Global Healthcare Cloud Based Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

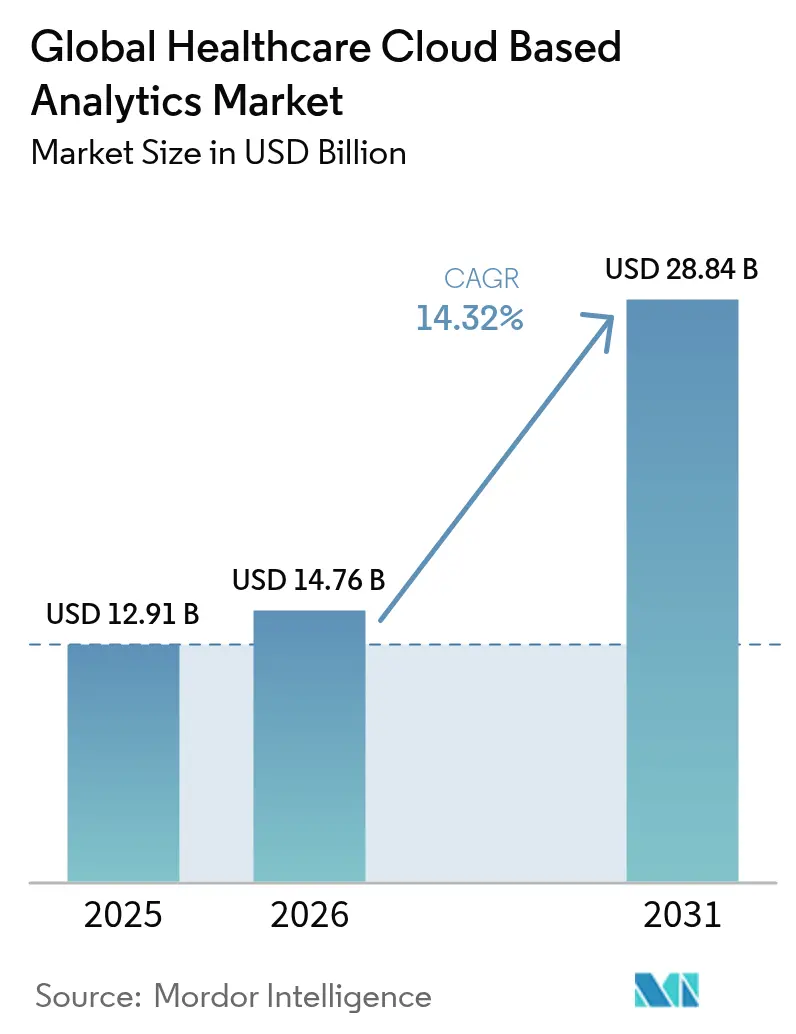

| Market Size (2026) | USD 14.76 Billion |

| Market Size (2031) | USD 28.84 Billion |

| Growth Rate (2026 - 2031) | 14.32% CAGR |

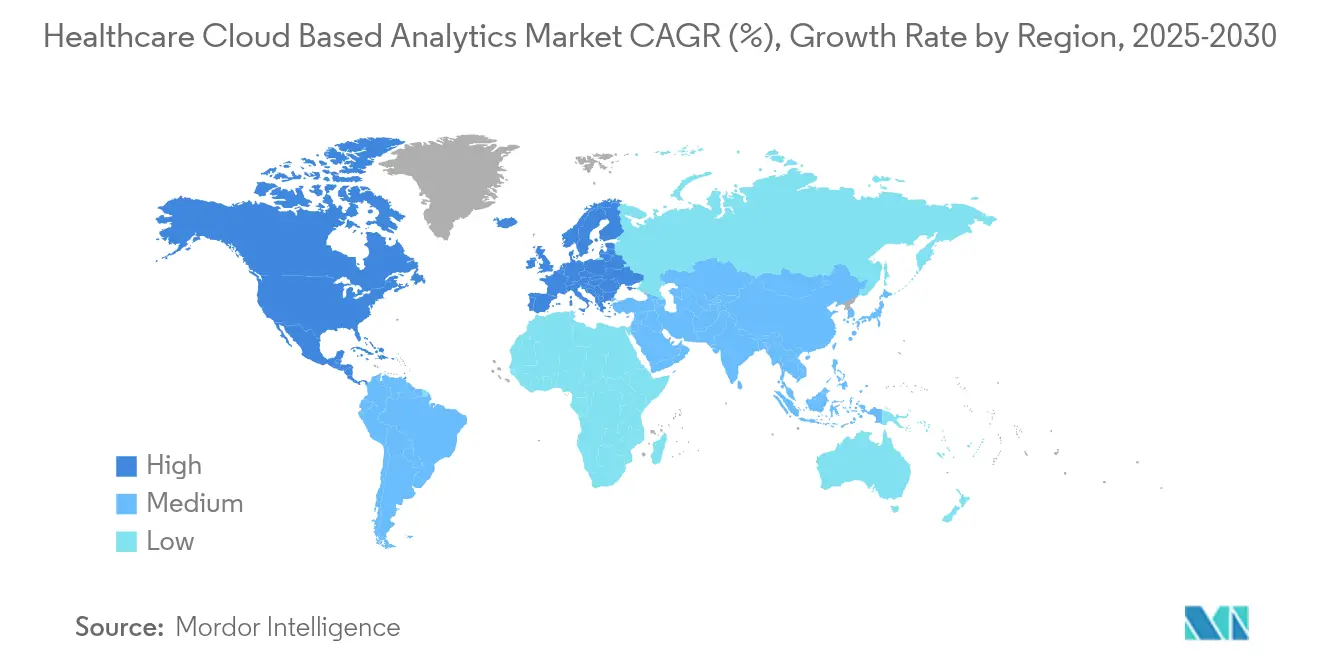

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Healthcare Cloud Based Analytics Market Analysis by Mordor Intelligence

The Healthcare cloud-based analytics market size is expected to grow from USD 12.91 billion in 2025 to USD 14.76 billion in 2026 and is forecast to reach USD 28.84 billion by 2031 at 14.32% CAGR over 2026-2031. Heightened pressure to prove measurable outcomes, surging volumes of digital patient information, and a decisive shift toward value-based reimbursement are accelerating investment in cloud-native analytics across hospitals, payers, and life-science sponsors. Regulatory mandates such as the 21st Century Cures Act, rapid telehealth adoption that funnels fresh data into clinical systems, and the promise of substantial infrastructure savings strengthen the economic rationale for cloud deployment. Providers that embraced cloud migration recorded infrastructure cost reductions of up to 95% in large-scale projects, demonstrating the fiscal appeal of elastic, on-demand computing. Talent shortages and intensifying cyber-risk temper momentum but simultaneously create white-space opportunities for vendors that bundle managed services with robust security architectures.

Key Report Takeaways

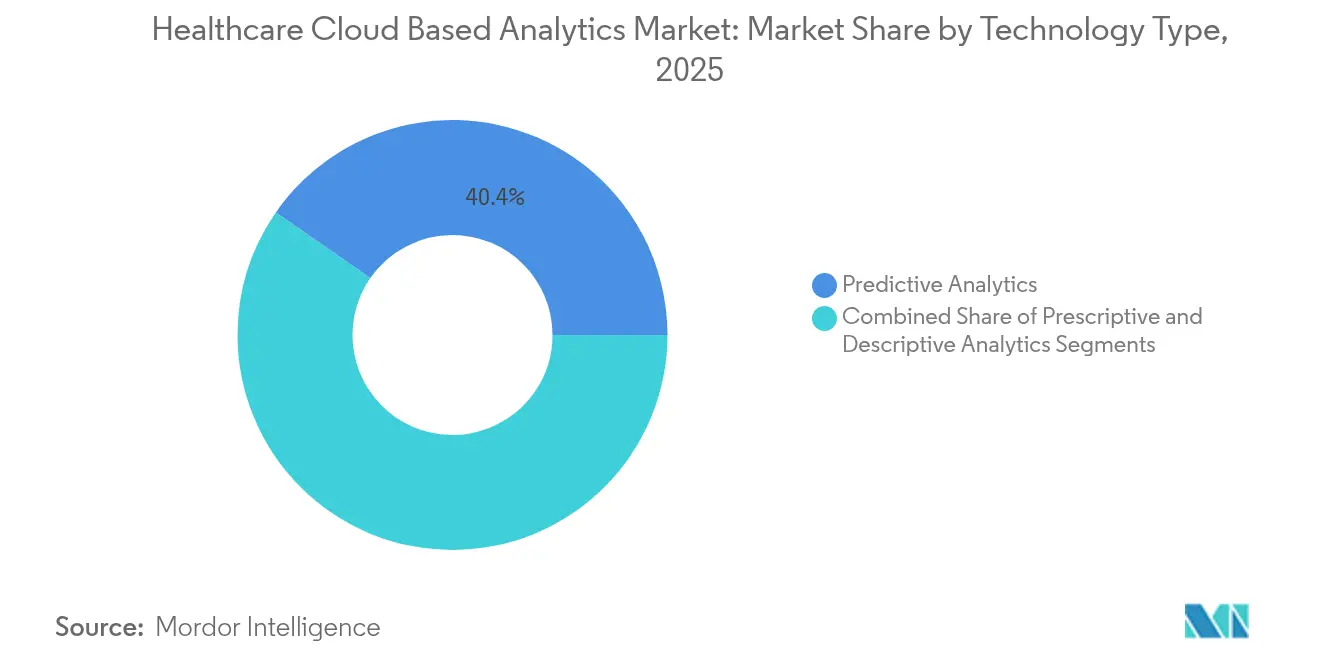

- By technology type, predictive analytics held 40.35% of the Healthcare Cloud-Based Analytics market share in 2025, while prescriptive analytics is projected to grow at a 15.62% CAGR to 2031.

- By application, clinical analytics commanded 45.08% of the Healthcare Cloud-Based Analytics market in 2025; population health management is expanding at a 16.88% CAGR through 2031.

- By component, software platforms led with a 50.12% revenue share in 2025, whereas services are set to advance at a 15.48% CAGR during the forecast period.

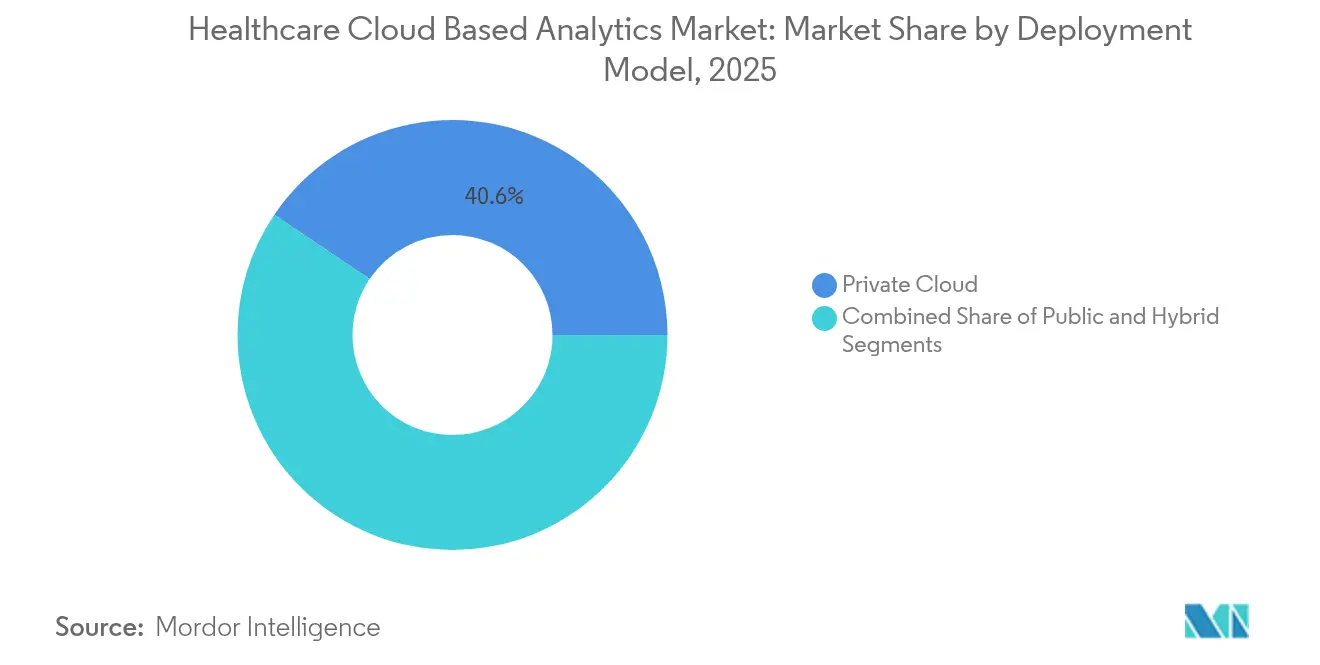

- By deployment model, private cloud deployments accounted for 40.55% of the Healthcare Cloud-Based Analytics market share in 2025, and hybrid cloud usage is poised for a 19.1% CAGR to 2031.

- By end-user, healthcare providers contributed 46.78% of the Healthcare Cloud-Based Analytics market size in 2025, while life sciences and CROs are forecast to rise at a 19.35% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Global Healthcare Cloud Based Analytics Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data explosion from digital health records | +3.20% | Global, North America leading | Medium term (2-4 years) |

| Transition to value-based care reimbursement | +2.80% | North America first, Europe next | Long term (≥ 4 years) |

| Cost efficiency and elasticity of cloud infrastructure | +2.10% | Global, cost-sensitive markets | Short term (≤ 2 years) |

| Government mandates for healthcare interoperability standards | +1.90% | North America & EU | Medium term (2-4 years) |

| Telehealth expansion generating continuous patient data streams | +1.70% | Global, APAC and North America | Short term (≤ 2 years) |

| Adoption of FHIR and open API ecosystems enabling cross-provider analytics | +1.50% | North America & EU expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data Explosion from Digital Health Records

Nearly every U.S. hospital (96%) and more than three-quarters of ambulatory physicians (78%) now run certified electronic health record (EHR) systems. The torrent of structured, semi-structured, and unstructured information overwhelms legacy servers yet fuels demand for cloud-hosted analytic engines that sift text, images, waveforms, and streaming telemetry. Natural-language processing converts physician notes into usable data, while machine-learning pipelines uncover patterns that inform readmission prevention and staffing optimization. By blending genomic profiles, wearable metrics, and social determinants, providers compose granular patient portraits that underpin precision medicine and community-wide interventions.

Transition To Value-Based Care Reimbursement

As per the Centers for Medicare & Medicaid Services, all Medicare beneficiaries are slated to receive care under value-based models by 2030, a shift that rewards quality over volume.[2]Centers for Medicare & Medicaid Services, “Innovation Center Strategy Refresh,” cms.govProviders, therefore, require real-time cohort visibility, risk scoring, and predictive alerts to avoid costs. Organizations participating in advanced payment arrangements have already shaved USD 28 million from annual spending through timely analytics-driven interventions, underscoring the fiscal upside of cloud scalability. As accountable-care participation widens in Europe, continual performance tracking becomes indispensable for both public and private systems.

Cost Efficiency and Elasticity of Cloud Infrastructure

Healthcare entities budget an average annual cloud spend of USD 38 million, outspending most industries yet still realizing double-digit operating savings through automation and usage-based pricing. Elastic scaling lets radiology groups cut imaging compute costs by 30% while boosting diagnostic accuracy. Freed from capital hardware cycles, IT teams experiment with advanced AI workloads without multimillion-dollar server outlays, reinforcing the appeal of native cloud analytics.

Government Mandates for Healthcare Interoperability Standards

The 21stCentury Cures Act outlaws’ information blocking and obliges U.S. providers to adopt standards-based APIs for data sharing. FHIR uptake now spans 84% of hospitals and 61% of clinicians. Similar directives under Europe’s Health Data Space push organizations toward platforms that aggregate multi-source records, monitor compliance automatically, and generate transparent audit trails, further boosting healthcare cloud-based analytics market adoption.[1]Office of the National Coordinator for Health Information Technology, “API and FHIR Adoption Fact Sheet,” healthit.gov

Restraints Impact Analysis of Global Healthcare Cloud Based Analytics Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent data privacy and cyber security threats | -2.30% | Global, regulated markets | Short term (≤ 2 years) |

| Legacy infrastructure and integration complexity | -1.80% | North America & Europe | Medium term (2-4 years) |

| Shortage of cloud-native healthcare data talent | -1.40% | Global | Long term (≥ 4 years) |

| Emerging data sovereignty and carbon-footprint regulations | -1.10% | Europe first, global next | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Data Privacy and Cyber Security Threats

Healthcare recorded 677 major breaches affecting 182.4 million people in 2024, including the ransomware incident that compromised 100 million patient records. Average breach costs reached USD 9.77 million, pressuring providers to invest heavily in encryption, zero-trust architecture, and 24/7 monitoring. Many organizations still lack in-house expertise, prolonging procurement cycles and slightly dampening the healthcare cloud-based analytics market momentum.[3]GovInfoSecurity Media Group, “Healthcare Breach Statistics 2024,” govinfosecurity.com

Legacy Infrastructure and Integration Complexity

Complex, decades-old clinical systems resist cloud connectivity. Data migrations tie up budgets, disrupt workflows, and demand lengthy validation to ensure fidelity. European hospitals contend with fragmented on-premises estates that slow e-Health rollouts and inflate modernization timelines, delaying analytics-first projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Global Healthcare Cloud Based Analytics Market Segment Analysis

By Technology Type:

Predictive Analytics Dominates Current DeploymentsPredictive tools accounted for 40.35% of the healthcare cloud-based analytics market in 2025, highlighting provider appetite for foresight into readmissions, sepsis onset, and staffing needs. Solutions ingest longitudinal EHR records, real-time vitals, and socio-economic markers to trigger proactive care pathways that lift quality scores and compress costs. Integrated dashboards alert multidisciplinary teams to high-risk patients, reducing emergency utilization.

Prescriptive engines, though still nascent, are scaling fastest at a 15.62% CAGR through 2031. These platforms simulate “what-if” scenarios across medication regimens or operating-room throughput and recommend optimal interventions. Decision optimization resonates with health systems seeking continuous margin improvement under value-based contracts, positioning prescriptive modules as the next growth frontier.

By Application:

Clinical Analytics Leads While Population Health AcceleratesClinical analytics captured 45.08% of the 2025 healthcare cloud-based analytics market share because bedside decision support, imaging triage, and drug interactions deliver visible patient benefits. Deep-learning algorithms shorten radiology turnaround times and subtle pathologies, while real-time antimicrobial-stewardship dashboards curb resistance trends.

Population health platforms, expanding at 16.88% CAGR, aggregate claims, pharmacy, and social-needs data to stratify risk and orchestrate community interventions. As capitated payment models proliferate, payers and providers rely on cohort-level metrics to pinpoint gaps in care. Cloud scalability proves vital when crunching thousands of variables across millions of covered lives.

By Component:

Software Platforms Drive Market While Services Expand RapidlySoftware solutions held 50.12% of revenue in 2025 as buyers favored modular platforms that unify data ingestion, quality, and visualization layers. Low-code interfaces let clinicians build ad hoc dashboards without deep SQL skills, boosting frontline adoption. The healthcare cloud-based analytics market size for software will keep expanding as embedded AI accelerators shrink inference times for pathology images and genomic data.

Services revenue is keeping pace, projected at a 15.48% CAGR to 2031, as migration, data governance, and managed-security packages offset staff shortages. Providers lean on third-party experts for HL7 mapping, FHIR API enablement, and continuous model performance auditing, locking in long-term services contracts that complement licensing fees.

By Deployment Model:

Private Cloud Dominates Security-Conscious MarketWith a 40.55% share, private clouds remain favored among risk-averse hospitals that demand single-tenant environments and granular access controls. Dedicated instances satisfy HIPAA, HITECH, and local privacy codes while delivering automated scaling.

Hybrid architectures, forecast to expand 19.1% annually, harmonize on-premises diagnostic gear with public compute bursts for machine-learning training. Oncology centers, for instance, store PET-CT scans locally for latency but offload research analytics to shared GPUs during evenings. This flexible topology balances sovereignty, cost, and performance.

By End-User:

Healthcare Providers Lead While Life Sciences AcceleratesHospitals, integrated delivery networks, and physician groups contributed 46.78% of 2025 revenue because they generate the largest data volumes and are directly accountable for outcomes. Digital command centers synthesize operational metrics, staffing rosters, and patient acuity to optimize bed turnover and reduce boarding times.

Life-science companies and CROs, growing at 19.35% CAGR, reimagine clinical trials by mining real-world data for patient recruitment and safety signal detection. Cloud analytics cuts time-to-insight when screening potential biomarkers or adjudicating adverse-event patterns across global studies, propelling adoption in R&D portfolios.

Geography Analysis

North America Healthcare Cloud Based Analytics Market

North America retains the leading revenue position, supported by near-universal EHR penetration, generous reimbursement for chronic-care management codes, and aggressive federal pushes for interoperability. Health systems shifting entire analytics workloads to hyperscalers report up to 95% cost savings and accelerated AI pilots that automatically draft progress notes. Cyber incidents remain an ever-present hazard, prompting widespread investment in zero-trust frameworks and influencing vendor selection criteria for the healthcare cloud-based analytics market.

Europe Healthcare Cloud Based Analytics Market

Europe records solid double-digit growth as the European Health Data Space mandates cross-border record portability and research reuse. Country-specific rules, such as Germany’s C5 and France’s HDS, spur private-cloud or hybrid strategies that assure data residency. Health ministries allocate digital-transformation grants to tame workforce shortages, tightening cooperation between cloud vendors and public agencies. Integrated health regions leverage federated-learning models to run joint cancer-screening algorithms without exporting raw images, satisfying privacy watchdogs while expanding analytic prowess.

APAC Healthcare Cloud Based Analytics Market

Asia Pacific exhibits the fastest trajectory, propelled by China’s internet-health boom and Southeast Asia’s burgeoning telehealth sector. Government programs in Japan, South Korea, and Singapore subsidize hospital cloud migration and clinical AI pilots to counter aging populations and clinician scarcity. Countries with limited specialist availability deploy remote-read solutions that route imaging studies to off-site radiologists, improving diagnostic reach. Investment momentum from regional technology giants fosters vibrant partnership ecosystems that tailor analytics offerings to local workflows and language nuances.

Regulatory Landscape

Regulation for healthcare cloud-based analytics is increasingly shaped by interoperability mandates, alongside tighter security and privacy compliance requirements for electronic health information. In the United States, the 21st Century Cures Act information-blocking framework and ONC rules continue to push standards-based APIs and FHIR-aligned exchange, which raises requirements for cloud analytics platforms that ingest, normalize, and audit multi-source EHI. ONC also uses the Standards Version Advancement Process (SVAP) to accelerate adoption of updated interoperability standards, with 2026 SVAP voluntary incorporation by certified health IT developers opening from August 29, 2026.

Cybersecurity and privacy enforcement is also tightening. HHS OCR advanced a proposed modification to the HIPAA Security Rule to strengthen cybersecurity protections for ePHI across covered entities and business associates, increasing the compliance bar for cloud-hosted analytics environments and managed service providers. In parallel, the HHS final rule supporting reproductive health care privacy took effect in June 2024, with compliance deadlines extending into February 2026, reinforcing the need for tighter access controls, monitoring, and data-governance capabilities in analytics stacks used for sensitive clinical data.

Competitive Landscape

Industry concentration is moderate. Tech majors like Oracle (Cerner), Optum, IBM (Merative), Microsoft, and Amazon Web Services bundle data warehousing, ML tooling, and domain-specific accelerators into unified suites aimed at regional health systems. Oracle’s USD 28.4 billion Cerner acquisition underscores the strategic value of clinical records, yet integration pace and client expectations present execution risks. Cloud-first challengers such as Arcadia, Datavant, and Health Catalyst emphasize rapid onboarding, API openness, and usage-based subscription models that resonate with midsize hospitals and digital-first payers.

AI infusion has become the main battleground. Leaders differentiate through pretrained medical-language models, radiology-specific computer vision, and automated chart summarization agents. The scarcity of certified cloud analytics professionals motivates providers to outsource operations, benefiting vendors that offer end-to-end managed services with built-in SOC2 monitoring and HITRUST alignment. Strategic partnerships—such as Datavant’s collaboration with AWS Clean Rooms combine hyperscaler security with healthcare-taxonomized data catalogs, broadening addressable use cases from payment integrity to epidemiology.

Regulatory scrutiny tightens around data-sharing deals, fostering interest in federated analytics and synthetic-data engines that limit patient re-identification risk. Vendors able to demonstrate transparent governance, algorithmic fairness, and verifiable carbon-reduction initiatives gain competitive leverage, particularly in European tenders. Overall, innovation cadence and managed-service breadth will be decisive factors in the next wave of Healthcare Cloud Based Analytics market expansion.

Global Healthcare Cloud Based Analytics Industry Leaders

Oracle (Cerner)

Optum

Amazon Web Services

IBM (Merative)

Microsoft

- *Disclaimer: Major Players sorted in no particular order

Global Healthcare Cloud Based Analytics Market Companies Covered in this Report

- Oracle

- Optum

- IBM (Merative)

- Microsoft

- Amazon Web Services

- Google Cloud Platform

- Allscripts (Veradigm)

- SAS Institute

- CitiusTech

- Health Catalyst

- Koninklijke Philips

- HP Enterprise

- Snowflake Inc.

- MedeAnalytics

- Verisk Health

- Mckesson

- Inovalon

- Flatiron Health

- IQVIA Analytics

- Arcadia IO

Read Analysis of Global Healthcare Cloud Based Analytics Companies

Market Opportunities and Future Outlook

Procurement is moving beyond basic migration toward analytics platforms that operationalize AI across clinical, payer, and life-science workflows. This is creating whitespace for vendors that bundle governed data foundations, model operations, and domain-ready applications. In provider IT, WellSpan Health completed a comprehensive migration of its technology portfolio to AWS in January 2026 to enable AI-enabled healthcare solutions across a network serving 1.2 million patients and 250-plus facilities, highlighting demand for cloud analytics layers that can unify data across care settings and support new AI use cases without rebuilding infrastructure. For payers, Optum expanded its collaboration with Google Cloud in April 2026 to advance Optum Real, reinforcing demand for cloud-native analytics that support real-time decisioning and automation under value-based reimbursement.

Life sciences is also pulling the market toward hybrid, high-performance analytics architectures that can handle clinical, imaging, and omics-scale workloads with governed collaboration. Roche deployed a large-scale AI factory in March 2026 using 2,176 NVIDIA Blackwell GPUs across on-premises and cloud infrastructure, reflecting the need for analytics environments that span hybrid compute while maintaining traceability and data controls. In Europe, sovereign and regulated hosting remains a concrete demand driver: Scaleway was selected to support Frances Health Data Hub transition to a sovereign cloud aligned with French HDS requirements, while the EU established the European Health Data Space via Regulation (EU) 2025/327, expanding secondary-use and cross-border access needs and increasing the value of platforms that embed data residency, consent, and auditability into cloud analytics deployments.

Recent Industry Developments in Global Healthcare Cloud Based Analytics Market

- June 2026: Oracle Health partnered with Theator to extend AI into the operating room by integrating surgical intelligence and video analytics with Oracle Cloud Infrastructure. The partnership brings high-volume surgical video and performance signals into cloud analytics workflows, expanding the addressable data types beyond traditional EHR and claims data.

- May 2026: Oracle supported the first clinical trial with the Africa Clinical Research Network using Oracle Clinical One along with safety and analytics applications. This extends cloud analytics penetration in clinical development and supports more standardized data capture and oversight across multi-site studies.

- December 2024: HEALWELL completed the acquisition of Orion Health, strengthening capabilities in health information exchange and cloud-based interoperability. The combination supports broader multi-source data aggregation, which is a prerequisite for scalable population, clinical, and real-world evidence analytics.

Global Healthcare Cloud Based Analytics Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the market covers revenue earned from cloud-based analytics used in healthcare, where clinical, operational, and financial data is turned into usable insights for decisions and reporting. In scope, analytics workloads run on public, private, or hybrid cloud setups.

Scope exclusions: We exclude on-premises-only analytics deployments, and we also exclude general cloud hosting or storage that does not include an analytics layer.

Segments Covered in This Report

- By Technology Type

- Predictive Analytics

- Prescriptive Analytics

- Descriptive Analytics

- By Application

- Clinical Analytics

- Administrative & Financial Analytics

- Population Health & Research Analytics

- Real-World Evidence & Pharmacovigilance

- By Component

- Hardware

- Software

- Services

- By Deployment Model

- Public Cloud

- Private Cloud

- Hybrid Cloud

- By End-user

- Healthcare Providers

- Payers

- Life-Science & CROs

- Public Health Agencies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the base context for cloud adoption in healthcare and to collect steady reference data series that can be checked year over year. We relied on public sources such as the World Health Organization, OECD health statistics, the World Bank, and national health agencies like the US CDC and CMS for utilization, spending patterns, and care delivery indicators that influence analytics demand.

We also reviewed regulator and standards body guidance, such as US FDA materials for software and digital health, plus documentation from cloud security and privacy bodies that shape buying cycles. Alongside this, we used company filings, investor presentations, press releases, and reputable press coverage to map product positioning and likely revenue exposure to cloud analytics. Select paid database subscriptions were used only for company financial intelligence, news screening, and patent visibility to validate timelines and investment intensity. These desk research sources are illustrative, and we also used other public and paid references for cross-checking and clarification.

Primary Interviews and Surveys

Primary work was used to pressure-test the desk assumptions and to convert broad adoption narratives into usable model inputs, including the typical cloud deployment mix, buying triggers, and realistic pricing movement. We spoke with a mix of providers, payers, life sciences users, and implementation specialists across APAC, EMEA, and the Americas, so demand signals were not overly shaped by a single region's reimbursement context or data rules.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 15% | APAC: 46% |

| Mid tier: 55% | Functional/Unit leaders: 42% | EMEA: 34% |

| Smaller Players: 17% | Managers: 43% | Americas: 20% |

Market-Sizing & Forecasting

Market sizing starts with a top-down build where healthcare digital spend signals and cloud uptake indicators are used to reconstruct the likely demand pool for analytics executed in cloud environments, and then filtered by adoption in key care and payer workflows. From there, we corroborated the results using selective bottom-up checks, such as sampled vendor revenue exposure to healthcare analytics, channel feedback on deal sizes, and volume by average subscription value to adjust totals when gaps show up.

The model uses a short list of market fingerprints as inputs, including EHR and claims digitization intensity, cloud deployment preference (public versus private versus hybrid), provider and payer budgeting patterns for data and analytics, data privacy and compliance readiness, and the speed of AI-enabled analytics feature adoption. When the forecast is built, we ran scenario analysis so the base case can be compared against slower or faster cloud migration paths described by our interviewees in their regions. If bottom-up visibility is weak in certain countries, we apply proxy penetration rates from similar health systems, then re-check the output against local spending and digital maturity signals.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent indicators, and then reviewed for year-to-year jumps that do not align with known adoption cycles or regulatory changes. Variance checks are run at the region level, followed by analyst review for pricing, currency timing, or scope mapping issues before sign-off.

Reports are refreshed annually, and interim checks are triggered when material events occur, such as policy shifts, major healthcare cloud security updates, or sharp changes in provider IT spending. Before delivery, we run a final pass to ensure assumptions and the current-year estimate reflect the latest available public signals and feedback from recent re-contacts.

Mordor Intelligence's Global Healthcare Cloud Based Analytics Market Market Size Compared With Other Published Estimates

Published market sizes for healthcare cloud-based analytics can differ even when the topic sounds identical, because each publisher draws the line differently on what counts as analytics revenue and which healthcare users are included. Differences also show up from how currency timing is handled, how fast cloud migration is assumed to be, and whether pricing is treated as steady or improving with AI features.

Some estimates widen the scope to include broader healthcare analytics, or they bundle basic cloud hosting and storage that sits under analytics deployments. In Mordor Intelligence, the value is counted only when an analytics layer is delivered in the cloud (public, private, or hybrid), and on-premises analytics and generic hosting without analytics are left out. This keeps the number tied to a clearer revenue pool.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.91 B (2025) | |

| Industry Publisher A | USD 12.24 B (2025) | Uses a broader, longer-horizon forecast structure with softer checks on what is counted as analytics versus adjacent enablement layers, and it can also apply more conservative cloud migration and pricing progression assumptions. |

| Consultancy B | USD 14.10 B (2025) | Often expands the included revenue pool by folding in nearby healthcare data platform and hosting spend that supports analytics projects, which pushes totals higher even when end-user demand signals look similar. |

The spread across published values is mainly explained by what is bundled into the definition, plus how adoption speed and price growth are treated in the base case. By keeping the model tied to observable deployment mix, healthcare digitalization signals, and repeatable pricing logic, our estimate stays easier to track and update year after year.

Key Questions Answered in the Report

What is the current Global Healthcare Cloud Based Analytics Market size?

The Global Healthcare Cloud Based Analytics Market is projected to register a CAGR of 14.32% during the forecast period (2026-2031)

What is the current size of the Healthcare Cloud Based Analytics market?

The market is valued at USD 14.76 billion in 2026 and is on track to hit USD 28.84 billion by 2031, reflecting 14.32% CAGR.

Which segment holds the largest Healthcare Cloud Based Analytics market share today?

Predictive analytics leads with 40.35% share, owing to strong demand for risk-stratification and readmission-prevention models.

Why are private clouds preferred in healthcare analytics deployments?

Private clouds offer dedicated environments that simplify HIPAA compliance and give hospitals greater control over sensitive patient data, which drove 40.55% share in 2025.

How fast is population health analytics expected to grow?

Population health management applications are projected to expand at a 16.88% CAGR by 2031 as value-based contracts spread.

Which region is the fastest-growing market for healthcare cloud analytics?

Asia Pacific shows the quickest growth path, supported by strong government digitization programs and expanding telehealth adoption.

What are the biggest barriers to wider cloud analytics adoption in healthcare?

Cybersecurity risks, legacy system integration hurdles, and shortages of cloud-savvy data professionals remain the top restraints, together pulling projected CAGR down by roughly 5%.

Page last updated on: