United States Data Center Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

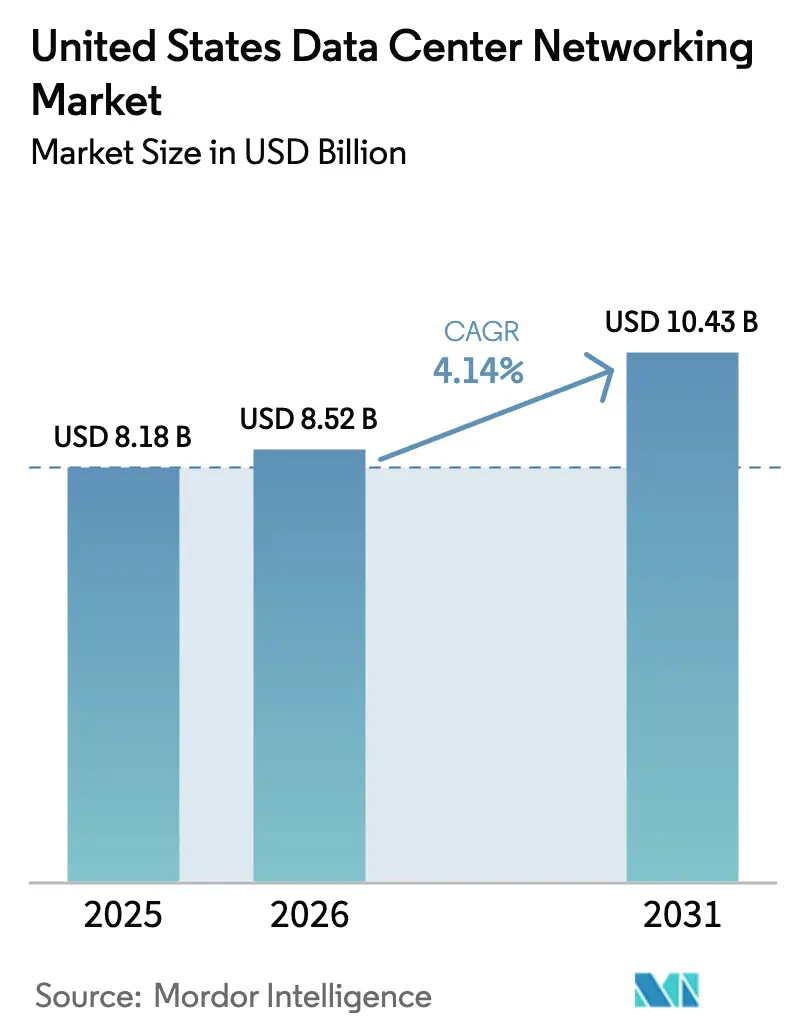

| Base Year Market Size (2025) | USD 8.18 Billion |

| Market Size (2026) | USD 8.52 Billion |

| Market Size (2031) | USD 10.43 Billion |

| Growth Rate (2026 - 2031) | 4.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Data Center Networking Market Analysis by Mordor Intelligence

The United States data center networking market size is expected to grow from USD 8.18 billion in 2025 to USD 8.52 billion in 2026 and is forecast to reach USD 10.43 billion by 2031 at 4.14% CAGR over 2026-2031. Growth stems from hyperscale operators that continue to absorb high-density switching, 400G/800G optics, and AI-ready fabrics to support large language models demanding ultra-low latency. The manufacturing surge tied to Industry 4.0 projects, the continued rollout of 5G edge sites, and government support through Executive Order 14179 further intensify demand. Meanwhile, services revenue is rising because many enterprises lack the skills to manage complex optical migrations or zero-trust micro-segmentation. Supply chain bottlenecks, water-usage restrictions, and rising upgrade costs temper expansion but have not reversed the upward trajectory.

Key Report Takeaways

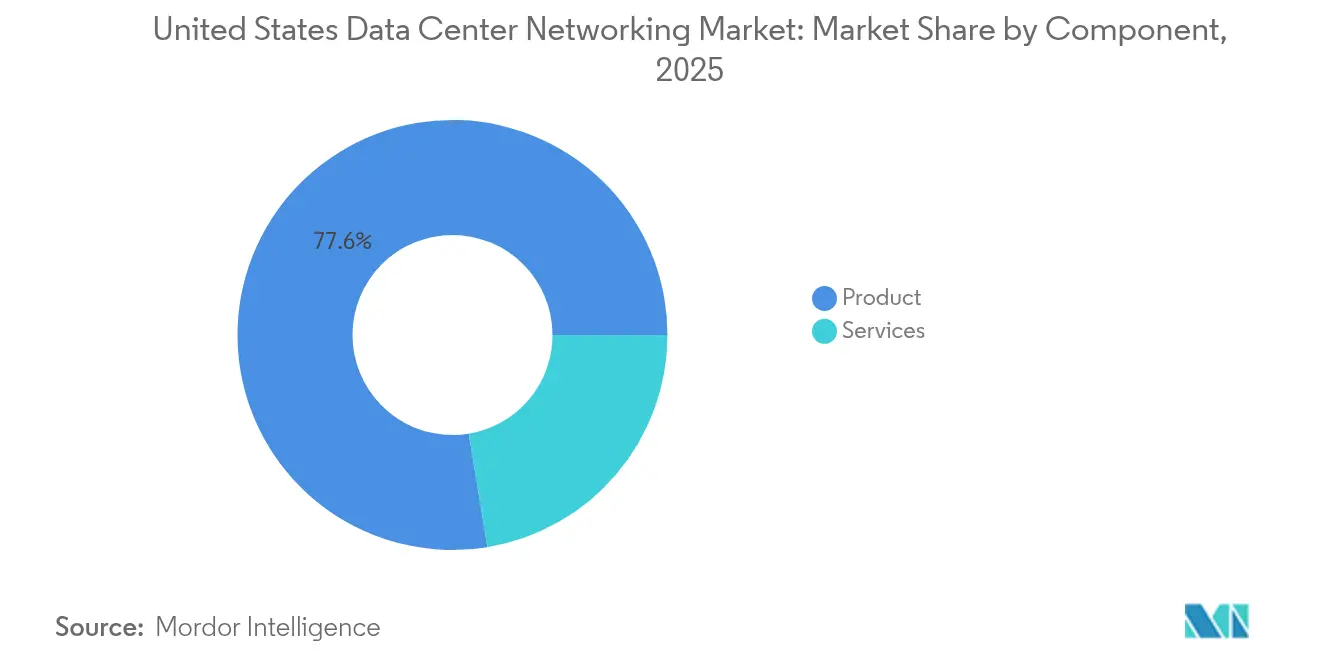

- By component, products led with 77.60% revenue share in 2025, while services are projected to expand at a 4.32% CAGR through 2031.

- By end-user, IT and telecom held 34.15% of the United States data center networking market share in 2025; manufacturing is poised for the fastest 5.08% CAGR to 2031.

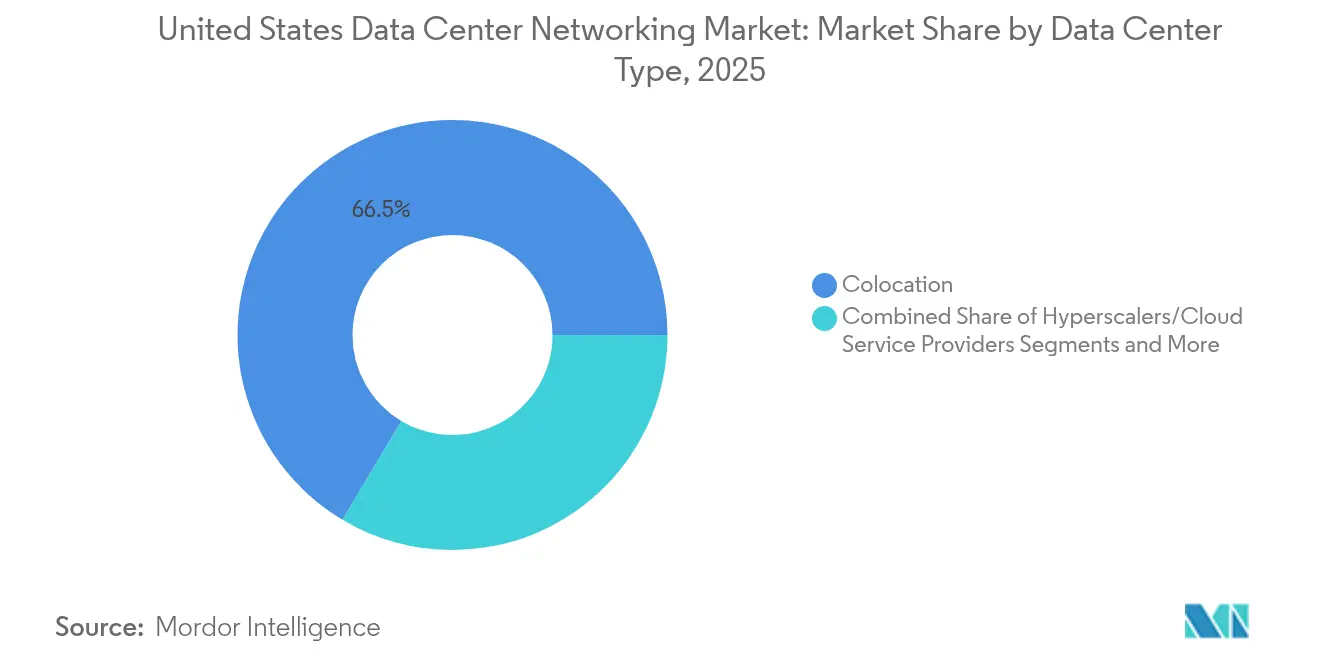

- By data-center type, colocation facilities accounted for 66.45% share in 2025, yet hyperscale deployments are forecast to grow at a 5.85% CAGR.

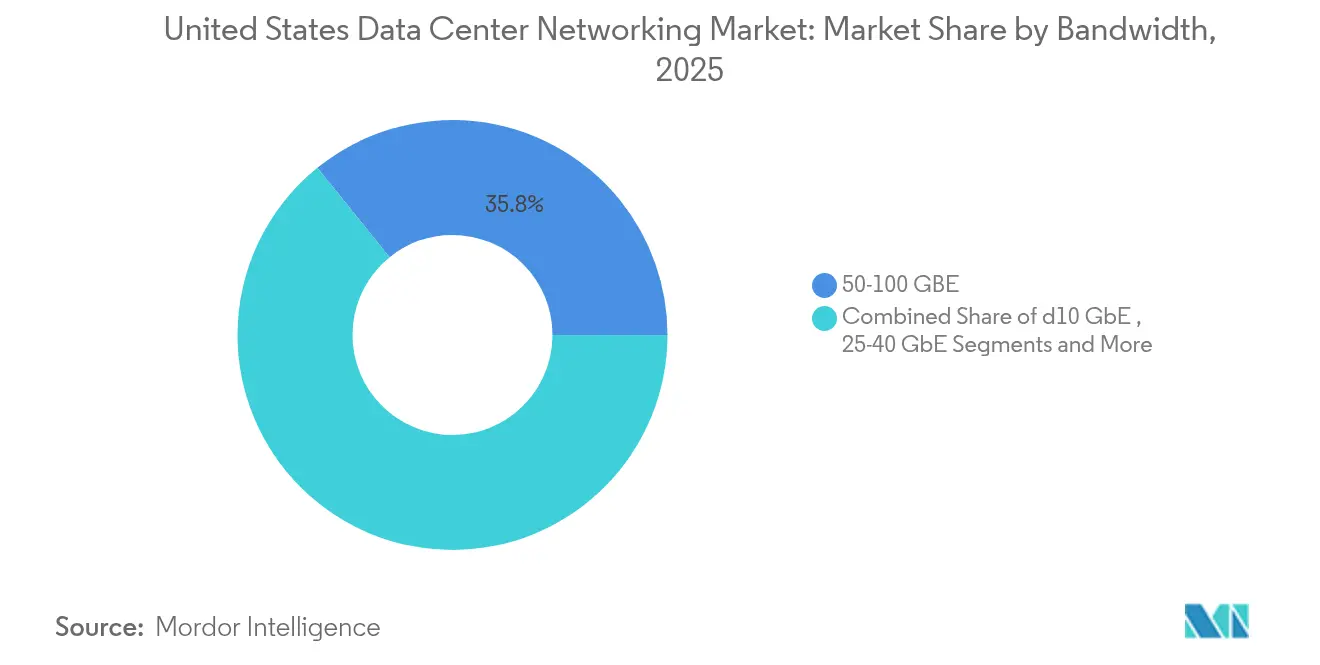

- By bandwidth, the 50-100 GbE category commanded 35.82% share of the United States data center networking market size in 2025, while the greater than 100 GbE segment is advancing at a 5.49% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Each country contributes a share rather than an absolute position, and United states is evaluated within that framework. The data center networking market share in Mordor Intelligence's global report defines how those shares are distributed worldwide.

United States Data Center Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in hyperscale and AI-driven bandwidth demand | +0.6% | Northern Virginia, Silicon Valley, Phoenix | Medium term (2-4 years) |

| Migration to 400G/800G Ethernet fabrics | +0.5% | Major hyperscale regions | Short term (≤2 years) |

| Expansion of edge and 5G micro-data-centers | +0.4% | Metropolitan areas nationwide | Long term (≥4 years) |

| State energy-efficiency incentives | +0.3% | CA, NY, WA, TX | Medium term (2-4 years) |

| Adoption of CXL-enabled disaggregated designs | +0.3% | AI research hubs nationwide | Long term (≥4 years) |

| Zero-trust push for fabric micro-segmentation | +0.3% | Government and enterprise sites | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Surge in Hyperscale and AI-driven Bandwidth Demand

Hyperscale operators are rebuilding networks to serve AI workloads that move 10-100 times more data than legacy applications. Meta’s adoption of Arista 7700R4 platforms for training clusters highlights the spread of non-blocking, terabit-scale east-west fabrics that reduce latency for distributed GPUs. Microsoft’s USD 80 billion AI build-out and AWS’s USD 30 billion expansion reinforce the steep equipment pull for AI-specific switches, optics, and NICs. Custom silicon from NVIDIA and AMD underlines operators’ desire to bypass general-purpose devices in favor of tightly integrated 800G parts.[1]NVIDIA Corp., “800G Networking Roadmap,” nvidia.com

Migration to 400G/800G Ethernet Fabrics

The jump to 400G and 800G is the largest step since 10 GbE, driven by GPU clusters that saturate 100G links. Broadcom’s Tomahawk 6 supports 1.6 Tb/s ports, anticipating future headroom. The Ultra Ethernet Consortium ratified UEC 1.0 in June 2025, adding packet-spraying and in-network compute specifically for AI traffic. Rollouts face 18-month lead times for 800G optics, constraining some hyperscale buildouts until production ramps in 2026.

Expansion of Edge and 5G Micro-data-centers

Edge sites require compact, high-density switches that tolerate harsh environments yet deliver hyperscale speed. DE-CIX Dallas completed a 400 GE upgrade that showcases rising interconnection traffic at the metro edge. These edge nodes open new revenue for vendors able to pre-assemble automation and remote-management features that offset the shortage of on-site engineers. Industrial automation and connected vehicle pilots are driving much of the early traffic uplift.

State Energy-efficiency Incentives for Smart Fabrics

California’s Title 24 and companion rules in New York and Washington reward operators that cut network power draw with automated traffic engineering.[2]ACEEE, “Data Center Energy Code Analysis 2025,” aceee.org Networking gear consumes 10-15% of facility electricity; dynamic path optimization can trim that load by 20-30%. Healthcare systems such as RWJBarnabas Health reported double-digit power savings after deploying fabric-wide energy controls.

Restraints Impact Analysis*

| Restraint | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Optical transceiver and ASIC supply bottlenecks | −0.3% | Hyperscale clusters nationwide | Short term (≤2 years) |

| High capex for 10/40 G greater than 400 G upgrades | −0.3% | Enterprise campuses nationwide | Medium term (2-4 years) |

| Water-usage limits curbing hyperscale growth | −0.2% | AZ, GA, VA, CO | Long term (≥4 years) |

| Scarcity of automation-skilled engineers | −0.1% | Secondary metro areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Optical Transceiver and ASIC Supply Bottlenecks

Lead times on 800G modules have stretched to 18 months as manufacturers prioritize AI-grade optics with ultra-low jitter. Lumentum shifted its roadmap to serve this niche, demonstrating the squeeze on conventional transceiver lines.[3]Lumentum Holdings, “Q2 2025 Earnings Call Transcript,” lumentum.com Tariff impacts added 8-20% to equipment costs, prompting some enterprises to defer upgrades and sweat 100G assets longer than planned.

High Capex for Legacy 10/40 G Greater Than 400 G Upgrades

Upgrading a full fabric requires new switches, structured cabling, optics, power, and cooling. Deutsche Bank’s single-site refresh exceeded USD 50 million, underscoring the financial barrier for mid-market firms. Facility retrofits regularly double equipment spend, delaying projects unless clear ROI ties to latency-sensitive workloads exist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Products Dominance Amid Services Acceleration

Products continued to hold 77.60% of 2025 revenue as hyperscalers bought thousands of fixed-form-factor switches. Ethernet switches remained the anchor category, while software-defined controllers gained favor for policy automation. Storage-area networking equipment lost momentum as disaggregated architectures separated compute and storage across high-speed optics. Network security appliances regained focus because zero-trust designs require pervasive segmentation.

The services slice is climbing at a 4.32% CAGR as clients seek design, integration, and managed support for multi-vendor 400G/800G fabrics. Installation teams coordinate timing-sensitive optics, while managed services offset scarce in-house automation skills. Training and consulting firms address a widening talent gap around AI-specific network tuning. The United States data center networking market increasingly rewards providers that bundle hardware, optics, and expertise under outcome-based contracts.

By End-User: IT-Telecom Leadership Challenged by Manufacturing Surge

IT-telecom operators retained a 34.15% share in 2025, anchored by early 5G core deployments and public-cloud backbone refreshes. Financial institutions followed, upgrading latency paths for algorithmic trading. Manufacturing, however, is posting a 5.08% CAGR as Industry 4.0 plants retrofit with real-time analytics and robotic lines. Automotive giants are installing deterministic fabrics that blend industrial protocols with enterprise traffic.

Government and defense agencies are modernizing classified networks to enable secure AI model training. Healthcare providers expand bandwidth for diagnostic imaging and electronic records. Media firms push 4K/8K pipelines that need burst capacity and jitter control. The United States data center networking market is therefore becoming a patchwork of vertical use cases rather than a monolithic telecom-led domain.

By Data-Center Type: Colocation Stability Versus Hyperscale Innovation

Colocation sites supplied 66.45% of 2025 revenue as enterprises outsourced racks yet kept control of gear. Operators are upgrading meet-me rooms with 100G cross-connects and offering GPU clusters as a service. Hyperscalers, though smaller in count, are generating a 5.85% CAGR on massive AI clusters. EdgeCore’s USD 17 billion Virginia campus typifies investments that stack compute near renewable power and fiber hubs. Edge and micro data centers emerge as a third pathway, inserting compact nodes in cell-tower shelters and factory floors. These locations need ruggedized switches and zero-touch provisioning. The United States data center networking market therefore splits between steady colocation revenue, hyper-growth cloud builds, and nascent edge nodes that could scale rapidly once automation matures.

By Bandwidth: 50-100 GbE Dominance Facing Greater Than 100 GbE Disruption

The 50-100 GbE tier held 35.82% share in 2025 because it balances cost and performance for most enterprise racks. Yet >100 GbE links are expanding at 5.49% CAGR as AI clusters adopt 400G spines and 800G trials. ≤10 GbE remains for legacy workloads and edge telemetry, while 25-40 GbE often gets skipped. Ciena’s WaveLogic 6 optics deliver 1.6 Tb/s line rates, foreshadowing terabit Ethernet backbones. Multi-speed fabrics mixing 100G leafs with 400G spines create configuration complexity that drives demand for telemetry and AI-based traffic engineering. The United States data center networking market size tied to >100 GbE is expected to widen materially as hyperscalers absorb terabit uplinks by 2027.

Geography Analysis

Northern Virginia anchors the United States data center networking market with the world’s largest concentration of facilities serving both public cloud and federal workloads. Silicon Valley follows as the primary innovation lab where vendors trial optical ASICs and programmable DPUs. The West Coast—spanning California, Washington, and Oregon—offers renewable power and tax incentives, yet rising water-usage limits challenge expansion plans.

Texas and other Southern states lure operators with competitive land and power rates. However, grid reliability in ERCOT and storm exposure require resilient designs that include automated reroute paths and on-site generation. Executive Order 14179 opens federal land in the Midwest and Mountain regions, promising clean-energy campuses that will diversify build patterns.

Regulatory divergence matters. Arizona, Georgia, and Virginia now cap water draws, pushing liquid-cooling adoption. FERC reviews for co-located generation in the PJM market highlight how rising peak load from AI clusters, forecast to hit 184 GW by 2030, could strain transmission lines. The United States data center networking market therefore mirrors a patchwork of power, water, and tax considerations that influence fabric design and deployment timelines.

Mordor Intelligence's coverage of the data center networking market extends across other regions including South America, Middle East, and Asia, while country-specific intelligence is also available for Brazil, Mexico, Israel, South Korea, Austria, and China, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The United States data center networking market shows moderate concentration. Cisco, Arista, Juniper, and HPE still control the bulk of switch ports, yet their combined share leaves room for challengers. Arista surpassed USD 2 billion quarterly revenue in Q1 2025 by leaning into AI cluster fabrics. Cisco counters with Nexus platforms embedding Hypershield security for zero-trust enforcement.

Broadcom dominates merchant silicon with Tomahawk and Trident lines, while Marvell pushes PCIe Gen 6 over optics for disaggregated racks. Ultra Ethernet and UALink consortia open paths for start-ups to ship AI-centric fabrics that undercut proprietary NVLink. Traditional incumbents race to embed telemetry, programmable pipelines, and DPU-offload features to differentiate beyond port counts.

Edge networking remains fragmented. Vendors that ruggedize hardware and pre-load automation win early pilots with telcos and manufacturers. Optical module suppliers confront consolidation as AI-grade specs narrow approved vendor lists. The competitive field rewards firms that bundle silicon, optics, and software into turnkey fabric-as-a-service offerings.

United States Data Center Networking Industry Leaders

Cisco Systems, Inc.

Arista Networks, Inc.

Juniper Networks, Inc.

Dell Technologies, Inc.

Hewlett Packard Enterprise (HPE)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: EdgeCore announced a USD 17 billion Virginia campus aimed at AI-optimized data centers.

- June 2025: The Ultra Ethernet Consortium released Specification 1.0 for AI and HPC traffic.

- June 2025: Broadcom unveiled Tomahawk 6 with 1.6 Tb/s switching capacity.

- May 2025: HPE launched the CX 10040 distributed services switch integrating AMD Pensando DPUs.

United States Data Center Networking Market Report Scope

Data center networking refers to the set of technologies, protocols, and hardware used to connect physical and network-based devices and manage the network infrastructure, storage, and processing of applications and data. Data center networking is very critical for 100% uptime of data centers. In the current web-connected world, business workloads are executed on single computers, hence leading to the need for data center networking. Networks provide servers, clients, applications, and middleware with a standard plan to stage the execution of workloads and also to manage access to the data produced.

The United States data center networking market is segmented by product (ethernet switches, routers, storage area network (SAN), application delivery controllers (ADC), and other networking equipment), by services (installation & integration, training & consulting, and support & maintenance), and by end-user (IT & telecommunication, BFSI, government, media & entertainment, and other end users). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Products | Ethernet Switches |

| Routers | |

| Storage Area Network (SAN) | |

| Application Delivery Controllers (ADC) | |

| Network Security Appliances | |

| Software-Defined Networking (SDN) Controllers | |

| Optical Interconnects | |

| Services | Installation and Integration |

| Training and Consulting | |

| Support and Maintenance | |

| Managed Network Services |

| IT and Telecommunications |

| Banking, Financial Services and Insurance (BFSI) |

| Government and Defense |

| Media and Entertainment |

| Healthcare and Life Sciences |

| Manufacturing and Industrial |

| Other End-Users |

| Colocation |

| Hyperscalers/Cloud Service Providers |

| Edge/Micro Data Centers |

| Less Than or Equal to10 GbE |

| 25-40 GbE |

| 50-100 GbE |

| Greater Than 100 GbE |

| By Component | Products | Ethernet Switches |

| Routers | ||

| Storage Area Network (SAN) | ||

| Application Delivery Controllers (ADC) | ||

| Network Security Appliances | ||

| Software-Defined Networking (SDN) Controllers | ||

| Optical Interconnects | ||

| Services | Installation and Integration | |

| Training and Consulting | ||

| Support and Maintenance | ||

| Managed Network Services | ||

| By End-User | IT and Telecommunications | |

| Banking, Financial Services and Insurance (BFSI) | ||

| Government and Defense | ||

| Media and Entertainment | ||

| Healthcare and Life Sciences | ||

| Manufacturing and Industrial | ||

| Other End-Users | ||

| By Data-Center Type | Colocation | |

| Hyperscalers/Cloud Service Providers | ||

| Edge/Micro Data Centers | ||

| By Bandwidth | Less Than or Equal to10 GbE | |

| 25-40 GbE | ||

| 50-100 GbE | ||

| Greater Than 100 GbE | ||

Key Questions Answered in the Report

What is the current size of the United States data center networking market?

The market stands at USD 8.52 billion in 2026 and is projected to reach USD 10.43 billion by 2031.

Which segment is growing fastest within this market?

Hyperscale cloud deployments are expanding at a 5.85% CAGR due to massive AI cluster investments.

Why are 400G and 800G upgrades important now?

AI workloads and east-west traffic saturate 100G links, making 400G/800G fabrics essential for low-latency GPU communication.

What regions lead new data center builds in the United States?

Northern Virginia and Silicon Valley host the highest facility density, while Texas and select Midwest states are gaining share due to favorable power rates.

Page last updated on: