Signal Generator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.89 Billion |

| Market Size (2031) | USD 2.45 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

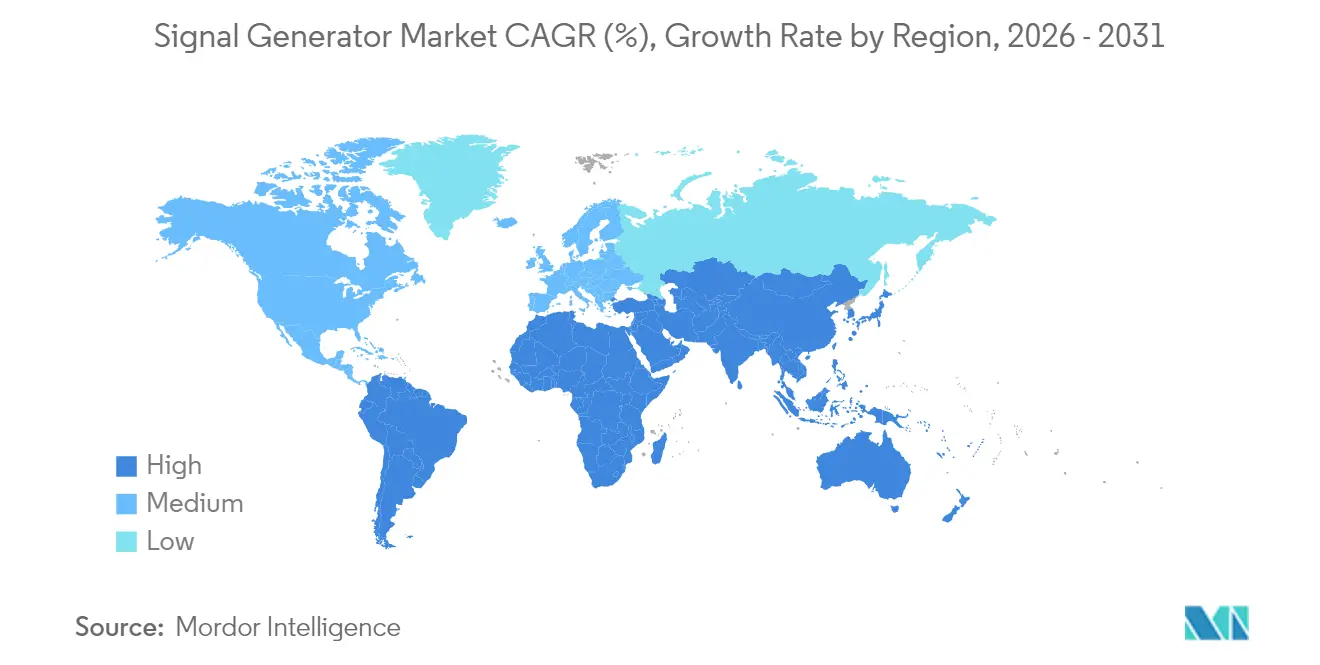

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Signal Generator Market Analysis by Mordor Intelligence

signal generator market size in 2026 is estimated at USD 1.89 billion, growing from 2025 value of USD 1.79 billion with 2031 projections showing USD 2.45 billion, growing at 5.34% CAGR over 2026-2031. This trajectory mirrors the sector’s pivot from traditional RF testing toward demanding 5G infrastructure validation, mmWave automotive radar prototyping, and early quantum-computing research, all of which impose tighter phase-noise, bandwidth, and frequency‐settability requirements on next-generation instruments. Spiraling wafer-fab equipment sales of USD 113 billion in 2024 elevated precision test-gear spend, while China’s plan to surpass 4.5 million 5G base stations in 2025 amplified sub-6 GHz and mmWave generator demand across Asia. North America retained leadership through aerospace-and-defense (A&D) radar modernizations, yet Asia-Pacific delivered the fastest growth as Taiwan and South Korea expanded semiconductor test capacity.

Key Report Takeaways

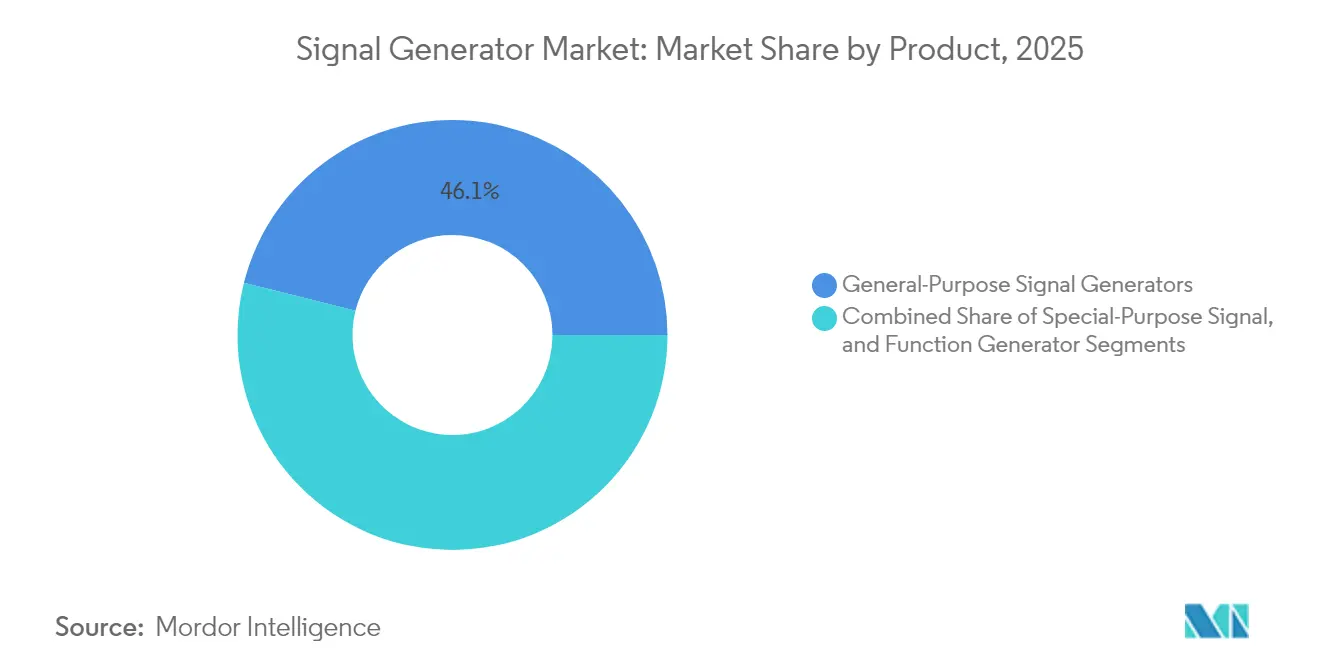

- By product type, general-purpose instruments led with 46.10% of signal generator market share in 2025, whereas vector/arbitrary-waveform units are projected to climb at a 6.85% CAGR to 2031.

- By frequency range, the 3–6 GHz band accounted for 33.70% of the signal generator market size in 2025; the above-12 GHz segment is on track for a 9.12% CAGR through 2031.

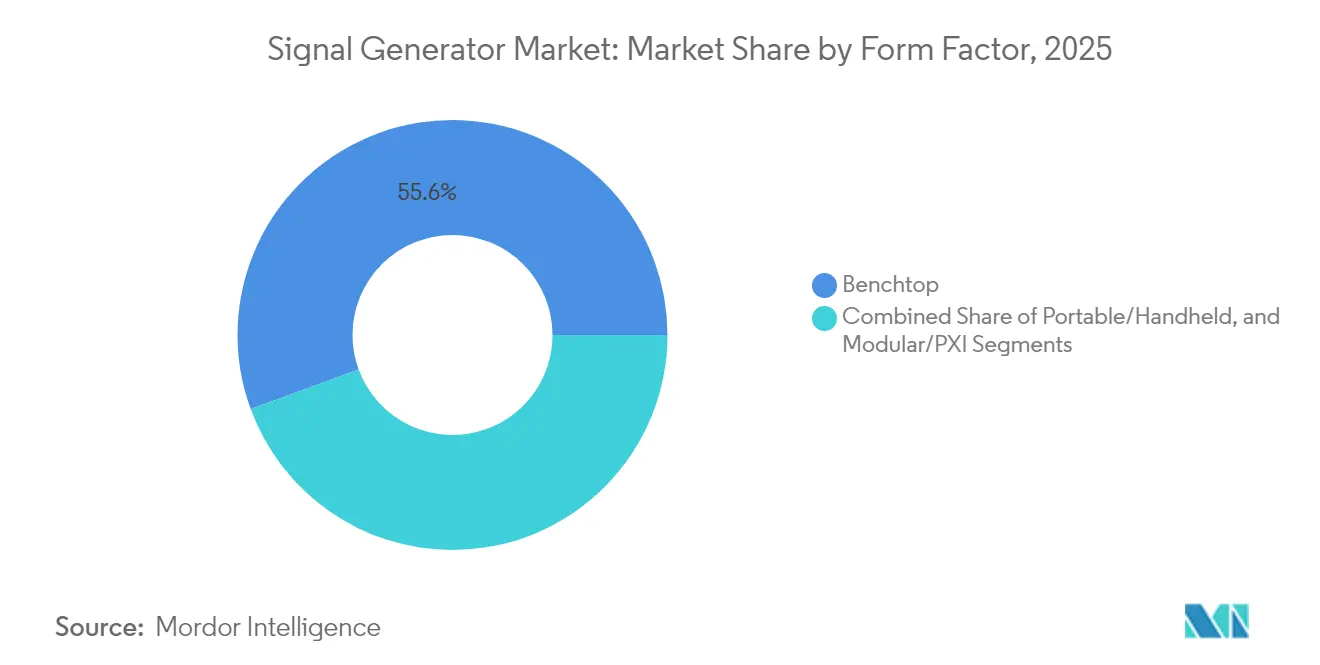

- By form factor, benchtop equipment held 55.60% share of the signal generator market size in 2025, while PXI/modular solutions show the strongest 7.76% CAGR outlook.

- By technology, 4G LTE commanded 36.60% of signal generator market share in 2025; 5G NR is advancing at a 10.05% CAGR through 2031.

- By application, design workflows captured 32.80% of the signal generator market size in 2025, yet the testing segment is pacing for an 8.34% CAGR.

- By end user, telecommunications led with 41.00% share in 2025; automotive is the fastest-growing vertical at 5.61% CAGR to 2031.

- By geography, North America represented 32.10% revenue in 2025, whereas Asia-Pacific is expanding at a 6.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Signal Generator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated 5G base-station roll-outs | +1.2% | Asia-Pacific core, spill-over to North America and EU | Medium term (2-4 years) |

| Radar upgrade programs in A&D | +0.8% | North America, secondary EU | Long term (≥ 4 years) |

| mmWave automotive radar prototyping | +0.7% | Europe core, global auto hubs | Medium term (2-4 years) |

| Semiconductor test expansions | +0.9% | Asia-Pacific, exports worldwide | Short term (≤ 2 years) |

| Quantum-computing research hubs | +0.3% | North America and EU | Long term (≥ 4 years) |

| Middle-East small-sat manufacturing | +0.4% | Middle East, satellite export | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated 5G Base-Station Roll-outs in Asia Requiring High-Frequency Vector Signal Generators

China expects more than 4.5 million live 5G base stations in 2025, up from 4.19 million in 2024, obligating operators to purchase multi-channel vector units that validate sub-6 GHz and mmWave waveforms with tight phase coherence. Each site needs several generators for RF conformance, and the domino effect now extends to India and Southeast Asia, which are fast-tracking open-RAN trials. MIMO and beamforming checks call for wider modulation bandwidths, propelling premium models that cover 3.5–28 GHz. Microwave backhaul, used by 60% of cell sites, pushes additional procurement of high-frequency sources. Consequently, Asia-Pacific is shaping the demand curve for the signal generator market well into the medium term.

Radar Upgrade Programs in North-American A&D Boosting Demand for Above 18 GHz Generators

The U.S. Department of Defense funds GaN-based AESA retrofits, prompting contractors to secure generators capable of 8–54 GHz threat-scenario emulation.[1]Matthew Funaiole et al., “The Need to De-Risk Gallium Material Supply Chains,” Center for Strategic & International Studies, csis.org Keysight’s VXG series, which streams coherent multichannel waveforms up to 54 GHz, typifies the new benchmark. Compounded by electronic-warfare red-team exercises and domestic sourcing mandates, demand for ultra-low phase-noise sources will persist into the next decade, incrementally lifting the signal generator market growth.

mmWave Automotive Radar Prototyping by European Tier-1s Fuels Multi-Channel AWG Sales

European suppliers shifting from 24 GHz to 77-81 GHz ADAS radars need arbitrary-waveform generators with nanosecond-level timing alignment for HIL simulation. Each luxury vehicle can house up to 12 radar sensors, magnifying test-bench requirements. European compliance for interference mitigation further necessitates clean-spectrum outputs, accentuating the uptake of multi-channel 79 GHz platforms. As fleet electrification scales, radar sensor volumes rise, cementing medium-term momentum for the signal generator market.

Semiconductor Test Capacity Expansions in Taiwan and South Korea Driving PXI Modular Units

Taiwanese and Korean fabs plan USD 54.3 billion combined 300 mm-equipment outlays by 2027. Test houses, therefore, install PXI signal sources that synchronize across hundreds of DUT sites for high-throughput characterizations. MPI Corporation already reports three-year order visibility fed by AI workload silicon. The short-term spike in modular platform demand filters globally via equipment exports, providing an immediate tailwind to the signal generator market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Entry-level Chinese benchtop units eroding prices | −0.6% | South America core, global effect | Short term (≤ 2 years) |

| GaAs/MMIC shortages delaying deliveries | −0.8% | Europe primary, global spill | Medium term (2-4 years) |

| EU electromagnetic emission norms | −0.4% | Europe, export impact | Long term (≥ 4 years) |

| RF-test talent shortage | −0.3% | Africa and Oceania | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Entry-Level Chinese Benchtop Units Eroding Prices in LATAM

Chinese vendors leverage post-COVID supply normalization to ship 6 GHz generators at prices 30–40% under Western brands, especially in price-sensitive South America.[2]Frank Cavallaro, “What to Expect in the 2025 Semiconductor Supply Chain,” sdcexec.com Component availability gives them cost levers, pressuring incumbents to defend margins or migrate upmarket. The resulting discounting pulls average selling prices down, trimming near-term revenue growth for the signal generator market.

GaAs/MMIC Shortages Delaying European Deliveries

Beijing’s gallium export curbs hit 98% of global supply, extending MMIC lead times from 16 to 30 weeks for European makers. MACOM’s acquisition of OMMIC seeks to localize wafer supply, yet ramp-up needs 18–24 months. Prolonged shortages risk order deferrals and, by extension, dent the signal generator market over the medium horizon.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: General-Purpose Dominance Amid Vector Innovation

General-purpose instruments accounted for 46.10% of 2025 revenue, underscoring their versatility across RF education, troubleshooting, and legacy wireless protocols. However, vector and arbitrary-waveform units, buoyed by 5G NR’s complex numerologies, will post a 6.85% CAGR and steadily shrink the gap. The signal generator market size for vector products is set to outpace conventional gear as two-box architectures give way to integrated I/Q modulators. Segment leaders now embed digital up-conversion and wide-bandwidth RF chains to span sub-GHz through 40 GHz, allowing one chassis to replace several legacy models.

Software-defined moves, such as Rohde & Schwarz’s SMW200A, which adds mmWave amplifiers via plug-in heads, grant path-to-terahertz upgrades without full capital refresh. Function generators keep a niche in academia, though shrinking price gaps encourage labs to purchase entry-level AWGs instead. Across OEM R&D, twin drivers - time-to-market and reduced rack footprints - sustain demand for hybrid generation-and-analysis benches, reaffirming a premium for accuracy and spectral purity in the signal generator market.

By Frequency Range: mmWave Acceleration Beyond Traditional Bands

The 3–6 GHz block delivered 33.70% of 2025 turnover through sub-6 GHz 5G, Wi-Fi 6E, and industrial IoT use cases. Yet, automotive radar, 5G mmWave backhaul, and satellite uplinks propel frequencies above 12 GHz at a 9.12% CAGR. Dual-path architectures covering DC-to-44 GHz compress multiple instruments into one, simplifying calibration chains.

Photonic techniques - demonstrated by Rohde & Schwarz’s ultra-stable tunable THz sources - extend internal references well past 100 GHz, a prerequisite for 6G trials. GaN front-ends mitigate output-power roll-off, though gallium constraints loom. As instruments flex wider instantaneous bandwidths, traditional band-based segmentation fades, yet procurement budgets still reference historic cutoff points, preserving clarity when allocating spend across the signal generator market.

By Form Factor: Benchtop Resilience Despite Modular Growth

Benchtop systems retained 55.60% share in 2025 thanks to intuitive GUIs, local knobs and rapid bench-top reconfiguration. Teaching labs and early-stage startups continue to favor standalone units over system-embedded modules. Even so, PXI cards will expand at an 7.76% CAGR as fab lines, RF front-end assembly, and board-level production test seek synchronized multichannel sources. The signal generator market size for PXI slots is, therefore, tied closely to semiconductor capex cycles.

Vendors now supply remote web-based control and cloud licensing for benchtop models, blurring boundaries with rack automation. In contrast, handheld demand stays niche - field techs for satellite gateways or small-sat factories require portability but accept narrower specs. For global OEMs, mixed fleets of benchtop for R&D and PXI for production strike the optimal CAPEX/throughput balance.

By Technology: 5G NR Acceleration Amid 4G Persistence

4G LTE accounted for 36.60% of 2025 revenue because many emerging markets still extend LTE coverage and IoT Cat-M deployments. Nonetheless, 5G NR will grow 10.05% annually as operators light up standalone cores, mid-band carrier aggregation, and mmWave fixed-wireless. Instruments must replicate 400 MHz instantaneous bandwidths, 1024-QAM, and FR1/FR2 coexistence in a unified platform, reshaping customer specifications.

Research alliances between Rohde & Schwarz and Qualcomm, validating 13 GHz FR3 links, mark a step toward 6G, prompting vendors to pre-install ultra-wideband D/A paths. Legacy 2G/3G calling for simple GMSK modulation remains profitable only in after-sales spares. Over the decade, tech convergence with Wi-Fi 7 and radar-sensing profiles - hallmarks of 6G ISAC concepts - will further complicate roadmaps, yet they anchor upside for the broader signal generator market.

By Application: Testing Surge Drives Market Evolution

Design benches captured 32.80% of 2025 spend, but regulatory, safety, and interoperability checks now make the testing phase the fastest-growing application at an 8.34% CAGR. Instruments must juggle compliance scripts, automated limit masks, and high-throughput switching, particularly for 77–81 GHz ADAS production lines.

Wafer-level probing uses PXI sources for vector-network sweeps within thermal chambers, linking yield losses directly to signal fidelity gaps. Meanwhile, on-site troubleshooting moves toward cloud-connected handhelds streaming IQ data for remote diagnostics. Each node expands recurring software revenues, improving the value proposition of premium SKUs in the signal generator market.

By End-User Industry: Telecommunications Leadership Amid Automotive Acceleration

Telecommunications retained a 41.00% revenue share in 2025, driven by densification, spectrum refarming, and the adoption of open-RAN conformance labs. Yet automotive electronics will chart a 5.61% CAGR, fuelled by high-resolution radar, V2X, and EV powertrain EMC. ADAS tier-ones require synchronized multi-gigahertz chirps with micro-radian phase repeatability, forcing them to spec premium arbitrary-waveform generators.

A&D customers seek coherent multi-emitters above 40 GHz for EW scenarios, while quantum-computing labs chase sub-100 fs jitter references at microwave carriers of 4-12 GHz. Education and healthcare hold niche demand; medical-imaging device OEMs validate ultrasound or MRI preamps. Universities mirror emerging 6G sub-THz curricula. Broadly, each vertical’s test depth and cadence dictate its proportional pull on the signal generator market.

Geography Analysis

North America held 32.10% of 2025 revenue, buoyed by persistent A&D funding and early 5G roll-outs. U.S. federal budgets back radar upgrades, while Canadian quantum clusters purchase ultra-low-phase-noise gear for superconducting-qubit experiments. Domestic sourcing preferences following tariff regimes favor local vendors, preserving premium pricing.

Asia-Pacific is the fastest-growing region at 6.18% CAGR through 2031. China’s announcement of 4.5 million live 5G macro sites in 2025 guarantees sustained sub-6 GHz vector-generator volume. Taiwan and South Korea will collectively pour more than USD 54 billion into 300 mm fabs by 2027, which will continuously expand PXI slot installations. Government tax credits catalyze local supply-chain clusters, reinforcing a virtuous cycle for the signal generator market.

Europe records steady but slower growth. Automotive radar R&D around Stuttgart, Munich, and Gothenburg anchors high-frequency demand, whereas stricter electromagnetic-emission norms raise test complexity for >20 dBm outputs. Gallium shortages, however, risk delivery delays for 40+ GHz models until on-shore wafer lines come online, marginally damping the regional signal generator market size. The Middle East and Africa, though currently small, invest in sovereign small-sat factories; portable RF sources accompany assembly and launch-site testing, offering upside once launch cadence accelerates.

Competitive Landscape

Industry consolidation escalated in 2024-25: Keysight’s USD 1.46 billion acquisition of Spirent and Emerson’s USD 8.2 billion purchase of National Instruments broadened portfolios from pure-play generation to complete design-verify-optimize stacks. Such a platform embeds common software layers that orchestrate signal source, analyzer, switch, and power-supply functions across benchtop and PXI, locking in customers and elevating switching costs.

Technology differentiation concentrates on phase noise, output flatness, and instantaneous bandwidth. Rohde & Schwarz pushes photonics-based terahertz vectors, while Anritsu’s 70 GHz analog Rubidium focuses on ultra-clean spur levels. Meanwhile, low-cost Chinese entrants capture first-time buyers in emerging markets with 6 GHz benchtops under USD 3,000, fragmenting the low-end. Established brands counter through service passports, calibration hubs, and subscription-based firmware that unlocks future bands, enabling lifecycle monetization.

White-space opportunities surface in quantum-computing readout chains, where -135 dBc/Hz at 10 kHz offset is mandatory, and in O-RAN conformance rigs needing phase-aligned multi-port sources above 7 GHz. Vendors investing in modular phase-noise cancellation and digital-predistortion (DPD) test algorithms are best placed to monetize these growth nodes. Overall, scale, software and spectral purity define competitive advantage in the evolving signal generator market.

Signal Generator Industry Leaders

Keysight Technologies Inc.

Rohde & Schwarz Gmbh & Co Kg

National Instruments Corporation

Teledyne Technologies Incorporated

Anritsu Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Taiwanese tester MPI Corp. reported three-year order visibility tied to AI silicon demand and full capacity utilization.

- May 2025: Rohde & Schwarz and Qualcomm validated 5G NR at 13 GHz (proposed FR3) using the CMX500 one-box tester.

- April 2025: China reached 4.4 million 5G base stations and set a 4.5 million target for 2025.

- March 2025: Keysight closed its Spirent acquisition and divested Spirent’s HSE business to VIAVI.

Global Signal Generator Market Report Scope

A signal generator is an electronic testing instrument that engages in generating repeating or non-repeating waveforms. Signal generators of all types are generally used to design, manufacture, service, and repair electronic devices.

The Signal Generator Market is Segmented by Product (General Purpose Signal Generator, Special Purpose Signal Generator, and Function Generator), Technology (2G, 3G, and 5G - 4G), Application (Designing, Testing, Manufacturing, Troubleshooting, and Repairing), End-user Industry (Telecommunication, Aerospace, and Defense, Automotive, Electronics Manufacturing, and Healthcare), and Geography.

| General-Purpose Signal Generator | RF Signal Generator |

| Microwave Signal Generator | |

| Arbitrary Waveform Generator | |

| Special-Purpose Signal Generator | Video Signal Generator |

| Audio Signal Generator | |

| Pitch Generator | |

| Function Generator | Analog Function Generator |

| Digital Function Generator | |

| Sweep Function Generator |

| Less than 3 GHz |

| 3-6 GHz |

| 6-12 GHz |

| Above 12 GHz (mmWave) |

| Benchtop |

| Portable/Handheld |

| Modular/PXI |

| 2G (GSM, CDMA) |

| 3G (W-CDMA, CDMA2000) |

| 4G (LTE, WiMAX) |

| 5G NR |

| Designing |

| Testing |

| Manufacturing |

| Certification |

| Troubleshooting |

| Repairing |

| Telecommunications |

| Aerospace and Defense |

| Automotive |

| Electronics Manufacturing and Semiconductors |

| Healthcare/Medical Devices |

| Education and Research |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics (Denmark, Sweden, Norway, Finland) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Product | General-Purpose Signal Generator | RF Signal Generator | |

| Microwave Signal Generator | |||

| Arbitrary Waveform Generator | |||

| Special-Purpose Signal Generator | Video Signal Generator | ||

| Audio Signal Generator | |||

| Pitch Generator | |||

| Function Generator | Analog Function Generator | ||

| Digital Function Generator | |||

| Sweep Function Generator | |||

| By Frequency Range | Less than 3 GHz | ||

| 3-6 GHz | |||

| 6-12 GHz | |||

| Above 12 GHz (mmWave) | |||

| By Form Factor | Benchtop | ||

| Portable/Handheld | |||

| Modular/PXI | |||

| By Technology | 2G (GSM, CDMA) | ||

| 3G (W-CDMA, CDMA2000) | |||

| 4G (LTE, WiMAX) | |||

| 5G NR | |||

| By Application | Designing | ||

| Testing | |||

| Manufacturing | |||

| Certification | |||

| Troubleshooting | |||

| Repairing | |||

| By End-User Industry | Telecommunications | ||

| Aerospace and Defense | |||

| Automotive | |||

| Electronics Manufacturing and Semiconductors | |||

| Healthcare/Medical Devices | |||

| Education and Research | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics (Denmark, Sweden, Norway, Finland) | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Southeast Asia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the signal generator market?

In 2026, the signal generator market size is USD 1.89 billion.

How fast will the market grow over the next five years?

Revenue is projected to rise at a 5.34% CAGR, reaching USD 2.45 billion by 2031.

Which region will expand the fastest?

Asia-Pacific shows the highest 6.18% CAGR, fueled by large-scale 5G deployments and semiconductor fab investments.

What product category is gaining momentum?

Vector and arbitrary-waveform generators will post a 6.85% CAGR as 5G, radar and quantum applications demand complex modulation.

Page last updated on: