Africa Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

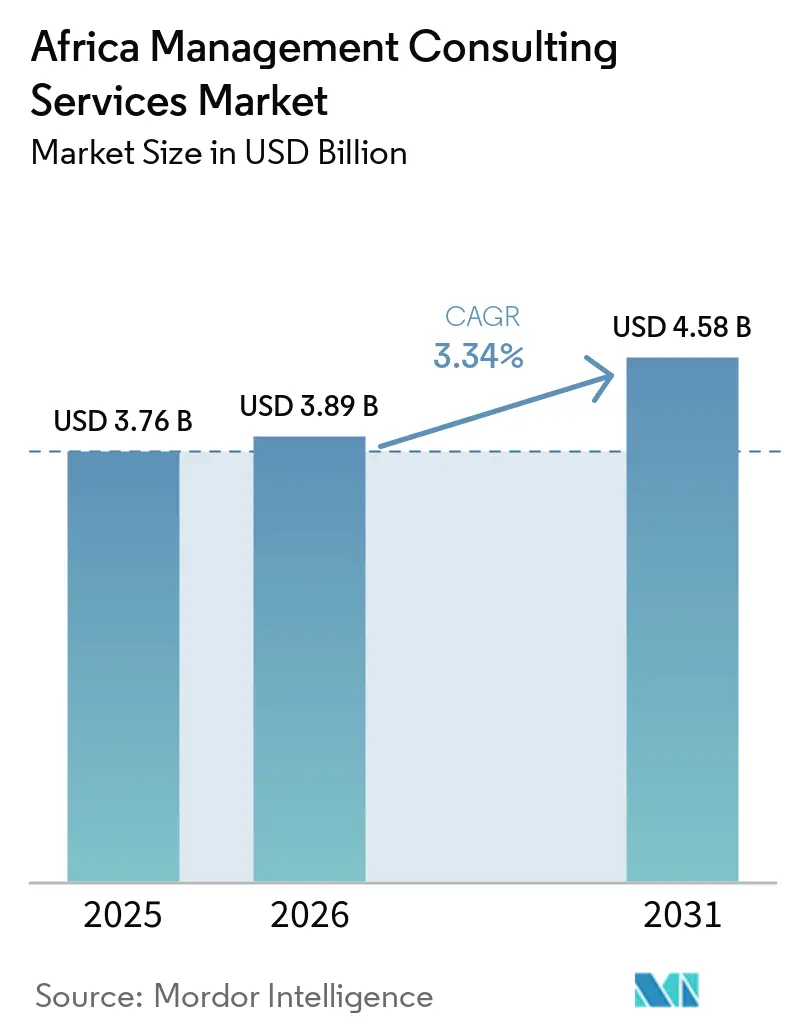

| Base Year Market Size (2025) | USD 3.76 Billion |

| Market Size (2026) | USD 3.89 Billion |

| Market Size (2031) | USD 4.58 Billion |

| Growth Rate (2026 - 2031) | 3.34% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Management Consulting Services Market Analysis by Mordor Intelligence

The Africa management consulting services market size in 2026 is estimated at USD 3.89 billion, growing from 2025 value of USD 3.76 billion with 2031 projections showing USD 4.58 billion, growing at 3.34% CAGR over 2026-2031. Expansion is fueled by continent-wide digital-transformation programs, sweeping state-owned enterprise (SOE) restructuring, and AfCFTA-related cross-border trade facilitation. Infrastructure spending—highlighted by the African Development Bank’s USD 1.5 billion support package for South Africa—continues to anchor consulting demand. Momentum is reinforced by a surge in artificial-intelligence adoption under the African Union Continental AI Strategy, as well as ESG-focused regulatory tightening that compels enterprises to seek governance and sustainability expertise. Currency volatility and talent shortages remain cautionary headwinds, yet the overall trajectory of the Africa management consulting services market remains positive as private and public actors pursue high-impact transformation initiatives.

Key Report Takeaways

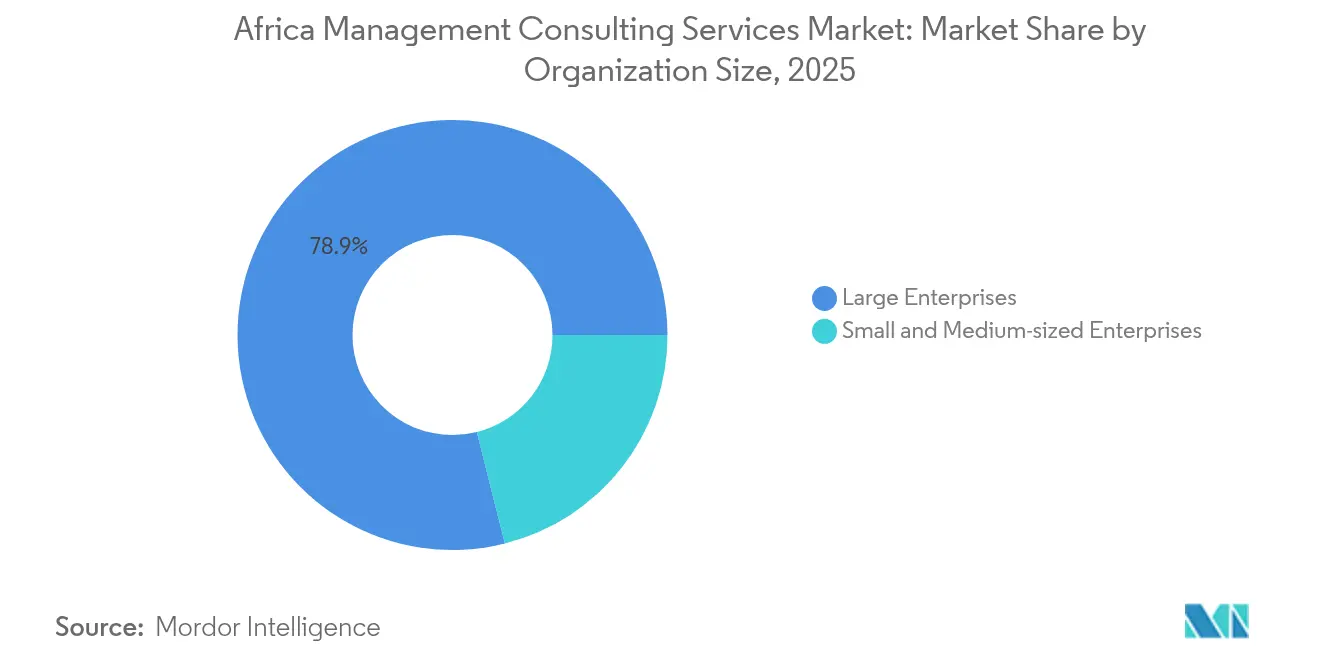

- By organization size, large enterprises held 78.92% of the Africa management consulting services market share in 2025, while small and medium-sized enterprises are advancing at a 4.73% CAGR to 2031.

- By service type, operations consulting led with 34.52% revenue share in 2025; technology consulting is projected to expand at a 6.58% CAGR through 2031.

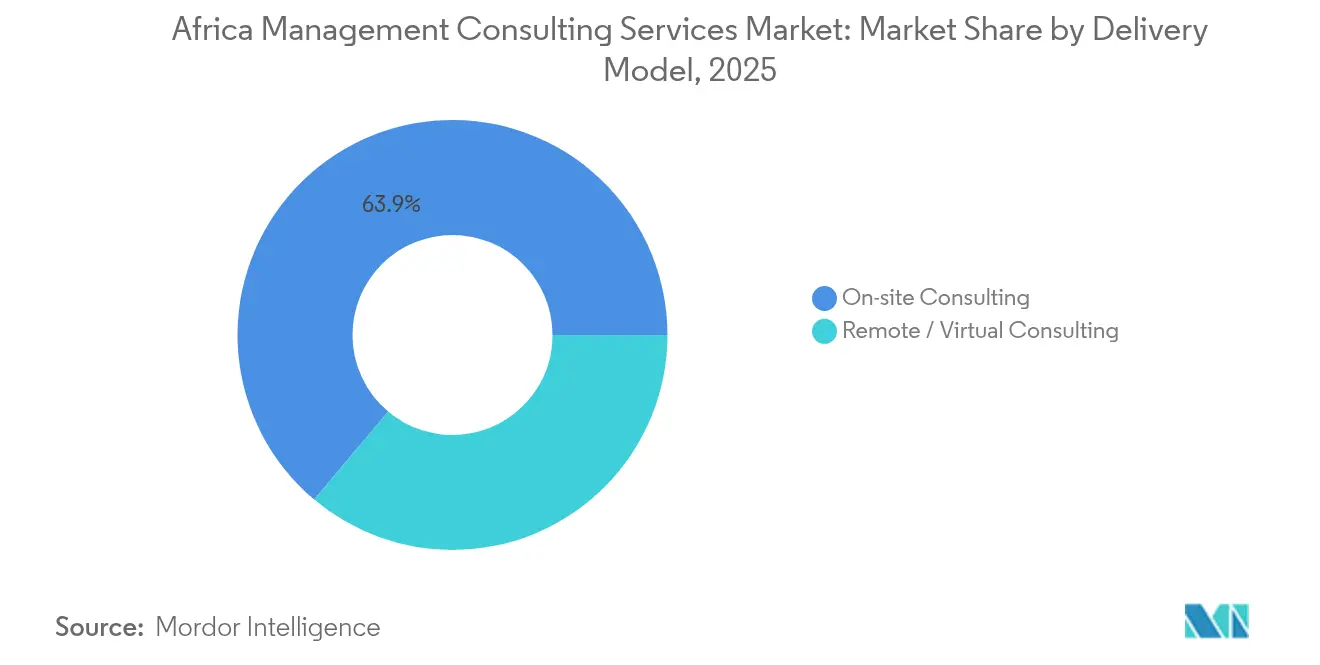

- By delivery model, on-site consulting accounted for 63.88% of the Africa management consulting services market size in 2025, while remote consulting is growing at a 4.03% CAGR to 2031.

- By end-user industry, financial services captured 26.32% share of the Africa management consulting services market size in 2025; healthcare shows the fastest momentum at a 10.47% CAGR through 2031.

- By geography, South Africa contributed 21.05% revenue share in 2025 and is expanding at a 6.05% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-transformation spend surge | +1.2% | South Africa, Nigeria, Egypt | Medium term (2-4 years) |

| Privatization and SOE restructuring wave | +0.8% | South Africa, Nigeria, Egypt | Long term (≥ 4 years) |

| Supply-chain efficiency mandates | +0.6% | Manufacturing hubs | Short term (≤ 2 years) |

| Expanding ESG and data-privacy regulations | +0.5% | South Africa, Nigeria | Medium term (2-4 years) |

| AfCFTA-led cross-border consulting demand | +0.4% | Early adopters | Long term (≥ 4 years) |

| Rise of impact-investment advisory | +0.3% | Infrastructure corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-transformation spend surge

Governments and enterprises are scaling digital-public-infrastructure projects such as identity platforms and instant-payment systems, pushing the Africa management consulting services market toward high-value technology engagements. The African tech economy is expected to reach USD 1.5 trillion by 2030, stimulating demand for AI, cloud, and cybersecurity advisory mandates. [1]David Thomas, “WEF 2025: Africa's $1.5 Trillion Tech Opportunity,” african.business Flagship initiatives include Ghana’s USD 1 billion UAE-backed tech hub and Cassava Technologies’ AI factory in South Africa, each generating multi-disciplinary consulting opportunities. Mobile penetration heading toward 88% by 2030 expands the client base for digital-strategy advisory, while ethical-AI guidance anchored in the AU Continental AI Strategy heightens governance consulting needs.

Privatization and SOE restructuring wave

Large-scale unbundling of utilities, rail, and telecom assets fuels recurring consulting contracts in market-design, regulatory, and operational optimization. Eskom’s separation into transmission, distribution, and generation entities underscores the complexity of these programs. [2]U.S. Commercial Service, “South Africa Energy Eskom Unbundling Update,” trade.gov Nigeria’s banking reforms and South Africa’s USD 1.5 billion World Bank-backed structural-reform loan further enlarge the advisory pipeline.

Supply-chain efficiency mandates

Manufacturing clusters from Ethiopia’s Glo-Djigbé Industrial Zone to Morocco’s automotive corridor require end-to-end supply-chain redesign services. Chinese investment in nine additional cement plants during 2023 and five more in 2024 increases local-integration complexities that favor process-engineering consulting.

Expanding ESG and data-privacy regulations

South Africa’s ESG code, the Alliance for Green Infrastructure’s USD 10 billion pipeline, and Nigeria’s Data Protection Act 2023 anchor compliance-driven consulting demand. International financiers such as the European Investment Bank require robust impact-measurement protocols that consulting firms are uniquely positioned to craft.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent shortage and high consultant churn | -0.7% | Nigeria, South Africa | Short term (≤ 2 years) |

| Currency volatility across key economies | -0.5% | Nigeria, Ghana, Zambia | Medium term (2-4 years) |

| Cyber-risk in remote consulting delivery | -0.4% | Digitally advanced markets | Medium term (2-4 years) |

| Growth of internal consulting units | -0.3% | Large enterprises | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Talent shortage and high consultant churn

A widening skills gap pushes firms to spend heavily on recruitment and upskilling as demand for AI, cybersecurity, and ESG expertise outpaces supply. OECD analysis flags mismatches between curricula and market needs, prompting consulting engagements in vocational-training design. [3]OECD, “More Investment in Skills Development Is Key to Africa's Growth Potential,” oecd.org Elevated turnover rates further erode project continuity, increasing delivery costs and compressing margins.

Currency volatility across key economies

Sharp naira and cedi swings complicate multi-year contract pricing and revenue recognition for cross-border projects. Research on Zambia confirms a negative correlation between exchange-rate instability and GDP growth, echoing client reluctance to sign long-tenor advisory agreements. While hedge mechanisms provide partial relief, inconsistent adoption maintains volatility as a structural restraint.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Organization Size: Large Enterprises Drive Transformation

The Africa management consulting services market size for large enterprises accounted for 78.92% market share in 2025, equating to a 78.92% Africa management consulting services market share. These corporations undertake complex restructuring, digital integration, and ESG-alignment projects that demand multidisciplinary advisory support. Ethiopian Airlines’ USD 7.8 billion Bishoftu airport expansion exemplifies the scale and sophistication of engagements in this segment.

Small and medium-sized enterprises contribute a modest portion of current revenue yet represent the fastest-growing cohort, advancing at 4.73% CAGR to 2031. UNDP programs that coached more than 12,000 MSMEs on AfCFTA readiness illustrate the rising appetite for affordable, outcome-based consulting assignments. Digital self-service toolkits and modular deliverables are enabling consultancies to tap this long-tail opportunity profitably.

By Service Type: Technology Consulting Accelerates

Operations consulting continues to dominate spend, driven by ongoing process-optimization needs in logistics, mining, and utilities. Yet technology consulting is scaling fastest, delivering a 6.58% CAGR as clients migrate to AI-enabled operating models. The launch of Africa’s first AI factory by Cassava Technologies and Nvidia is set to produce knock-on advisory work in data-center design, edge-compute strategy, and regulatory alignment.

Cybersecurity, cloud migration, and data governance engagements form the core of technology pipelines, complementing broader digital strategy road-mapping. Sustainability and impact-investment advisory is emerging as an adjunct capability as enterprises embed climate-resilience metrics into digital-transformation charters.

By Delivery Model: Remote Engagement Gains Momentum

On-site delivery was the largest segment and accounted for 63.88% of the market in 2025. It remains the preferred mode for politically sensitive or mission-critical transformations that require extensive stakeholder alignment. Board-level trust and cultural nuances make physical presence indispensable for infrastructure megaprojects and regulatory overhauls.

The remote model, however, is registering consistent gains—especially for specialist technology or compliance work that can be executed virtually. Improved bandwidth from 77 operational undersea-cable systems and rising enterprise comfort with secure collaboration platforms underpin the 4.03% CAGR in virtual consulting. Hybrid delivery frameworks combining periodic on-site workshops with virtual sprints are becoming standard, enabling faster turnaround times and broader talent sourcing.

By End-user Industry: Healthcare Surges Ahead

Financial services held 26.32% of 2025 consulting revenue, sustained by banking-sector currency reforms, open-banking rollouts, and fintech scaling in Nigeria, Kenya, and Egypt. Advisory work spans regulatory road-mapping, risk analytics, and customer-experience redesign.

Healthcare, advancing at 10.47% CAGR, now represents the most dynamic vertical. National digital-health-ID programs in Ethiopia and Somalia’s telemedicine ecosystems require clinical workflow re-engineering, cybersecurity, and change management consulting. Infrastructure investments such as the African Medical Centre of Excellence’s USD 40 million equity round further widen demand for project-finance, design, and commissioning expertise.

Geography Analysis

South Africa’s slice of the Africa management consulting services market size is supported by a USD 1.5 billion World Bank loan that targets freight and energy reform, driving large-scale implementation mandates across SOEs. Johannesburg remains the preferred hub for global firms seeking a continental foothold, thanks to seasoned talent pools and robust legal infrastructure. The National Treasury’s push to remove bureaucratic bottlenecks further amplifies spend on change-management consulting.

Nigeria’s consulting demand thrives on fintech proliferation and oil-sector reforms that compel dual-track strategy and regulatory engagements. Open-banking APIs and payments modernization drive technology-consulting pipelines, while the Petroleum Industry Act demands new ESG and local-content compliance frameworks. Currency volatility introduces pricing risk but also opens advisory niches around hedge-accounting and Treasury optimization.

Northern and Francophone markets such as Egypt, Morocco, and Côte d’Ivoire leverage manufacturing and renewable-energy programs to attract specialized consultants in automotive value chains, green hydrogen, and agri-processing. East-Africa’s corridor projects—like the USD 4 billion Lobito railway—anchor cross-border supply-chain advisory. Collectively, these regional currents ensure the Africa management consulting services market continues to diversify and deepen.

Competitive Landscape

Global majors—Accenture, McKinsey & Company are some of the major players in the market. These companies retain a stronghold position on flagship transformation projects owing to methodology depth and global delivery networks. They are progressively embedding AI accelerators and digital twins into proposal toolkits, shortening diagnostic phases and fortifying value-demonstration.

Professional-services conglomerates PwC, EY, KPMG, and Deloitte leverage audit relationships to cross-sell tax, ESG, and cyber-consulting, while regional specialists such as IQbusiness and Dalberg capitalize on intimate knowledge of local procurement norms and political ecosystems. Technology-focused boutiques have surfaced to serve niche areas like cloud cost-optimization, DevSecOps, and carbon accounting.

Recent partnerships—exemplified by the European Investment Bank’s joint climate-resilience vehicle with Africa Finance Corporation—underscore a shift toward ecosystem-based delivery in which consultancies orchestrate consortia of financiers, engineering firms, and digital-platform providers. Cybersecurity, AI governance, and cross-border trade facilitation remain open white spaces where nimble entrants can disrupt incumbents.

Africa Management Consulting Services Industry Leaders

Accenture plc

McKinsey & Company, Inc.

Deloitte Consulting LLP

PricewaterhouseCoopers International Ltd (PwC)

Ernst & Young Global Ltd (EY)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: International Finance Corporation projected USD 11 billion in pharma-manufacturing investment needs by 2030, spotlighting advisory opportunities in GMP design and supply-chain optimization.

- June 2025: Ghana-UAE USD 1 billion accord to build a 25 km² tech hub positions Ningo-Prampram as a new consulting hotspot for AI-ecosystem planning.

- June 2025: World Bank approved USD 1.5 billion to overhaul South Africa’s energy and freight sectors, generating large-scale organizational-change mandates.

- March 2025: Cassava Technologies and Nvidia launched plans for Africa’s first AI factory in South Africa, unlocking a wave of AI-implementation consulting demand.

Africa Management Consulting Services Market Report Scope

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Technology Consulting |

| Other Service Types |

| On-site Consulting |

| Remote / Virtual Consulting |

| IT and Telecommunications |

| Healthcare and Life Sciences |

| Financial Services (BFSI) |

| Manufacturing and Industrial |

| Energy and Utilities |

| Government and Public Sector |

| Real Estate and Construction |

| Retail and Consumer Goods |

| Media, Entertainment and Sports |

| Hospitality and Travel |

| Other Industries |

| South Africa |

| Nigeria |

| Egypt |

| Rest of Africa |

| By Organization Size | Large Enterprises |

| Small and Medium-sized Enterprises | |

| By Service Type | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Technology Consulting | |

| Other Service Types | |

| By Delivery Model | On-site Consulting |

| Remote / Virtual Consulting | |

| By End-user Industry | IT and Telecommunications |

| Healthcare and Life Sciences | |

| Financial Services (BFSI) | |

| Manufacturing and Industrial | |

| Energy and Utilities | |

| Government and Public Sector | |

| Real Estate and Construction | |

| Retail and Consumer Goods | |

| Media, Entertainment and Sports | |

| Hospitality and Travel | |

| Other Industries | |

| By Geography | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

Key Questions Answered in the Report

What is the current value of the Africa management consulting services market?

The sector is valued at USD 3.89 billion in 2026 and is projected to hit USD 4.58 billion by 2031.

Which segment is growing fastest within consulting services?

Technology consulting leads growth with a 6.58% CAGR through 2031, driven by AI and cloud adoption initiatives.

Why is South Africa the largest geographic market?

South Africa combines advanced ESG regulations, robust capital markets, and major SOE reforms that require extensive advisory support, giving it 21.05% revenue share.

What restrains consulting growth in Africa?

Key challenges include talent shortages, currency volatility, cyber-security risks, and the rise of internal consulting teams.

How does AfCFTA influence consulting demand?

AfCFTA harmonizes trade rules, prompting companies to seek guidance on customs modernisation, market-entry strategy, and cross-border supply-chain alignment.

Which industry vertical shows the highest future growth?

Healthcare is forecast to expand at a 10.47% CAGR through 2031, fueled by digital-health infrastructures and hospital megaprojects.

Page last updated on: