Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

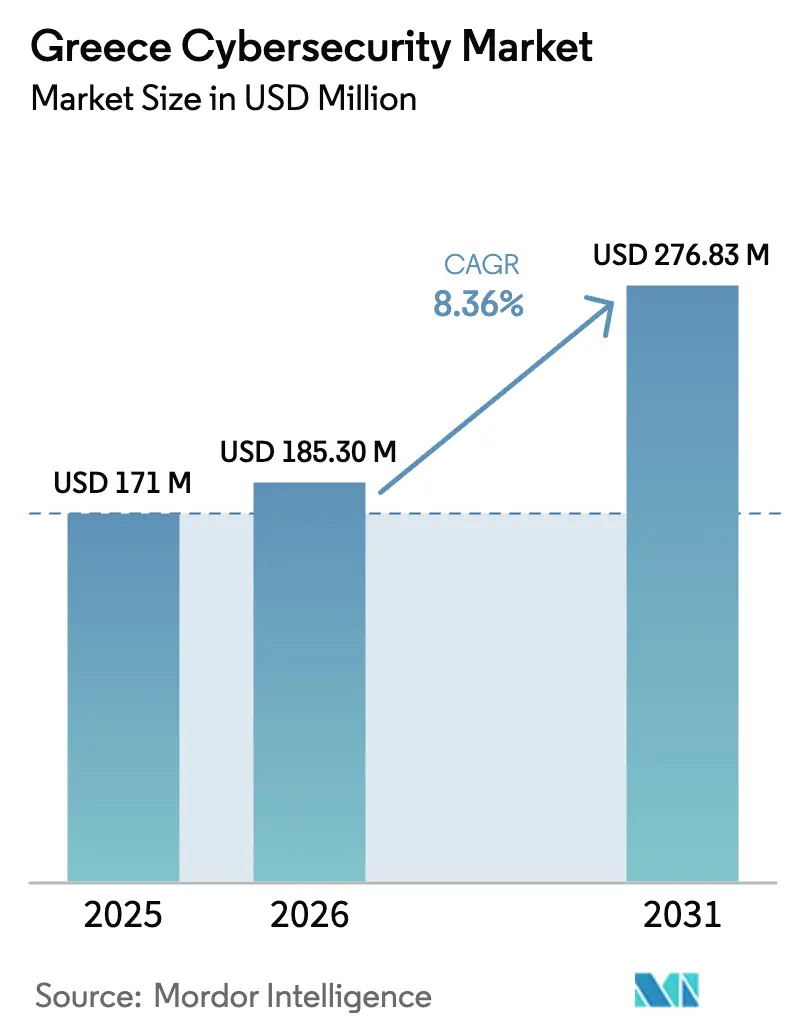

| Base Year Market Size (2025) | USD 171.0 Million |

| Market Size (2026) | USD 185.3 Million |

| Market Size (2031) | USD 276.83 Million |

| Growth Rate (2026 - 2031) | 8.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Greece Cybersecurity Market Analysis by Mordor Intelligence

The Greece cybersecurity market size was valued at USD 171.0 million in 2025 and estimated to grow from USD 185.3 million in 2026 to reach USD 276.83 million by 2031, at a CAGR of 8.36% during the forecast period (2026-2031). Rising investment from the EU Recovery and Resilience Facility, mandatory alignment with the NIS2 Directive under Greek Law 5160/2024, and Microsoft’s USD 1.0 billion hyperscale datacenter region underpin sustained demand. Organizations now channel 9% of overall IT budgets toward security as weekly incidents against maritime, energy and telecom targets climb, while a 900% attack surge in shipping since 2017 recalibrates risk appetites. Expansion of submarine cable corridors linking Egypt, Cyprus and mainland Greece promotes network-security spending, and the talent deficit propels managed security services as a default procurement route for mid-market firms.

Key Report Takeaways

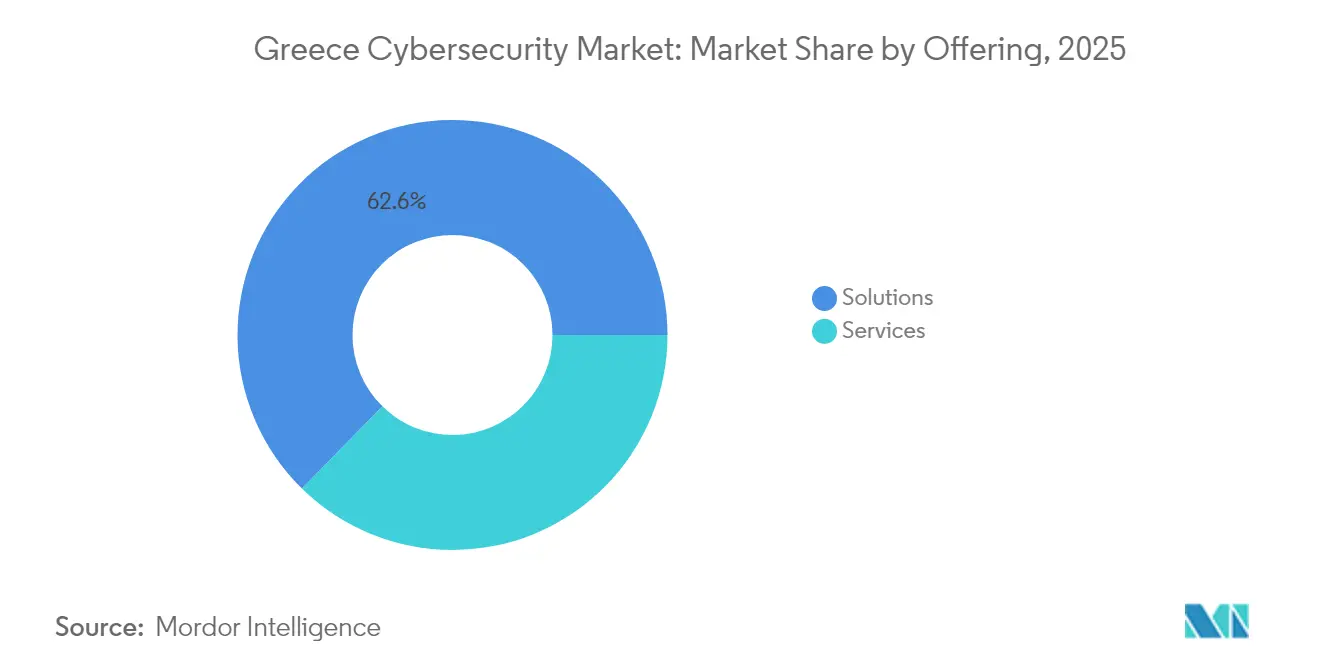

- By offering, solutions held 62.65% of the Greece cybersecurity market share in 2025; services are forecast to grow at a 12.35% CAGR to 2031.

- By deployment mode, cloud captured 56.85% of revenue in 2025, while on-premise trails; cloud is advancing at an 11.05% CAGR through 2031.

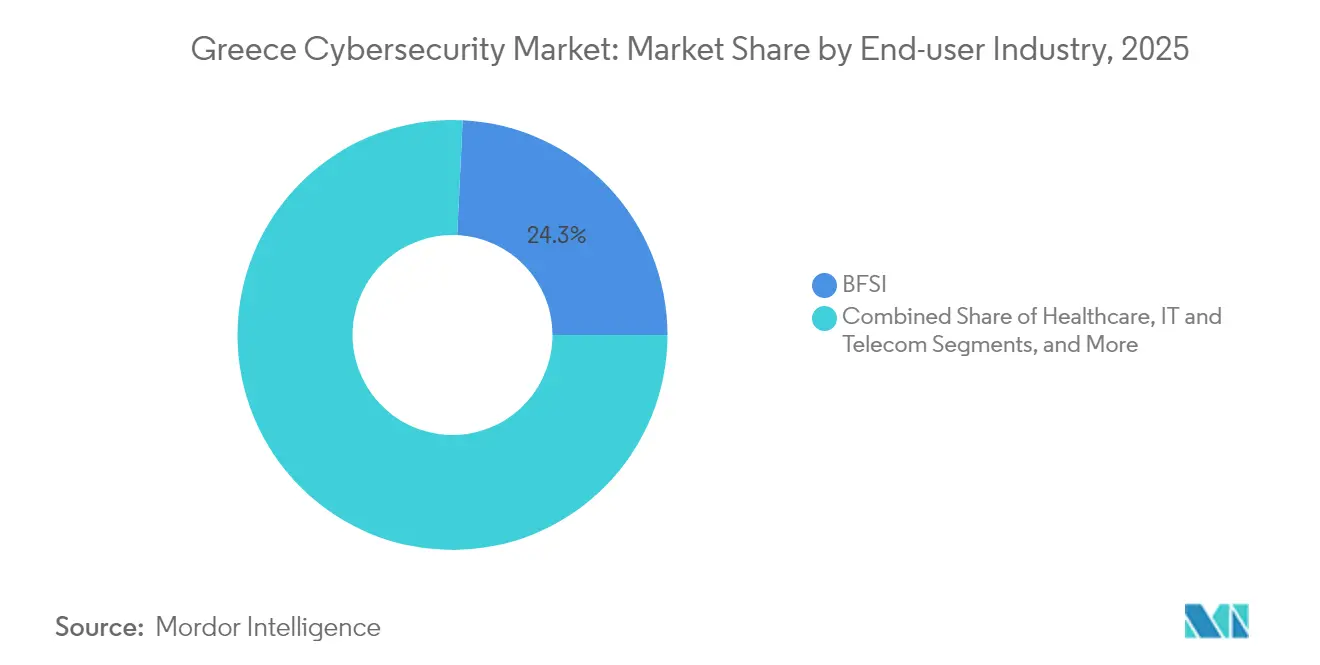

- By end-user industry, BFSI led with 24.25% revenue share in 2025, whereas healthcare is projected to expand at a 13.05% CAGR to 2031.

- By end-user enterprise size, large enterprises commanded 71.05% of the Greece cybersecurity market size in 2025, yet SMEs post the top-line growth at 13.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Greece Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory compliance with NIS2 and Greek Law 5160/2024 | +2.1% | Nationwide, 2,000+ entities | Medium term (2–4 years) |

| Surge in sophisticated attacks on critical infrastructure | +1.8% | Ports of Piraeus, Thessaloniki | Short term (≤ 2 years) |

| Accelerated cloud migration under “Greece 2.0” plan | +1.5% | Attica datacenter cluster | Medium term (2–4 years) |

| EU Recovery-fund fuelled security spend in BFSI and public sector | +1.3% | Countrywide | Short term (≤ 2 years) |

| Growth of hyperscale datacentres | +1.0% | Spata, Koropi, Heraklion | Long term (≥ 4 years) |

| Emergence as SE-Europe telecom-cable hub | +0.8% | Crete landing stations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory compliance with NIS2 and Greek Law 5160/2024

Greek Law 5160/2024, effective November 2024, broadens liability from 400 critical operators to more than 2,000 essential and important entities, enforces 24-hour incident notifications and levies fines up to USD 10 million for non-compliance. Board-level accountability and compulsory supply-chain risk assessments push enterprises to adopt integrated detection and response platforms, automated reporting tools and cyber-governance consulting. Demand strengthens for threat-hunting and vulnerability-management services able to prove resilience audits to the National Cybersecurity Authority.

Surge in sophisticated cyber-attacks on critical infrastructure

State-sponsored activity now targets energy micro-grids, maritime control networks and cable landing stations, with large Greek organizations reporting 10–20% upticks in attack frequency and average breach costs of USD 504,000 [1]Insurance Journal, “Greek Solar Farms Expose Grid to Cyber Risk,” insurancejournal.com. The 900% escalation in maritime incidents since 2017 forces ship-operators to overhaul vessel OT monitoring, while shared threat-intelligence exchanges linking shipping, power and telecom operators emerge as risk-mitigation norms.

Accelerated cloud migration under “Greece 2.0” digital plan

USD 7.7 billion earmarked for Greece 2.0 accelerates 450 public-sector workloads toward cloud datacentres operated by Microsoft, Amazon Web Services and Google, fuelling identity-access, encryption and posture-management uptake. SME vouchers subsidise secure SaaS adoption for 100,000 companies, expanding mass-market demand for cloud-native security frameworks.

EU Recovery-fund fuelled security spend in BFSI and public sector

Greek transposition of the Digital Operational Resilience Act (DORA) via Law 5193/2025 imposes mandatory penetration tests, third-party risk assessments and continuous monitoring on banks and insurers supervised by the Bank of Greece. Parallel public-hospital imaging projects covering 2 million annual exams necessitate data-protection controls, stimulating cross-sector procurement of unified governance, risk and compliance (GRC) suites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute cybersecurity talent shortage | –1.4% | Athens, Thessaloniki tech hubs | Medium term (2–4 years) |

| SME cost-sensitivity toward advanced tools | –0.9% | Nationwide, 99% of firms | Short term (≤ 2 years) |

| Regulatory overlap causing fatigue | –0.6% | Multi-sector entities | Medium term (2–4 years) |

| Legacy OT in shipping and energy | –0.7% | Piraeus, Thessaloniki ports | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute cybersecurity talent shortage

Greece will require up to 400,000 additional technology workers by 2030, with 32% of firms failing to fill security roles as wage inflation outstrips budgets [2]ENISA, “Cybersecurity Skills Shortage in the EU,” enisa.europa.eu. MSSPs raise retainers, and universities race to harmonise curricula, but the supply–demand gap persists, curbing in-house SOC expansion.

SME cost-sensitivity toward advanced security tools

Eighteen percent of Greek SMEs lack any cybersecurity controls and 44% rely solely on antivirus suites, citing funding and expertise gaps. Although the EU voucher scheme offsets procurement costs, unfamiliar tender rules and limited technical staff restrict uptake, lengthening sales cycles for enterprise-grade solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Acceleration Outpaces Solutions Maturity

Solutions contributed 62.65% of revenue in 2025 as firms established baseline controls for NIS2 alignment. Services, though smaller, are scaling at a 12.35% CAGR, reflecting reliance on external specialists to bridge the talent deficit. Application- and cloud-security suites command adoption in newly built Attica datacentres, while identity-access tools gain traction among remote workforces.

Professional and managed services growth is underpinned by architecture reviews, incident-response retainers and regulatory-gap assessments. Providers such as KPMG Greece bundle NIS2, DORA and ISO-27001 readiness within fixed-fee engagements, positioning services as the fastest-rising revenue stream within the Greece cybersecurity market.

By Deployment Mode: Cloud Dominance Accelerates Infrastructure Transformation

Cloud held a 56.85% stake in 2025 and extends at an 11.05% CAGR to 2031, mirroring USD 5.0 billion in hyperscale facility investments by Microsoft, Digital Realty and AWS. Hybrid models capture utilities and BFSI entities that must keep legacy mainframes on-premise yet modularise new workloads in the cloud.

Greek Law 5069/2023 simplifies zoning for datacentres above 10 MW, sparking a cluster near Spata. Edge-compute nodes along submarine-cable landing sites create micro-segmented security perimeters. On-premise deployments remain essential for air-gapped maritime and energy OT, but the direction of travel favours SaaS and infrastructure-as-code security disciplines that underpin the Greece cybersecurity market.

By End-user Industry: Healthcare Surge Challenges BFSI Leadership

BFSI controlled 24.25% revenue in 2025, anchored in card-fraud analytics and core-banking modernisation. DORA makes continuous penetration testing and supply-chain audits mandatory, sustaining expenditure. Healthcare, boosted by AGFA HealthCare’s imaging rollout at 37 hospitals, logs the swiftest 13.05% CAGR, as patient-data confidentiality rules drive encryption and IAM projects.

Energy operators invest to neutralise rooftop solar vulnerabilities, while the maritime community introduces vessel-communications firewalls ahead of IMO cyber-deadlines. Retail and manufacturing activity is modest yet accelerating as SMEs utilise voucher funding, further broadening demand profiles inside the Greece cybersecurity market.

By End-user Enterprise Size: SME Growth Potential Exceeds Large-Enterprise Stability

Large enterprises accounted for 71.05% of 2025 spending, leveraging deeper budgets and mature governance structures. However, SMEs will outpace them at a 13.55% CAGR, catalysed by simplified security-as-a-service bundles and subsidised cloud migrations.

The talent crunch is acute for smaller firms lacking full-time CISOs, prompting MSSP partnerships for 24×7 monitoring. Government-supported dashboards such as SMESEC deliver unified risk views, instilling best-practice baselines and widening the customer funnel for the Greece cybersecurity market.

Geography Analysis

Attica anchors the domestic market as Microsoft, AWS and Digital Realty establish multi-availability-zone campuses near Spata and Koropi, igniting a local ecosystem of SOC providers, compliance consultants and start-ups. The National Cybersecurity Authority and leading integrators Space Hellas and Uni Systems operate their headquarters in Athens, securing public-sector NIS2 roll-outs .

Crete’s Heraklion campus and the Egyptian land-link via Port Said elevate the island as a Mediterranean cable crossroads, necessitating layered network-security gateways and sovereign data-governance controls. Thessaloniki hosts a secondary innovation pole tied to rooftop-solar R&D, where demonstrations of remote PV hijacking spark grid-protection pilots across mainland energy zones.

Regional export potential grows as Balkan neighbours seek EU-aligned frameworks. The Pharos AI supercomputing program and DAEDALUS initiative position Greece as a regional R&D nucleus, beckoning cross-border ventures and reinforcing the Greece cybersecurity market as a Southeast European security hub.

Competitive Landscape

Global vendors—IBM, Cisco, Microsoft, Fortinet and Palo Alto Networks—serve large enterprises with full-stack platforms, combining XDR, SASE and zero-trust toolkits. Their scale advantages include global threat-intelligence feeds and local PoP coverage inside Athens datacentres.

Domestic integrators such as Space Hellas (USD 78.9 million H1 2024 revenue) and Uni Systems leverage native language support, EU-fund bid experience and entrenched public-sector ties to secure NIS2 and DORA compliance projects. Hybrid alliances form: Space Hellas resells Cisco SecureX, while Uni Systems integrates Microsoft Sentinel for managed detection.

Service-centred firms—EY, KPMG, Accenture—differentiate via governance consulting as the talent drought intensifies, pricing retainer contracts at premium rates. Maritime-focused start-ups emerge, including Optima Cyber, addressing operational-technology niches. The moderate blend of local and global providers keeps the Greece cybersecurity market moderately concentrated yet competitive.

Greece Cybersecurity Industry Leaders

IBM Corporation

Fortinet Inc.

Cisco Systems, Inc.

Check Point Software Technologies Ltd.

Palo Alto Networks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The European Commission raised 2025 cybersecurity R&D funding to USD 90.5 million, prioritising AI-driven defence and post-quantum cryptography.

- April 2025: Greece unveiled the USD 27.0 billion Agenda 2030 rearmament initiative, embedding cyber-defence in the Shield of Achilles program.

- March 2025: Optima Shipping Services launched Optima Cyber with TicTac Cyber Security and Crimelab to secure domestic fleets.

- October 2024: Vodafone Greece and ELIAMEP presented citizen-centric cybersecurity proposals to the National Cybersecurity Authority at the Delphi Economic Forum.

Greece Cybersecurity Market Report Scope

Cybersecurity solutions help organizations monitor, report, and counter cyber threats to maintain data confidentiality. The adoption of cybersecurity solutions is expected to grow in line with the rising internet penetration among developing and developed countries. The need for cybersecurity has increased as every system in today's world is connected to the internet, making data more accessible to cybercriminals.

The Greece cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security | |

| End-point Security | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| Cloud |

| On-Premise |

By End-user Industry

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

By End-user Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security | ||

| End-point Security | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | Cloud | |

| On-Premise | ||

| By End-user Industry | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By End-user Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

Key Questions Answered in the Report

What is the current size of the Greece cybersecurity market and how fast is it growing?

The market is valued at USD 185.3 million in 2026 and is forecast to reach USD 276.83 million by 2031, registering an 8.36% CAGR.

Which segment is expanding faster—solutions or services?

Services are the fastest-growing segment at a 12.35% CAGR through 2031, outpacing the solutions segment that currently holds the larger revenue share.

Why is cloud deployment gaining momentum in Greece?

USD 5.0 billion in hyperscale datacenter investments from Microsoft, Digital Realty and AWS, coupled with the Greece 2.0 digital-transformation program, is driving an 11.05% CAGR for cloud-based security.

How does NIS2 compliance impact Greek organizations?

Greek Law 5160/2024 extends cybersecurity obligations to more than 2,000 entities, imposes 24-hour breach-notification rules and fines up to USD 10 million, accelerating demand for automated detection and response tools.

Page last updated on: