User Activity Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

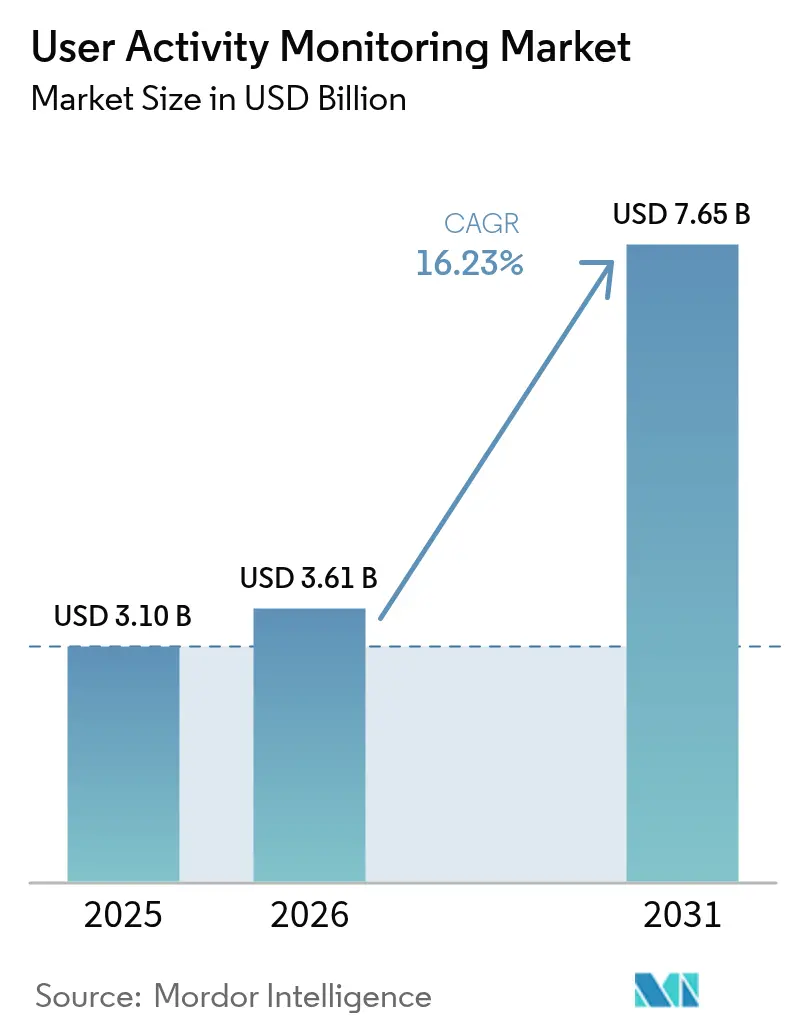

| Market Size (2026) | USD 3.61 Billion |

| Market Size (2031) | USD 7.65 Billion |

| Growth Rate (2026 - 2031) | 16.23% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

User Activity Monitoring Market Analysis by Mordor Intelligence

User activity monitoring market size in 2026 is estimated at USD 3.61 billion, growing from 2025 value of USD 3.1 billion with 2031 projections showing USD 7.65 billion, growing at 16.23% CAGR over 2026-2031. The growth path signals a clear pivot from perimeter-centric protections toward continuous verification, as zero-trust programs encourage real-time inspection of every privileged action across hybrid environments. Rapid cloud migration, rising cyber-insurance prerequisites, and the convergence of operational technology with traditional IT networks combine to expand addressable demand for the user activity monitoring market, particularly among sectors facing tight audit deadlines. Meanwhile, vendors differentiate through integrated analytics, regulatory-specific reporting, and open APIs that let enterprises embed monitoring feeds into broader observability pipelines. This shift favors solutions that scale elastically, enrich alert context automatically, and respect regional privacy constraints without sacrificing detection depth.

Key Report Takeaways

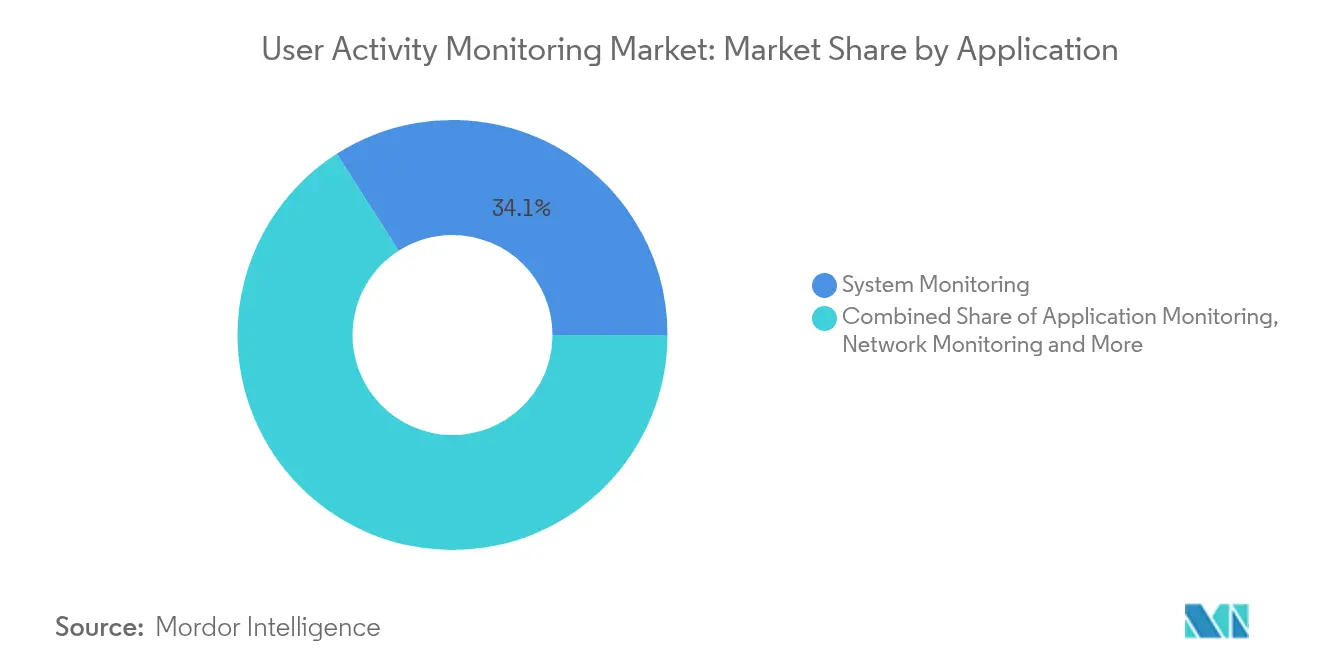

- By application, system monitoring led with 34.05% of the user activity monitoring market share in 2025, while database monitoring is on track to grow at 18.05% CAGR through 2031.

- By deployment model, on-premise retained 50.75% share of the user activity monitoring market size in 2025, yet cloud deployment is projected to expand at 23.18% CAGR to 2031.

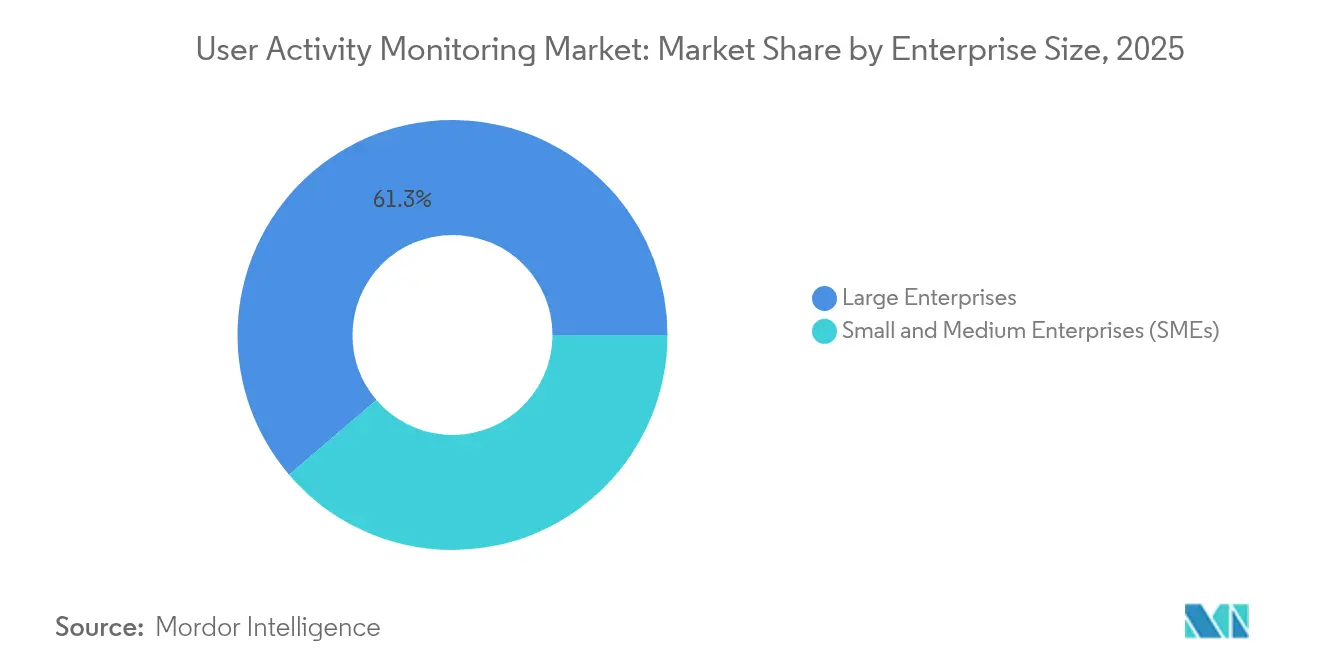

- By enterprise size, large enterprises accounted for 61.25% of the user activity monitoring market share in 2025; small and medium enterprises are advancing at 19.65% CAGR through 2031.

- By end-user industry, the BFSI segment held 29.15% of the user activity monitoring market size in 2025, whereas healthcare is forecast to grow at 19.12% CAGR through 2031.

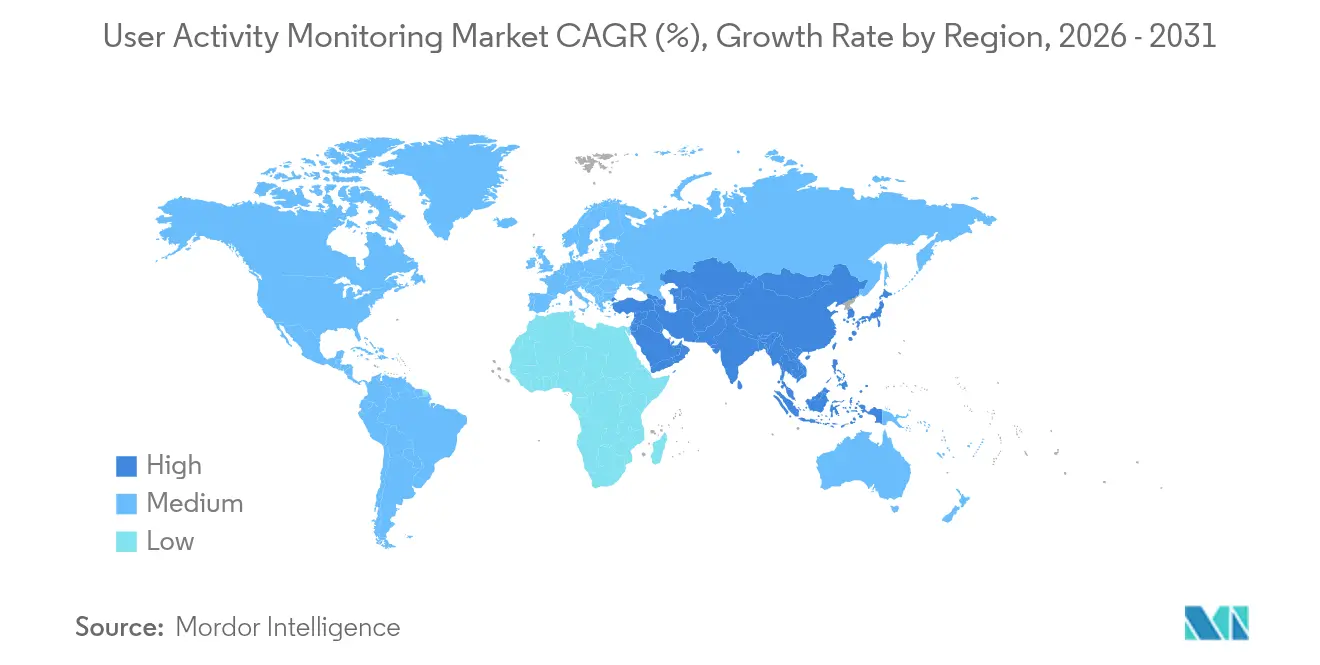

- By geography, North America commanded 44.15% revenue share in 2025, while the Asia-Pacific region is expected to post 17.74% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global User Activity Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Remote & hybrid-workforce expansion | +3.2% | Global; strongest in North America and Europe | Medium term (2-4 years) |

| Rising insider-threat & compliance mandates | +4.1% | Global; BFSI and healthcare sectors lead | Short term (≤ 2 years) |

| Shift to zero-trust security architectures | +3.8% | North America and EU lead; APAC follows | Medium term (2-4 years) |

| Need for unified observability stacks | +2.9% | Enterprise deployments worldwide | Long term (≥ 4 years) |

| Cyber-insurance driven real-time risk scoring | +2.1% | Primarily North America and Europe | Short term (≤ 2 years) |

| AI-native productivity analytics monetization | +1.4% | Technology sector globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Remote & Hybrid-Workforce Expansion

Government and private employers now support permanent distributed staffing models, prompting visibility gaps that traditional perimeter tools cannot fill. The United States Department of Defense allocated USD 469.8 million in FY 2025 to Continuous Diagnostics and Mitigation programs that watch activity across home offices and classified facilities alike. Similar patterns in banking force institutions to adopt cloud-native user activity monitoring platforms able to baseline behavior regardless of location. Vendors respond with lightweight agents that adjust thresholds dynamically as employees transition between networks, coworking spaces, and unmanaged devices. The associated productivity gains create board-level support for investments that separate legitimate remote work from credential misuse in real time.

Rising Insider-Threat & Compliance Mandates

Financial regulators, including SIFMA, revised best-practice guides in 2024 to require granular tracking of privileged user behavior for audit defense. Banking loss analyses attribute significant portions of fraud to insiders, accelerating interest in AI-driven anomaly detection that highlights subtle deviations such as off-hour data pulls. Manufacturing sees similar urgency as 52% of malware incidents feature ransomware that often begins with compromised internal accounts. Compliance teams therefore demand detailed audit trails able to reconstruct every keystroke during investigations, pushing organizations to treat user activity monitoring as an operating cost akin to firewalls rather than a discretionary tool.

Shift to Zero-Trust Security Architectures

Executive Order 14028 obliges United States federal agencies to implement zero-trust by 2027, embedding user behavior analytics into real-time policy decisions. Benchmarks show combined single sign-on and zero-trust designs authenticate in 30.03 milliseconds while flagging double-digit anomalies within hours, demonstrating that effective controls need seamless analytics rather than scheduled audits. Japanese enterprises echo this direction as 77.7% adopt cloud services yet struggle to watch automated service identities, elevating demand for platforms that link identity management with continuous context evaluation. Vendors that ship open API hooks for identity platforms and endpoint telemetry gain advantage because they let security teams orchestrate deny-or-step-up actions instantly.

Need for Unified Observability Stacks

Splunk’s FY 2024 Cloud ARR rose 23% to USD 2.186 billion as customers sought a single console for performance and security analytics. Operators want direct correlation between a failed database write, a spike in CPU, and the user who triggered both within milliseconds, rather than toggling among siloed dashboards. Cisco’s USD 28 billion offer for Splunk illustrates demand for convergence of SIEM, application performance management, and user activity monitoring market capabilities. This alignment aids compliance as auditors increasingly request proof that companies supervise the full stack, not isolated layers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Employee privacy & works-council pushback | -2.8% | Europe, with spillover across multinationals | Short term (≤ 2 years) |

| High TCO for multi-modal data capture | -1.9% | Worldwide; SME budgets most affected | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Employee Privacy & Works-Council Pushback

The EU AI Act categorizes many monitoring solutions as high-risk, obliging firms to conduct impact assessments, preserve human oversight, and pay fines up to EUR 35 million for violations.[1]European Commission, “Cloud Computing – Statistics on the Use by Enterprises,” Eurostat, ec.europa.eu Works councils commonly challenge deployments that log granular keystrokes without worker consultation, forcing enterprises to deploy privacy-by-design models that anonymize data until investigation triggers occur. Multinationals then standardize on the strictest jurisdiction to avoid policy fragmentation, occasionally reducing analytic depth in regions that actually permit deeper inspection. Vendors invest in differential privacy, local-storage architectures, and role-based masking to maintain European viability while keeping detection true-positive rates acceptable elsewhere.

High TCO for Multi-Modal Data Capture

Comprehensive visibility calls for endpoint, network, file, and database telemetry streamed in real time, driving compute, storage, and license costs that can deter smaller organizations.[2]Organisation for Economic Co-operation and Development, “SME Digitalisation in 2024: Managing Shocks and Transitions,” OECD, oecd.org Semiconductor supply chain strain may escalate hardware expenses as global wafer fabrication outlays reach USD 2.3 trillion between 2024 and 2032. Although cloud models shift investment from capital to operating budgets, data-sovereignty rules can mandate local retention, pushing enterprises toward hybrid builds that replicate ingestion pipelines both on-premise and in the public cloud. SMEs therefore prioritize modular packages that let them begin with high-value assets such as databases, expanding toward full stack coverage when budgets permit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Database Monitoring Drives Innovation

Database monitoring holds the fastest 18.05% CAGR through 2031 even as system monitoring commanded 34.05% of the user activity monitoring market share in 2025. The user activity monitoring market size attached to database oversight is forecast to expand rapidly because structured records hold regulated customer and financial data that present high breach penalties. Vendors embed query profiling and privilege escalation alerts to meet auditors’ expectations for precise chain-of-custody evidence. Complementary modalities-file, network, and application monitoring-continue to mature, but buyers increasingly insist on a unified console capable of tracing a transaction from initial request to final write.

Organizations therefore adopt platforms that stitch user identities, process IDs, and SQL statements into a single timeline, reducing meantime-to-incident-resolution and improving report generation for standards such as PCI DSS and Basel III. System monitoring maintains relevance by covering every endpoint, including unmanaged personal devices now admitted under bring-your-own-device policies. Application monitoring gains traction within DevSecOps pipelines, enabling development teams to shift left by detecting risky behavior during staging rather than after production release.

By Deployment Mode: Cloud Acceleration Reshapes Architecture

Cloud delivery exhibits a 23.18% CAGR as enterprises move telemetry workloads off-premise in tandem with broader software modernization. On-premise still accounted for 50.75% of the user activity monitoring market size in 2025 because legacy industries and governments often retain sensitive workloads behind strict firewalls. Adoption rates accelerate in Europe, where 45.2% of businesses purchased cloud services in 2023. Hybrid models emerge as the default: sensitive log data is written locally to comply with sovereignty rules, while lower-risk streams enter regional cloud zones for elastic processing.

This split architecture urges vendors to design agent-based collection that forwards data selectively based on tagging rules. Innovations such as edge-native preprocessing compress payloads before they reach collectors, lowering egress fees and latency. As network bandwidth costs decline and hyperscalers introduce privacy vaults, more customers migrate cold storage to object repositories while keeping hot analytic clusters close to real-time data sources.

By Enterprise Size: SME Adoption Accelerates

Large enterprises held 61.25% revenue in 2025, yet SMEs are growing at 19.65% CAGR, shifting the buyer demographic of the user activity monitoring market. Affordability improved through subscription models that start below three-digit USD monthly tiers, removing upfront license fees that once barred smaller firms. Cyber-insurance carriers now expect log retention and privileged access monitoring as minimum requirements for coverage, compelling even micro businesses to adopt baseline telemetry.

Enterprise buyers continue to spend most in absolute terms, demanding native integration with security orchestration platforms, asset management databases, and data lakes. Advanced features such as container-aware tracing and remote session video recording remain optional for SMEs but default for multinational corporations that manage thousands of privileged contractors. Observed convergence between compliance and operations suggests future packages will bundle governance dashboards accessible to finance and legal teams without separate tooling.

By End-User Industry: Healthcare Leads Growth

BFSI remained the largest vertical at 29.15% revenue in 2025, supported by extensive regulatory frameworks like the New York DFS Part 500 rule set. Healthcare, however, is forecast to post 19.12% CAGR after proposed HIPAA Security Rule updates in January 2025 require multi-factor authentication and expanded audit controls. Providers adopt agentless discovery that captures ePHI access across electronic medical record systems, medical IoT devices, and third-party billing portals.

Manufacturing faces a distinct threat profile dominated by ransomware groups targeting operational technology. Energy utilities invest heavily in grid modernization security programs, integrating user activity telemetry from SCADA consoles and field laptops to satisfy Department of Energy implementation plans. Government agencies comply with 10 USC 2224 mandates for automated insider detection across cleared networks, further evidencing that sector-specific rules remain chief budget drivers.

Geography Analysis

North America generated 44.15% of 2025 revenue, benefiting from early zero-trust mandates, strong cyber-insurance penetration, and prolific state-level legislation that now requires continuous monitoring within public sector contracts. Federal departments align to Executive Order 14144, and the Energy Modernization Cybersecurity Implementation Plan outlines 32 initiatives that fund telemetry sensors across substations and cloud edge nodes. Vendor ecosystems cluster around Washington, D.C., and Silicon Valley, fostering rapid feature iteration and robust customer success communities that shorten deployment timelines.

Asia-Pacific is the fastest-growing region at 17.74% CAGR through 2031. China’s Network Data Security Management Regulations, effective January 2025, compel nearly every large enterprise to implement risk assessment and user activity logs, while India’s Digital Personal Data Protection Act tightens breach-reporting windows and mandates consent tracking. Japan’s Cloud Security Alliance surveys find 46% of firms struggle to monitor non-human identities, driving interest in identity-centric solutions integrated into public-cloud ecosystems. Start-ups from Singapore and South Korea focus on multilingual natural-language search interfaces that suit heterogeneous IT deployments across the region.

Europe sustains measured adoption amid privacy complexities. The user activity monitoring market size in Germany, France, and the Nordics expands as companies negotiate works-council approvals by adopting privacy-preserving analytics. With the EU AI Act coming into force in August 2026, vendors invest early in algorithmic explainability and human-in-the-loop controls to retain access to continental buyers. Emerging economies in Latin America, the Middle East, and Africa increasingly embed monitoring clauses in data-protection directives, although budget constraints redirect preference toward SaaS platforms hosted in regional data centers.

Competitive Landscape

The user activity monitoring market remains moderately fragmented, with household names—Microsoft, IBM, Cisco, Splunk, and Broadcom—competing against specialists like CyberArk, Forcepoint, and ObserveIT. Cisco’s planned integration of Splunk indicates a strategic bet that security buyers prefer end-to-end observability over point solutions. Established vendors expand machine-learning capabilities, adding context from identity providers and configuration management databases to reduce alert fatigue.

Specialists differentiate through depth rather than breadth. CyberArk emphasizes privileged session recording and just-in-time credential issuance, securing contracts in defense and energy verticals that demand National Institute of Standards and Technology compliance. Insider-risk newcomers leverage local differential-privacy algorithms so personal identifiers stay encrypted until an alert threshold is crossed, satisfying European works councils while preserving forensics integrity.

Open-source projects, including Wazuh and Elastic Security, penetrate cost-sensitive segments, especially SMEs requiring basic file-integrity monitoring. Partnerships matter: cloud providers bundle baseline log retention within broader workload protection platforms, creating challenges for independent vendors that must justify additional spend. Overall, winning strategies hinge on interoperability with security information and event management systems, low-latency processing, and transparent pricing that scales predictably with data volume rather than static seat counts.

User Activity Monitoring Industry Leaders

Micro Focus International PLC

Splunk Inc.

Imperva Inc.

CyberArk Software Ltd.

Centrify Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Japan Cloud Security Alliance reported that 46% of enterprises struggle to watch non-human SaaS identities, spotlighting demand for automated identity telemetry

- April 2025: The U.S. Department of Justice launched the Data Security Program under PADFAA, requiring reviews of de-identified health data transfers, broadening logging scope for healthcare providers

- March 2025: China issued Facial Recognition Technology Application Safety Management Measures, effective Jun 2025, that necessitate explicit consent and stricter storage controls

- January 2025: HHS proposed HIPAA Security Rule updates imposing stronger multi-factor authentication and audit standards for ePHI systems

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the user activity monitoring (UAM) market as all software and associated services that capture, store, and analyze end-user actions across endpoints, networks, and cloud assets to detect threats, meet compliance mandates, and improve workforce productivity. According to Mordor Intelligence, the global UAM market stood at about USD 3.10 billion in 2025 and is projected to reach nearly USD 6.70 billion by 2030.

Scope exclusion: pure time-tracking tools lacking forensic logging or network visibility are outside this study.

Segmentation Overview

- By Application

- System Monitoring

- Application Monitoring

- File Monitoring

- Network Monitoring

- Database Monitoring

- Others

- By Deployment Mode

- On-premise

- Cloud

- Hybrid

- By Enterprise Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By End-user Industry

- BFSI

- Retail and E-commerce

- IT and Telecom

- Healthcare and Life Sciences

- Manufacturing

- Government and Defense

- Energy and Utilities

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Across North America, Europe, and Asia-Pacific, we interview CISOs, security integrators, and data-protection officers to validate deployment patterns, license seat ranges, and average selling prices. Short surveys of SME IT managers refine cloud-adoption curves and cost obstacles.

Desk Research

We begin with open datasets from bodies such as NIST, ENISA, and Eurostat for breach counts, privacy fines, and digital-workforce trends. We then review cyber-security directives released by the European Commission, the U.S. Office of Management and Budget, and Japan's IPA to size regulatory pull. Company 10-Ks, IPO filings, and privacy impact assessments reveal vendor revenue splits, while Questel patent searches track innovation velocity. Import-export records from Volza illuminate appliance shipments. The sources listed are illustrative; many additional references inform our evidence pool.

Market-Sizing & Forecasting

A top-down model anchors on global paid-seat inventories derived from labor statistics and hybrid-work penetration, which are then multiplied by authenticated UAM adoption rates. Supplier roll-ups and channel ASP checks supply bottom-up cross-checks before figures are finalized. Key variables include insider-threat incident rates, zero-trust program uptake, regulatory fine trends, endpoint growth, and cloud-deployment share. A multivariate regression with ARIMA smoothing projects these through 2030, and interview-approved ranges bridge any data gaps.

Data Validation & Update Cycle

Outputs face peer review, anomaly flags, and year-on-year variance tests. Reports refresh annually, with interim revisions when material events arise. A final analyst pass assures clients receive the latest view.

Why Mordor's User Activity Monitoring Baseline Inspires Confidence

Published UAM estimates often diverge because firms mix dissimilar solution scopes, adoption multipliers, and refresh cadences. We clarify these gaps so decision-makers can pick the figure that truly fits. Other public numbers range from about USD 4.0 billion for 2024 to roughly USD 3.39 billion in the same year.

Differences usually stem from whether services revenue is bundled, how aggressively cloud migration is assumed, and how quickly new privacy rules are costed in. Mordor reports the full paid-seat universe yet applies conservative utilization ramps and updates every twelve months, whereas others may extrapolate older disclosures or rely on single-region samples.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.10 B (2025) | Mordor Intelligence | - |

| USD 4.00 B (2024) | Global Consultancy A | Bundles managed services and broader monitoring tools |

| USD 3.39 B (2024) | Industry Publisher B | Uses constant 24 % CAGR and assumes universal licensing for all remote staff |

In sum, Mordor's tempered seat counts, dual-sourced ASPs, and disciplined update rhythm give clients a balanced, transparent baseline that links directly to clearly stated variables and repeatable steps.

Key Questions Answered in the Report

What is the current value of the user activity monitoring market?

The user activity monitoring market stands at USD 3.61 billion in 2026 and is set to reach USD 7.65 billion by 2031.

Which application segment is growing fastest?

Database monitoring is projected to expand at 18.05% CAGR through 2031 as enterprises focus on protecting structured data repositories.

Why are small and medium enterprises now adopting user activity monitoring?

SMEs face rising cyber-insurance requirements and can leverage affordable cloud-native platforms that remove upfront hardware costs, supporting a 19.65% CAGR in this buyer group.

How do privacy regulations in Europe affect deployment?

The EU AI Act designates many monitoring tools as high-risk, requiring strict governance, impact assessments, and privacy-preserving analytics before rollout.

What role does zero-trust architecture play in future demand?

Zero-trust programs embed behavioral analytics into access decisions, making real-time user activity monitoring a foundational layer for every privileged operation across hybrid environments.

Page last updated on: