RF Plasma Generator Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

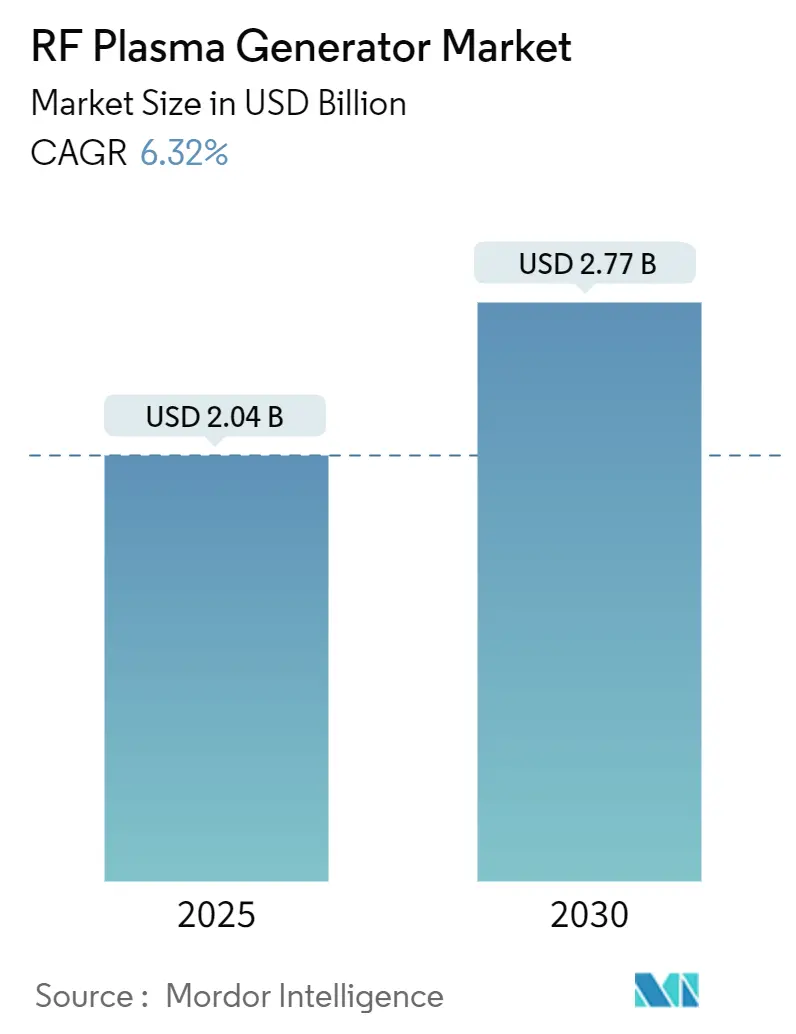

| Market Size (2025) | USD 2.04 Billion |

| Market Size (2030) | USD 2.77 Billion |

| Growth Rate (2025 - 2030) | 6.32% CAGR |

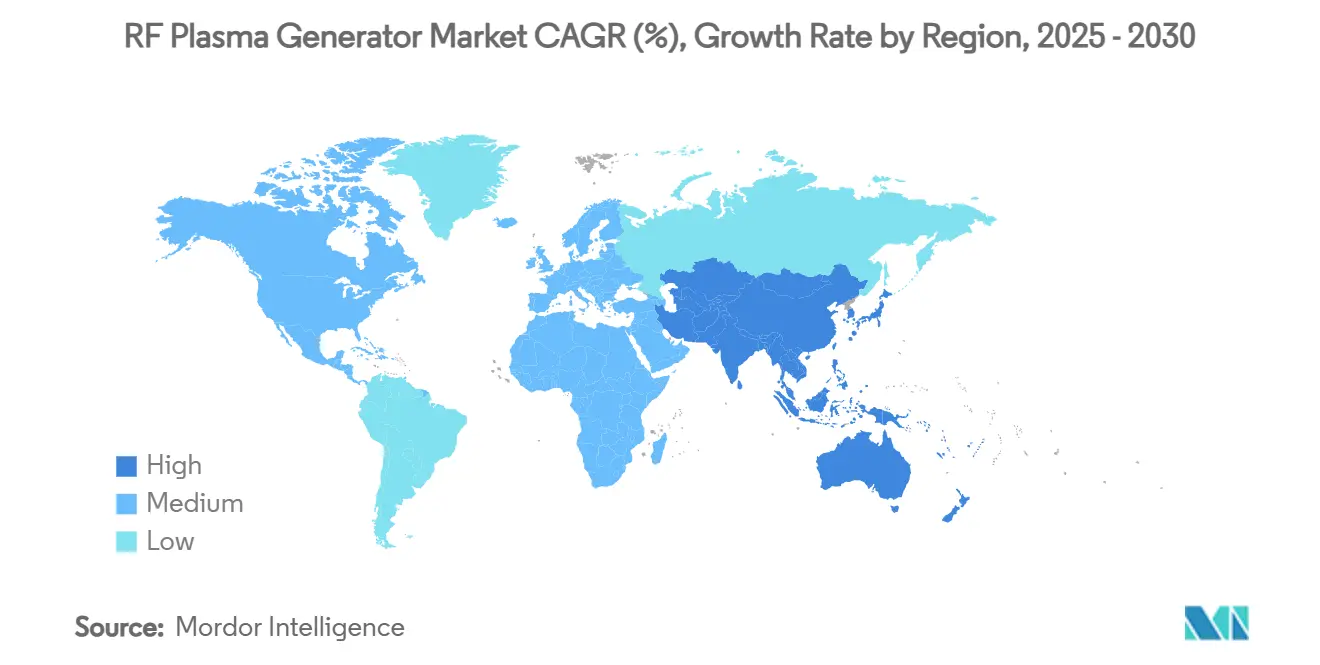

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

RF Plasma Generator Market Analysis by Mordor Intelligence

The RF plasma generator market size stood at USD 2.04 billion in 2025 and is forecast to climb to USD 2.77 billion by 2030, advancing at a 6.32% CAGR over the period. More than half of this incremental value stems from the migration to solid-state architectures that deliver sub-microsecond pulsing, which allows atomic-scale etch and deposition control. Foundry investments in gate-all-around transistors, the surge of 3D NAND demand, and rapid adoption of dry-plasma sterilizers in hospitals are the clearest demand triggers, while regional subsidy programs such as the CHIPS and European Chips Acts shorten replacement cycles for legacy magnetron systems. Suppliers compete on frequency agility, matching-network intelligence, and power efficiency, and most now integrate self-diagnostic software to meet fab predictive-maintenance mandates. At the same time, the RF plasma generator market faces capex sensitivity, evident in memory-led downcycles, and tighter greenhouse-gas rules that require costly abatement tie-ins.

Key Report Takeaways

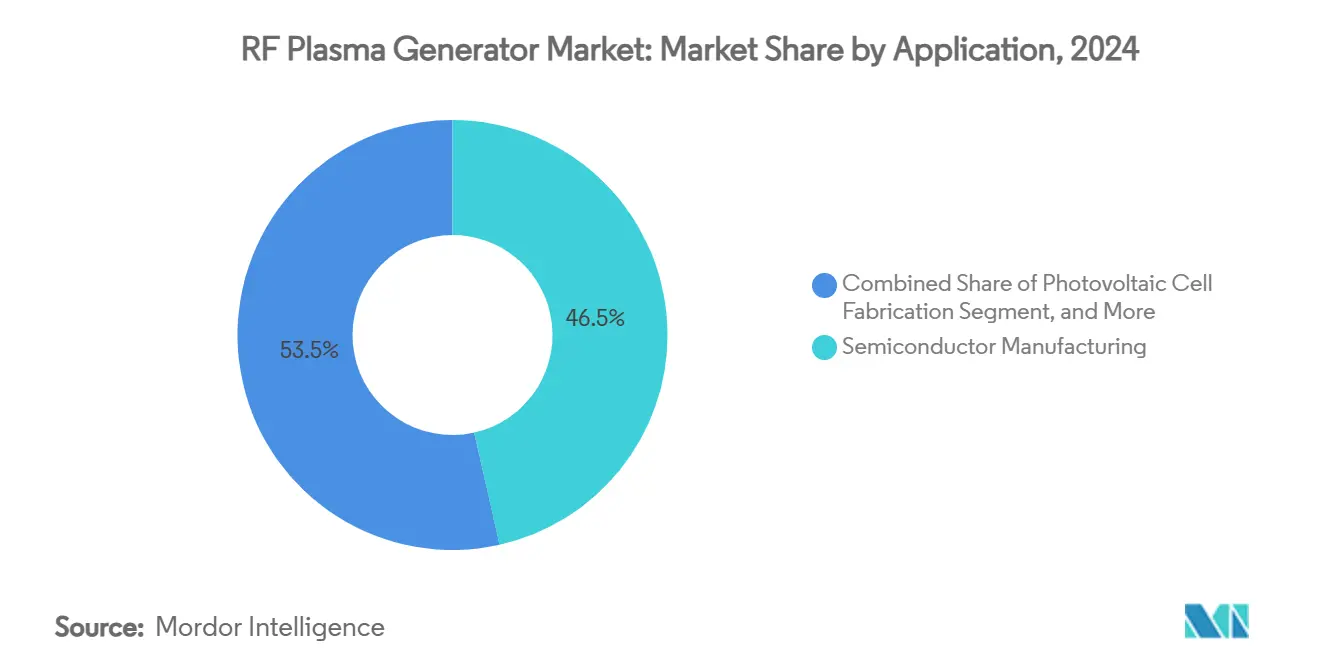

- By application, semiconductor manufacturing led with 46.50% of RF plasma generator market share in 2024; medical device sterilization is projected to register a 6.89% CAGR and become the fastest-growing outlet through 2030.

- By frequency, the well-entrenched 13.56 MHz segment commanded 63.20% of the RF plasma generator market size in 2024, whereas systems operating above 200 MHz are poised to expand at a 7.21% CAGR.

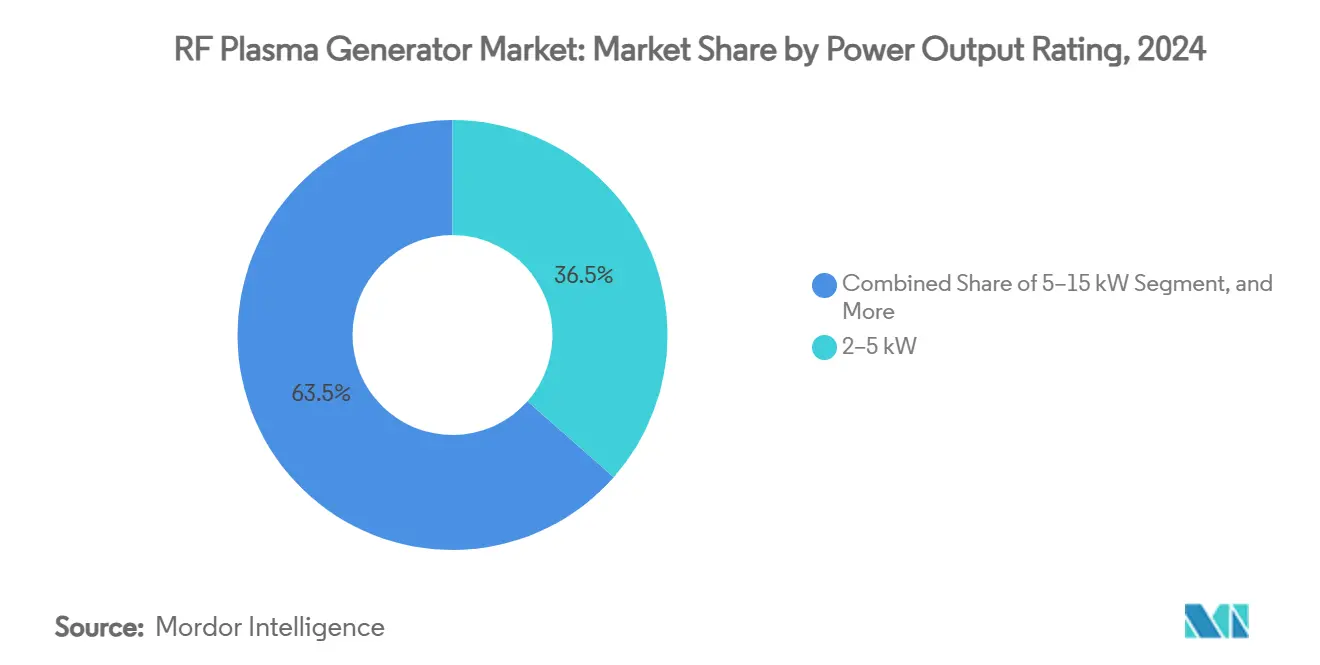

- By power rating, 2–5 kW units captured 36.50% revenue in 2024; sub-2 kW solutions are forecast to rise at a 6.78% CAGR as precision processes and hospital sterilizers scale.

- By plasma coupling type, inductively coupled plasma (ICP) equipment held 54.78% share of the RF plasma generator market size in 2024, while microwave plasma installations should see a 7.56% CAGR on the back of diamond-like carbon and wide-bandgap semiconductor applications.

- By geography, Asia-Pacific retained 49.00% of the RF plasma generator market in 2024 and is set to log a 7.29% CAGR to 2030, propelled by fab expansions in Taiwan, South Korea, and mainland China

Global RF Plasma Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging advanced-node semiconductor fab expansions | +1.8% | APAC, North America | Medium term (2–4 years) |

| Proliferation of thin-film solar PV capacity additions | +1.2% | China, Europe, North America | Long term (≥ 4 years) |

| Ramp-up of OLED and microLED display manufacturing lines | +0.9% | APAC, North America | Medium term (2–4 years) |

| Government incentives for domestic chip supply chains | +1.1% | North America, Europe | Short term (≤ 2 years) |

| Solid-state RF topology enables sub-µs pulsed control | +0.7% | Global | Long term (≥ 4 years) |

| Adoption of dry-plasma sterilization in hospitals | +0.5% | North America, Europe, developed APAC | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surging Advanced-Node Semiconductor FAB Expansions

Large-scale commitments topping USD 400 billion for 300 mm tools through 2027 lock in multi-year demand for more than 10,000 high-precision RF generators.[1]SEMI, “Global Semiconductor Industry Plans to Invest $400 Billion in 300 mm Fab Equipment Over Next Three Years,” semi.org Each gate-all-around logic fab or 3D NAND line now specifies dozens of above-200 MHz solid-state units for high-aspect-ratio etch, pushing the RF plasma generator market toward higher frequency and faster pulsing. Domestic diversification drives orders in Arizona, Texas, and Dresden as operators aim to derisk Asia-centric supply chains.[2]National Institute of Standards and Technology, “CHIPS for America Awards,” nist.gov Strong back-end demand for chiplets and advanced packaging adds further pull for sub-2 kW units that enable delicate insulating-layer trimming. Consequently, suppliers secure backlog visibility extending well beyond a typical semiconductor equipment cycle, cushioning the RF plasma generator market from macro slowdowns.

Proliferation of Thin-Film Solar PV Capacity Additions

Third-generation CIGS and perovskite cell makers rely on plasma-enhanced CVD to form ultra-thin absorber layers with nanometer precision, creating a ready outlet for mid-power ICP systems. Each new gigawatt of thin-film PV capacity calls for 50-100 RF generators tuned for low-temperature, atmospheric-pressure operation. Europe’s renewable-energy mandate and China’s production-linked incentives accelerate gigafactory build-outs, sustaining the RF plasma generator market even when crystalline-silicon demand plateaus. Solid-state generators offering 80% wall-plug efficiency trim operating costs and shorten payback periods, a decisive advantage amid razor-thin PV margins.

Ramp-up of OLED and MicroLED Display Manufacturing Lines

Gen-8.5 and Gen-10.5 LCD fabs converting to OLED require hundreds of 13.56 MHz sources for transparent-conductor deposition and high-uniformity plasma cleaning, while emerging microLED lines specify 40-200 MHz units capable of sub-µs pulsed operation to maintain pixel integrity. Automotive demand for curved, glare-free dashboards further magnifies the RF plasma generator market, as plasma-based anti-reflective coating steps proliferate. Capacity additions by Samsung Display and LG Display underline the momentum, with each new line budgeting USD 20–30 million purely for RF power delivery hardware. As display glass sizes grow, uniform plasma density across oversized substrates elevates generator power-stability requirements, favouring vendors with closed-loop impedance-matching systems.

Government Incentives for Domestic Chip Supply Chains

The CHIPS Act’s USD 4.745 billion award to Samsung Texas and USD 1.45 billion to GlobalFoundries New York effectively front-loads domestic equipment orders. A 25% tax credit on tool purchases slashes payback periods, allowing fabs to upgrade to premium solid-state units rather than incremental magnetron retrofits. Parallel European Chips Act allocations, such as Infineon’s EUR 5 billion Smart Power Fab, seed fresh demand nodes outside Asia.[3]Infineon Technologies, “German Government Issues Final Funding Approval for New Fab in Dresden,” infineon.com Because most grants stipulate cybersecurity and origin-of-manufacture clauses, local assembly plants for RF generators emerge, but vendors must certify secure firmware and transparent supply chains to qualify. These incentives compress the procurement window into a 24-to-30-month span, inflating near-term RF plasma generator market revenue visibility.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex of RF generators and matching networks | -1.4% | Global | Short term (≤ 2 years) |

| Cyclicality of semiconductor equipment investments | -1.1% | Global | Medium term (2–4 years) |

| EMI compliance challenges at 13.56 MHz in dense fabs | -0.6% | APAC advanced facilities | Long term (≥ 4 years) |

| Tightening GHG rules on PFC emissions in plasma etch | -0.8% | North America, Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Capex of RF Generators and Matching Networks

Leading-edge solid-state systems cost USD 200,000–500,000 apiece before add-ons, limiting adoption among tier-two fabs and emerging-market assemblers. Matching networks and impedance tuners can double lifecycle outlays, prompting procurement deferrals during downturns. Leasing programs mitigate upfront cash burn, yet elevated interest rates still hamper small operators. As a result, some capacity expansions deploy a hybrid fleet-keeping legacy magnetron sources for non-critical steps-tempering the RF plasma generator market’s penetration pace.

Cyclicality of Semiconductor Equipment Investments

Wafer-fab spending swings of 30-40% every three to four years create feast-and-famine cycles that cascade through the RF plasma generator market. Memory manufacturers in particular cancel or accelerate tool deliveries based on spot-pricing swings, complicating inventory planning. The current AI-driven boom softens the downside, yet the possibility of demand digestion after hyperscale build-outs lingers. Vendors with diversified end-market exposure-such as medical sterilization or thin-film PV-weather these troughs more effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Semiconductor Manufacturing Drives Advanced-Node Demand

Semiconductor manufacturing contributed 46.50% of the RF plasma generator market size in 2024, reflecting its dependence on plasma-enabled etch and deposition for 2 nm logic and 3D NAND stacks. Every advanced logic fab incorporates more than 500 RF power channels, with half earmarked for high-frequency, pulsed processes that demand sub-µs control. Medical device sterilization, while only a mid-single-digit share today, expands at a 6.89% CAGR as hospitals phase out ethylene-oxide and prefer rapid, low-temperature RF plasma cycles.

The RF plasma generator industry also benefits from OLED and microLED display growth, where transparent-conductor sputter and pixel delineation steps rely on stable 13.56 MHz sources. Thin-film solar producers increase orders for 40–60 MHz units tailored to low-temperature CVD, while aerospace and automotive coaters adopt ICP systems for wear-resistant surfaces. Across all uses, predictive-maintenance dashboards bundled with modern generators help fabs push utilization, deepening vendor lock-in.

By Frequency: 13.56 MHz Dominance Faces High-Frequency Challenge

The 13.56 MHz segment maintained 63.20% of RF plasma generator market share in 2024, thanks to ISM-band availability and well-established process recipes. Above-200 MHz generators, however, exhibit a 7.21% CAGR and encroach on advanced-node etch, where a tighter ion-energy spread is mandatory. 40.68 MHz and 60–200 MHz units occupy a middle ground, servicing legacy logic and R&D labs that need higher plasma density without completely overhauling matching networks.

Looking ahead, fab floor EMI congestion may accelerate the pivot toward higher frequencies. Vendors experiment with frequency-hopping modes to avoid standing-wave hotspots, integrating AI-driven impedance tuning to preserve uniformity. Certification for these novel bands remains a hurdle, yet early adopters report yield gains that justify the premium, keeping the RF plasma generator market in a state of healthy technological churn.

By Power Output Rating: Mid-Range Systems Dominate Process Applications

Units rated 2–5 kW held 36.50% of 2024 revenue, the sweet spot for mainstream 300 mm processes that balance throughput and wafer thermal budgets. Sub-2 kW models, on track for a 6.78% CAGR, penetrate sterilization cabinets and atomic-layer etch tools where thermal management is critical. Conversely, >15 kW behemoths serve Gen-10.5 glass and large-area coating lines that need uniform ion flux across 3 plus-square-meter substrates.

Solid-state GaN devices propel efficiency to 80%, reducing chill-water loads and making high-power platforms palatable for green-fab initiatives. In parallel, modular architectures let fabs daisy-chain low-power bricks to hit tailored output targets, an approach that simplifies spares logistics and elevates the RF plasma generator market’s service revenue component.

By Plasma Coupling Type: ICP Technology Leads Advanced Applications

Inductively coupled plasma sources captured 54.78% of the RF plasma generator market size in 2024 because they attain higher plasma densities and lower ion energies compared to capacitive alternatives. ICP chambers excel in high-aspect-ratio etch for 3D structures, justifying their premium. Capacitive systems remain prevalent in mature logic and MEMS lines where uniformity demands are less exacting.

Microwave plasma, while only a sliver today, grows 7.56% annually and finds niches in diamond-like carbon, gallium nitride, and specialty coatings. Hybrid systems that switch between ICP and microwave modes within the same reactor emerge, promising flexibility but challenging generator vendors to deliver multi-band, multi-kilowatt outputs in compact footprints-yet another spur for RF plasma generator market innovation.

Geography Analysis

Asia-Pacific’s cluster of mega-fabs and display super-lines powers nearly half of global shipments, and regional grants-such as South Korea’s K-Chip initiative-anchor capacity additions through the decade. Taiwan pursues 1.4-nm pilot-lines that will each require an estimated 600 RF power channels, ensuring continued leadership for the RF plasma generator market. South Korea’s HBM uplift and mainland China’s thin-film PV surge add parallel growth layers. Regional vendors leverage proximity for quick service response, cementing stickiness.

North America’s share accelerates on the back of Samsung Texas, TSMC Arizona, and Intel Ohio build-outs. The 25% AMIC credit effectively lowers net tool capex, encouraging fabs to specify premium solid-state RF stacks rather than refurbish older sets, a boon for domestic generator assemblers. Medical-device hubs in Minnesota and California deploy low-power sterilizers, widening the RF plasma generator market’s healthcare footprint.

Europe’s Smart Power Fab in Dresden and onsemi’s SiC line in the Czech Republic create fresh demand for mid-power ICP systems optimized for wide-bandgap materials. Stringent F-gas quotas push adoption of advanced abatement and low-PFC chemistries, which in turn mandate more precise RF power control. While regional volumes are smaller than APAC, Europe’s focus on sustainability sparks orders for ultra-efficient GaN-based generators, setting benchmarks that ripple worldwide.

Competitive Landscape

Advanced Energy Industries and MKS Instruments collectively supply more than one-third of global generator channels, capitalizing on end-to-end portfolios that bundle matching networks, arc suppression, and process control software. Advanced Energy’s USD 374.2 million Q3 2024 revenue underscored strength in both foundry and data-center sectors. MKS pairs RF power with proprietary impedance-tuner algorithms, locking in high gross margins.

ASM International vaulted into the top tier after acquiring Reno Sub-Systems for its electronically variable capacitor technology, enabling sub-millisecond power modulation that raises wafer throughput. Niche entrants such as Ampleon exploit GaN-on-Si to deliver 80% efficiency, attracting green-fab projects and forcing incumbents to accelerate their own wide-bandgap roadmaps.

Geopolitical risk reshapes sourcing. U.S. fabs favor American-built generators to secure export-control compliance, whereas Chinese equipment vendors-supported by state grants-target domestic OLED and PV lines. Service contracts and firmware updates become long-term revenue levers, with predictive analytics reducing unscheduled downtime. As the RF plasma generator market becomes more software-centric, incumbents beef up cybersecurity to defend intellectual property and satisfy new regulatory clauses embedded in subsidy programs.

RF Plasma Generator Industry Leaders

Advanced Energy Industries Inc.

MKS Instruments Inc.

TRUMPF Hüttinger GmbH + Co. KG

Comet Plasma Control Technologies AG

Daihen Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: : Infineon received final German funding for its EUR 5 billion Smart Power Fab in Dresden, with production slated for 2026 and an expected order for more than 800 RF channels.

- January 2025: MACOM committed USD 345 million to expand 100 mm GaN and GaAs wafer capacity and introduce 150 mm GaN-on-SiC, boosting long-term demand for high-frequency RF plasma generators.

- December 2024: SEMI projected global semiconductor equipment revenue to hit USD 139 billion in 2026, with wafer-fab tools at USD 101 billion, reinforcing tailwinds for the RF plasma generator market.

- October 2024: The U.S. Treasury finalized the Advanced Manufacturing Investment Credit rules, granting 25% tax relief on semiconductor equipment, including RF generators, effective immediately.

Global RF Plasma Generator Market Report Scope

| Semiconductor Manufacturing |

| Display and Flat-Panel Processing |

| Industrial Coatings and PECVD |

| Photovoltaic Cell Fabrication |

| Medical Device Sterilization |

| Other Applications |

| 13.56 MHz |

| 40.68 MHz |

| 60–200 MHz (HF/VHF) |

| above 200 MHz Pulsed/Custom |

| less than or equals to 2 kW |

| 2–5 kW |

| 5–15 kW |

| above 15 kW |

| Capacitively Coupled Plasma (CCP) |

| Inductively Coupled Plasma (ICP) |

| Microwave Plasma |

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East and Africa |

| By Application | Semiconductor Manufacturing |

| Display and Flat-Panel Processing | |

| Industrial Coatings and PECVD | |

| Photovoltaic Cell Fabrication | |

| Medical Device Sterilization | |

| Other Applications | |

| By Frequency | 13.56 MHz |

| 40.68 MHz | |

| 60–200 MHz (HF/VHF) | |

| above 200 MHz Pulsed/Custom | |

| By Power Output Rating | less than or equals to 2 kW |

| 2–5 kW | |

| 5–15 kW | |

| above 15 kW | |

| By Plasma Coupling Type | Capacitively Coupled Plasma (CCP) |

| Inductively Coupled Plasma (ICP) | |

| Microwave Plasma | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

How large is the RF plasma generator market in 2025?

The RF plasma generator market size reached USD 2.04 billion in 2025 and is set to rise to USD 2.77 billion by 2030.

What CAGR is expected for RF plasma generators through 2030?

Mordor Intelligence projects a 6.32% CAGR from 2025 to 2030, driven by solid-state upgrades and regional subsidy programs.

Which application segment dominates demand?

Semiconductor manufacturing held 46.50% of 2024 revenue thanks to advanced-node fabs that require hundreds of RF channels each.

Which frequency band is growing the fastest?

Generators operating above 200 MHz are forecast to expand at a 7.21% CAGR because they support sub-µs pulsed etch for 2 nm logic.

How will the CHIPS Act affect equipment suppliers?

The 25% tax credit on qualifying tools accelerates U.S. fabs’ procurement schedules, lifting near-term orders for domestic generator vendors.

What environmental regulations influence product design?

Stricter PFC-emission caps in the U.S. and EU compel generator makers to integrate high-efficiency power chains and abatement-ready interfaces.

Page last updated on: