Egg Donation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

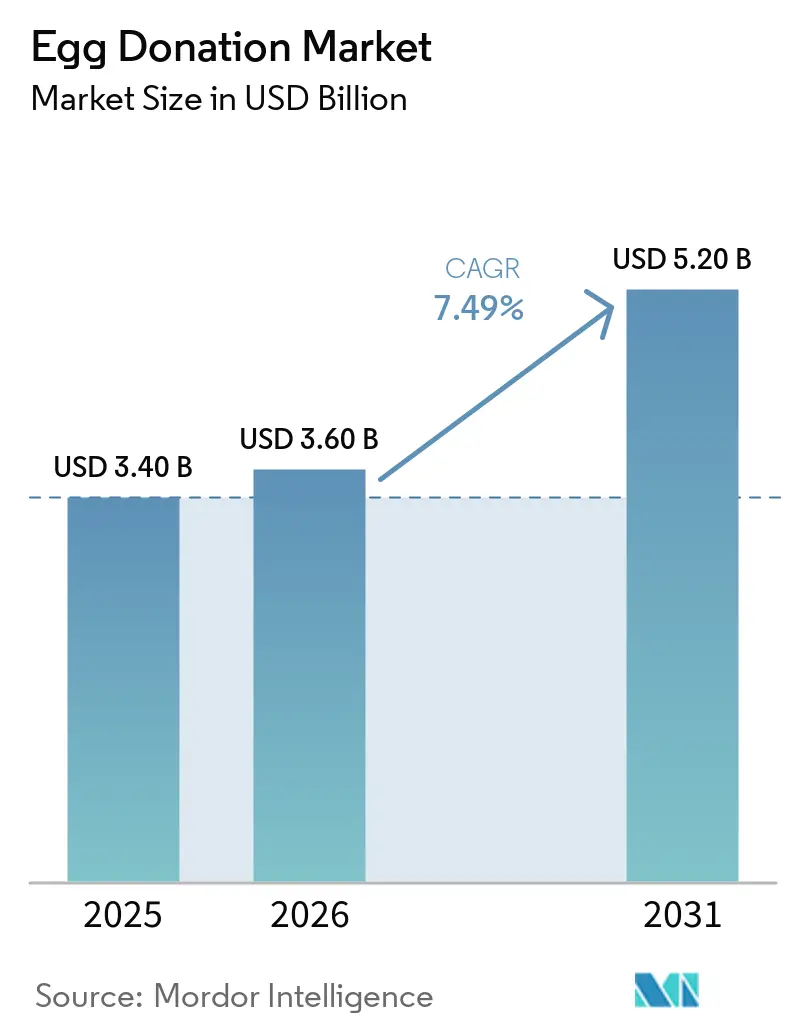

| Market Size (2026) | USD 3.60 Billion |

| Market Size (2031) | USD 5.20 Billion |

| Growth Rate (2026 - 2031) | 7.49% CAGR |

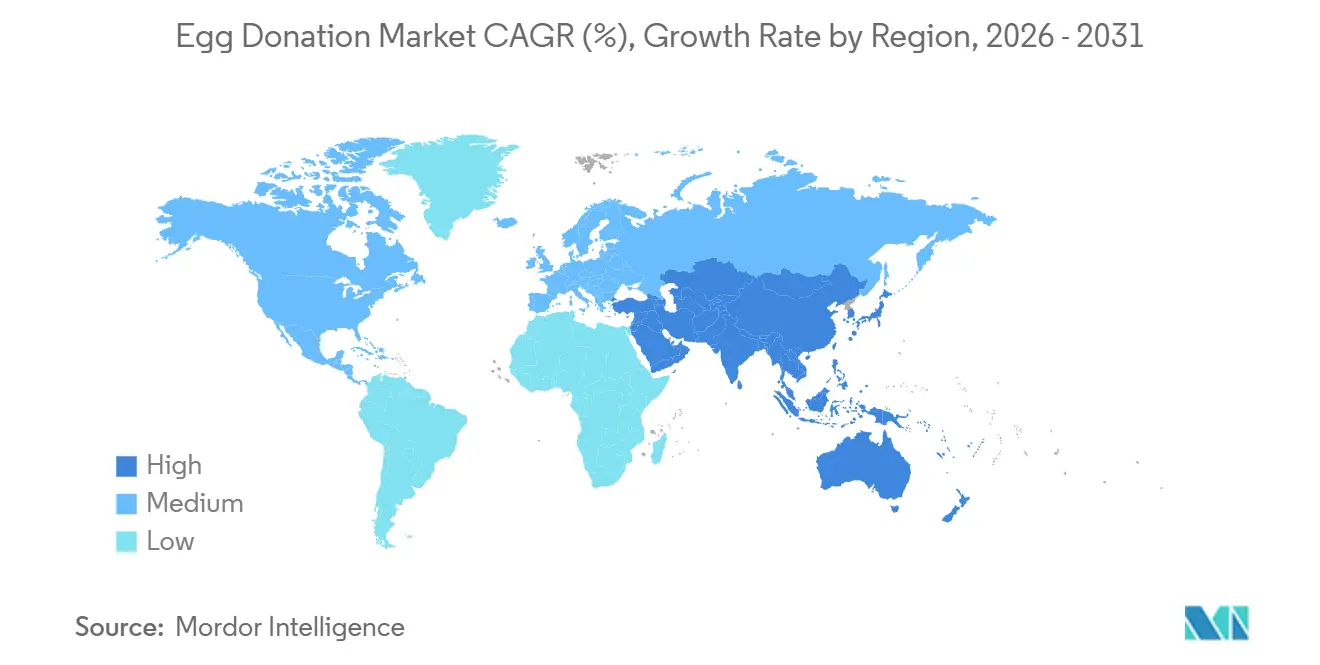

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egg Donation Market Analysis by Mordor Intelligence

The Egg Donation Market size is expected to increase from USD 3.40 billion in 2025 to USD 3.60 billion in 2026 and reach USD 5.20 billion by 2031, growing at a CAGR of 7.49% over 2026-2031.

Employer-funded fertility mandates, live-birth parity between frozen and fresh donor eggs, and cross-border care that funnels recipients toward permissive European hubs are reshaping global access. Fresh donor eggs commanded the majority share in 2025 and will outpace frozen eggs due to higher per-cycle egg yields, although vitrification success rates above 90% continue to narrow the gap. Intensifying consolidation exemplified by a USD 535 million U.S. laboratory roll-up that added 13 labs and 32 satellite sites in 2024 positions large networks to negotiate with payers and match recipients at scale.

Key Report Takeaways

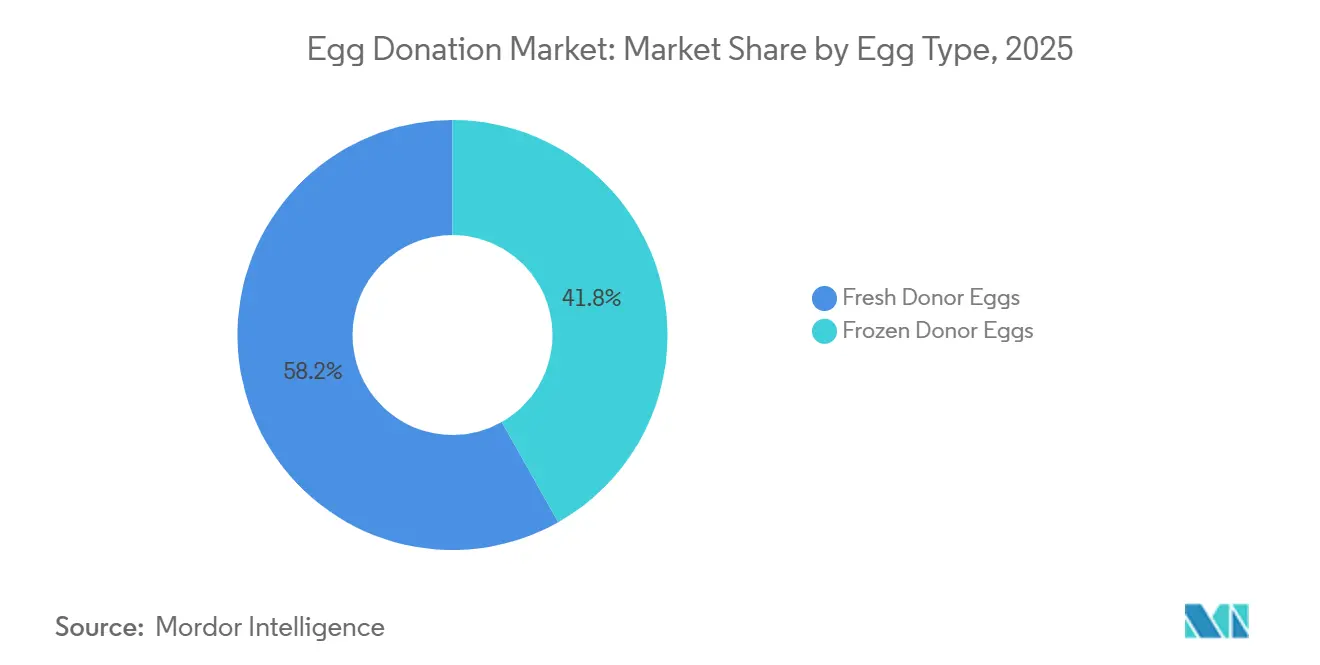

- By egg type, fresh donor eggs led with 58.18% of egg donation market share in 2025; frozen donor eggs are projected to grow at an 8.13% CAGR through 2031.

- By end user, fertility clinics accounted for 55.17% of the egg donation market in 2025, while hospitals are advancing at a 8.09% CAGR through 2031.

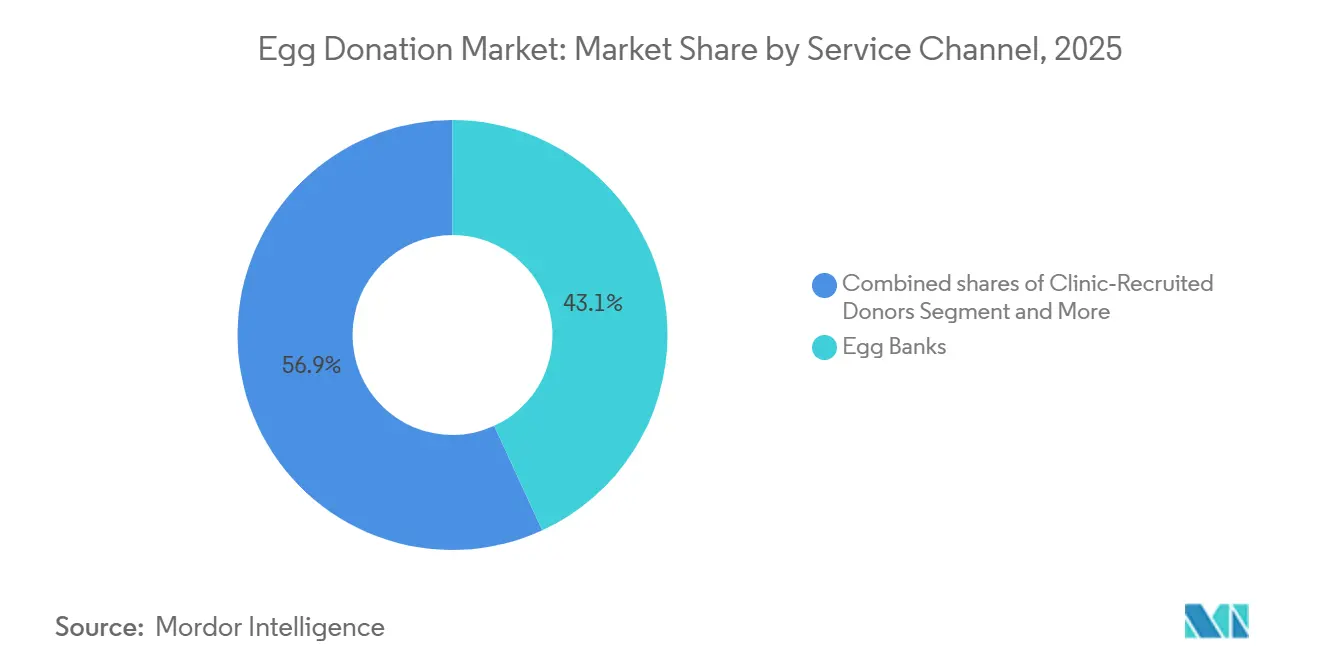

- By service channel, egg banks accounted for 43.15% of revenue in 2025; clinic-recruited donor programs are the fastest-growing channel, with an 8.21% CAGR through 2031.

- By geography, North America led with 36.19% of egg donation market share in 2025; Asia-Pacific is projected to grow at an 8.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Egg Donation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Employer-sponsored fertility coverage widens patient pool | +1.2% | North America, Western Europe | Short term (≤ 2 years) |

| Frozen-egg success parity encourages use of egg banks | +1.5% | Global, early gains in North America, Europe, core APAC | Medium term (2-4 years) |

| Medical travel channels recipients to Spain and the Czech Republic | +0.9% | Europe (Spain, Czech Republic) with spill-over to MEA and APAC | Medium term (2-4 years) |

| Clinic–bank partnerships broaden donor choice worldwide | +1.3% | Global, strongest in North America and Asia-Pacific | Long term (≥ 4 years) |

| Telehealth consults enable remote matching and monitoring | +0.7% | Global, initial traction in North America and Europe | Short term (≤ 2 years) |

| AI tools refine donor screening and embryo selection | +0.8% | Global, concentrated in North America, Europe, APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Employer-Funded Fertility Benefits Expand Access and Affordability

California’s Senate Bill 729 obliges group plans with more than 100 employees to cover IVF and donor-egg cycles beginning in 2026, erasing out-of-pocket barriers for nearly 2 million residents[1]Fertility Bridge, “Employer-Funded Fertility Benefits Expand Access,” fertilitybridge.com. Illinois extended Medicaid fertility benefits in January 2026, and the U.S. Federal Employees Health Benefits program clarified in 2025 that donor-egg procedures qualify for reimbursement. Digital platform Maven Clinic reports employer-sponsored plans now fund majority of its patient volume, underscoring how mandates expand the egg donation market beyond high-income households. Scale favors national clinic chains that can meet sudden demand surges, whereas smaller practices face margin pressure from negotiated reimbursement rates. Comparable legislation under debate in the United Kingdom and Australia signals a broader shift toward insurer-backed fertility coverage.

Vitrification Parity Boosts Adoption of Banked Donor Eggs

Rapid-freeze vitrification prevents ice-crystal damage, yielding survival rates above 90% and live-birth outcomes indistinguishable from those of fresh cycles, according to multiple peer-reviewed studies published between 2024 and 2026. Parity erodes longstanding clinical bias toward fresh eggs and enables egg banks to hold diverse donor inventories, cutting matching times from months to weeks. London Egg Bank reports more than 20,000 frozen eggs ready for overnight shipment across the United Kingdom, while a January 2026 export pact allows Asian Egg Bank to distribute 1,500 frozen eggs to seven countries. Lower donor burden six to ten eggs can be thawed on demand reduces cycle cost and widens access in altruistic-only markets that cap or prohibit monetary compensation.

Cross-Border Care Concentrates Donor Supply in EU Hubs

Spain and the Czech Republic serve as Europe’s egg-donation clearinghouses by permitting anonymous donation, compensating donors EUR 800-1,200, and allowing recipients up to age 49 (Spain) or 50 (Czech Republic). Costs of USD 4,500-9,000 per cycle are roughly half those in Australia or the United States, attracting patients from Germany, the United Kingdom, and Scandinavia, where waiting lists exceed two years. Reprofit’s multilingual tele-consultations and no-wait guarantee highlight how Czech clinics court international recipients. Policy tightening elsewhere, France ended donor anonymity in March 2025, and Belgium proposed a similar shift in November 2025, reinforcing traffic toward permissive EU hubs.

Clinic–Egg Bank Networks Globalize Donor Access

MyEggBank partners with more than 200 U.S. clinics and launched flexible Open ID, Semi-Open, and ID Release donor options in July 2025 to navigate emerging identity-disclosure laws. Fairfax EggBank’s 2024 integration of Luminary Donor Eggs doubled its catalog to over 450 profiles, while Asian Egg Bank maintains 700 active donors for export across the Pacific. Networks standardize embryology protocols, share outcome data, and negotiate discounted cryo-logistics, allowing a rural clinic to offer a donor pool rivaling that of urban centers.

Restraints Impact Analysis*

| Restraint | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure cost and uneven insurance coverage | -1.1% | Global, acute in Australia, United Kingdom, emerging markets | Short term (≤ 2 years) |

| Legal bans or tight limits in key countries | -0.8% | China, Japan, Middle East, parts of Europe | Long term (≥ 4 years) |

| Loss of donor anonymity raises compliance burden | -0.6% | Europe, North America, Australia | Medium term (2-4 years) |

| Limited donor pool, higher screening spend, ethical concerns | -0.9% | Global, severe in Australia, United Kingdom, altruistic markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost and Patchy Reimbursement

A donor-egg IVF cycle costs USD 15,000-25,000 in the United States, USD 10,000-20,000 in Australia, and GBP 8,000-12,000 in the United Kingdom, with donor compensation frequently excluded from insurance[2]Elfy Scott, “Should Australia Change Its Egg Donation Laws?” SBS News, sbs.com.au. California’s 2026 mandate and Illinois’s Medicaid expansion contrast with Australia’s Medicare exclusion and the U.K.’s rationing of National Health Service coverage, creating affordability cliffs. In Australia, a 1:52 donor-to-recipient ratio forces many patients abroad, while a USD 120 million public fertility program launched in 2024 has recorded only 140 pregnancies and one live birth by early 2026.

Regulatory Bans or Restrictions in Key Markets

China prohibits commercial egg donation, leaving fewer than 0.2% of annual assisted-reproduction cycles reliant on donor eggs. Japan limits donation to altruistic cases under professional guidelines that bar egg banks and restrict donors to women under 35 with children, keeping the domestic supply negligible. Germany, Switzerland, and multiple Middle-Eastern countries enforce outright bans. Colorado’s July 2024 law requiring donor identity disclosure discouraged U.S. participation, and France’s similar move stranded 10,600 patients on waitlists by early 2026[3]Human Fertilisation and Embryology Authority, “Written Evidence for WEC Inquiry,” hfea.gov.uk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Egg Type: Fresh Cycles Retain Edge Despite Frozen Gains

Fresh donor eggs held 58.18% of 2025 revenue, and the segment will grow at an 8.13% CAGR through 2031 as recipients favor higher egg yields per retrieval. The egg donation market size for fresh cycles is forecast to reach USD 3.0 billion by 2031, aided by personalized matching in the United States and Spain. Vitrification survival rates above 90% have narrowed the outcome gap, propelling the use of frozen eggs among older recipients and cross-border patients.

Frozen eggs compress timelines from months to weeks, reduce donor burden, and are less exposed to tightening anonymity laws because many were banked before new disclosure mandates. Asian Egg Bank’s partnership to export 1,500 frozen eggs annually demonstrates how banked inventories serve donor-short jurisdictions. Price gaps also matter: frozen cycles in Spain cost EUR 4,500-6,500 versus EUR 6,000-9,000 for fresh, steering value-oriented recipients toward vitrified options.

By End User: Hospitals Accelerate Through Integrated Networks

Fertility clinics accounted for 55.17% of revenue in 2025, reflecting deep embryology expertise and proprietary donor catalogs. Hospitals, however, are advancing at an 8.09% CAGR to 2031 as integrated health systems embed fertility suites, retain insured patients, and tap intra-system referrals. Conemaugh Memorial’s 2025 alliance with Shady Grove Fertility and UNC Health’s 2026 partnership with IVI RMA illustrate a trend that is expanding the egg donation market’s clinical footprint in secondary cities.

Hospital settings benefit from existing compliance structures under HIPAA and GDPR, a boon as identity-disclosure rules spread. Clinics remain dominant where specialized genetic testing or high-volume donor recruitment is required, yet university hospitals are catching up by acquiring or partnering with niche providers.

By Service Channel: Clinic-Recruited Donors Outpace Banked Eggs

Egg banks accounted for 43.15% of 2025 revenue, but clinic-recruited, fresh-donor programs are the fastest-growing channel, with an 8.21% CAGR, reflecting recipient preference for customizable donor traits and larger egg batches per cycle. The egg donation market share of clinic-recruited programs is forecast to climb by 2031. Open-ID frameworks let donors decide their future contact preferences, align with evolving disclosure laws, and encourage participation.

Agencies that charge USD 30,000-50,000 for concierge donor matching cater to high-net-worth clientele, especially same-sex male couples who also need surrogacy. In altruistic-only markets such as Australia and the United Kingdom, limited domestic donors push clinics to import frozen eggs or work through agencies abroad, reinforcing the value of trans-border networks.

Geography Analysis

North America held 36.19% of 2025 revenue, driven by employer mandates, private-equity consolidation, and the world’s most liquid donor-egg supply chain. Colorado’s disclosure law and a 97% applicant rejection rate due to FDA criteria signal a tightening of the labor supply, even as coverage widens. Trait-based compensation differentials, White and Asian donors earning up to USD 100,000 over their lifetimes, are drawing ethical scrutiny. Canada remains constrained by altruistic rules, while Mexico serves as a cost-sensitive destination for U.S. patients.

Europe’s landscape is bifurcated. Spain and the Czech Republic continue to welcome international recipients with anonymous donations and cycle fees below USD 10,000. France’s 2025 anonymity repeal and Belgium’s pending legislation have lengthened waitlists, illustrating how policy can shrink supply faster than recruitment campaigns can respond. The United Kingdom raised donor compensation to GBP 985 in 2024, yet donor numbers stayed flat at around 1,500 annually, leaving thousands on National Health Service waiting lists. Germany, Switzerland, and Austria ban donation, funneling patients into Spain and the Czech Republic.

Asia-Pacific is the fastest-growing territory at an 8.97% CAGR through 2031. Japan reimburses about majority of advanced fertility costs but still forbids commercial donation, sending patients abroad. Australia faces a chronic 1:52 donor-recipient ratio and lags despite a USD 120 million public program that delivered only one birth by early 2026. China’s ban on commercial donation keeps domestic penetration below 1%, although provincial pilots may soften restrictions as population pressure mounts.

Competitive Landscape

Three forces define competition: private-equity roll-ups, technology infusion, and regulatory arbitrage. A 2024 USD 535 million acquisition created the largest U.S. fertility network, integrating 13 labs and 32 satellites to serve employer-mandate growth. KKR’s earlier USD 3.25 billion stake validated egg donation as a private-equity platform play. CSG.BIO’s March 2026 purchase of Hanabusa IVF and Asian Egg Bank extends this strategy into Asia-Pacific.

Technology distinguishes front-runners. Maven Clinic raised USD 125 million to scale its AI-supported network of 475 clinics, while Lucina Egg Bank’s ReflEggction algorithm predicts embryo viability, and Ovom Care’s AI workflow improved fertilization in European trials. Automation reduces lab variability, mitigates donor shortages by optimizing oocyte utilization, and shortens time-to-pregnancy.

Identity-disclosure laws create white space. Platforms that vet donors willing to allow future contact enjoy a first-mover advantage in Colorado and France. Smaller regional clinics retain niche positions by offering multilingual teleconsults and zero-wait guarantees, particularly in medical tourism corridors like Brno and Alicante. Still, the top five operators already control majority of U.S. cycle volume, and further deals are expected as valuations remain buoyant.

Egg Donation Industry Leaders

Cryos International A/S

California Cryobank

IVIRMA Global

Donor Egg Bank USA

Virtus Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: CSG.BIO acquired Hanabusa IVF and Asian Egg Bank to expand donor-egg logistics across seven Asia-Pacific countries.

- March 2026: Lucina Egg Bank launched ReflEggction, a machine-learning tool that predicts embryo viability to shorten cycle timelines.

- February 2026: IVI RMA and UNC Fertility formed a university-hospital partnership that embeds donor-egg services in North Carolina

Global Egg Donation Market Report Scope

As per the scope of the report, egg donation is an advanced form of assisted reproductive technology where a fertile woman provides her eggs, or oocytes, to help another individual or couple conceive a child. This process is typically utilized by recipients facing infertility due to advanced maternal age, premature ovarian failure, or a desire to avoid passing on genetic disorders.

The egg donation market is segmented by egg type, end users, service channel, and geography. Based on egg type, the market is segmented into fresh donor eggs and frozen donor eggs. Based on distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies (including D2C e-commerce). By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Fresh Donor Eggs |

| Frozen Donor Eggs |

| Fertility Clinics |

| Hospitals |

| Others |

| Egg Banks (Banked Frozen Oocytes) |

| Clinic‑Recruited Donors (Fresh) |

| Agencies / Matching Services |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Egg Type | Fresh Donor Eggs | |

| Frozen Donor Eggs | ||

| By End User | Fertility Clinics | |

| Hospitals | ||

| Others | ||

| By Service Channel | Egg Banks (Banked Frozen Oocytes) | |

| Clinic‑Recruited Donors (Fresh) | ||

| Agencies / Matching Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the egg donation market be by 2031?

It is projected to reach USD 5.2 billion, growing at a 7.49% CAGR from 2026 to 2031.

Which region is expanding fastest?

Asia-Pacific, propelled by insurance reforms in Japan and clinic expansion in India, is set for an 8.97% CAGR through 2031.

Do frozen donor eggs work as well as fresh ones?

Peer-reviewed studies show survival rates above 90% and comparable live-birth outcomes, making vitrified eggs a viable alternative.

What are the main cost barriers for patients?

Donor-egg IVF cycle prices range from USD 10,000 to USD 25,000, and insurance coverage varies across countries and even within the U.S. states.

Page last updated on: