Electronic Data Capture Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

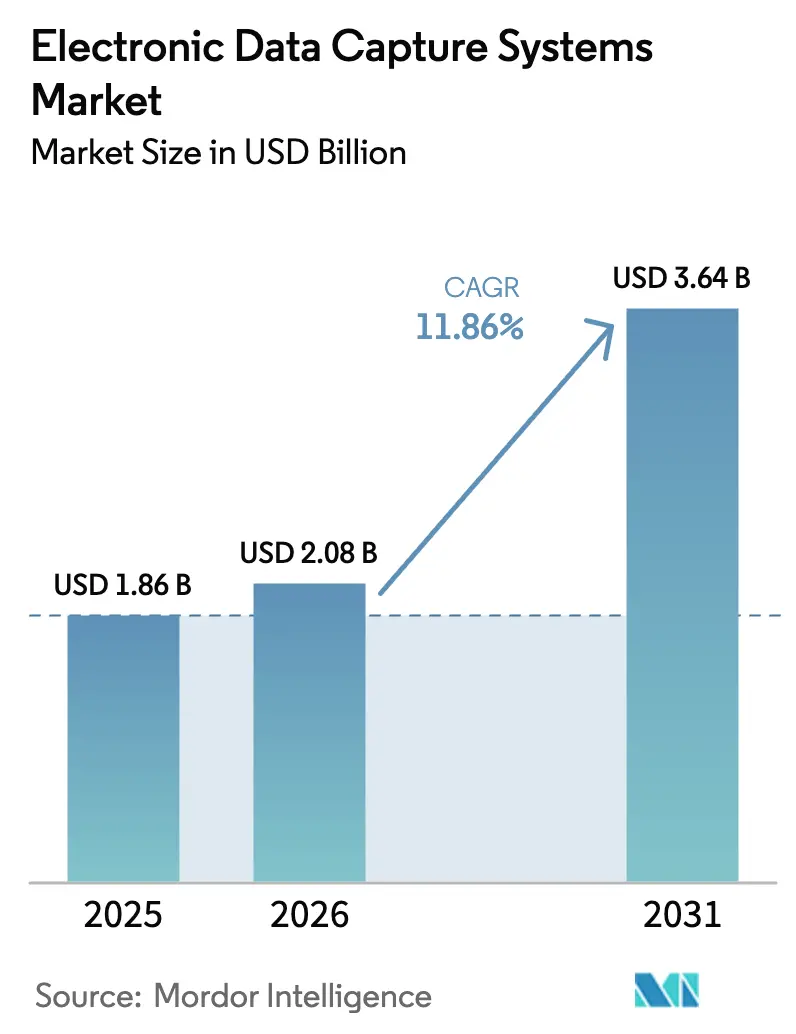

| Market Size (2026) | USD 2.08 Billion |

| Market Size (2031) | USD 3.64 Billion |

| Growth Rate (2026 - 2031) | 11.86% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronic Data Capture Systems Market Analysis by Mordor Intelligence

The Electronic Data Capture Systems market size is expected to grow from USD 1.86 billion in 2025 to USD 2.08 billion in 2026 and is forecast to reach USD 3.64 billion by 2031 at 11.86% CAGR over 2026-2031. Demand accelerates as decentralized and hybrid clinical-trial models become routine, cloud deployment overtakes on-premise systems, and pharmaceutical sponsors intensify investments in AI-ready platforms. Wider use of tokenization to secure real-world data, fast-growing post-market surveillance studies, and strategic vendor consolidation combine to keep the Electronic Data Capture Systems market on a steep growth curve. Persistent concerns around cybersecurity, high implementation costs, and interoperability gaps with next-generation digital health technologies temper the pace but do not derail overall momentum.

Key Report Takeaways

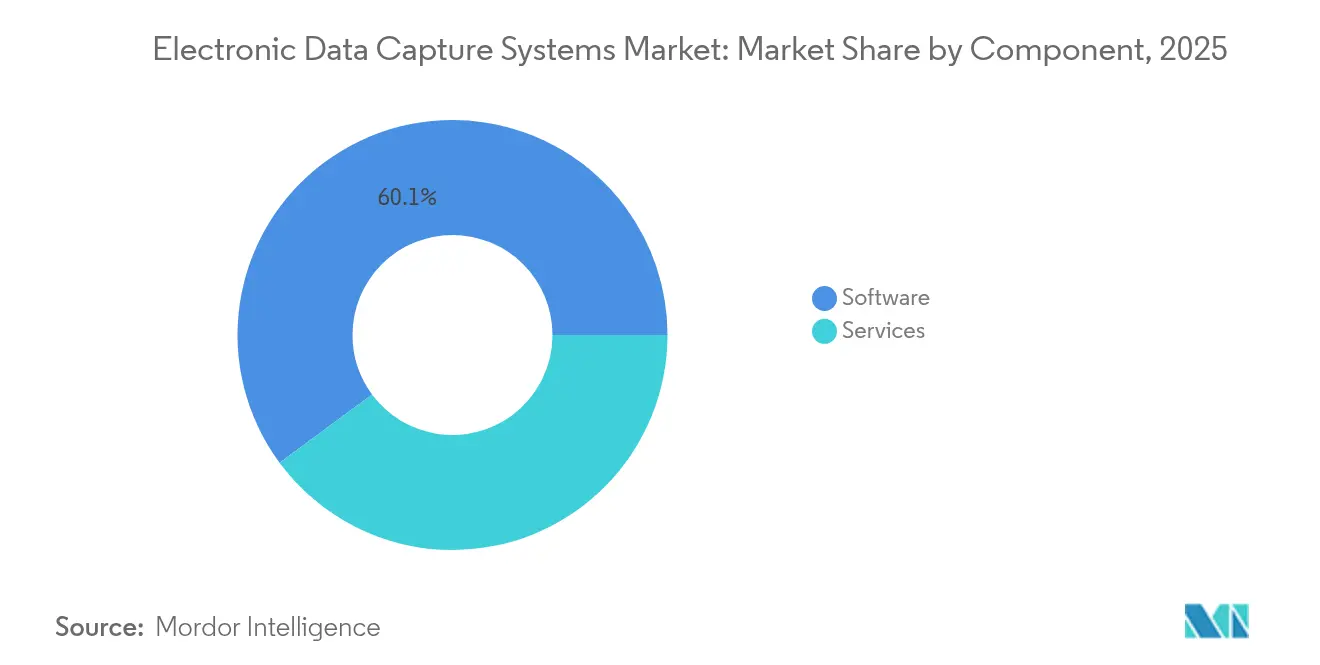

- By component, software led with a 60.12% revenue share in 2025 while services are forecast to expand at a 14.03% CAGR to 2031.

- By delivery mode, web and cloud-based solutions commanded 89.10% of the Electronic Data Capture Systems market share in 2025 and are positioned for a 15.62% CAGR through 2031.

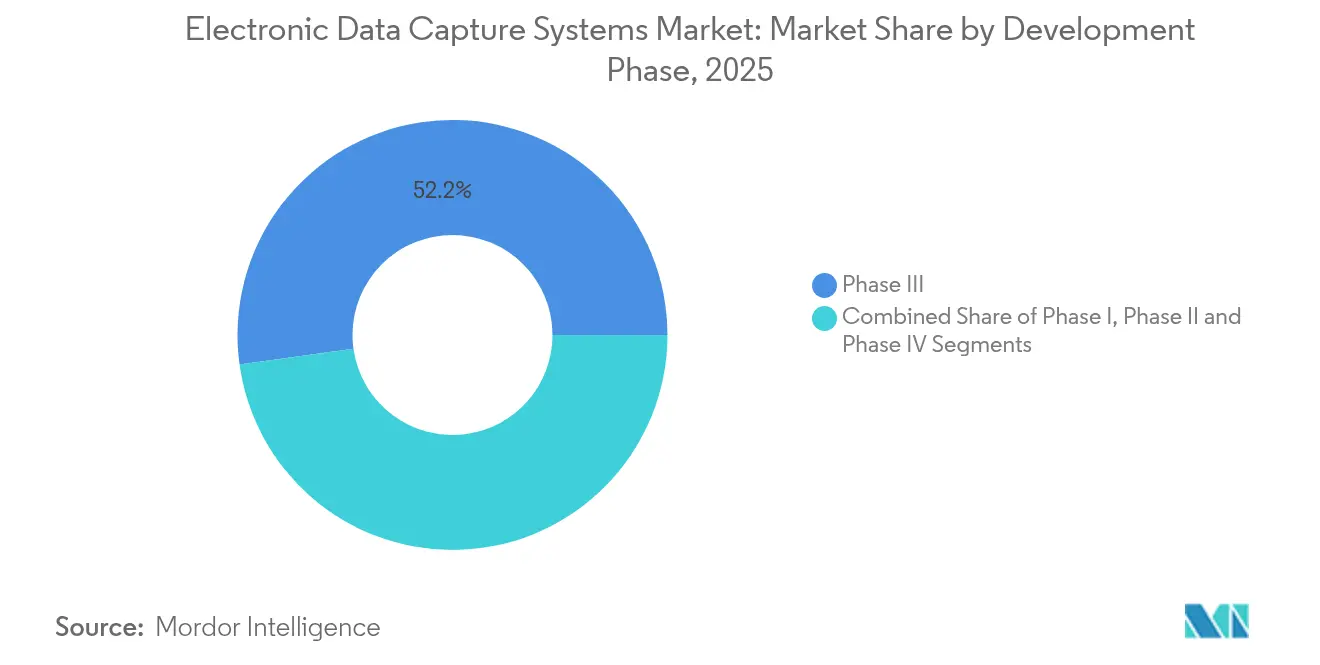

- By development phase, Phase III applications captured 52.20% of the Electronic Data Capture Systems market size in 2025; Phase IV is projected to grow at 13.44% CAGR between 2026-2031.

- By end user, Contract Research Organizations held 37.65% share of the Electronic Data Capture Systems market in 2025, while hospitals and academic sites are set for a 14.52% CAGR to 2031.

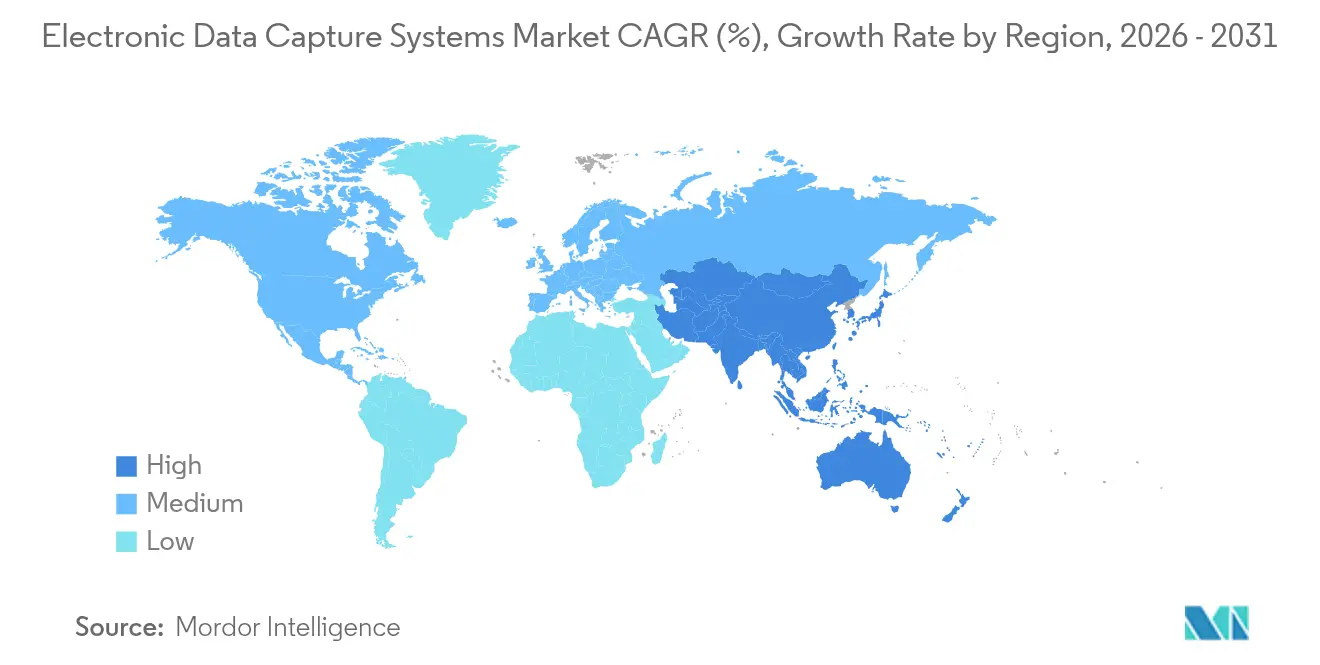

- By geography, North America accounted for 48.10% revenue share in 2025; Asia-Pacific is the fastest-growing region with a projected 15.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electronic Data Capture Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Decentralized & Hybrid Clinical-Trial Models | +2.5% | Global, with early adoption in North America & Europe | Medium term (2-4 years) |

| Rising Data-Volume & Complexity In Protocol Design | +1.8% | Global, concentrated in major pharmaceutical hubs | Long term (≥ 4 years) |

| Stringent Global Data-Integrity & GxP Compliance Mandates | +1.2% | Global, led by FDA and EMA jurisdictions | Short term (≤ 2 years) |

| Accelerated Adoption Of AI-Ready EDC Architectures | +1.5% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Integration Of Synthetic-Patient Data To Reduce Recruitment Cycles | +1.0% | North America & Europe, pilot programs in Asia-Pacific | Long term (≥ 4 years) |

| Tokenization-Based Privacy Layers Enabling Real-World-Data Capture | +0.8% | Global, with regulatory variations by region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Decentralized & Hybrid Clinical-Trial Models

Decentralized trials reshape EDC workflows by shifting data collection to patients’ homes, making mobile-first functionality essential. FDA guidance on digital health technologies published in 2024 triggered rapid uptake of platforms capable of real-time data synchronisation across remote sites. Solutions such as Medidata’s Site Insights Program illustrate how modern EDCs capture and validate streaming data from wearables while providing sponsors with instant study visibility[1]“Medidata Launches the Site Insights Program,” Medidata Solutions, medidata.com. Built-in telehealth modules reduce site burden and improve query resolution rates, driving measurable efficiency gains. Broader adoption also elevates the need for predictive analytics to track recruitment and retention across distributed cohorts. Vendors that couple EDC, eConsent, and patient-engagement tools within one interface are positioned to capture additional spend as sponsors seek unified trial-execution environments.

Rising Data-Volume & Complexity In Protocol Design

Next-generation protocols incorporate genomic sequences, imaging archives, and real-world health-record feeds, multiplying data volume far beyond traditional designs. Modern EDC architectures therefore require elastic cloud scaling and native support for high-throughput formats. Compliance with CDISC standards is mandatory, yet sponsors now demand AI-enabled anomaly detection that flags outliers in near real time. AstraZeneca’s generative-AI initiatives showcase the shift toward automated documentation and advanced analytics pipelines. Adaptive designs further complicate matters, as mid-study amendments must propagate instantly without jeopardizing audit trails. Collectively, these factors consolidate demand around enterprise-grade, cloud-native EDC ecosystems.

Stringent Global Data-Integrity & GxP Compliance Mandates

Following several well-publicised misconduct cases, regulators heightened scrutiny of computerised systems. Updated FDA guidance on Part 11 validation and EMA directives require demonstrable controls across all electronic records. Vendors now embed automatic jurisdiction-specific validation templates and blockchain-based audit immutability to satisfy inspectors. Cyber incidents at prominent research organisations hastened calls for real-time monitoring and layered encryption. GxP obligations now extend to every integrated module—from wearables to laboratory feeds—forcing platform providers to certify entire interface ecosystems rather than isolated databases.

Accelerated Adoption Of AI-Ready EDC Architectures

Sponsors deploy AI for patient identification, protocol feasibility, and risk-based monitoring. Tempus’ acquisition of Deep 6 AI underscores demand for EDCs able to query electronic health records in natural language and ingest structured outputs instantly. Machine-learning models embedded within cloud EDCs predict enrolment bottlenecks and automate deviation management, slashing cycle times. Early adopters leverage large language models to generate draft CSRs minutes after database lock, accelerating regulatory submission. Seamless integration with hyperscale-cloud AI services keeps total cost of ownership manageable while enabling continual tool upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation & Validation Costs | -1.5% | Global, particularly impacting smaller research sites | Short term (≤ 2 years) |

| Persistent Cybersecurity & Privacy-Breach Concerns | -1.2% | Global, with heightened concerns in North America & Europe | Medium term (2-4 years) |

| Limited Interoperability With Next-Gen Wearable / DHT Endpoints | -0.8% | Global, with technical challenges varying by device ecosystem | Medium term (2-4 years) |

| Vendor Lock-In & Long-Term Total-Cost-Of-Ownership Risk | -0.7% | Global, particularly affecting mid-size pharmaceutical companies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation & Validation Costs

Total EDC deployment expenses range from USD 500,000 to USD 2 million once validation, staff training, and system integration are counted, placing a disproportionate burden on small research sites. Validation timelines commonly stretch 6–18 months as teams execute exhaustive test scripts to comply with Part 11 and Annex 11. Rising cybersecurity requirements pushed costs 30% higher since 2024, even as subscription pricing for software itself moderates. Software-as-a-Service models relieve capital outlay but still demand resource-intensive data migration and user uptake programs, prompting some academic centres to postpone upgrades or adopt limited-function tools.

Persistent Cybersecurity & Privacy-Breach Concerns

Healthcare data breaches averaged USD 10.93 million per incident in 2025, with clinical trial records fetching premium valuations on illicit markets. The integration of wearable feeds and patient-engagement apps widens the attack surface, compelling sponsors to mandate rigorous penetration testing and cyber-insurance coverage. Cloud deployment offers advanced security frameworks yet raises data sovereignty questions, especially in multi-jurisdiction trials. Advanced persistent threat groups increasingly target trial endpoints, recognising the financial and public health leverage tied to programme delays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Growth Outpaces Software Maturity

Software retained a 60.12% share of the Electronic Data Capture Systems market in 2025, anchored by multi-year subscription contracts that fund steady enhancements. Services, however, are tracking a 14.03% CAGR as sponsors rely on specialised consultants for configuration, validation, and ongoing optimisation. The Electronic Data Capture Systems market size attributable to service engagements is expanding fastest in Asia-Pacific, where local language support and regulatory guidance are crucial. Growth also stems from AI-related data-science projects that demand bespoke algorithm tuning and customised dashboard development. Software revenue growth moderates as competition intensifies and price transparency improves, yet recurring cloud fees still underpin vendor profitability.

Demand for services accelerates when organisations migrate from legacy paper or first-generation EDC tools toward integrated, AI-ready platforms. Pharmaceutical firms now view implementation partners as change-management advisors who ensure site adoption and streamline SOP alignment. Vendors bundle managed-service offerings that cover data-migration utilities, automated user provisioning, and continuous training, creating sticky revenue streams. The Electronic Data Capture Systems market share of pure-play service providers rises as sponsors outsource complex integration of patient-reported outcome measures and real-world evidence feeds. This shift fosters partnerships between platform vendors and CRO-affiliated consultancies, blurring traditional boundaries between software and services.

By Delivery Mode: Cloud Dominance Drives Digital Transformation

Web and cloud delivery accounted for 89.10% of the Electronic Data Capture Systems market in 2025 and is advancing at a 15.62% CAGR. Sponsors embrace SaaS architectures for rapid deployment, automated upgrades, and elastic compute capacity. The Electronic Data Capture Systems market size attached to on-premise installations is diminishing as data-protection officers and regulators acknowledge enhanced cloud security certifications. Multi-tenant models enable vendors to roll out AI modules and therapeutic-area accelerators simultaneously to all clients, sharply reducing upgrade lag

Ongoing demand for direct EHR-to-EDC integration cements cloud leadership by allowing secure APIs to hospital systems without complex VPNs. Regional data-residency requirements are addressed through zonal hosting, avoiding the capital expenditure of local server farms. Cloud-native platforms also deliver near-instant disaster-recovery fail-over, an increasingly critical contract stipulation following recent ransomware events. This operational resilience strengthens buyer confidence and reinforces the sector’s transition away from on-premise models.

By Development Phase: Phase IV Growth Reflects Real-World Evidence Focus

Phase III trials represented 52.20% of 2025 applications, mirroring their pivotal role in regulatory submissions. Still, Phase IV post-market studies boast a 13.44% CAGR, the fastest within the Electronic Data Capture Systems market. Rising pharmacovigilance expectations force sponsors to capture long-term safety and effectiveness data from routine clinical care. Regulators now encourage label expansion based on robust real-world datasets, pushing EDC platforms to interface seamlessly with electronic health records. The Electronic Data Capture Systems market size for Phase IV is poised to widen further as tokenised data pipelines reduce patient-privacy risk while enabling passive outcome monitoring.

Growth in earlier phases remains steady. Adaptive Phase I designs require flexible forms and real-time dosing adjustments, while biomarker-oriented Phase II studies integrate laboratory and genomic feeds that demand high-frequency data-quality checks. Unified EDC architectures capable of supporting every phase throughout a product’s lifecycle deliver cost efficiencies and simplify vendor management.

By End User: Hospital Growth Challenges CRO Dominance

Contract Research Organizations retained 37.65% of revenue in 2025, leveraging established expertise to win full-service outsourcing contracts. Hospitals and academic sites, however, are forecast to register a 14.52% CAGR, the quickest pace across end users. The Electronic Data Capture Systems market share among healthcare institutions grows as integrated research-care models seek EDC platforms tied directly to resident EHR systems, lowering duplicate data entry. Sponsors also favour hospital networks for real-world patient access, driving direct licensing to research-active sites.

Academic centres provide fertile ground for pilot deployments of AI-driven functionality. Their early-adopter status accelerates vendor feedback loops and sparks co-development partnerships. Meanwhile, pharmaceutical and biotech sponsors continue upgrading enterprise licences but at more measured growth rates as adoption plateaus. Mid-size biotechs increasingly rely on CRO-hosted EDC environments to avoid internal buildouts, sustaining CRO volume even as hospitals gain ground.

Geography Analysis

North America led with 48.10% revenue share in 2025 owing to a proactive regulatory stance, the world’s largest sponsor base, and deep venture funding for clinical-tech start-ups. FDA draft guidance on AI and decentralised trials catalysed wider rollout of cloud platforms able to manage hybrid designs. Integration initiatives such as Epic’s AI extensions give hospitals direct access to EDC-ready data streams, further lifting adoption. Private capital continues to flow into enabling technologies, exemplified by Validose’s USD 2 million seed round for AI-powered adherence devices that feed study databases. Rising cyber-threat awareness fuels demand for advanced security certifications, yet supportive regulation and robust infrastructure ensure sustained growth.

Asia-Pacific is the fastest-growing region at a projected 15.63% CAGR. China and India dominate volume through large treatment-naïve populations and progressively streamlined approval pathways. Local cloud availability zones lower latency and satisfy emerging data-sovereignty laws, helping multinationals deploy global studies with minimal configuration changes. Japan and South Korea add momentum through high digital-health literacy and early uptake of AI-enabled analytics. Government incentives, including China’s accelerated review procedures for innovative therapies, encourage sponsors to shift trial conduct eastward, driving EDC demand.

Europe shows steady expansion underpinned by EMA harmonisation and enforced transparency via the Clinical Trials Regulation. GDPR raises the compliance bar, prompting sponsors to favour vendors with demonstrable privacy-by-design features. Brexit-related complexities are easing as UK authorities align submissions with EU standards, preserving cross-border study feasibility. Sophisticated academic networks spur pilot work on AI-assisted data review, and cloud EDC usage climbs despite pockets of scepticism about extra-regional hosting. Vendors accommodate these sensitivities with selectable data-residency and encryption-key-management options.

Competitive Landscape

The Electronic Data Capture Systems market remains moderately fragmented yet consolidating. Medidata Solutions, Oracle Health Sciences, and IQVIA anchor the top tier by bundling EDC with randomisation, patient engagement, and real-world evidence modules. Cloud-native challengers such as Clinical Ink emphasise mobile-first interfaces and AI integration to win greenfield studies[3]“Clinical Ink Launches EDC Platform,” Clinical Trials Arena, clinicaltrialsarena.com. Competitive differentiators increasingly revolve around low-code form builders, automated SDV-risk scoring, and tokenisation frameworks that facilitate secure linkage to longitudinal data.

M&A activity accelerates. The Suvoda-Greenphire merger couples interactive response technology with financial services to streamline participant reimbursements. eClinical Solutions secured growth capital from GI Partners to scale its intelligent data-analytics engine. Vendors also pursue therapeutic-area specialisation; EDETEK’s oncology accelerator exemplifies how domain-specific templates shorten study start-up times. Strategic alliances with EHR vendors and wearables manufacturers expand ecosystem reach, while smaller players differentiate by offering flexible modules that integrate into sponsor-preferred stacks. Pricing pressure persists as buyers compare total cost of ownership across expanding vendor short-lists.

Electronic Data Capture Systems Industry Leaders

Oracle Health Sciences

IQVIA

Medidata Solutions (Dassault Systemes)

Amazon Web Services (AWS)

IBM Clinical Development

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Clearmind Medicine Inc. launched its Electronic Data Capture (EDC) system to support its Phase I/II trial of MEAI-based therapy for Alcohol Use Disorder.

- March 2025: IgniteData, Memorial Sloan Kettering, and AstraZeneca initiated full deployment of the Archer EHR-to-EDC automation tool in a Phase III oncology study.

Global Electronic Data Capture Systems Market Report Scope

As per the scope of the report, electronic data capture systems assist in data collection, storage, and security in clinical studies.

The electronic data capture systems market is segmented by delivery mode, development stage, end-user, and geography. By delivery mode, the market is segmented into web and cloud-based and on-premises. By development stage, the market is segmented into phase l, phase ll, phase ll, and phase lV. By end user, the market is segmented into pharmaceutical and biotechnology firms, hospital providers, contract research organizations, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the values (USD) for all the above segments.

| Software |

| Services |

| Web- & Cloud-Based |

| On-Premise |

| Phase I |

| Phase II |

| Phase III |

| Phase IV |

| Pharmaceutical & Biotechnology Firms |

| Contract Research Organisations (CROs) |

| Hospitals & Academic Sites |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Delivery Mode | Web- & Cloud-Based | |

| On-Premise | ||

| By Development Phase | Phase I | |

| Phase II | ||

| Phase III | ||

| Phase IV | ||

| By End User | Pharmaceutical & Biotechnology Firms | |

| Contract Research Organisations (CROs) | ||

| Hospitals & Academic Sites | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the Electronic Data Capture Systems market?

The market reached USD 2.08 billion in 2026 and is forecast to hit USD 3.64 billion by 2031 at a 11.86% CAGR.

Which deployment mode is growing fastest?

Web and cloud-based solutions dominate with 89.10% share in 2025 and are projected to expand at a 15.62% CAGR.

Why are Phase IV studies boosting EDC demand?

Regulators require real-world evidence for safety and effectiveness, driving a 13.44% CAGR for Phase IV EDC use between 2026-2031.

Which region offers the strongest growth opportunity?

Asia-Pacific leads with a forecast 15.63% CAGR, propelled by large patient pools and supportive regulatory reforms.

What is the main barrier to wider EDC adoption at small research sites?

High implementation and validation costs remain the primary obstacle, with total deployment expenses ranging up to USD 2 million.

Page last updated on: