RF And Microwave Diodes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.11 Billion |

| Market Size (2031) | USD 2.48 Billion |

| Growth Rate (2026 - 2031) | 3.28% CAGR |

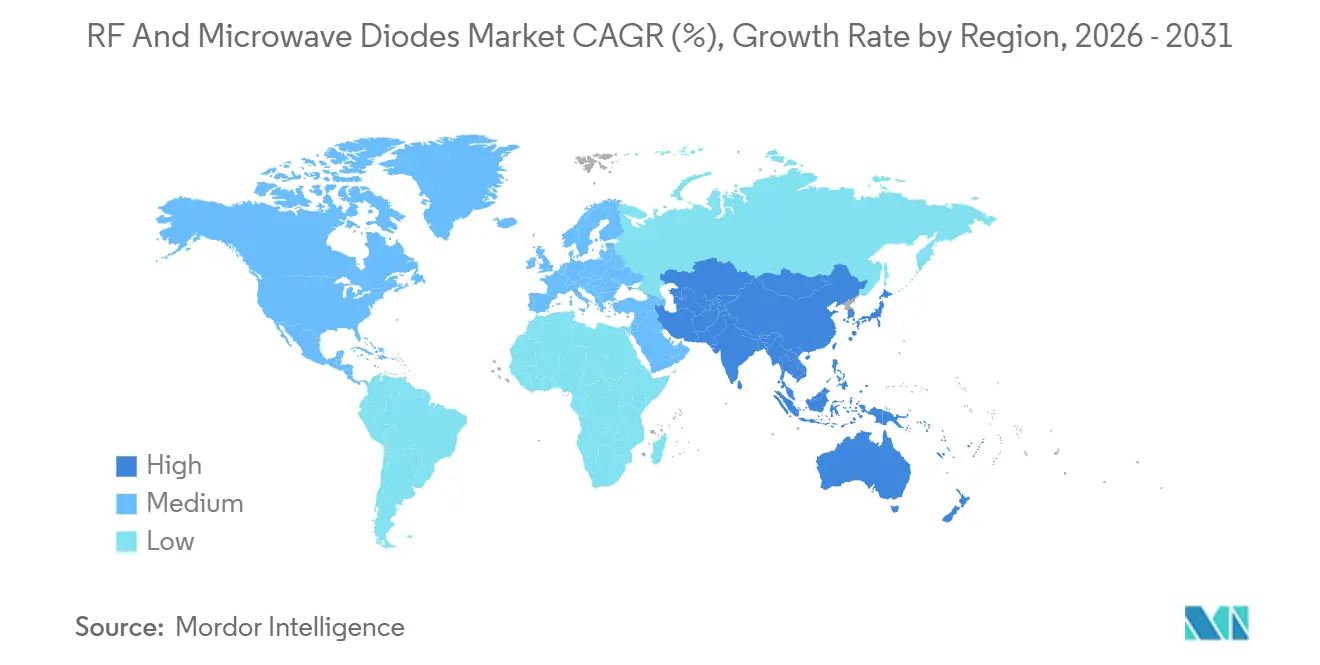

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

RF And Microwave Diodes Market Analysis by Mordor Intelligence

The RF and Microwave Diodes market size is projected to expand from USD 2.03 billion in 2025 and USD 2.11 billion in 2026 to USD 2.48 billion by 2031, registering a CAGR of 3.28% between 2026 to 2031. Surging 5G roll-outs, automotive radar mandates and low-Earth-orbit satellite launches are creating broad-based volume pull, while gallium export bans and export-control tightening are adding cost pressure and reshaping sourcing strategies. Wide-bandgap GaN and SiC devices are closing the cost gap with silicon, particularly as 300 mm substrates reach pilot production and promise double-digit die cost savings. Asia Pacific remains the demand engine on the back of China’s 4.838 million 5G macro cells and 1.204 billion 5G subscriptions, but North America is regaining share as CHIPS Act incentives drive new wafer-fab investments. Frequency dynamics have bifurcated; legacy 3–8 GHz C/X-band systems still anchor nearly one-third of sales, yet above-40 GHz mmWave designs are recording the fastest uptake as satellite operators migrate feeder links to Q/V-band and E-band. Competitive intensity is rising because no single supplier holds more than 15% share, and incumbents face margin pressure as parallel product lines are required for unrestricted and controlled export regions.

Key Report Takeaways

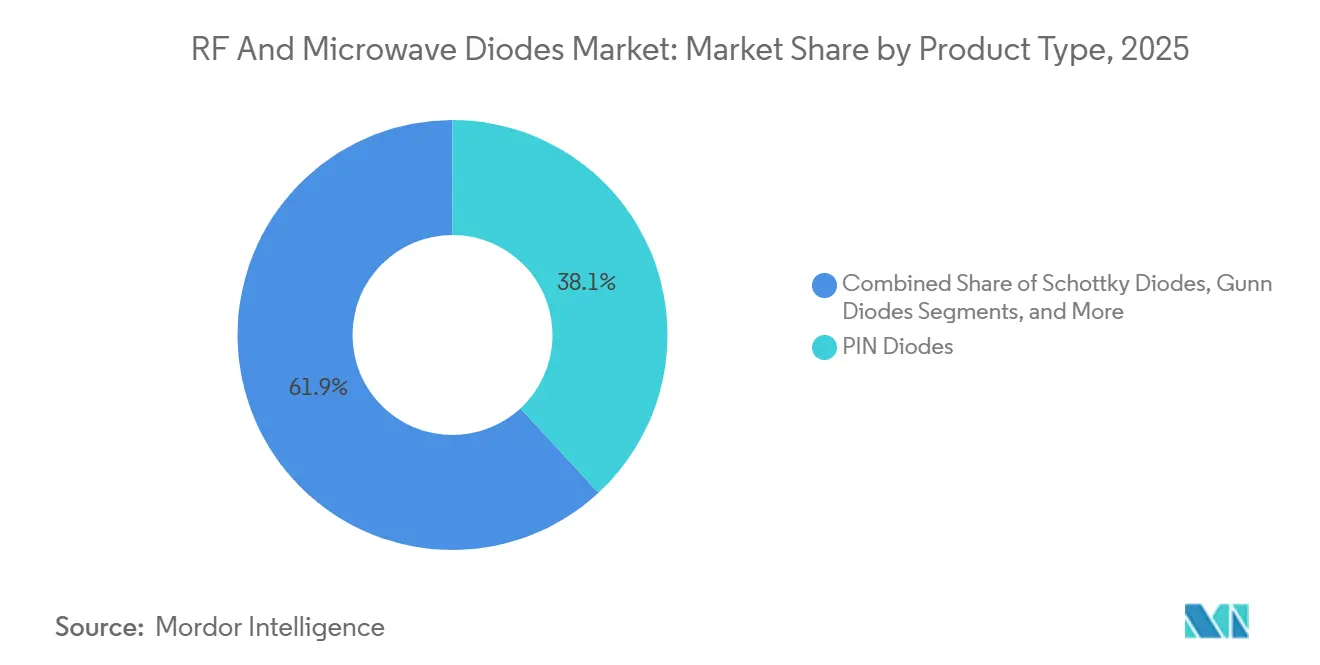

- By product type, PIN diodes led with 38.12% revenue share in 2025, while Schottky variants are forecast to record the fastest 3.83% CAGR through 2031.

- By frequency band, the 3–8 GHz C/X-band captured 29.53% of RF and Microwave Diodes market share in 2025, whereas the above-40 GHz mmWave band is projected to expand at a 3.74% CAGR to 2031.

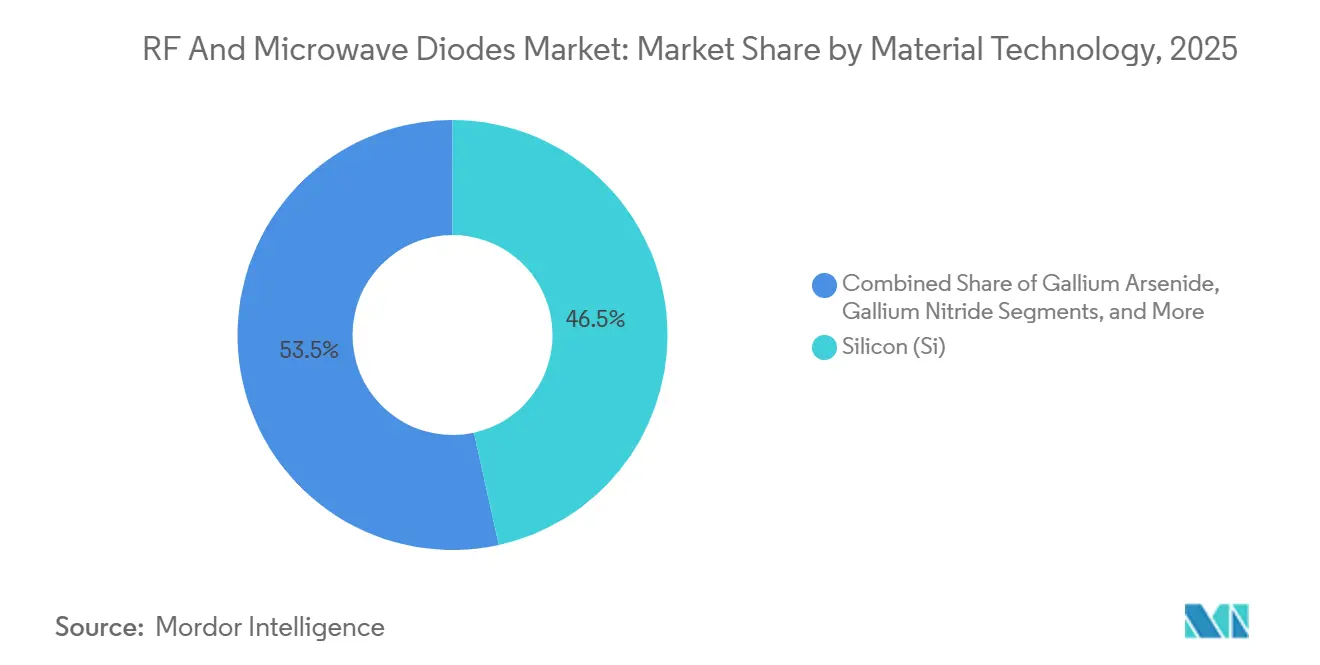

- By material technology, silicon accounted for 46.54% of RF and Microwave Diodes market size in 2025, and gallium nitride is poised for the quickest 3.68% CAGR during the forecast window.

- By end-user industry, telecommunications and networking held 37.57% revenue share in 2025, yet automotive is advancing at the highest 3.84% CAGR on the back of ADAS mandates.

- By geography, Asia Pacific commanded 42.43% sales in 2025 and is estimated to grow at a 3.46% CAGR to 2031, maintaining regional leadership.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global RF And Microwave Diodes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Global 5G Infrastructure | +0.8% | Asia Pacific, North America, Europe | Medium term (2-4 years) |

| Rising IoT and Smart Consumer Electronics Demand | +0.6% | Global | Medium term (2-4 years) |

| Expansion of Automotive Radar and ADAS Adoption | +0.7% | North America, Europe, Asia Pacific | Long term (≥ 4 years) |

| Growth of LEO Satellite Constellations | +0.5% | Global | Long term (≥ 4 years) |

| mmWave Radar Uptake in Industrial Drones and Robots | +0.3% | Early adoption in North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Shift Toward Wide-Bandgap GaN/SiC Technology | +0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation Of Global 5G Infrastructure

More than 642 network operators had allocated capital to 5G by 2025, with 374 of them launching commercial service, and 182 already investing in standalone cores. China’s 4.838 million macro cells translate into very large volumes of PIN diodes for transmit-receive switching and varactor diodes for oscillator tuning.[1]Ministry of Industry and Information Technology, “2025 Communications Industry Statistical Bulletin,” miit.gov.cn Antenna densification in massive-MIMO radios is pulling additional Schottky rectifiers into low-noise power rails that must handle sub-nanosecond switching events. Parallel mid-band and mmWave spectrum allocations are widening the design-in envelope and supporting multi-band front-end architectures. The resulting component proliferation is giving device makers the scale they need to accelerate GaN cost reductions.

Rising IoT And Smart Consumer Electronics Demand

China counted 2.888 billion cellular IoT connections in 2025, an 8.7% year-over-year increase that highlights the heterogeneous nature of RF design targets. Wearables emphasize low leakage current to maximize battery life, while industrial gateways require higher thermal margins. Wi-Fi 6E and Wi-Fi 7 upgrades are broadening tuning ranges for varactor diodes in routers and smartphones. Meanwhile, Schottky rectifiers are displacing PIN devices in low-voltage converters for always-on radios because their lower forward drop improves system efficiency. Edge-AI use in home assistants and security cameras adds further demand for quiet power rails, reinforcing the shift to low-loss Schottky structures.

Expansion Of Automotive Radar And ADAS Adoption

Euro NCAP’s 2026 protocol makes Lane Support Systems mandatory for a five-star rating, the EU General Safety Regulation mandated AEB and Lane Keep Assist from July 2024, and NHTSA requires AEB on all U.S. passenger vehicles by September 2029.[2]Euro NCAP, “2026 Assessment Protocols,” euroncap.com Each 77 GHz radar module integrates several Schottky mixer diodes plus varactors that generate FMCW chirps. Infineon’s October 2025 automotive-qualified GaN suite allows smaller die size, lowering insertion loss and extending detection range. The industry migration from 77 GHz to 79 GHz for finer range resolution is set to create a replacement cycle that will sustain RF and Microwave Diodes market growth well beyond first-fit volumes.

Growth Of LEO Satellite Constellations

Starlink alone operated 6,676 active craft in 2025 and targets 42,000 satellites, while Eutelsat-OneWeb keeps 648 spacecraft in orbit,. Next-generation “V3” buses pursue 1 Tbit/s throughput, forcing a switch to Q/V-band and E-band feeder links where Schottky mixers and PIN limiters work in tandem. Vacuum environments complicate heat removal, so Kyocera’s copper-molybdenum spreaders and Gore’s sub-0.3 dB thermal insulation have become necessary adjuncts,. As launch cadences tighten, satellite builders lock in multiyear diode contracts, de-risking demand even when consumer broadband uptake fluctuates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Raw-Material Prices (Ga, Si, SiC, InP) | -0.5% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Semiconductor Capacity Constraints and Supply Chain Risk | -0.3% | Global | Medium term (2-4 years) |

| Thermal-Management Challenges Above 40 GHz | -0.2% | Global | Long term (≥ 4 years) |

| Export-Control Restrictions on High-Frequency Devices | -0.3% | U.S.–China trade corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Prices (Ga, Si, SiC, InP)

China’s December 2024 gallium export ban removed 98–99% of global supply, driving European spot prices to USD 687 per kg by May 2025, a 150% surge.[3]U.S. Geological Survey, “Mineral Commodity Summaries: Gallium,” usgs.gov U.S. consumption relies entirely on imports, and fabs scrambled to qualify Japanese and South Korean suppliers once China’s May shipments fell to zero. Wolfspeed’s 300 mm SiC wafer breakthrough promises up to 40% cost relief, yet volume production will not materialize before 2027, leaving near-term pricing unpredictable. Indium phosphide, essential for high-frequency Gunn and tunnel diodes, also suffers from regional concentration. Such volatility squeezes margins and deters long-horizon capacity planning for RF and Microwave Diodes market participants.

Semiconductor Capacity Constraints And Supply Chain Risk

Global fab output reached 42.5 million 300 mm-equivalent wafers per quarter by Q1 2025, yet wafer-fab-equipment spending rose 19% year-over-year, signaling ongoing tightness. More than 100 U.S. projects worth over USD 500 billion aim to triple domestic capacity by 2032, but labor shortages may delay ramps, as the sector faces a projected 67,000-worker gap by 2030. Operating costs in the United States run 10–35% above Asian hubs, and any disruption in Taiwan or South Korea could ripple through diode supply chains within weeks. Export-license reviews now cover PIN and Schottky diodes, further stretching lead times for customers in controlled geographies.[4]Bureau of Industry and Security, “Export Control Updates December 2024,” bis.doc.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Schottky Diodes Outpace Legacy PIN Solutions

PIN devices held 38.12% of 2025 revenue, underscoring their indispensability in base-station switches and attenuators that must handle high RF power with low distortion. Schottky variants, though, are forecast at a 3.83% CAGR thanks to lower forward voltage and faster recovery that enhance DC-DC conversion efficiency. The RF and Microwave Diodes market size for Schottky-enabled power conditioning in 5G active-antenna units is set to expand sharply as carriers densify urban networks. Infineon’s industrial GaN device with an integrated Schottky diode, released in April 2025, eliminates bond-wire inductance and enables power-stage switching well above 100 MHz, a specification increasingly required for mmWave beamforming boards.

Varactor diodes continue to ride the Wi-Fi 6E and Wi-Fi 7 upgrade cycle, while Gunn and tunnel devices preserve narrow defense and instrumentation niches. Zener solutions remain crucial for transient suppression in multiband transceivers, particularly as vehicle electrical systems migrate from 12 V to 48 V. Other specialty diodes such as step-recovery parts address harmonic-rich timing circuits in test gear. As original-equipment makers move from discrete devices toward module-level integration, suppliers that package Schottky mixers together with low-noise amplifiers gain design-win momentum, lifting average selling prices inside the RF and Microwave Diodes market.

By Frequency Band: mmWave Momentum Builds Above 40 GHz

The up-to-3 GHz tier still powers IoT gateways and sub-6 GHz cellular networks, but its unit volumes do not translate into proportional revenue because pricing remains commoditized. In contrast, the 3–8 GHz C/X-band commanded 29.53% of 2025 turnover, benefiting from entrenched microwave backhaul and weather-radar fleets. Moving higher, the 20–40 GHz Ka/V-segment has become the workhorse for 77 GHz automotive radar and 24–29 GHz 5G millimeter-wave small cells. However, the above-40 GHz category shows the fastest 3.74% CAGR as LEO operators adopt Q/V-band and E-band feeder links; that trajectory is pulling higher-margin PIN limiters and Schottky mixers into payloads, increasing the RF and Microwave Diodes market share of wide-bandgap material suppliers.

Thermal-management complexity rises steeply in the mmWave domain, forcing diode vendors to co-design with substrate providers on copper-molybdenum spreaders or embedded heat pipes. Gore’s insulation, with less than 0.3 dB insertion loss at package level, demonstrates that even fractional performance gains can unlock multi-year supply agreements. As satellite data-rate targets approach terabit-per-second levels, every tenth-of-a-percent efficiency improvement frees stored energy, adding revenue leverage for component vendors that can deliver validated mmWave operating envelopes.

By Material Technology: GaN Nears Cost Parity With Silicon

Silicon sustained 46.54% of 2025 sales because 300 mm lines provide mature yields above 95%, and sub-8 GHz designs rarely require the power density of wide-bandgap devices. Yet gallium nitride is forecast to grow 3.68% over the outlook as telecom and radar designers push into frequencies where silicon losses become untenable. The RF and Microwave Diodes market size tied to GaN is set to accelerate once 300 mm wafers exit pilot stage; Infineon shipped the first samples in Q4 2025, promising to halve die cost compared with 200 mm production.

GaAs keeps a foothold in the 8–40 GHz space, bridging the cost gap between silicon and GaN, while Wolfspeed’s 300 mm SiC announcement signals meaningful cost relief for high-temperature, high-power designs. Indium phosphide and other exotic substrates remain essential for ultra-high-frequency research radar and scientific instrumentation. Intellectual-property filings are tilting the competitive field; 70% of Q3 2025 GaN patent families originated in China, suggesting local fabs aim to capture multiband infrastructure sockets despite export-license constraints.

By End-User Industry: Automotive Takes The Growth Crown

Telecommunications and networking delivered 37.57% of 2025 turnover, buoyed by 5G macro cell rollouts in Asia Pacific and mid-band refarming in North America. Automotive, however, is projected to post a 3.84% CAGR to 2031, making it the fastest-growing vertical. Each modern light vehicle will integrate at least three long-range radar modules plus multiple short-range sensors, embedding eight to ten Schottky mixer diodes and several varactors per car by mid-decade. The RF and Microwave Diodes market size tied to automotive radar therefore expands in lockstep with ADAS adoption curves.

Consumer electronics remains price sensitive yet vast, with Wi-Fi 6E routers and Wi-Fi 7 smartphones introducing wider tuning ranges for varactor diodes. Industrial automation is another bright spot, as 60 GHz radar augments optical sensors in autonomous mobile robots. Aerospace and defense preserve high-margin demand for GaN solutions above 20 GHz, especially in active electronically steered arrays. Energy and utilities, notably in smart-grid communications, and medical equipment such as microwave ablation systems round out a diversified customer base that helps buffer cyclical swings in any single sector.

Geography Analysis

Asia Pacific held 42.43% of 2025 revenue and is on track to expand at a 3.46% CAGR to 2031. China’s scale dominates, but South Korea and Taiwan add resilience through foundry specialization, while Japan’s Rapidus project seeks to reclaim advanced-node production. Gallium export leverage and a 70% share of recent GaN patent filings provide additional strategic weight for the region.

North America is re-emerging as a manufacturing base thanks to CHIPS Act incentives worth up to USD 52 billion, complemented by state-level tax abatements. MACOM’s USD 345 million GaN expansion, backed by USD 70 million in federal funding, and Infineon’s Dresden-to-Kulim expansion plan underscore a pivot toward regional redundancy. Yet higher capex and opex, alongside a skilled-labor shortage, temper the growth rate relative to Asia.

Europe’s opportunity revolves around its auto industry. Euro NCAP and EU General Safety Regulation mandates ensure every new car sold across the bloc will contain radar modules by mid-decade, anchoring diode demand even as production volumes plateau. Meanwhile, Middle East and Africa and South America remain sub-scale markets that grow primarily when telecom operators accelerate 4G-to-5G upgrades or when mining automation pilots convert to full deployments.

Competitive Landscape

The RF and Microwave Diodes market is moderately concentrated, with the top five suppliers Infineon, MACOM, Qorvo, Skyworks and Broadcom commanding major share of sales. Infineon is leveraging cost leadership through 300 mm GaN wafers and the April 2024 acquisition of GaN Systems, securing both intellectual property and a broader automotive design-in pipeline. MACOM is doubling down on defense and satellite sectors with its USD 345 million GaN capex program, betting that high-power radar use cases will absorb price premiums.

Qorvo’s May 2024 buyout of Anokiwave added beamforming IP that strengthens its position in phased-array basestations and LEO gateways. Broadcom and Skyworks remain volume leaders in sub-6 GHz silicon devices but face margin compression as telecom customers shift spend toward high-bandwidth mmWave links. Smaller niche players such as SemiGen and Central Semiconductor serve aerospace, medical and custom low-volume runs, thriving on agility rather than wafer scale.

Export-control tightening forces multinationals to carry duplicate product lines, elevating R&D spend and complicating inventory. Chinese fabs with rising GaN know-how are positioned to enter global infrastructure sockets once domestic demand hits critical mass, a trend foreshadowed by their dominant share of 2025 patent filings. The competitive playing field therefore hinges on simultaneous mastery of material science, compliance logistics and application-specific reference designs.

RF And Microwave Diodes Industry Leaders

Microchip Technology Inc.

Infineon Technologies AG

Diodes Incorporated

MACOM Technology Solutions Holdings, Inc.

Nexperia B.V. (Wingtech Technology Co., Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Wolfspeed demonstrated the first 300 mm SiC wafer, achieving 2.3× the chip yield of 200 mm wafers and opening a path to 30–40% cost reduction once production scales.

- October 2025: Infineon released AEC-Q101-qualified GaN devices for 77 GHz radar and on-board EV chargers.

- July 2025: Infineon shipped 300 mm GaN wafer samples to select telecom and automotive customers.

- May 2025: European gallium spot prices climbed to USD 687 per kg following China’s export ban, forcing fabs to qualify Japanese and South Korean suppliers.

Global RF And Microwave Diodes Market Report Scope

The RF and Microwave Diodes Market is witnessing significant growth due to increasing demand across various industries, including automotive, consumer electronics, and telecommunications. The advancements in material technologies and the rising adoption of high-frequency applications are driving the market's expansion. Additionally, the growing need for efficient and compact electronic components is further propelling the demand for RF and microwave diodes globally.

The RF and Microwave Diodes Market Report is Segmented by Type (PIN, Schottky, Varactor, Gunn, Tunnel, Zener, Other Diodes), Frequency Band (Up to 3 GHz, 3-8 GHz, 8-20 GHz, 20-40 GHz, Above 40 GHz), Material Technology (Si, GaAs, GaN, SiC, Other Materials), End-User Industry (Automotive, Consumer Electronics, Telecom, Industrial, Medical, Aerospace and Defense, Energy, Other), and Geography (North America, Europe, Asia Pacific, South America, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| PIN Diodes |

| Schottky Diodes |

| Varactor (Tuning) Diodes |

| Gunn Diodes |

| Tunnel Diodes |

| Zener Diodes |

| Other Diodes |

| Up to 3 GHz |

| 3 - 8 GHz, C-/X-Band |

| 8 - 20 GHz, Ku-/K-Band |

| 20 - 40 GHz, Ka-/V-Band |

| Above 40 GHz, mmWave |

| Silicon (Si) |

| Gallium Arsenide (GaAs) |

| Gallium Nitride (GaN) |

| Silicon Carbide (SiC) |

| Other Material Technologies |

| Automotive |

| Consumer Electronics |

| Telecommunications and Networking |

| Industrial Manufacturing and Automation |

| Medical and Healthcare |

| Aerospace and Defense |

| Energy and Utilities |

| Other End-User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Product Type | PIN Diodes | |

| Schottky Diodes | ||

| Varactor (Tuning) Diodes | ||

| Gunn Diodes | ||

| Tunnel Diodes | ||

| Zener Diodes | ||

| Other Diodes | ||

| By Frequency Band | Up to 3 GHz | |

| 3 - 8 GHz, C-/X-Band | ||

| 8 - 20 GHz, Ku-/K-Band | ||

| 20 - 40 GHz, Ka-/V-Band | ||

| Above 40 GHz, mmWave | ||

| By Material Technology | Silicon (Si) | |

| Gallium Arsenide (GaAs) | ||

| Gallium Nitride (GaN) | ||

| Silicon Carbide (SiC) | ||

| Other Material Technologies | ||

| By End-User Industry | Automotive | |

| Consumer Electronics | ||

| Telecommunications and Networking | ||

| Industrial Manufacturing and Automation | ||

| Medical and Healthcare | ||

| Aerospace and Defense | ||

| Energy and Utilities | ||

| Other End-User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the RF and Microwave Diodes market by 2031?

The market is projected to reach USD 2.48 billion by 2031.

Which segment is expected to grow fastest within the RF and Microwave Diodes market?

The above-40 GHz mmWave frequency band is forecast to register the quickest 3.74% CAGR through 2031.

Why is automotive radar boosting demand for RF and microwave diodes?

Regulatory mandates in the United States and Europe require AEB and lane-support functions, embedding multiple Schottky mixers and varactor diodes in each vehicle radar module.

How will gallium export controls influence diode pricing?

China’s export ban has already lifted European gallium prices by 150%, introducing cost volatility that may persist until alternative sources scale.

Which material technology shows the best growth outlook?

Gallium nitride is poised to expand at a 3.68% CAGR as 300 mm substrates reduce die costs and enable higher-frequency, higher-efficiency designs.

Are supply-chain risks easing with new U.S. fabs?

CHIPS Act projects improve regional balance, yet higher operating costs and skilled-labor shortages mean capacity additions will take several years to significantly reduce dependency on Asian hubs.

Page last updated on: