Enterprise Monitoring Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 14.30 Billion |

| Market Size (2030) | USD 24.40 Billion |

| Growth Rate (2025 - 2030) | 11.28% CAGR |

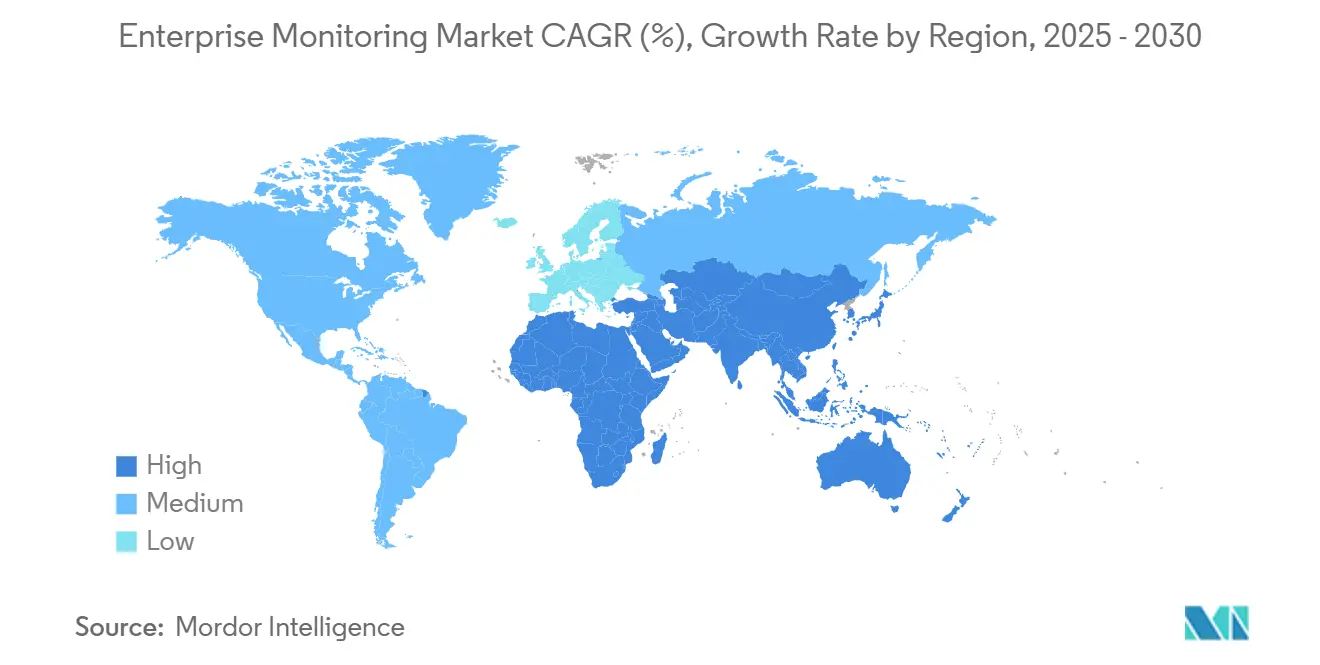

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Monitoring Market Analysis by Mordor Intelligence

The enterprise monitoring market stands at USD 14.3 billion in 2025 and is forecast to reach USD 24.4 billion by 2030, expanding at an 11.28% CAGR over 2025-2030. This growth path reflects how cloud-native architectures, hybrid and multi-cloud strategies, and AI-driven analytics are reshaping observability requirements across industries worldwide. Heightened complexity in distributed systems fuels spending on platforms that unify application, infrastructure, and security telemetry, while regulatory mandates turn always-on monitoring into a board-level priority. Cost optimization pressures favor open-source tooling and consumption-based pricing, yet advanced AIOps capabilities propel premium platform demand. Competitive intensity rises as hyperscalers bundle observability with core cloud services, even as enterprises pursue multi-vendor strategies to escape lock-in and control data-ingestion costs.

Key Report Takeaways

- By offering, software accounted for a 69.22% enterprise monitoring market share in 2024, whereas services are projected to expand at a 12.22% CAGR through 2030.

- By deployment mode, cloud deployment models captured 55.42% of the enterprise monitoring market size in 2024; however, hybrid deployments are expected to lead growth at a 13.14% CAGR through 2030.

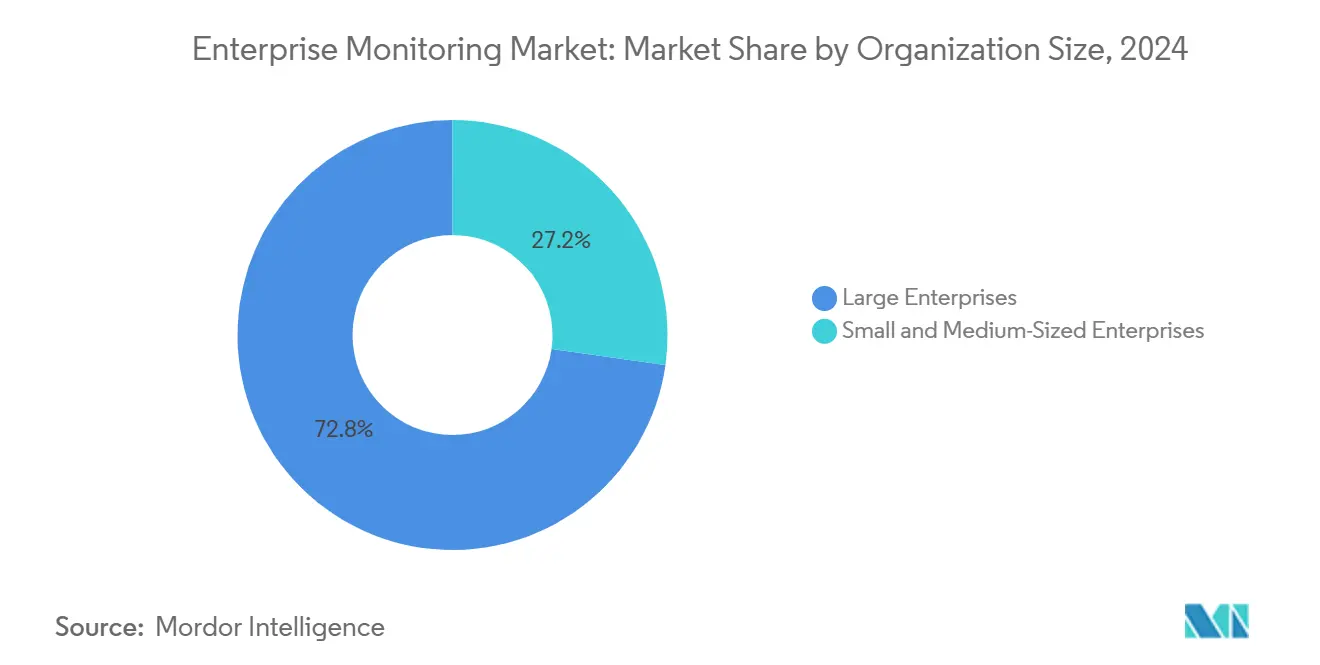

- By organization size, large enterprises held 72.77% of the enterprise monitoring market share in 2024; however, small and medium enterprises are expected to expand at a 14.44% CAGR by 2030.

- By monitoring type, application performance monitoring led with a 31.14% enterprise monitoring market share in 2024, while digital experience monitoring is expected to advance at a 12.52% CAGR through 2030.

- By end-user industry, the IT and telecom sector retained a 25.44% share of the enterprise monitoring market in 2024, whereas the healthcare and life sciences sector is poised for 13.58% CAGR growth. and at a 14.44% CAGR to 2030.

- By geography, North America commanded a 42.22% share of the enterprise monitoring market in 2024; however, the Asia Pacific is forecast to progress at a 13.25% CAGR over the same horizon.

Global Enterprise Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating cloud-native adoption in digital enterprises | +2.1% | Global, with concentration in North America and Asia Pacific | Medium term (2-4 years) |

| Expansion of hybrid and multi-cloud architectures | +1.8% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Growing compliance mandates for observability data retention | +1.4% | Europe and North America, expanding to Asia Pacific | Short term (≤ 2 years) |

| Surge in AI-powered root-cause analysis and AIOps | +2.3% | Global, led by North America | Medium term (2-4 years) |

| Proliferation of edge workloads requiring unified visibility | +1.6% | Global, early adoption in Asia Pacific and North America | Long term (≥ 4 years) |

| Rising demand for full-stack monitoring in DevSecOps pipelines | +1.9% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating Cloud-Native Adoption in Digital Enterprises

Enterprises shifting from monoliths to microservices deploy container orchestration at scale, tripling monitoring complexity and amplifying telemetry volume growth. Modern observability suites that ingest distributed traces across service meshes replace agent-centric tools no longer fit for ephemeral workloads. Vendors incorporate advanced data-compression and sampling to manage ballooning ingestion bills without sacrificing anomaly detection fidelity. The architectural pivot anchors long-term demand for platforms that embed Kubernetes-aware analytics, auto-instrument new services, and surface golden-signal metrics in real time.

Expansion of Hybrid and Multi-Cloud Architectures

Organizations blending on-premises assets with workloads across AWS, Azure, and Google Cloud wrestle with siloed dashboards that obscure end-to-end performance baselines. OpenTelemetry and vendor-agnostic correlation engines emerge as de facto standards, empowering IT teams to evaluate latency, cost, and resiliency trade-offs in one pane of glass. Multi-cloud governance concerns elevate unified observability from operational convenience to strategic necessity, stimulating adoption of platforms capable of ingesting hyperscaler metrics alongside legacy infrastructure counters.

Growing Compliance Mandates for Observability Data Retention

Regulations such as GDPR Article 32, SOX Section 404, and HIPAA security rules explicitly require continuous monitoring and auditable event archives.[1]European Commission, “EU Data Protection Rules,” ec.europa.eu Enterprises accordingly extend data-retention windows beyond operational norms, driving demand for tiered storage, tamper-evident logs, and automated compliance reporting. Observability vendors differentiate through built-in encryption, fine-grained access controls, and policy-based deletion workflows that satisfy data-protection authorities while containing archival costs.

Surge in AI-Powered Root-Cause Analysis and AIOps

Machine-learning engines now correlate symptoms across logs, metrics, and traces to isolate failure patterns, compressing mean time to resolution by up to 60% in production environments. Predictive incident forecasting shifts monitoring from reactive alert storms to proactive remediation workflows. However, algorithm efficacy hinges on historical data breadth, prompting enterprises to prioritize platforms with large pretrained incident libraries and transparent model-explainability features that satisfy risk-management committees.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of data ingestion and storage at scale | -1.7% | Global, impacting SMEs | Short term (≤ 2 years) |

| Talent shortage in observability and SRE skill sets | -1.2% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Vendor lock-in concerns in proprietary monitoring platforms | -0.9% | Global, particularly regulated industries | Long term (≥ 4 years) |

| Data-sovereignty limitations in regulated industries | -0.8% | Europe, Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Data Ingestion and Storage at Scale

Telemetry pipelines can consume 15-25% of total cloud-infrastructure budgets as terabytes of data flow daily from real-time analytics, IoT, and high-frequency trading workloads.. Flat-rate or host-based licensing fails to map neatly onto bursty, microservices traffic, compelling enterprises to adopt intelligent sampling and tiered retention. Yet aggressive cost controls risk discarding low-frequency anomalies that foreshadow critical outages, creating a perpetual balancing act between fiscal discipline and reliability engineering.

Talent Shortage in Observability and SRE Skill Sets

Site Reliability Engineering vacancies remain unfilled for 4.2 months on average, while compensation premiums surpass 40% of traditional IT-operations salaries. Smaller organizations without marquee brand appeal struggle to recruit or retain specialists versed in distributed tracing, log analytics, and chaos engineering. In response, many businesses pivot to managed observability services or SaaS platforms with opinionated best-practice workflows, even if such solutions sacrifice in-house customization flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Accelerate Despite Software Dominance

Services contributed 30.78% of 2024 revenue yet are projected to expand at a 12.22% CAGR as enterprises seek external expertise for complex migrations. Advisory partners gain traction by coupling architecture assessments with hands-on implementation, especially for AIOps rollouts that demand data-science proficiency beyond core IT operations.

Managed-service providers increasingly bundle monitoring, incident response, and compliance reporting, enabling mid-market buyers to access enterprise-grade capabilities without large capital outlays. Software licensing retains a dominant 69.22% share but its growth decelerates as subscription models saturate early-adopter verticals and price competition intensifies.

By Deployment Mode: Hybrid Models Bridge Cloud-Premises Gap

Hybrid environments represent the fastest expanding slice at 13.14% CAGR as organizations reconcile data-residency mandates with cloud elasticity advantages. Sensitive workloads remain on-premises, while real-time analytics and machine-learning inference migrate to hyperscalers, necessitating instrumentation that spans private and public domains.

Cloud deployment still owns 55.42% of 2024 spend, bolstered by continuous platform upgrades and instant global reach. Yet the enterprise monitoring market sees a steady pivot toward architectures that keep ingestion pipelines and proprietary logs under direct governance while offloading compute-intensive inference to cloud-native engines.

By Monitoring Type: Digital Experience Monitoring Gains Prominence

Digital Experience Monitoring is forecast to grow at 12.52% CAGR as line-of-business leaders equate page responsiveness and transaction latency with revenue conversion. Synthetic tests and real-user monitoring allow retailers and banks to benchmark customer journeys against service-level objectives, triggering investment in tools that surface demographic-specific performance deviations.

Application Performance Monitoring maintains a commanding 31.14% share through its deep code-level diagnostics but approaches maturity in North America. Infrastructure and network monitoring evolve toward telemetry convergence, integrating with application-layer traces to provide unified root-cause visibility across the technology stack.

By Organization Size: SMEs Embrace Cloud-Native Solutions

Small and medium enterprises record a 14.44% CAGR as SaaS observability lowers barriers to entry and consumption-based pricing aligns with constrained budgets. Turnkey dashboards, auto-instrumentation, and vendor-managed updates allow limited-headcount shops to achieve parity with large-enterprise monitoring maturity.

Large enterprises still command 72.77% of the enterprise monitoring market size due to their expansive infrastructure footprints and stringent governance needs. They increasingly pursue platform consolidation to reduce operational silos, optimize licensing spend, and standardize incident-response workflows across business units.

By End-User Industry: Healthcare Compliance Drives Accelerated Adoption

Healthcare and Life Sciences exhibit 13.58% CAGR momentum as electronic health-record mandates and patient-privacy rules require immutable audit trails and anomaly detection for protected data access. Built-in compliance templates for HIPAA, HITRUST, and regional equivalents differentiate vendors in competitive bids.

IT and Telecom sustains 25.44% share through early adoption and scale, yet its growth stabilizes while heavily regulated verticals like banking, financial services, and insurance intensify spending to meet stress-testing and fraud-monitoring obligations. Manufacturing also gains share as Industry 4.0 initiatives bring operational technology assets online, demanding real-time visibility into factory-floor performance.

Geography Analysis

Asia Pacific is on track for a 13.25% CAGR, propelled by greenfield digital infrastructure builds and cloud adoption among enterprises in India, Indonesia, and Vietnam. Government-backed digital-economy programs and 5G rollouts accelerate the need for end-to-end observability across edge, core, and cloud assets. Asia Pacific’s growth outpaces all other regions as enterprises leapfrog legacy constraints and build cloud-native stacks from day one. State-sponsored stimulus for data-center expansion and fiber connectivity creates a fertile environment for observability tooling adoption. Chinese technology giants promote domestic monitoring platforms that align with national cybersecurity policies, whereas India’s IT-services exports push local integrators to adopt leading global solutions for multi-client environments.

North America maintains a 42.22% share due to concentrated vendor ecosystems and advanced DevSecOps maturity. Yet growth decelerates as early-stage adoption gives way to optimization, consolidation, and cost-management priorities. Europe splits the difference, focusing on GDPR-compliant hybrid deployments and sovereign-cloud strategies to safeguard personal data. North America’s leadership rests on long-standing enterprise adoption, a robust ecosystem of observability vendors, and compliance frameworks such as SOX and HIPAA that embed monitoring deep inside corporate controls systems.[2]Board of Governors, “Financial Stability Report,” Federal Reserve, federalreserve.gov Financial-services firms refine incident-response automation to satisfy real-time operational-resilience directives, while healthcare providers invest in zero-trust architectures that elevate continuous telemetry acquisition to mission-critical status.

Europe’s trajectory hinges on sophisticated data-protection laws that necessitate granular audit logs and strict retention schedules. Sovereign-cloud initiatives in France and Germany support hybrid deployment preferences, enabling sensitive telemetry to reside within national borders while leveraging public-cloud analytics to drive incident predictability. Nordic public-sector digitization projects showcase best-in-class transparent monitoring, setting performance benchmarks for broader European markets.

Competitive Landscape

The enterprise monitoring market remains moderately fragmented despite headline acquisitions, yielding a healthy pipeline of innovation. Cisco’s USD 28 billion purchase of Splunk in March 2024 underscores consolidation trends aimed at fusing network analytics with observability to deliver end-to-end telemetry.[3]U.S. Securities and Exchange Commission, “Cisco Systems Inc. Form 8-K,” sec.gov Hyperscalers respond by embedding native metrics, logs, and traces deeper into their clouds while preserving open-source compatibility to court multi-cloud clients.

Traditional APM specialists such as New Relic diversify into infrastructure and edge monitoring, whereas Datadog augments its portfolio with AI-driven root-cause analytics that shorten incident lifecycles. Vendors courting regulated industries emphasize compliance automation, granular encryption, and regional data residency options to differentiate amid parity in basic collection capabilities. Start-ups target niche pain points like cost-efficient data-pipeline optimization, maintaining competitive pressure on incumbents to simplify licensing and improve ingestion economics.

Partnerships proliferate as platform ecosystems mature. Observability vendors integrate with ITSM suites such as ServiceNow to orchestrate workflow automation, while security-analytics collaborations with endpoint-protection leaders create unified dashboards spanning performance and threat telemetry. Open-source projects including Prometheus and Grafana continue to anchor cost-sensitive deployments, compelling proprietary vendors to justify premium pricing through AI-assisted insights, turnkey compliance packs, and enterprise-grade support SLAs.

Enterprise Monitoring Industry Leaders

Splunk Inc.

Datadog Inc.

New Relic Inc.

IBM Corporation

SolarWinds Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Datadog announced its Q3 2025 revenue reached USD 690 million, representing 26% year-over-year growth, driven primarily by AI-powered observability features and expanded enterprise customer adoption across hybrid cloud environments. The company's customer base exceeding USD 100,000 in annual recurring revenue grew 18% quarter-over-quarter, indicating strong enterprise market penetration and platform consolidation trends.

- September 2025: Microsoft integrated Azure Monitor with OpenAI's GPT-4 to launch conversational observability capabilities, enabling operations teams to query monitoring data using natural language and receive automated root cause analysis recommendations. This represents the first major implementation of generative AI in enterprise monitoring platforms, potentially reducing mean time to resolution by 40% according to beta customer feedback.

- August 2025: Splunk completed its integration with Cisco's networking portfolio following the 2024 acquisition, launching unified network and application observability solutions that provide end-to-end visibility across IT infrastructure and security operations. The integrated platform addresses the growing demand for converged IT and network operations, targeting enterprises with complex hybrid cloud architectures.

- July 2025: New Relic secured a USD 150 million strategic investment from Bain Capital to accelerate its AI-powered observability platform development and expand into edge computing monitoring capabilities.

Global Enterprise Monitoring Market Report Scope

| Software |

| Services |

| On-Premises |

| Cloud |

| Hybrid |

| Application Performance Monitoring |

| Infrastructure Monitoring |

| Network Monitoring |

| Log and Event Monitoring |

| Cloud Monitoring |

| Digital Experience Monitoring |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| IT and Telecom |

| Banking, Financial Services and Insurance |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Manufacturing |

| Government and Public Sector |

| Other End-User Industry |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Offering | Software | |

| Services | ||

| By Deployment Mode | On-Premises | |

| Cloud | ||

| Hybrid | ||

| By Monitoring Type | Application Performance Monitoring | |

| Infrastructure Monitoring | ||

| Network Monitoring | ||

| Log and Event Monitoring | ||

| Cloud Monitoring | ||

| Digital Experience Monitoring | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By End-User Industry | IT and Telecom | |

| Banking, Financial Services and Insurance | ||

| Healthcare and Life Sciences | ||

| Retail and E-Commerce | ||

| Manufacturing | ||

| Government and Public Sector | ||

| Other End-User Industry | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the enterprise monitoring market?

The enterprise monitoring market is valued at USD 14.3 billion in 2025.

How fast is spending on observability platforms growing?

Market revenue is projected to rise at an 11.28% CAGR between 2025 and 2030.

Which deployment model is expanding the quickest?

Hybrid architectures are forecast to increase at a 13.14% CAGR as firms balance cloud scalability with data-residency control.

Why is Digital Experience Monitoring gaining traction?

Organizations link end-user responsiveness directly to revenue, pushing Digital Experience Monitoring toward a 12.52% CAGR through 2030.

Which region shows the strongest growth outlook?

Asia Pacific leads with a 13.25% CAGR driven by greenfield cloud projects and supportive digital-economy policies.

How is market consolidation shaping competition?

High-value acquisitions such as Cisco-Splunk signal a shift toward integrated networking and observability suites, although fragmentation persists among specialized newcomers.

Page last updated on: