scripts that populate device identifiers and clinical data directly into mandated databases.

What role does AI play inside modern MedTech Enterprise Resource Planning suites?

AI engines support demand forecasting, supplier risk scoring, and real-time quality analytics, helping manufacturers cut inventory and detect defects earlier.

Page last updated on: