ERP Implementation Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

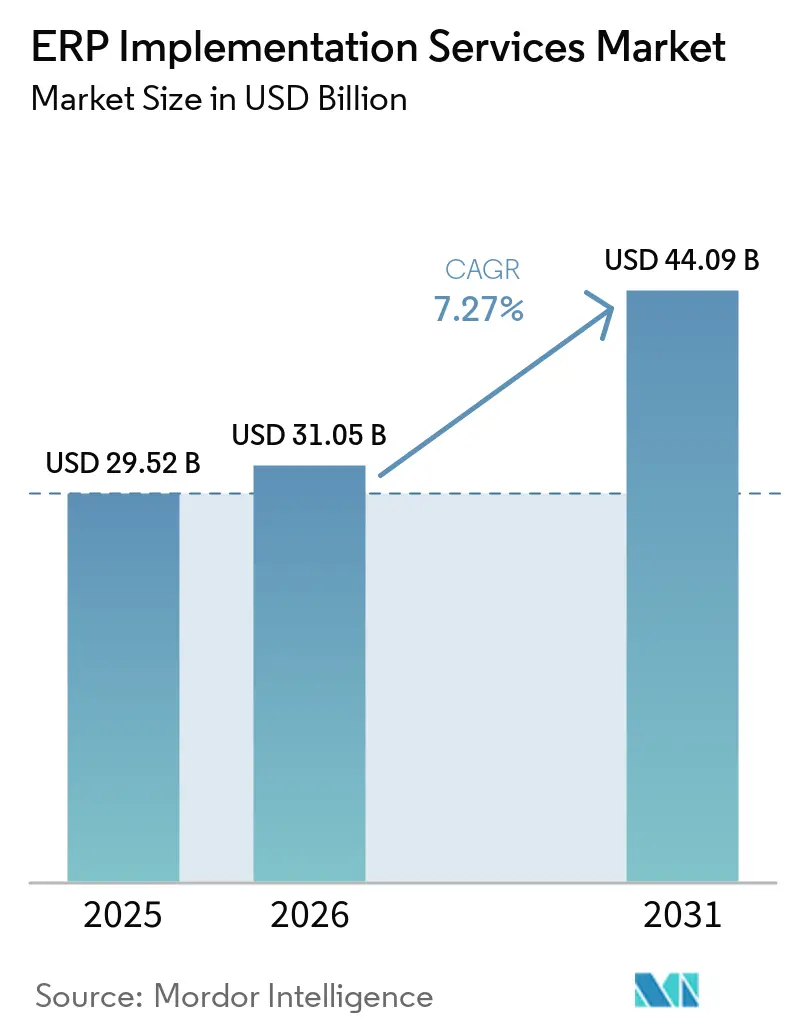

| Market Size (2026) | USD 31.05 Billion |

| Market Size (2031) | USD 44.09 Billion |

| Growth Rate (2026 - 2031) | 7.27% CAGR |

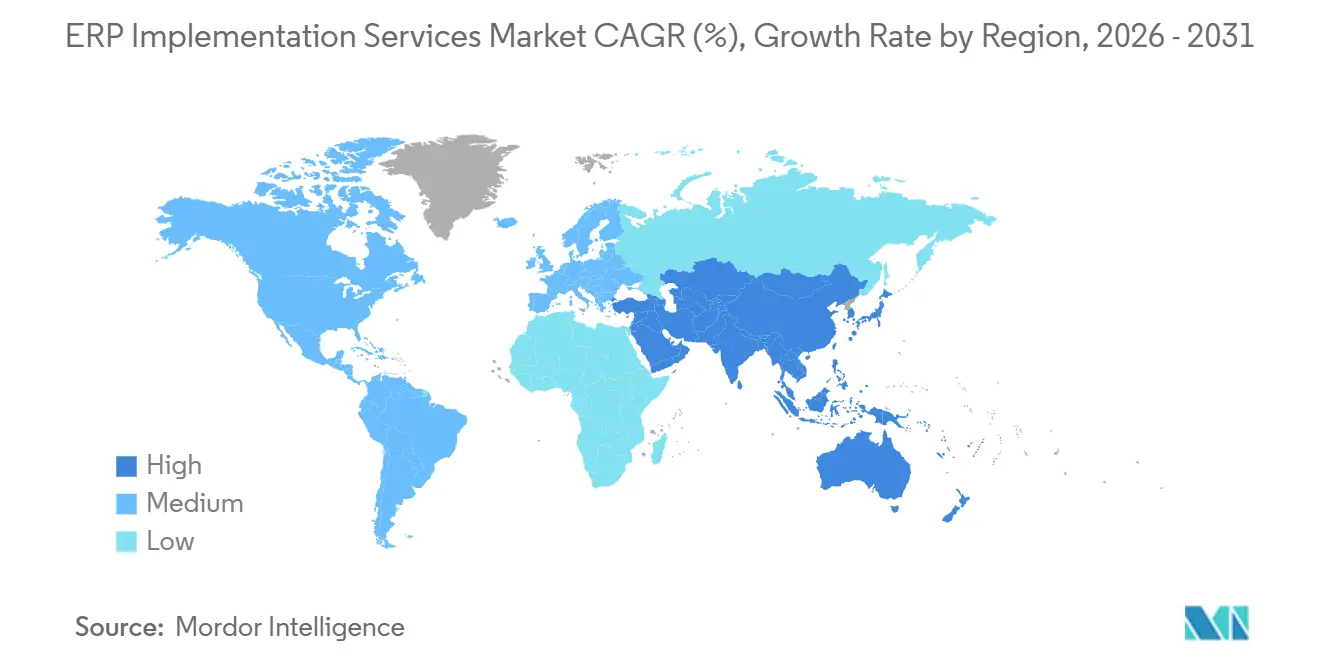

| Fastest Growing Market | Middle East |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ERP Implementation Services Market Analysis by Mordor Intelligence

The ERP implementation services market size expanded from USD 29.52 billion in 2025 to USD 31.05 billion in 2026 and is projected to reach USD 44.09 billion by 2031, registering a 7.27% CAGR over 2026-2031. Rising demand reflects enterprises moving away from incremental upgrades toward cloud-native platforms that embed artificial intelligence within transactional workflows. The shift is accelerated by SAP’s 2027 end-of-support deadline for ECC 6.0, which is pushing roughly 12,000 customers to S/4HANA. Cloud deployments accounted for 58% of 2025 revenue, yet regulated industries are assembling hybrid topologies that keep sensitive data on-premises while leveraging public-cloud analytics, a configuration now advancing at 17.8% annually. Large enterprises held 63% of 2025 spending, but small and medium enterprises are adopting subscription-based ERP at a 14% CAGR because vendors have begun unbundling core financials from vertical modules, slashing upfront capital outlays. Implementation demand is also propelled by real-time, data-driven decision-making, stricter compliance in sectors such as healthcare and banking, and the rise of agentic AI tools that reduce configuration and testing time.

Key Report Takeaways

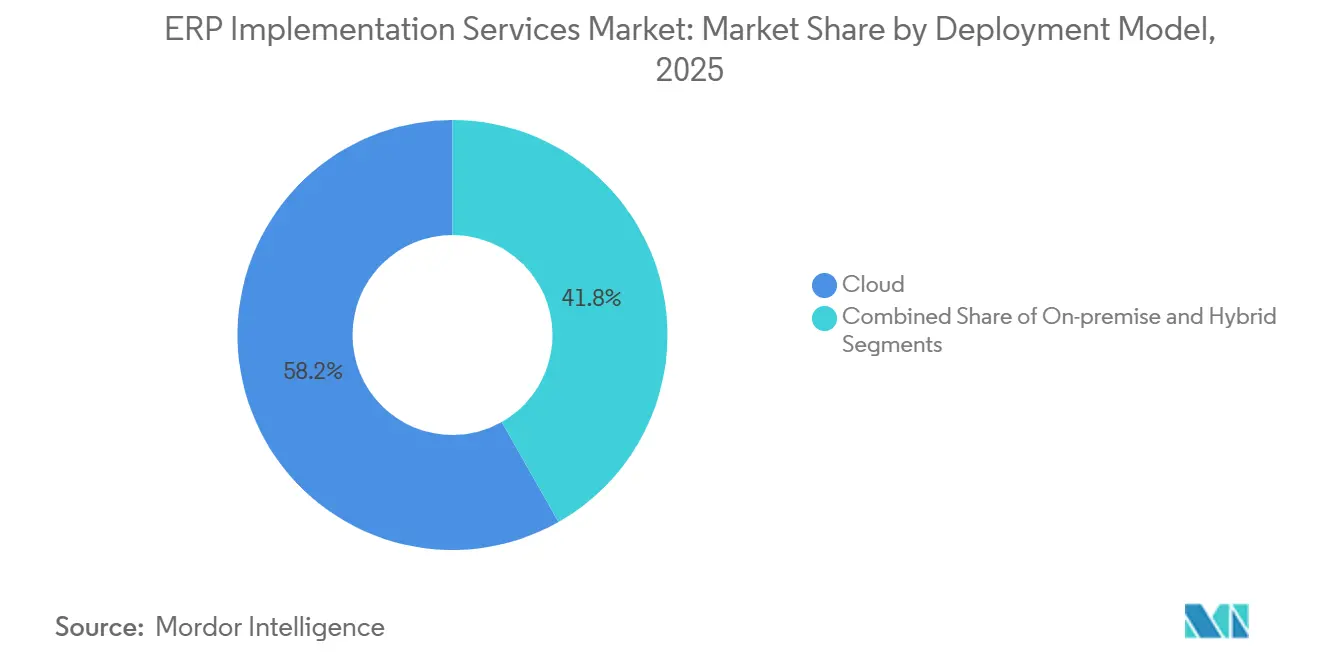

- By deployment model, cloud captured 58% of the ERP implementation services market share in 2025, while hybrid architectures are advancing at a 17.8% CAGR through 2031.

- By organization size, large enterprises commanded 63% of the ERP implementation services market size in 2025, whereas small and medium enterprises are expanding at a 14% CAGR to 2031.

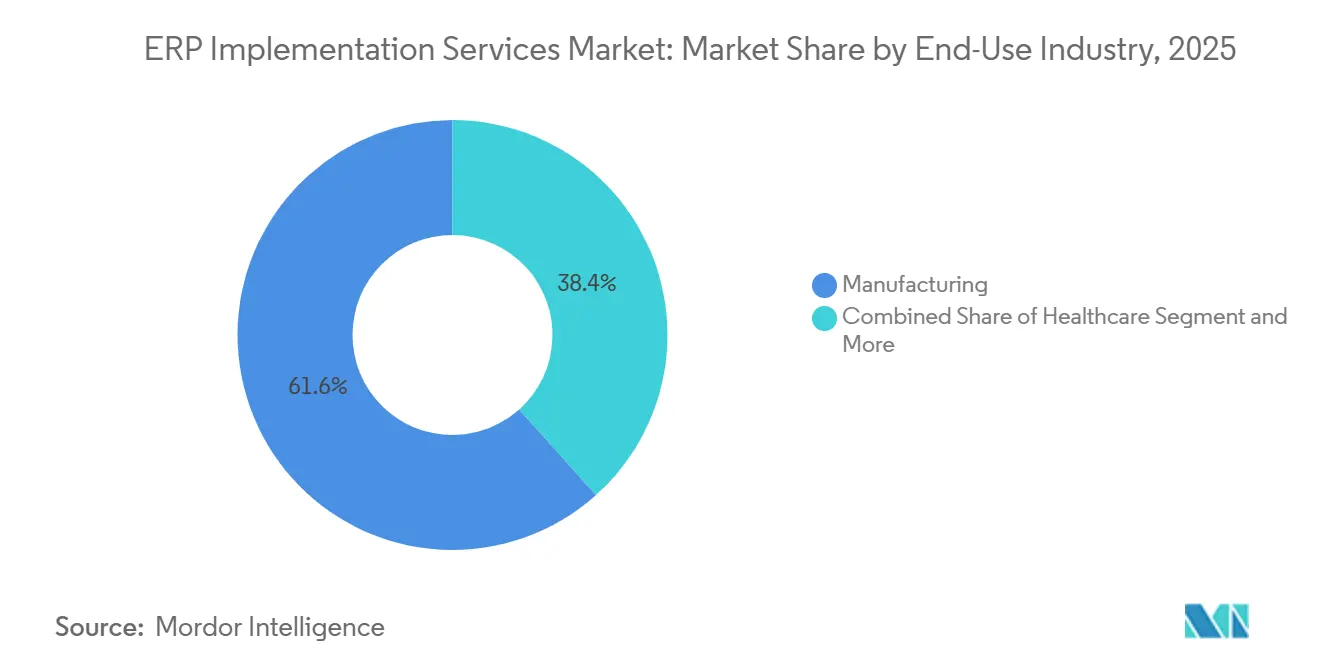

- By end-use industry, manufacturing accounted for 24% of 2025 spending, and healthcare is slated to grow at a 15% CAGR during 2026-2031.

- By geography, North America accounted for 37% of 2025 spending, and the Middle East is slated to grow at a 16% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global ERP Implementation Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-First Digital Transformation Mandates | +2.1% | Global, especially North America, Europe, Middle East | Medium term (2-4 years) |

| Surge in Real-Time Data-Driven Decision Making | +1.8% | Global, led by Asia-Pacific and North America manufacturing hubs | Medium term (2-4 years) |

| Rapid Subscription-Based ERP Uptake Among SMEs | +1.5% | Global, concentrated in North America, Europe, India | Short term (≤ 2 years) |

| Compliance-Induced ERP Modernization in Regulated Sectors | +1.2% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| AI-Enabled Automated Configuration and Testing | +0.9% | North America, Europe, early adopters in Middle East | Short term (≤ 2 years) |

| Vertical-Specific Composable Micro-Service Frameworks | +0.7% | Global, niche uptake in manufacturing, retail, healthcare | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Digital Transformation Mandates

Governments have tied modernization budgets to certified cloud adoption, compressing purchasing cycles and steering public-sector spending toward hyperscaler-hosted ERP. The United States Office of Management and Budget’s 2024 cloud directive and the European Union’s Digital Decade program are propelling migrations, while Saudi Arabia’s 2025 National Cloud Computing Framework bans new on-premises ERP purchases. Integrators are grappling with a skills gap because 40% of consultants still lack multi-tenant SaaS expertise.[1]Office of Management and Budget, “Federal Cloud-Smart Strategy,” whitehouse.gov

Surge in Real-Time Data-Driven Decision Making

Manufacturers now embed ERP systems within operational technology networks to re-plan production the moment supply-chain anomalies surface. Siemens integrated SAP S/4HANA with its MindSphere IoT suite across 15 factories in 2025, reducing inventory holding costs by 18%. [2]Siemens AG, “MindSphere and SAP S/4HANA Power Smart Factories,” press.siemens.com Automotive OEMs and large retailers are echoing the model, linking demand forecasts to supplier lines and point-of-sale feeds, respectively, thereby reducing monthly close cycles from 10 days to 3 days. [3]Oracle Corporation, “Oracle Retail Suite Enables Real-Time Merchandising,” oracle.com

Rapid Subscription-Based ERP Uptake Among SMEs

Oracle NetSuite’s starter bundles at USD 999 per month and Microsoft Business Central’s essentials tier at USD 70 per user per month have eliminated the USD 50,000-100,000 license hurdle for firms with fewer than 50 employees. SME ERP penetration in North America rose from 38% in 2023 to 52% in 2025, and typical implementation hours have fallen from 200 to 40 thanks to template-driven setups. [4]U.S. Small Business Administration, “Small Business Technology Adoption,” sba.gov Although customization flexibility narrows, SMEs favor the lower switching costs of month-to-month contracts.

Compliance-Induced ERP Modernization in Regulated Sectors

Updated rules, such as Europe’s PSD2 for banking, the U.S. 21st Century Cures Act for healthcare, and the FDA’s electronic batch record requirement, are compelling institutions to retire legacy ERPs that cannot deliver immutable ledgers or HL7/FHIR interfaces. Integrators increasingly bundle compliance assessments with deployments, a premium service that can lift project margins by 15-20%.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost of Ownership for Brownfield Integrations | -1.4% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Shortage of Skilled ERP Functional Consultants | -1.1% | Global, most severe in North America and Europe | Short term (≤ 2 years) |

| Data Sovereignty Barriers in Multi-Tenant Environments | -0.8% | Europe, China, India, emerging regions | Long term (≥ 4 years) |

| Vendor Lock-In Risks with Low-Code Extension Platforms | -0.5% | Global, concentrated in mid-market enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership for Brownfield Integrations

Surveys show that 68% of SAP ECC customers have more than 500 custom objects, ballooning refactoring budgets by 40-60% during migration to S/4HANA. Similar challenges plague Oracle E-Business Suite customers whose bespoke forms lack direct upgrade paths to Oracle Cloud ERP. Integration of dozens of bolt-on applications often consumes 30-40% of project spend, prompting 34% of mid-market manufacturers to extend on-premises support contracts instead of moving to the cloud.

Shortage of Skilled ERP Functional Consultants

SAP disclosed in late 2025 that North American and European demand for S/4HANA-certified professionals outstripped supply three-to-one, causing 15% of planned go-lives to slip. Oracle Cloud ERP and Microsoft Dynamics 365 face parallel gaps, with fewer than 5,000 fusion-architecture consultants worldwide as of December 2025. Partners have pushed utilization above 90%, driving day-rates higher and forcing some firms to offshore work where experience remains thin.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Architectures Reconcile Sovereignty and Scale

Hybrid deployments captured 17.8% CAGR during 2026-2031, the fastest pace among models, as banks, healthcare chains, and defense contractors hold master data behind the firewall while routing analytics to public cloud. Cloud configurations still accounted for 58% of 2025 revenue, primarily from digital-native firms and SMEs that treat infrastructure as a utility, whereas on-premises estates contracted but persisted in air-gapped defense networks. Sovereign cloud variants introduced by SAP and Oracle in 2025 keep data within national borders and command 25-35% price premiums, illustrating how sovereignty adds complexity but also value. Integrators monetize the intricacy by selling governance frameworks that trim post-go-live incidents 40%, thereby reinforcing recurring revenue streams tied to managed services.

Enterprises that lean on hybrid models increasingly blend event-streaming platforms with ERP cores, enabling manufacturing plants to process telemetry locally while still pushing aggregated insights to cloud lakes for advanced analytics. The dual-stack approach expands the ERP implementation services market by requiring system integrators to design secure network overlays, latency-aware data pipelines, and standardized integration patterns. By 2031, hybrid architectures are expected to underpin compliance in sectors dealing with personally identifiable information, national security data, and regulated financial records, reinforcing their role as a long-term bridge between legacy investments and full-cloud aspirations.

By Organization Size: SMEs Accelerate as Vendors Unbundle Suites

Large enterprises accounted for 63% of the ERP implementation services market in 2025 through global transformation programs spanning finance, supply chain, and workforce analytics. Growth, however, is tilting toward small and medium enterprises, which are scaling at a 14% CAGR, driven by modular subscriptions that lower capital barriers. Pre-configured templates such as Oracle SuiteSuccess and Microsoft Rapid Start compress deployment from nine months to as little as 12 weeks, creating an attractive total cost of ownership narrative for companies with USD 10 million-50 million in annual revenue. As a result, the ERP implementation services market increasingly depends on volume-driven SME rollouts rather than a handful of mega-deals.

Vendors now court mid-market customers with bundled migration tools, 40 hours of remote consulting, and month-to-month cancellation clauses that limit vendor lock-in risk. This tactic has expanded penetration in hospitality, nonprofit, and light manufacturing segments that once relied on spreadsheets and isolated accounting applications. For large enterprises, spending is shifting toward composable extensions, control towers, sustainability ledgers, and predictive maintenance engines, rather than outright core replacements, signaling a maturation phase that will moderate their contribution to absolute growth yet deepen services annuities tied to value-added modules.

By End-Use Industry: Healthcare Surges on Interoperability Mandates

Manufacturing retained a 24% market share in ERP implementation services in 2025 as automotive and industrial equipment makers embedded industrial IoT feeds directly into production planning modules. Healthcare, nonetheless, is projected to post a 15% CAGR to 2031, the fastest among verticals, because the U.S. 21st Century Cures Act penalizes hospitals that cannot integrate billing with electronic health records. This interoperability mandate is forcing chief information officers to jettison fragmented departmental software in favor of unified revenue-cycle platforms. Retail and e-commerce firms are also modernizing their ERPs to orchestrate omnichannel fulfillment, while banking institutions are upgrading their treasury and risk modules to comply with instant payments and open-banking APIs.

Government agencies worldwide are consolidating fragmented ledgers under a single cloud ERP umbrella to enhance fiscal transparency, as exemplified by Australia’s USD 385 million defense ERP overhaul in 2025. Telecommunications operators, in turn, are automating order-to-cash processes for subscription services, linking provisioning and billing within the ERP core. Construction and energy firms are adopting project-centric ERP modules that monitor budgets, schedules, and compliance across multi-year capital builds, demonstrating the broadening relevance of the ERP implementation services market across the industrial spectrum.

Geography Analysis

North America generated 37% of 2025 revenue, supported by compliance-driven refresh cycles in financial services and healthcare, and by the 2024 U.S. federal cloud mandate, which channels USD 3.5 billion per year into cloud ERP. Canada is consolidating provincial systems to cut operating costs, and Mexico’s automotive exporters are modernizing their ERPs to meet United States-Mexico-Canada Agreement traceability requirements. Implementation partners with FedRAMP accreditation both dominate federal work and cross-sell similar governance frameworks to regulated private sectors.

The Middle East is the fastest-growing region, charting a 16% CAGR over 2026-2031. Saudi Arabia’s Vision 2030 and the UAE’s cloud-first federal policy have banned fresh on-premises ERP purchases for government agencies, funneling USD 1.2 billion annually into local hyperscaler regions. Projects such as NEOM showcase integrated ERP platforms managing construction, utilities, and municipal services for an eventual population of 1 million, providing a marquee reference for Gulf Cooperation Council smart-city initiatives.

Asia-Pacific is bifurcated. China’s Data Security Law forces state-owned manufacturers onto domestic ERP stacks, raising integration complexity and cost, while India’s Digital India subsidies encourage SMEs to adopt global cloud platforms. Japan leverages ERP-IoT fusion to offset labor shortages, and Australia’s public sector pursues cloud ERP to bolster transparency. Europe is focusing on embedding sustainability and cyber-resilience metrics into ERP systems to comply with the Corporate Sustainability Reporting Directive. South America and Africa remain nascent but show pockets of activity in Brazil, Argentina, South Africa, and Nigeria, where electronic invoicing and core banking upgrades anchor demand.

Competitive Landscape

The ERP implementation services market is moderately concentrated. SAP, Oracle, and Microsoft have extended their software franchises into advisory and delivery services, often competing directly with their own partner ecosystems. SAP’s services arm now targets strategic S/4HANA projects, prompting partners to differentiate via sector depth or proprietary automation tools. Oracle Consulting and Microsoft’s FastTrack program similarly undercut third-party rates for large deals, compressing integrator margins.

Global system integrators Accenture, Deloitte, IBM, Capgemini, PwC, and KPMG respond by weaving agentic AI into delivery blueprints. Deloitte’s INTEGRATE platform, launched in 2026, auto-generates data-migration scripts and test cases, slicing project timelines by 25-30%. Indian majors Tata Consultancy Services, Infosys, and Wipro leverage cost advantages and hyperscaler alliances, reflected in Microsoft’s December 2025 allocation of more than 200,000 Copilot licenses to these firms. Mid-tier integrators such as Cognizant, DXC, and CGI pursue acquisitions to shore up specialized skills, typified by Cognizant’s 2025 purchase of Thirdera for workflow automation expertise.

White-space opportunities have emerged in composable ERP, where enterprises assemble best-of-breed modules linked through APIs rather than adopting monolithic suites. This favors firms steeped in integration middleware. Rimini Street exploits another niche by offering third-party support at half the cost of vendor maintenance, letting clients divert savings toward digital initiatives while delaying full migrations. Regulatory bodies have yet to impose interoperability standards, although the IEEE began work on an open-exchange protocol in 2025, with enterprise adoption unlikely before 2030.

ERP Implementation Services Industry Leaders

Accenture plc

Deloitte Touche Tohmatsu Limited

Capgemini SE

Tata Consultancy Services Limited

International Business Machines Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Deloitte and UiPath introduced an agentic ERP solution that deploys autonomous AI agents to configure workflows, migrate data, and execute test scripts, trimming project timelines by up to 30%.

- March 2026: SAP and Microsoft integrated SAP Business Data Cloud Connect with Microsoft Fabric to enable real-time replication of SAP data into a lakehouse architecture, targeting general availability in Q3 2026.

- February 2026: Kito Crosby completed a 14-month SAP S/4HANA rollout across 22 countries, consolidating 18 legacy systems to standardize global inventory visibility.

- January 2026: Deloitte unveiled INTEGRATE for SAP Cloud ERP, embedding machine learning models trained on more than 500 prior implementations to automate data migration and testing.

Global ERP Implementation Services Market Report Scope

The ERP Implementation Services market comprises the ecosystem of professional and managed services focused on planning, deployment, integration, customization, and optimization of Enterprise Resource Planning (ERP) systems across organizations.

The ERP Implementation Services Market Report is Segmented by Deployment Model (On-Premises, Cloud, Hybrid), Organization Size (Small and Medium Enterprises, Large Enterprises), End-Use Industry (Manufacturing, Retail and E-Commerce, Banking Financial Services and Insurance, Healthcare, Government and Public Sector, IT and Telecom, Other End-Use Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| On-Premises |

| Cloud |

| Hybrid |

| Small and Medium Enterprises |

| Large Enterprises |

| Manufacturing |

| Retail and E-Commerce |

| Banking, Financial Services and Insurance |

| Healthcare |

| Government and Public Sector |

| IT and Telecom |

| Other End-Use Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Deployment Model | On-Premises | |

| Cloud | ||

| Hybrid | ||

| By Organization Size | Small and Medium Enterprises | |

| Large Enterprises | ||

| By End-Use Industry | Manufacturing | |

| Retail and E-Commerce | ||

| Banking, Financial Services and Insurance | ||

| Healthcare | ||

| Government and Public Sector | ||

| IT and Telecom | ||

| Other End-Use Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of ERP implementation services worldwide by 2031?

The market is forecast to reach USD 44.09 billion by 2031, expanding at a 7.27% CAGR from 2026 to 2031.

Which deployment approach is growing fastest in ERP projects?

Hybrid architectures are advancing at a 17.8% CAGR because they meet data-sovereignty rules while unlocking cloud analytics.

Why are small and medium enterprises adopting ERP faster than before?

Modular subscriptions priced on a per-user basis have cut upfront fees and trimmed implementation time from months to weeks.

Which vertical is expected to record the highest ERP growth through 2031?

Healthcare is set to grow at a 15% CAGR as hospitals unify patient admissions, revenue cycle, and supply management systems to meet interoperability mandates.

What is the biggest restraint facing ERP rollouts today?

High total cost of ownership for brownfield migrations, driven by extensive custom code and data-cleansing demands, can inflate budgets by up to 60%.

How are leading integrators shortening project timelines?

Firms such as Deloitte are embedding agentic-AI platforms that auto-generate configuration, migration, and testing assets, cutting delivery schedules by roughly 30%.

Page last updated on: