Food & Beverage

2nd MayMarket Analysis of Synthetic Food Colorants for a Beverage Leader

5 Min Read

The Global Pea Flakes Market is Segmented by Product Type (Yellow Pea Flakes, Green Pea Flakes, and Speckled/Maple Pea Flakes), by Processing Technique (Steam-Rolled and Extruded/Instantised), by Application (Food and Animal Feed), and by Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

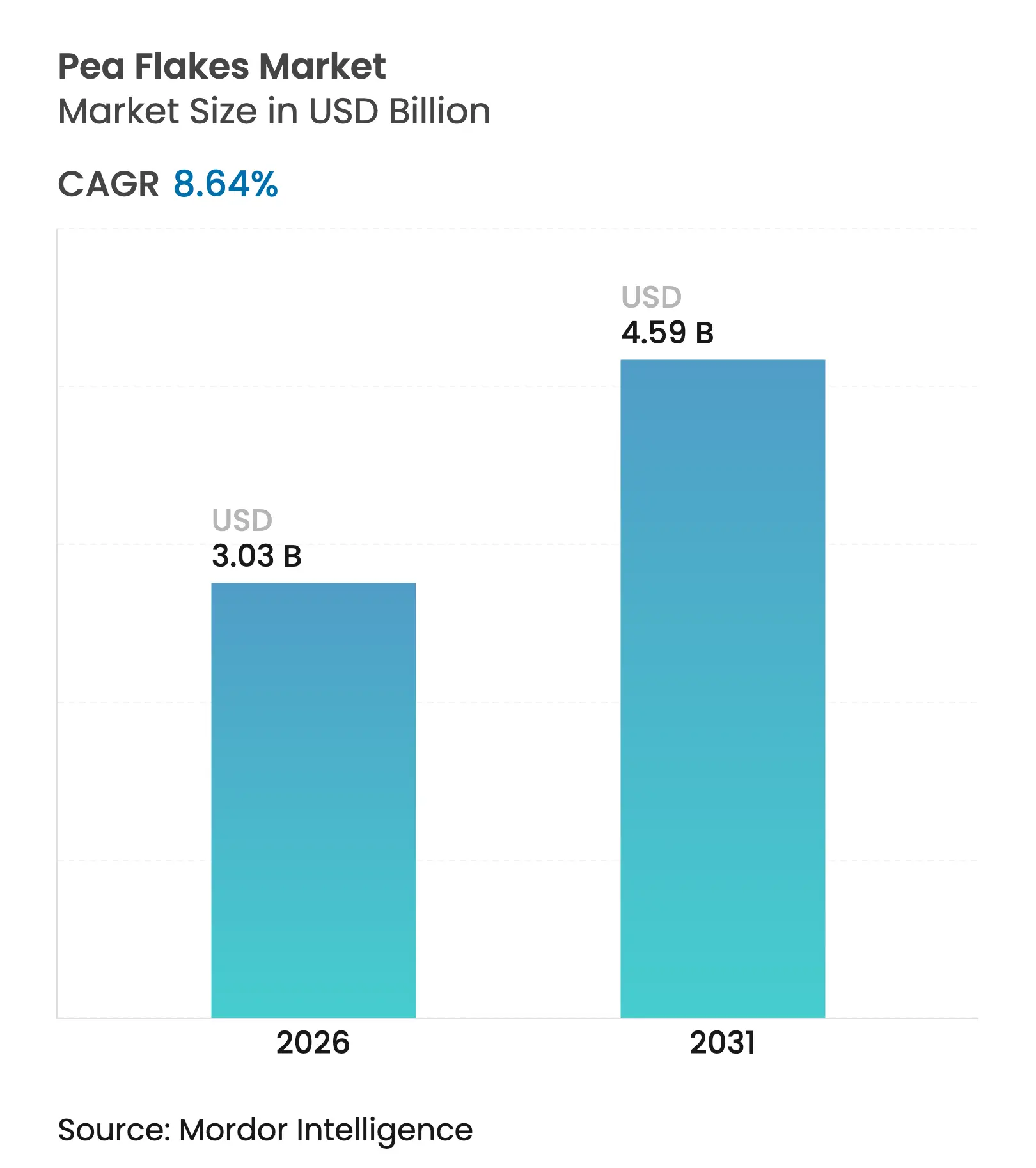

| Market Size (2026) | USD 3.03 Billion |

| Market Size (2031) | USD 4.59 Billion |

| Growth Rate (2026 - 2031) | 8.64 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Pea Flakes Market size market size in 2026 is estimated at USD 3.03 billion, growing from 2025 value of USD 2.79 billion with 2031 projections showing USD 4.59 billion, growing at 8.64% CAGR over 2026-2031. The market expansion is primarily driven by increasing consumer awareness of plant-based proteins, growing demand for sustainable food alternatives, and rising adoption in animal feed formulations. The market growth is further supported by the rising prevalence of veganism, technological advancements in food processing, and increasing incorporation of pea-based ingredients in convenience foods. The market demonstrates strong potential across both developed and emerging economies, supported by versatile applications in food manufacturing and animal nutrition. The increasing investment in research and development activities, coupled with innovations in processing technologies, has enhanced product quality and expanded application scope, while the growing emphasis on sustainable agriculture practices and rising demand for organic pea flakes present significant opportunities for market participants.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising demand for plant-based protein Rising demand for plant-based protein | +2.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.8% | Geographic Relevance:Global, with concentration in North America and Europe | Impact Timeline:Medium term (2-4 years) |

Growing awareness of gut and digestive health Growing awareness of gut and digestive health | +1.9% | Global, particularly developed markets | Long term (≥ 4 years) | |||

Rise in pet ownership Rise in pet ownership | +1.6% | North America, Europe, Asia-Pacific urban centers | Short term (≤ 2 years) | |||

Growing adoption in functional foods Growing adoption in functional foods | +1.4% | Europe, North America, with expansion to Asia-Pacific | Medium term (2-4 years) | |||

Expansion of pea-based feeds in aquaculture Expansion of pea-based feeds in aquaculture | +1.1% | Asia-Pacific, Europe, with emerging presence in Latin America | Long term (≥ 4 years) | |||

Growth in vegan and vegetarian lifestyles Growth in vegan and vegetarian lifestyles | +0.9% | Global, with highest penetration in developed markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand for Plant-Based Protein

The global pea flakes market is primarily driven by increasing demand for plant-based proteins, influenced by evolving dietary preferences, health consciousness, sustainability concerns, and ethical consumption choices. Pea flakes offer high protein content, good digestibility, and hypoallergenic properties, making them a viable alternative to soy and dairy-based proteins. Consumers in North America, Europe, and Asia-Pacific are increasingly choosing plant-derived proteins to reduce meat consumption, address health concerns, and support vegan and vegetarian diets. Pea flakes are utilized both as a direct ingredient in cereals, granola bars, and snacks, and as a base material for pea protein isolates and concentrates used in meat alternatives, protein powders, and functional beverages. According to Canada Statistics, India recorded the highest demand for plant-based protein ingredients in packaged food categories in 2023, with staple food products consuming 1,316 metric tonnes. This data indicates that emerging economies are driving business-to-business demand for ingredients like pea flakes, particularly in processed foods [1]Source: Canada Statistics, " Plant-based protein food and drink trends in India", www.canada.ca.

Growing Awareness of Gut and Digestive Health

The increasing recognition of gut and digestive health on overall well-being continues to drive substantial growth in the global pea flakes market. The gut microbiome demonstrates significant influence in regulating immune function, mood stability, and disease prevention mechanisms. The prevalence of gastrointestinal disorders, including irritable bowel syndrome (IBS), inflammatory bowel disease (IBD), and acid reflux, has generated considerable demand for digestive health-enhancing foods. According to the National Institutes of Health (NIH), inflammatory bowel disease (IBD) affected approximately 322,600 Canadians in 2023. Pea flakes contain substantial amounts of soluble and insoluble fiber that facilitate regular bowel movements and mitigate constipation symptoms. These dietary fibers support beneficial gut bacteria proliferation, establishing a robust and diverse gut microbiome that subsequently reduces inflammation and optimizes nutrient absorption. Furthermore, manufacturing entities have integrated pea flakes into diverse product formulations, including snacks, cereals, and fortified blends, responding to consumer requirements for minimally processed, functional foods specifically formulated to enhance gut health.

Rise in Pet Ownership

The global pea flakes market is experiencing growth due to increasing pet ownership worldwide. According to the American Pet Products Association (APPA), 66% of United States households owned pets in 2023/24, representing 86.9 million households [2]Source: American Pet Products Association (APPA), "latest pet ownership and spending data", https://americanpetproducts.org/. The pet food industry has adopted pea protein as a hypoallergenic substitute for conventional animal proteins to address food sensitivities and allergies in pets. Pet food manufacturers use precision fermentation technologies to produce proteins that match the amino acid profiles of animal sources while reducing contaminants and environmental impact. The growing trend toward premium pet nutrition increases the demand for functional ingredients, as pea protein offers comparable digestibility to traditional sources while providing additional benefits like fiber content and sustainability. The simplified regulatory requirements for alternative proteins in pet food, compared to human food applications, facilitate faster market adoption and generate early revenue opportunities for pea flakes manufacturers.

Growing Adoption in Functional Foods

The increasing incorporation of functional foods drives the global pea flakes market growth, as manufacturers and consumers seek ingredients that provide both nutrition and health benefits. Functional foods contain bioactive compounds that promote health beyond basic nourishment by supporting immune function, digestive health, and reducing chronic disease risks. Pea flakes contain plant-based protein, dietary fiber, vitamins, and minerals, making them suitable for functional food formulations. The high protein content in pea flakes supports muscle growth and recovery, attracting fitness enthusiasts and health-conscious consumers. The Food and Drug Administration (FDA)'s "Healthy" label initiative and various state-level nutrition incentive programs encourage the use of nutrient-dense ingredients in food products. These regulatory frameworks and public health initiatives create favorable conditions for market growth and innovation in the pea flakes market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Limited consumer awareness Limited consumer awareness | -1.8% | Global, particularly in emerging markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.8% | Geographic Relevance:Global, particularly in emerging markets | Impact Timeline:Short term (≤ 2 years) |

Functional limitations in food formulations Functional limitations in food formulations | -1.4% | Global, with higher impact in processed food applications | Medium term (2-4 years) | |||

Competition from alternative protein sources Competition from alternative protein sources | -1.1% | Global, with regional variations in protein preferences | Long term (≥ 4 years) | |||

Price volatility of raw materials Price volatility of raw materials | -0.90% | Europe, North America, with spillover effects globally | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Limited Consumer Awareness

Limited consumer awareness presents a significant restraint to the global pea flakes market, particularly in emerging markets where traditional protein sources remain predominant in dietary preferences. The acceptance of plant-based alternatives in these regions remains lower compared to developed markets. The market faces additional constraints as major industry players concentrate their marketing initiatives primarily on food manufacturers instead of end consumers, resulting in a disconnect between ingredient innovation and market demand. Furthermore, the absence of standardized regulatory frameworks for plant protein health claims in various regions restricts manufacturers from effectively conveying functional benefits to consumers. The complex nature of protein quality measurements, including Digestible Indispensable Amino Acid Score (DIAAS) and Protein Digestibility Corrected Amino Acid Scores (PDCAAS), requires simplified communication methods to effectively convey pea protein's nutritional advantages compared to conventional alternatives.

Functional Limitations in Food Formulations

The global pea flakes market faces significant restraints due to technical limitations in food formulation. Pea protein exhibits lower gel strength and emulsification capacity compared to dairy proteins, requiring extensive reformulation efforts. While heat treatment can improve solubility and emulsifying properties, it may compromise other functional characteristics essential for food applications. In high-moisture meat alternatives, achieving optimal textures remains challenging despite specific protein-starch interactions, even when using corn zein and rice starch combinations. The inherent yellow-green color and earthy flavor notes of pea protein restrict its application across various food categories. Furthermore, the transition from laboratory to industrial-scale production presents additional challenges, particularly regarding protein functionality, thermal stability, and ingredient interactions during extended storage periods.

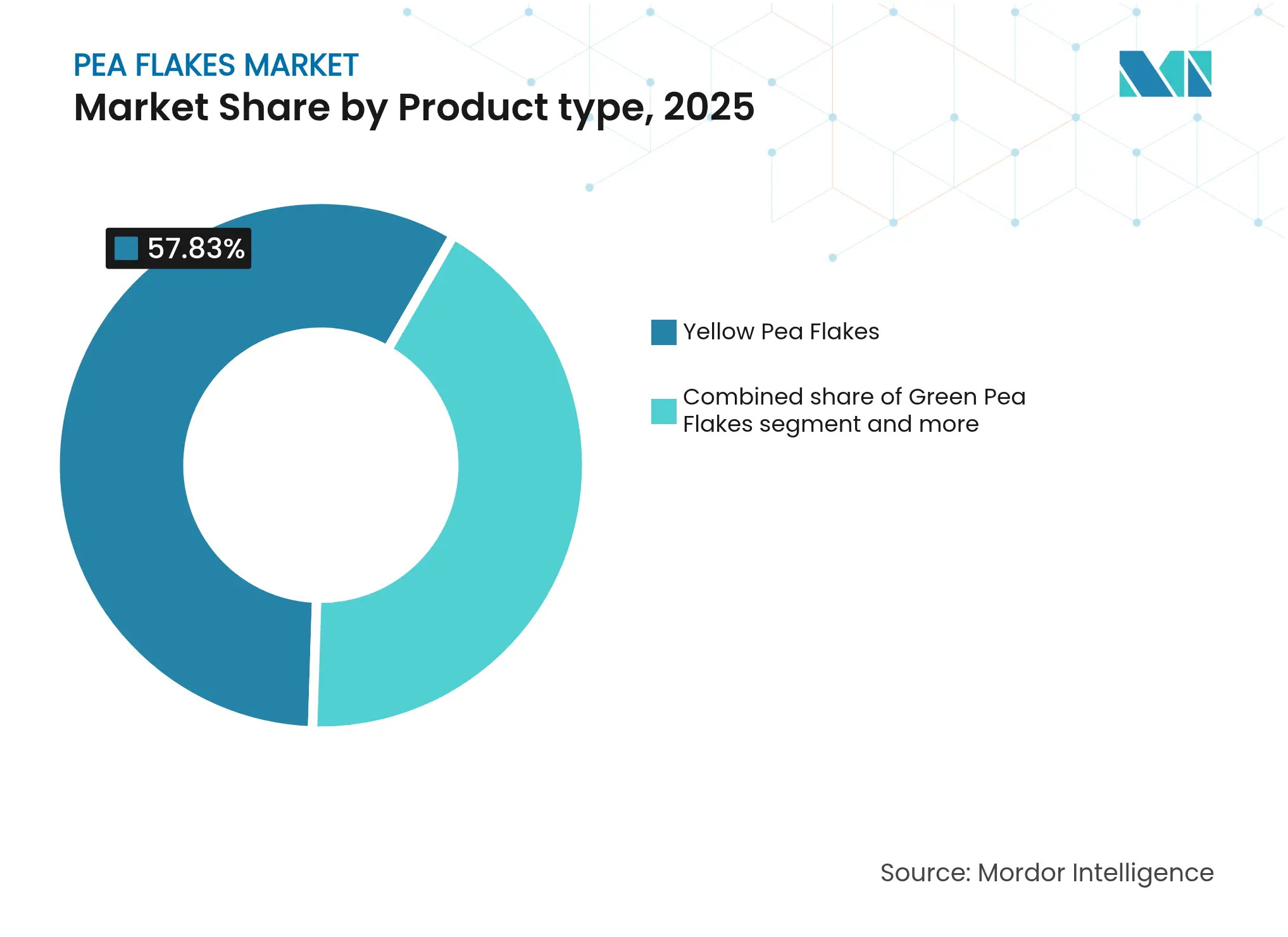

By Type: Yellow Dominance Drives Market Leadership

Yellow pea flakes maintain a significant 57.83% market share in 2025, driven by robust supply chain infrastructure and substantially higher protein content compared to alternative varieties. Their market dominance is attributed to the scientifically validated protein concentration and amino acid composition that effectively meet human nutritional requirements. The industrial-scale processing capabilities, particularly advanced dry fractionation methodologies, ensure consistent protein purity while maintaining structural integrity and functional properties essential for commercial food applications.

Speckled/maple pea flakes demonstrate substantial market growth with an 10.79% CAGR through 2031, primarily due to increasing consumer demand for alternative protein sources and technological advancements in processing methods. These varieties exhibit market expansion through documented improvements in digestibility and nutritional profiles, supported by systematic breeding programs focused on protein enhancement and antinutritional factor reduction. Green pea flakes maintain a stable market position in premium organic segments, driven by consumer preferences for natural ingredients and the increasing demand for visually appealing plant-based products in the health food sector.

Note: Segment shares of all individual segments available upon report purchase

By Processing Technique: Steam-Rolling Maintains Traditional Leadership

Steam-rolled pea flakes hold a dominant 66.07% market share in 2025, supported by established processing infrastructure and cost advantages. Meanwhile, extruded/instantised variants demonstrate strong growth at 10.58% CAGR, driven by their superior texture properties and enhanced digestibility in food applications. The traditional steam-rolling process provides economic efficiency and scalability by using controlled temperature and pressure to flatten peas while maintaining nutritional value and extending shelf life through moisture reduction. The mature steam-rolling equipment infrastructure and operator expertise create entry barriers for alternative processing methods, especially in animal feed applications where functional requirements are less demanding than human food uses.

Extrusion and instantisation technologies are gaining adoption due to their ability to modify protein structure and enhance functional properties, including improved solubility, emulsification capacity, and texture development essential for meat alternatives. High-moisture extrusion cooking shows particular effectiveness in creating fibrous meat analogues, with processing variables such as temperature, moisture content, and screw speed influencing the final product texture and consumer acceptance. Industry investment in advanced processing capabilities indicates that improved texture and functionality justify increased processing costs, particularly in premium food applications where these characteristics directly impact consumer acceptance and price premiums.

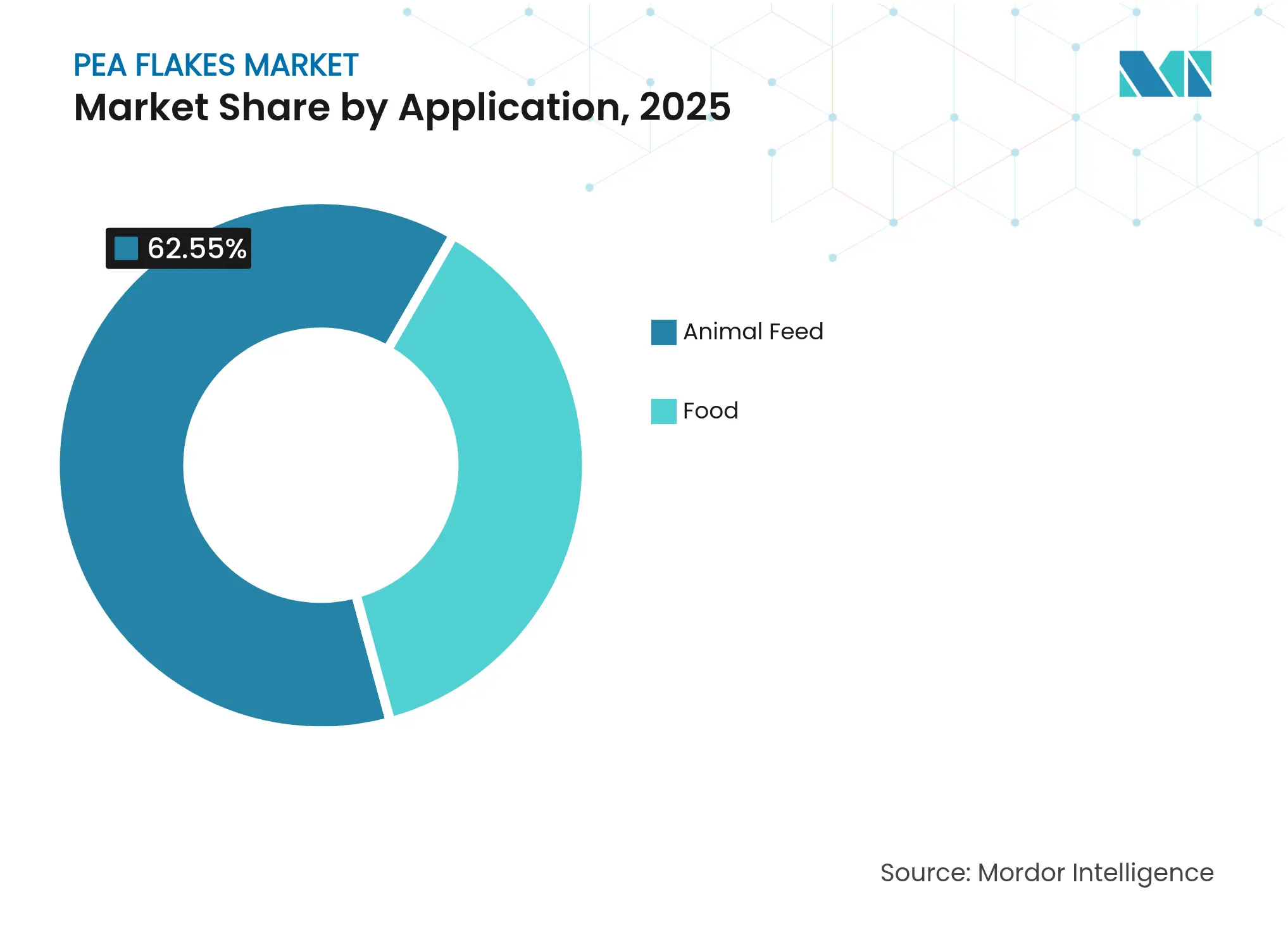

By Application: Animal Feed Leadership Faces Food Segment Challenge

Animal feed applications command 62.55% of the market share in 2025, primarily driven by several key factors. The segment's dominance is attributed to increasing livestock production, rising demand for protein-rich animal nutrition, and stringent regulations on feed quality standards. Additionally, the cost-effectiveness and well-established supply chains further strengthen its market position. The animal feed segment leverages pea flakes' high protein content and superior digestibility compared to traditional grain-based feeds. In response to the growing prevalence of pet food allergies and dietary sensitivities, pet food manufacturers are systematically incorporating pea protein as a hypoallergenic alternative in their formulations.

Food applications are projected to grow at a 9.96% CAGR through 2031, driven by functional food development and increased health consciousness. This growth spans breakfast cereals, bakery products, snacks, and ready meals, where manufacturers use pea flakes for protein fortification and texture enhancement. In bakery applications, pea protein serves as an emulsifier and nutritional enhancer, particularly beneficial in gluten-free products where maintaining protein content is challenging. The snack food segment has evolved through extrusion processing, creating pea-based products that offer improved texture and nutritional value, meeting the demand for healthier convenience foods.

Note: Segment shares of all individual segments available upon report purchase

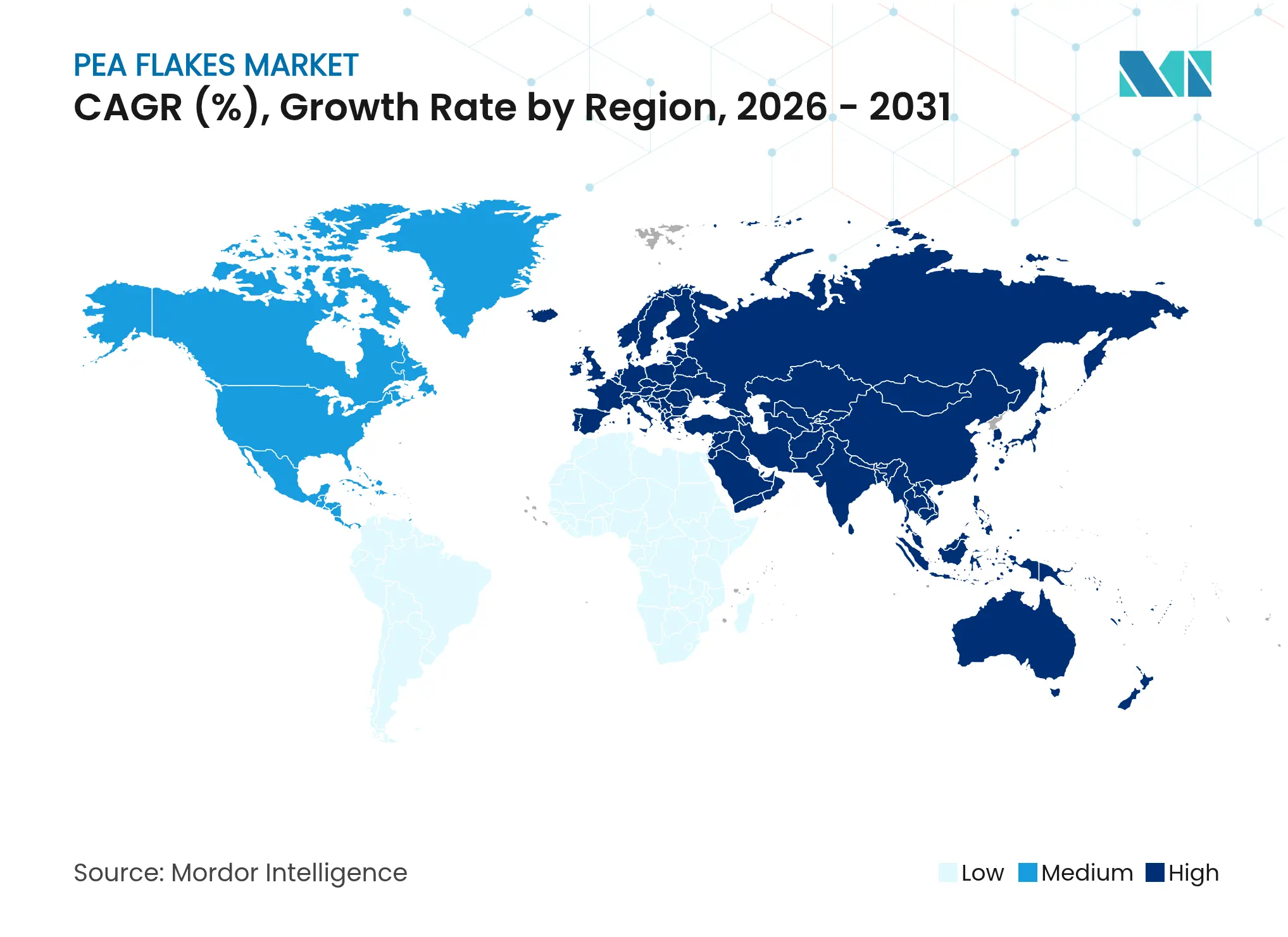

Europe holds 33.94% market share in 2025 through its established pulse processing infrastructure and regulatory support for plant protein development. The region's leadership stems from decades of investment in pulse processing technology and agricultural systems optimized for pea cultivation. Countries like France and Germany lead production while maintaining strict quality standards that enhance export competitiveness. In November 2023, the Budget Committee of the German Bundestag announced funding of EUR 38 million in 2024 for the sustainable protein transition, supporting domestic pea protein production and processing capabilities.

Asia-Pacific registers the fastest growth rate at 11.02% CAGR, driven by urbanization, rising incomes, and increasing health consciousness among consumers. The region's growth stems from rapid urbanization and dietary transitions toward protein-rich foods, with plant-based alternatives gaining acceptance. China's position in the global pea protein trade faces challenges from the United States' tariffs imposing 280.31% dumping rates, creating opportunities for regional producers while reshaping global supply chains . India shows market potential due to its growing middle-class population and increasing awareness of plant-based nutrition benefits, though infrastructure development and consumer education remain essential.

The North American region, particularly the United States and Canada's prairie provinces, contributes significantly to the global pea flakes market due to its proximity to major pea cultivation zones. Canada maintains its position as the world's largest producer and exporter of field peas, with production reaching 43,110 metric tons of fresh peas in 2023, according to Canada Statistics. This geographic advantage ensures a consistent, cost-efficient, and traceable supply of raw material for pea flakes and other value-added pea-based products. The Middle East and Africa present growth opportunities driven by population growth and economic development, though market penetration faces challenges from infrastructure limitations and developing regulatory frameworks for plant-based protein products.

Market Concentration

The pea flakes market exhibits moderate fragmentation. This market structure facilitates competition between established companies, leveraging operational scale advantages, and emerging firms pursuing technological innovation and specialized market segments. The competitive environment is dominated by key market participants, including Roquette Frères, Inland Empire Foods Inc., Gemef Industries, and Emsland Group, who maintain their positions through comprehensive value chains encompassing agricultural procurement, processing advancement, and application development.

The industry demonstrates significant capital allocation toward technological advancement, particularly in processing equipment and extraction methodologies. This investment pattern reflects the market's emphasis on operational efficiency and product quality optimization. Market leaders have established robust research and development capabilities, enabling them to maintain technological superiority and meet evolving industry standards.

The competitive landscape is further shaped by strategic integration initiatives across the value chain. Companies are actively pursuing vertical integration through agricultural production expansion and finished product development, while simultaneously implementing horizontal growth strategies. These expansion efforts focus on diversifying protein sources and processing technologies, enabling market participants to broaden their operational scope and reduce dependency on singular ingredient categories.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE and GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

The global pea flakes market is segmented by type into green pea and yellow pea market. Based on the application, the market is segregated as animal feed, processed foods, aquafeed, and others. By Distribution Channel, the market segments are hypermarket/supermarket, convenience stores, online stores, and others. Moreover, the market is segmented by geography.

Market Analysis of Synthetic Food Colorants for a Beverage Leader

5 Min Read

US Market Entry for Taiwanese Machine Tool Manufacturers

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.