Energy Security Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

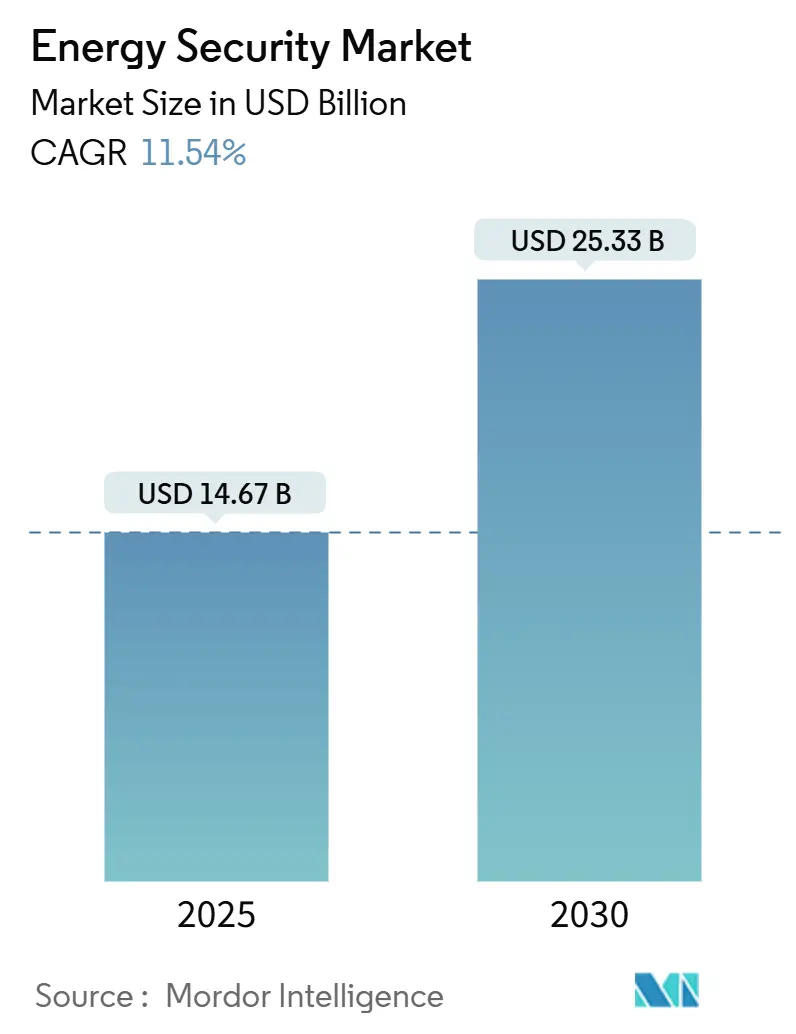

| Market Size (2025) | USD 14.67 Billion |

| Market Size (2030) | USD 25.33 Billion |

| Growth Rate (2025 - 2030) | 11.54% CAGR |

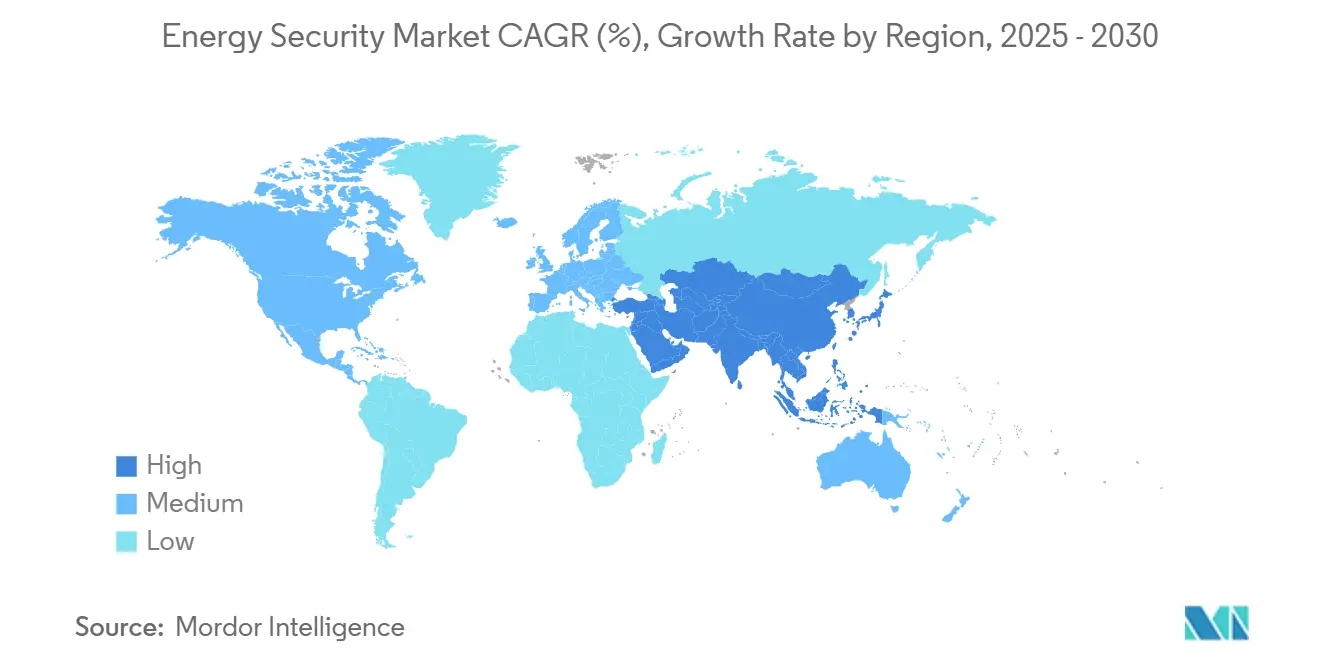

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

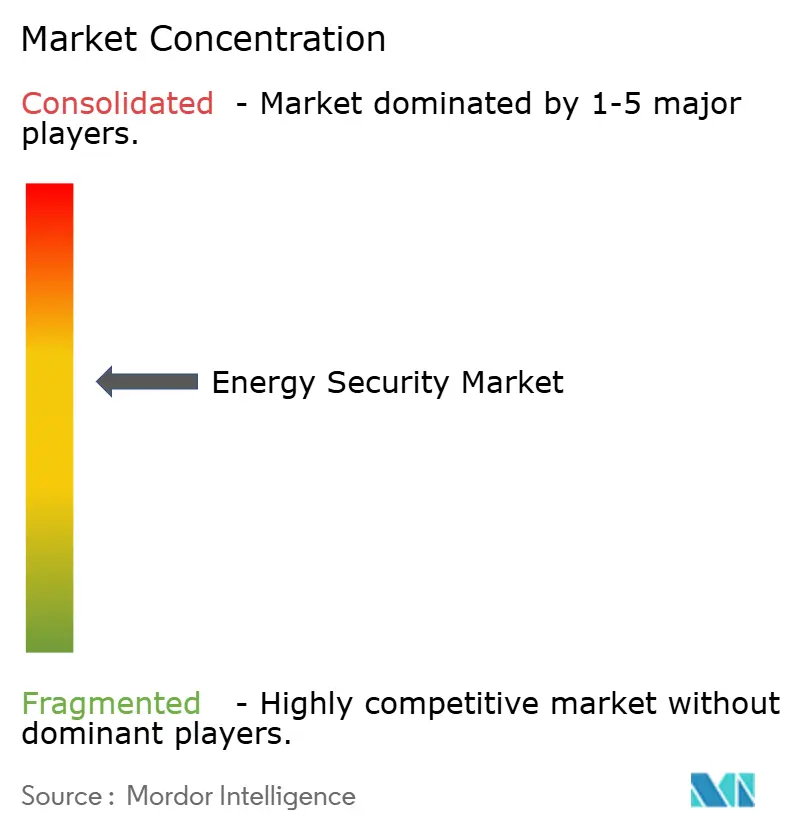

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Energy Security Market Analysis by Mordor Intelligence

The energy security market size stands at USD 14.67 billion in 2025 and is forecast to reach USD 25.33 billion by 2030, translating into an 11.54% CAGR over the period. Surging cyber-physical attacks on operational technology, rapid renewable integration, and stricter critical-infrastructure mandates are driving capital toward converged security solutions. Utilities are moving quickly to protect OT and IT assets, while post-quantum cryptography, hydrogen-hub safety, and satellite surveillance are shaping vendor road maps. Intensifying geopolitical risk keeps underwater cables, pipelines, and grid interties in regulators’ sights, prompting new investment rules even in cost-sensitive emerging markets. Established automation majors and specialist cyber vendors now compete on platform interoperability, AI-enabled analytics, and managed detection reach.

Key Report Takeaways

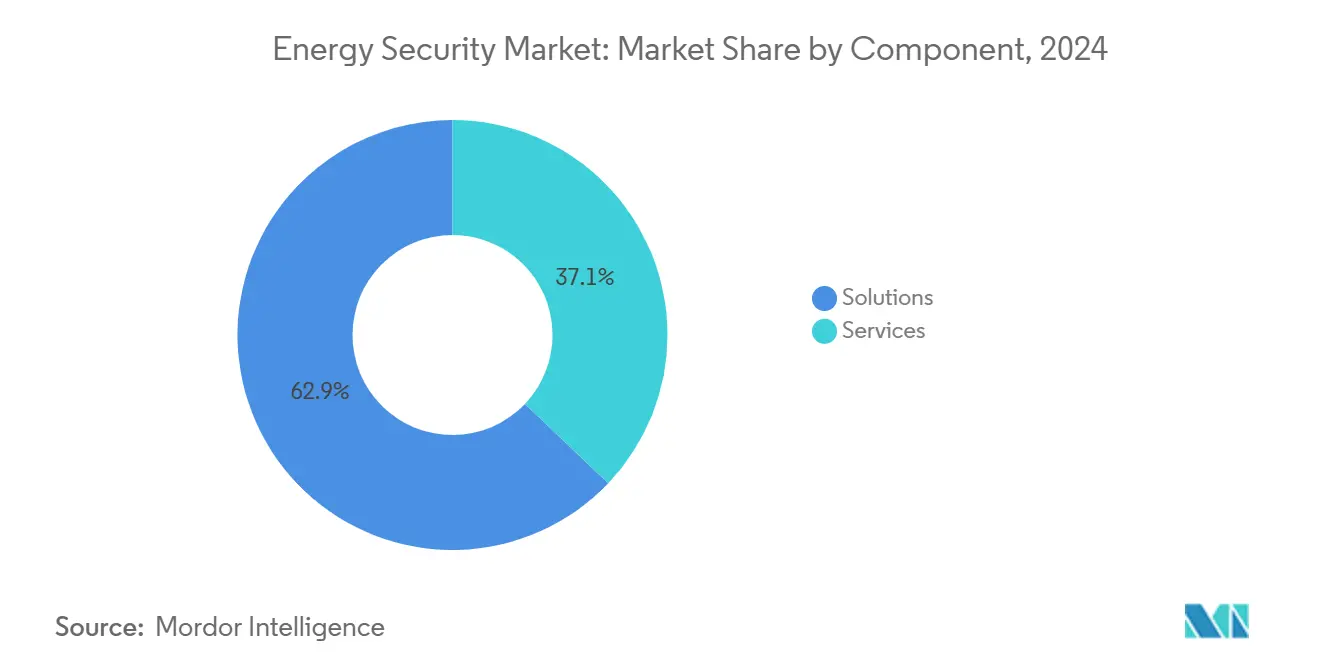

- By component, solutions led with 62.90% energy security market share in 2024, whereas services are advancing at 12.77% CAGR through 2030.

- By security type, network and application security contributed 38.50% revenue share in 2024, while cloud and edge security are projected to expand at a 12.97% CAGR to 2030.

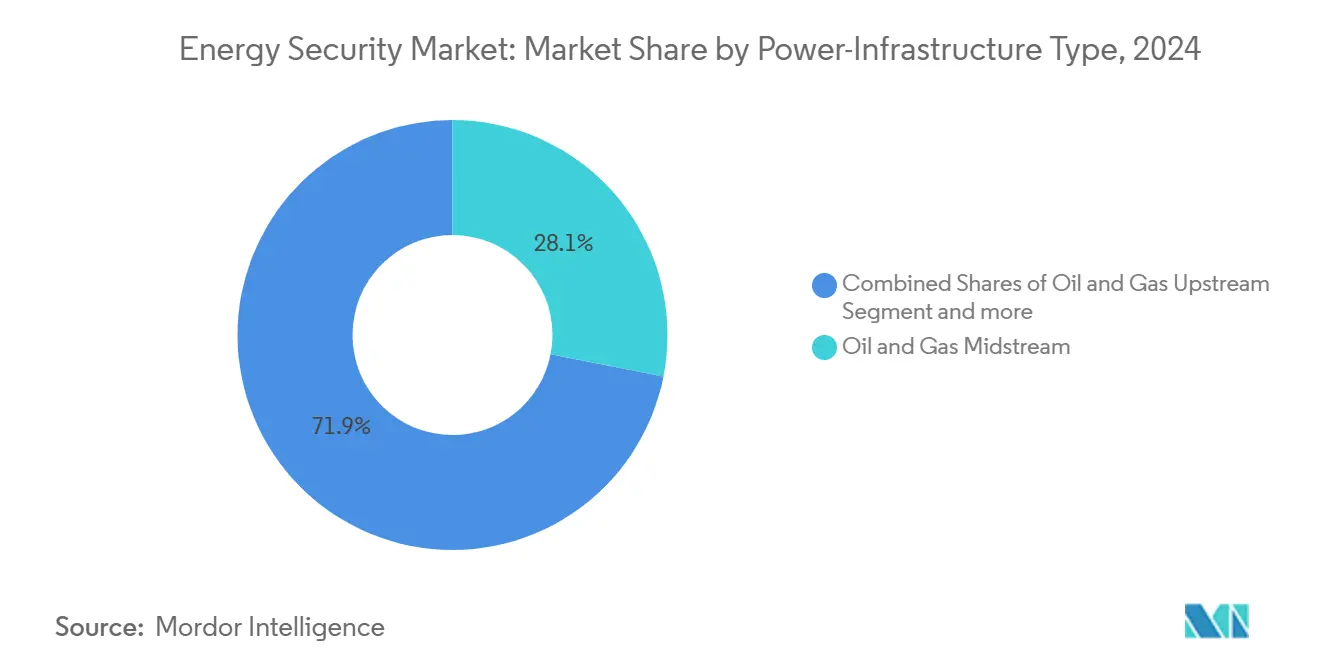

- By power infrastructure, oil and gas midstream accounted for 28.10% of the energy security market size in 2024, yet renewable power assets show the highest growth at 14.37% CAGR.

- By application, surveillance and monitoring held a 29.60% share in 2024; managed detection and response is forecast to post a 13.98% CAGR to 2030.

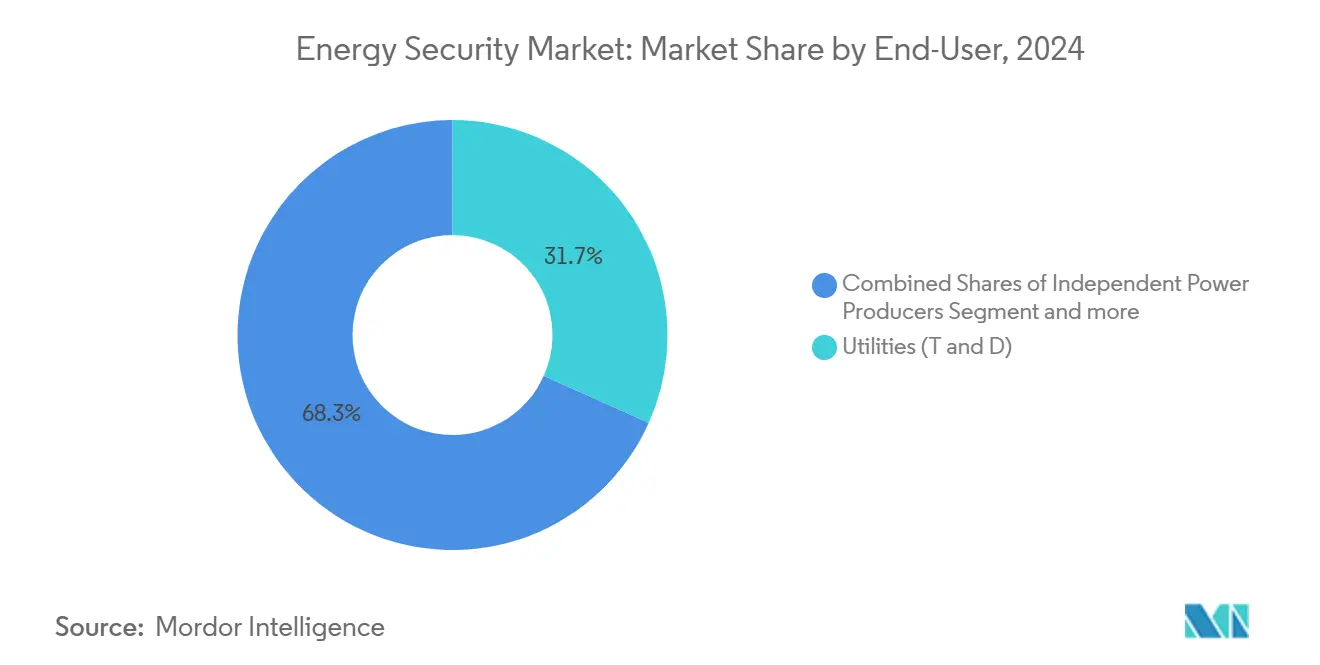

- By end-user, utilities (transmission and distribution) commanded a 31.70% share in 2024, while independent power producers represent the fastest trajectory at 13.57% CAGR.

- By geography, North America led with 38.70% revenue share in 2024; Asia-Pacific is poised for 14.76% CAGR through 2030.

Global Energy Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating cyber-attacks on critical energy OT/IT convergence | +2.90% | Global, with concentration in North America & Europe | Short term (≤ 2 years) |

| Integration of distributed renewable assets into legacy grids | +2.50% | Global, led by Asia-Pacific & Europe | Medium term (2-4 years) |

| Stricter North American Critical Infrastructure Protection (NERC-CIP) standards | +2.10% | North America, with spillover to allied nations | Medium term (2-4 years) |

| Rising geopolitical sabotage of subsea energy cables & pipelines | +1.70% | Europe, Asia-Pacific, with global implications | Short term (≤ 2 years) |

| Commercialisation of satellite-based ISR for pipeline monitoring | +1.40% | Global, early adoption in North America & Middle East | Long term (≥ 4 years) |

| Hydrogen-hub build-outs demanding new safety/security layers | +0.90% | Europe, Asia-Pacific, select North American regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Cyber-Attacks on Critical Energy OT/IT Convergence

CISA logged more than 200 energy-sector incidents in 2024, a 40% year-on-year rise, underscoring how merged OT and IT networks have erased traditional air-gaps. [1]Cybersecurity and Infrastructure Security Agency, “2024 Year in Review,” CISA, Jul 01 2024, cisa.gov Germany’s interior ministry called espionage threats a “new dimension,” reiterating rising state-sponsored interest in grid disruption. Attackers exploit legacy SCADA links to business systems, creating urgent demand for unified detection platforms that can pinpoint lateral movement without halting operations. Vendors respond with AI-driven analytics that correlate OT telemetry with IT event logs, shortening dwell time and easing compliance audits. Utilities accelerating digital-substation rollouts now budget security at project inception rather than retrofit.

Integration of Distributed Renewable Assets into Legacy Grids

Smart inverters, microgrids, and storage nodes add thousands of remote endpoints, each a possible breach vector. The FBI’s advisory on renewable-asset vulnerabilities elevated board-level scrutiny, while NARUC’s 2024 baselines require distribution utilities to harden DER connections.[2]Cybersecurity and Infrastructure Security Agency, “JCDC AI Cybersecurity Collaboration Playbook,” CISA, Dec 31 2024, cisa.gov Cloud dashboards and wireless protocols enhance flexibility yet widen the attack surface, pushing demand for edge-security gateways and PKI-based device identity. Cyber-secure inverter firmware upgrades are becoming a procurement criterion, influencing supplier ranking in utility RFPs. As renewables expand toward majority-share generation in several Asian markets, grid operators pivot to zero-trust architectures that treat every DER as an untrusted node.

Stricter North American Critical Infrastructure Protection (NERC-CIP) Standards

FERC’s CIP-015-1 extends continuous monitoring to internal networks and physical-access systems, obliging utilities to deploy IDS sensors across previously unmonitored segments.[3]Federal Energy Regulatory Commission, “Critical Infrastructure Protection Reliability Standard CIP-015-1,” Federal Register, Sep 27 2024, federalregister.gov High and medium-impact BES assets must implement anomaly detection capable of correlating cyber and badge-access events, pushing uptake of converged OT-IT SIEM platforms. The 2025 deadline has already accelerated request-for-proposal cycles, with utilities favoring solutions offering pre-configured compliance reports. New supply-chain rules mandate vendor SBOM disclosure, creating opportunities for risk-rating platforms and third-party assessment providers. North American lessons are beginning to influence allied utilities in Latin America and parts of Asia.

Rising Geopolitical Sabotage of Subsea Energy Cables & Pipelines

The Nord Stream and Baltic incidents illustrated how undersea assets can serve as geopolitical leverage. Europe’s subsea data cables, now integral to energy-trading telemetry, remain difficult to patrol, keeping threat perception high.[4]Lella Ifigeneia, “ENISA Threat Landscape 2024,” European Union Agency for Cybersecurity, Sep 17 2024, enisa.europa.eu NATO and EU projects fund sonar meshes, autonomous underwater vehicles, and rapid-repair consortia, yet coverage gaps persist. Utilities and TSOs increasingly commission redundancy studies to reroute critical data and power flows via alternate corridors. Insurers factor sabotage risk into premium models, nudging operators toward proactive surveillance subscriptions. Vendors offering joint physical-cyber risk dashboards gain traction with European utilities managing cross-border interties.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented vendor landscape delaying platform interoperability | -1.70% | Global, particularly acute in North America & Europe | Medium term (2-4 years) |

| High up-front CAPEX for converged physical-cyber solutions | -1.40% | Global, with greater impact in emerging markets | Short term (≤ 2 years) |

| Limited insurance actuarial data for energy-sector cyber-risk | -0.90% | Global, concentrated in developed insurance markets | Long term (≥ 4 years) |

| Rural talent scarcity for OT cybersecurity operations centres | -0.60% | North America, Europe, Australia rural regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Vendor Landscape Delaying Platform Interoperability

Utilities often run mixed fleets of turbines, SCADA hosts, and firewall brands, forcing bespoke middleware to stitch telemetry into a unified security view. Integration consulting can reach 40% of the total project cost, prolonging deployment timelines and raising lifecycle OPEX. The EU’s network code on cybersecurity aims to standardize APIs, yet heterogeneity persists as incumbents defend proprietary protocols[5]Directorate-General for Energy, “New Network Code on Cybersecurity for EU Electricity Sector,” European Commission, Mar 11 2024, energy.ec.europa.eu. Vendors now form alliances to publish shared data models, but momentum remains slow, especially among legacy automation suppliers. Multi-utility holding companies thus favor suppliers offering vendor-agnostic connectors and open-source SDKs.

High Up-Front CAPEX for Converged Physical-Cyber Solutions

Comprehensive deployments bundle hardened switches, cameras, AI analytics, SIEM, and SOC services, ranging from USD 5 million to USD 15 million per flagship plant[6]Walton Robert, “Utility Regulators Raise Cybersecurity Baselines,” Cybersecurity Dive, Feb 29 2024, cybersecuritydive.com. Rate-regulated utilities struggle to win commission approval when ROI is risk-mitigation rather than revenue. Rural cooperatives face even tighter balance sheets, resulting in phased rollouts or partial coverage. Financing innovations such as security-as-a-service and outcome-based contracts are emerging, yet credit-ratings agencies still discount such models, dampening penetration in emerging markets. Vendors counter by modularizing offerings and deferring license fees until assets go live.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Reinforce Defensive Foundations

Solutions captured 62.90% of the energy security market in 2024 as utilities prioritized hardening core defenses before outsourcing day-to-day monitoring. Deployments ranged from secure gateways for legacy PLCs to AI-enabled anomaly detection covering OT and IT networks. The share dominance underscores how foundational tooling precedes services uptake, especially under compliance deadlines. Services, however, are climbing at 12.77% CAGR as operators confront resource shortages and seek managed detection centers. Outsourced SOC contracts increasingly bundle patch management and threat-intel feeds, turning security from capex into opex.

Rising service demand also reflects complexity in maintaining crypto-agile architectures and continuous NERC-CIP evidence collection. Vendors offering turnkey compliance dashboards gain a competitive edge, particularly among mid-sized municipal utilities. Hybrid engagement models-on-prem sensors with cloud analytics-balance data-sovereignty concerns against scale efficiencies. Over 2026-2028, service providers are expected to win larger multiyear frameworks tied to grid-modernization grants, further shifting the spending mix.

By Security Type: Network Protection Steers the Architectural Shift

Network and application security owned 38.50% energy security market share in 2024 owing to the collapse of air-gaps and the surge in remote asset management. Deep-packet-inspection firewalls, zero-trust gateways, and OT-aware intrusion systems dominate procurement shortlists. Cloud and edge security’s 12.97% CAGR mirrors the proliferation of SaaS energy-management suites and containerized micro-services at substations. Utilities integrate cloud workload protection with hardware-root-of-trust at the edge, creating layered defense for analytics pipelines.

Evolving architectures push demand for software-defined perimeters where identity governs access rather than IP ranges. Vendors embed post-quantum algorithms into VPNs to future-proof investments against coming cryptanalytic breakthroughs. Physical security converges with cyber schemes via unified dashboards, letting SOC teams triangulate camera analytics with network alerts in real time. Such integrations reduce alert fatigue and speed incident triage.

By Power-Infrastructure Type: Midstream Dominance Meets Renewable Surge

Oil and gas midstream held 28.10% share of the energy security market size in 2024, a testament to pipeline network sprawl and the high economic stakes of flow disruptions. Proprietary SCADA links, valve actuators, and compressor stations require layered defenses spanning intrusion sensing and vibration analytics. Yet renewable power assets lead growth at 14.37% CAGR as solar, wind, and storage nodes multiply connection points. Their modular, distributed nature demands micro-segmented security and certificate-based authentication at scale.

Upstream operations wrestle with satellite backhaul latency and harsh environments that complicate patching windows. Nuclear and thermal plants maintain niche yet stringent profiles, focusing on physical fortification and regulatory audits. Vendors see opportunity in offering asset-class-specific playbooks-pipeline-grade DPI signatures, inverter anomaly models-within a common orchestration shell, easing multi-energy-portfolio oversight.

By Application: Surveillance Extends into Proactive Detection

Surveillance and monitoring contributed 29.60% of revenue in 2024, reflecting utilities’ need for holistic situational awareness across remote sites. High-resolution cameras, LiDAR, and vibration sensors now feed AI models that flag unauthorized excavations or abnormal temperature rise. Managed detection and response’s 13.98% CAGR signals pivot from passive alerting to active threat-hunting. SOCs ingest OT telemetry, badge access logs, and satellite feeds, shortening mean time to respond.

Access-control refresh cycles dovetail with badge-less, biometric solutions, enabling context-aware door policies tied to cyber-risk scores. Incident- and risk-management suites automate report generation for regulators, slashing audit prep and enabling continuous-compliance postures. Command-and-control hardening focuses on cryptographic authentication and deterministic networks resistant to jitter-vital for micro-second protection-relay actions.

By End-User: Utilities Anchor Modernization, IPPs Accelerate Adoption

Utilities (T and D) commanded 31.70% share in 2024, driven by statutory reliability obligations and regulator-approved cost recovery. Large footprint and asset criticality spur multimillion-dollar security programs embedded within grid-modernization road maps. Independent power producers, growing at 13.57% CAGR, leverage flexible financing and lean structures to adopt cloud-native security stacks quickly. Their renewable-heavy portfolios align with edge-security trends and managed SOC subscriptions.

National oil companies sustain demand through mega-pipeline and refining projects, often integrating proprietary standards that require bespoke connectors. EPC contractors and system integrators shape vendor selection, influencing architectural preferences across new-build projects. As cross-border interconnections rise, stakeholders coordinate security baselines to safeguard import–export power corridors.

Geography Analysis

North America led the energy security market with 38.70% share in 2024, underpinned by NERC-CIP mandates and federal grants channeled into grid-hardening programs. The White House Energy Modernization Cybersecurity Implementation Plan guides agency funding, ensuring alignment of utility projects with national resilience goals. Canada tightens critical-infrastructure guidelines, whereas Mexico’s CFE invests selectively in substation upgrades.

Asia-Pacific posts the fastest trajectory at 14.76% CAGR to 2030, buoyed by massive renewable rollouts, China’s smart-grid drive, and India’s DER cybersecurity manual. Japan pilots post-quantum crypto at gas utilities, while Australia guards remote mining micro-grids. Regional suppliers bundle security into turnkey EPC contracts, accelerating adoption among new-build assets.

Europe remains growth-steady, propelled by NIS2 transposition and heightened awareness after Baltic sabotage events. Germany’s KRITIS law widens operator obligations, and the EU network code sets minimum controls, though implementation pacing diverges among member states. Nordic TSOs coordinate SOC functions across borders, sharing threat intel to protect deeply interlinked grids. Southern European DSOs, facing capex pressure, lean on managed-service offerings.

Middle East and Africa see rising demand as Gulf states expand hydrogen and solar megaprojects. Saudi Arabia’s NCA enforces cyber-controls via mandatory audits, and the UAE embeds zero-trust within its smart-city power backbone. Sub-Saharan utilities modernize slowly but target high-impact nodes first, such as main transmission substations.

South America experiences moderate uptake. Brazil’s ANEEL requires cyber reporting for renewable operators intersecting critical load centers, while Argentina and Colombia channel multilateral loans into OT segmentation pilots. Limited sovereign credit ratings temper rollout speed but niche managed-service vendors are filling capability gaps.

Competitive Landscape

The market is moderately fragmented, with automation leaders Honeywell, Siemens, and ABB integrating recently acquired cyber platforms to field end-to-end offerings. Specialist players such as Dragos, Nozomi Networks, and Armis Security differentiate on deep-packet-inspection engines and OT threat-intel libraries. Utilities weigh longevity and integration breadth against speed and domain specialization, prolonging procurement cycles.

Interoperability is emerging as a decisive factor; joint reference architectures allow newer entrants to plug into incumbents’ control-room consoles. Honeywell’s 2024 acquisition of a zero-trust gateway firm signals convergence momentum, while Nozomi’s alliance with Accenture expands managed-service reach. AI features-automated playbooks, behavior baselining-now top RFP scoring matrices, forcing lagging vendors to accelerate roadmap deliveries. White-space persists in hydrogen facilities, post-quantum crypto orchestration, and undersea-asset monitoring.

Regional dynamics shape competition. North American utilities often dual-source between an automation major and a cyber boutique for risk hedging. European DSOs favor platform vendors adhering to emerging network code schemas, while Asia-Pacific buyers prioritize local support and price-performance ratios. Consolidation is expected as capital requirements for AI-driven R&D escalate.

Energy Security Industry Leaders

Honeywell International Inc.

Siemens Energy AG

ABB Ltd.

Schneider Electric SE

General Electric (GE) Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: CISA released the JCDC AI Cybersecurity Collaboration Playbook, fostering multilateral information-sharing to counter AI-specific threats in critical-infrastructure environments. The move positions federal agencies as conveners and accelerates SOC adoption of AI-for-AI defense approaches.

- January 2025: The EU adopted Regulation 2025/38 establishing Cyber Hubs that pool detection capacity across member states. The strategy aims to equalize defensive maturity and create a pooled incident-response fund, lowering single-country exposure.

- December 2024: The White House published the Energy Modernization Cybersecurity Implementation Plan, aligning federal funding with utility modernization to ensure security-by-design. The blueprint signals to vendors that projects tied to federal dollars must meet crypto-agility and zero-trust milestones.

- October 2024: CISA’s “Post-Quantum Considerations for OT” outlined migration paths toward quantum-resistant algorithms, prompting utilities to budget for crypto-agile firmware updates. The guidance accelerates vendor timelines for PQC modules.

Global Energy Security Market Report Scope

| Solutions |

| Services |

| Physical Security |

| Network and Application Security |

| Endpoint and Industrial-Control Security |

| Cloud and Edge-Security |

| Oil and Gas - Upstream |

| Oil and Gas - Midstream |

| Oil and Gas - Downstream |

| Thermal Power Generation |

| Nuclear Power Generation |

| Renewable Power Assets |

| Surveillance and Monitoring |

| Access Control and Perimeter Security |

| Command and Control Systems |

| Incident and Risk Management |

| Managed Detection and Response |

| Utilities (Transmission and Distribution) |

| Independent Power Producers |

| Oil Companies |

| EPC Contractors and System Integrators |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Solutions | ||

| Services | |||

| By Security Type | Physical Security | ||

| Network and Application Security | |||

| Endpoint and Industrial-Control Security | |||

| Cloud and Edge-Security | |||

| By Power-Infrastructure Type | Oil and Gas - Upstream | ||

| Oil and Gas - Midstream | |||

| Oil and Gas - Downstream | |||

| Thermal Power Generation | |||

| Nuclear Power Generation | |||

| Renewable Power Assets | |||

| By Application | Surveillance and Monitoring | ||

| Access Control and Perimeter Security | |||

| Command and Control Systems | |||

| Incident and Risk Management | |||

| Managed Detection and Response | |||

| By End-User | Utilities (Transmission and Distribution) | ||

| Independent Power Producers | |||

| Oil Companies | |||

| EPC Contractors and System Integrators | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the energy security market in 2030?

The energy security market is forecast to reach USD 25.33 billion by 2030, reflecting an 11.54% CAGR.

Which region is expected to grow the fastest through 2030?

Asia-Pacific is projected to record a 14.76% CAGR, driven by renewable capacity additions and evolving cyber mandates.

Which component segment is expanding most rapidly?

Services, especially managed detection and response, are growing at 12.77% CAGR as utilities seek external expertise.

How do NERC-CIP updates influence spending?

New CIP-015-1 internal monitoring requirements compel North American utilities to invest in OT-aware sensors and SIEM integrations before the September 2025 deadline.

Why is hydrogen infrastructure security gaining attention?

Hydrogen's material challenges and higher operating pressures necessitate novel leak-detection and cyber-hardening measures, opening new solution niches.

What drives the rise of satellite-based surveillance in pipelines?

Affordable LEO imaging and AI analytics enable near-real-time detection of leaks and sabotage, reducing manual patrol costs and environmental risk.

Page last updated on: