Data Center Networking Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

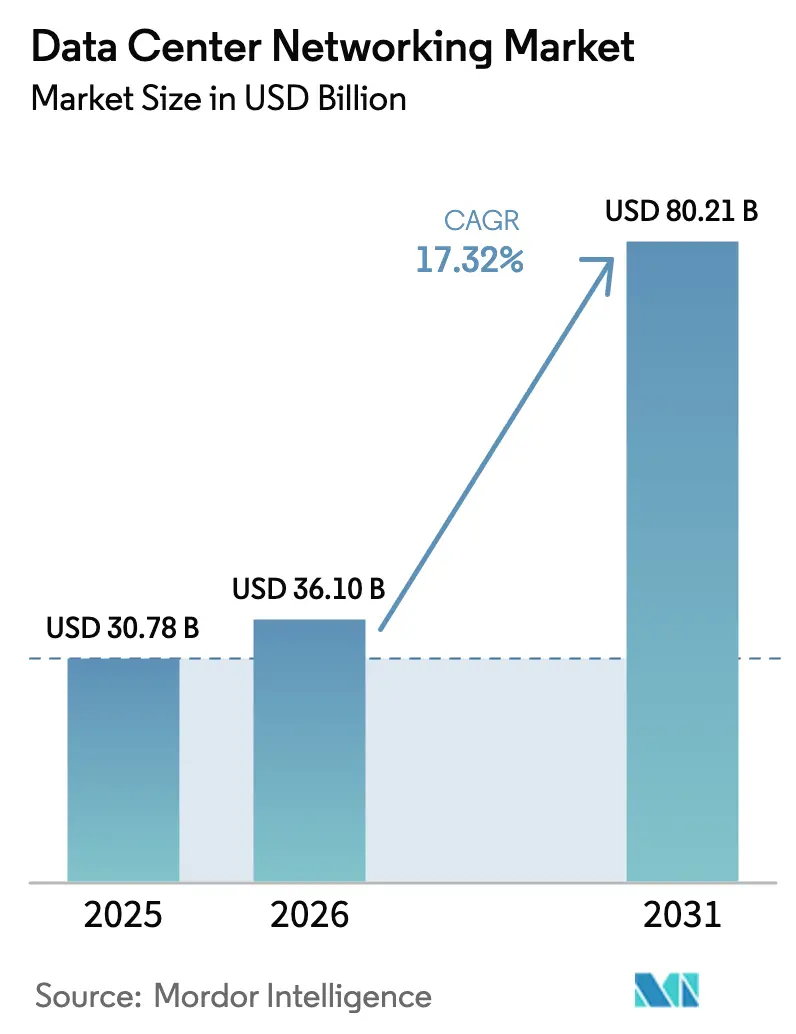

| Market Size (2026) | USD 36.1 Billion |

| Market Size (2031) | USD 80.21 Billion |

| Growth Rate (2026 - 2031) | 17.32% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Data Center Networking Market Analysis by Mordor Intelligence

The global data center networking market size is expected to grow from USD 30.78 billion in 2025 to USD 36.1 billion in 2026 and is forecast to reach USD 80.21 billion by 2031 at 17.32% CAGR over 2026-2031. The data center networking market is expanding because enterprises are redesigning three-tier networks into AI-optimized fabrics that reduce east-west congestion and shorten model-training times. Growing hyperscale investments, rapid 400 GbE price erosion, and government-led digital sovereignty initiatives are accelerating new-build projects in both developed and emerging economies. Vendor competition now pivots on lossless Ethernet capabilities, merchant-silicon roadmaps, and ecosystem partnerships that simplify AI cluster deployment. Power density constraints and supply chain dependencies on switching ASICs pose the primary structural risks to growth.

Key Report Takeaways

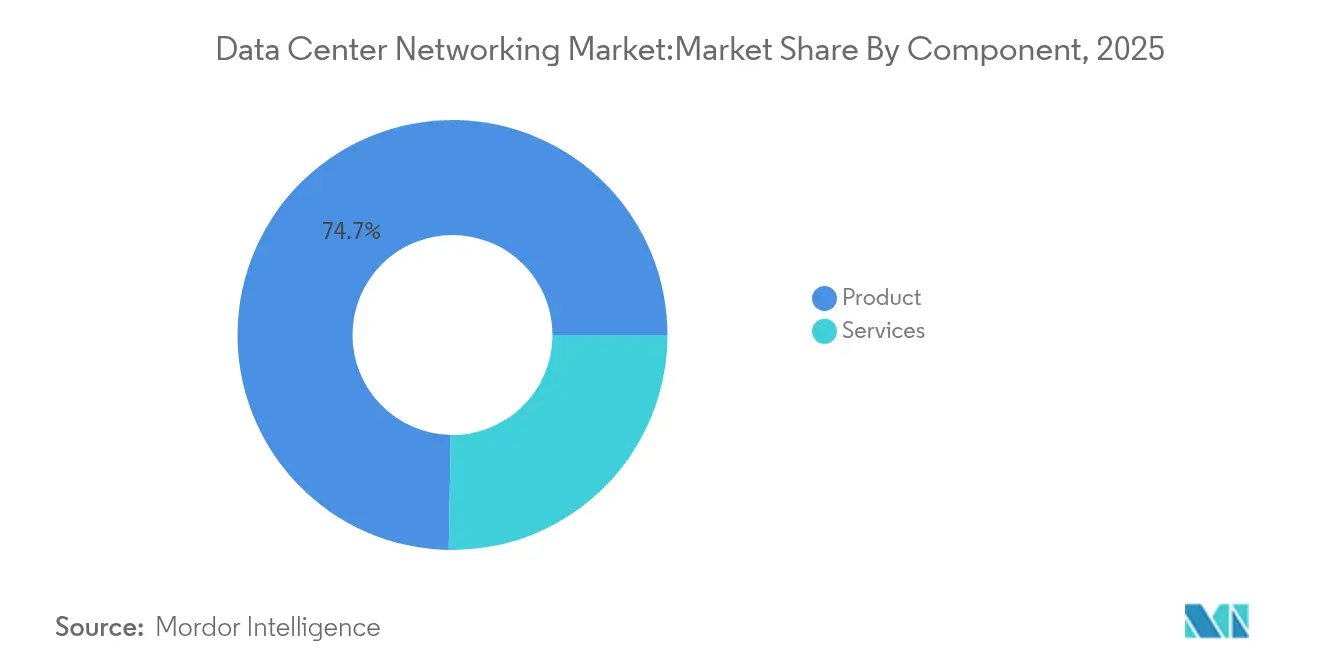

- By component, products led with 74.72% data center networking market share in 2025, while Services is projected to expand at a 17.7% CAGR to 2031.

- By end-user, IT and Telecommunications held 35.75% of the data center networking market size in 2025; Manufacturing and Industrial is forecast to grow at an 18.05% CAGR through 2031.

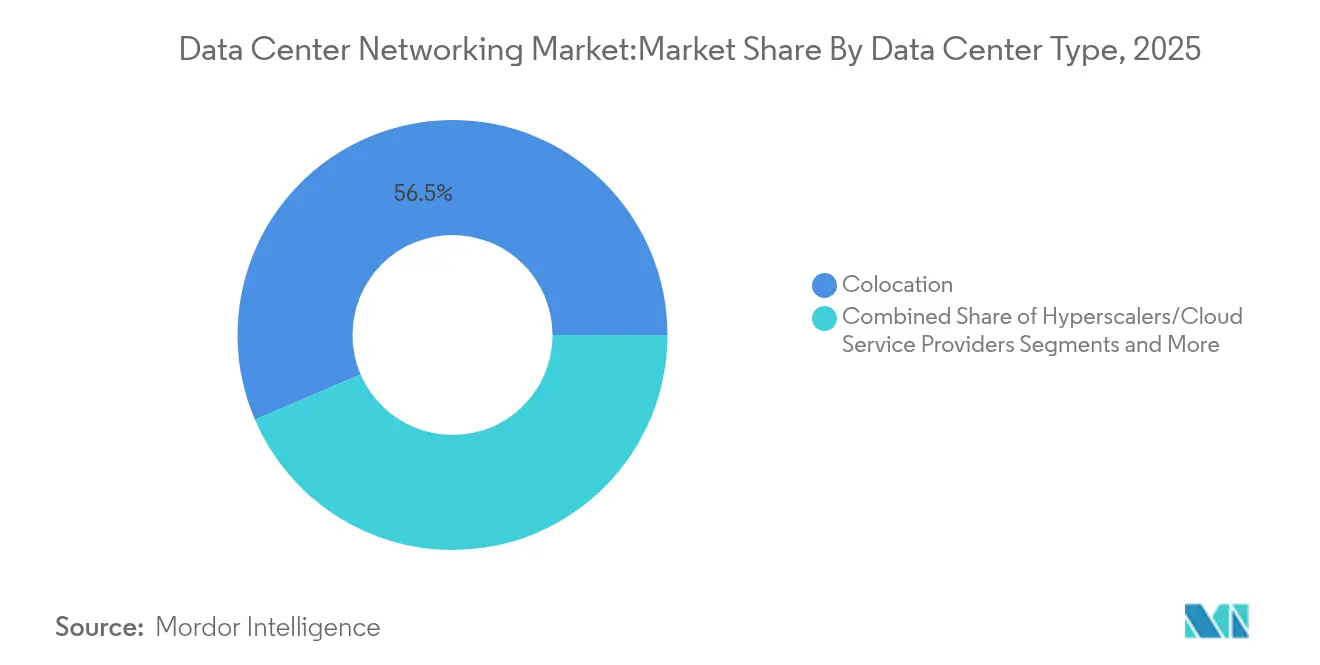

- By data-center type, colocation accounted for 56.45% of the data center networking market size in 2025; Hyperscaler/Cloud Service Provider facilities will advance at a 19.05% CAGR to 2031.

- By bandwidth, the 50–100 GbE class commanded 38.15% share of the data center networking market size in 2025, whereas ports above 100 GbE will increase at an 17.74% CAGR between 2026 and 2031.

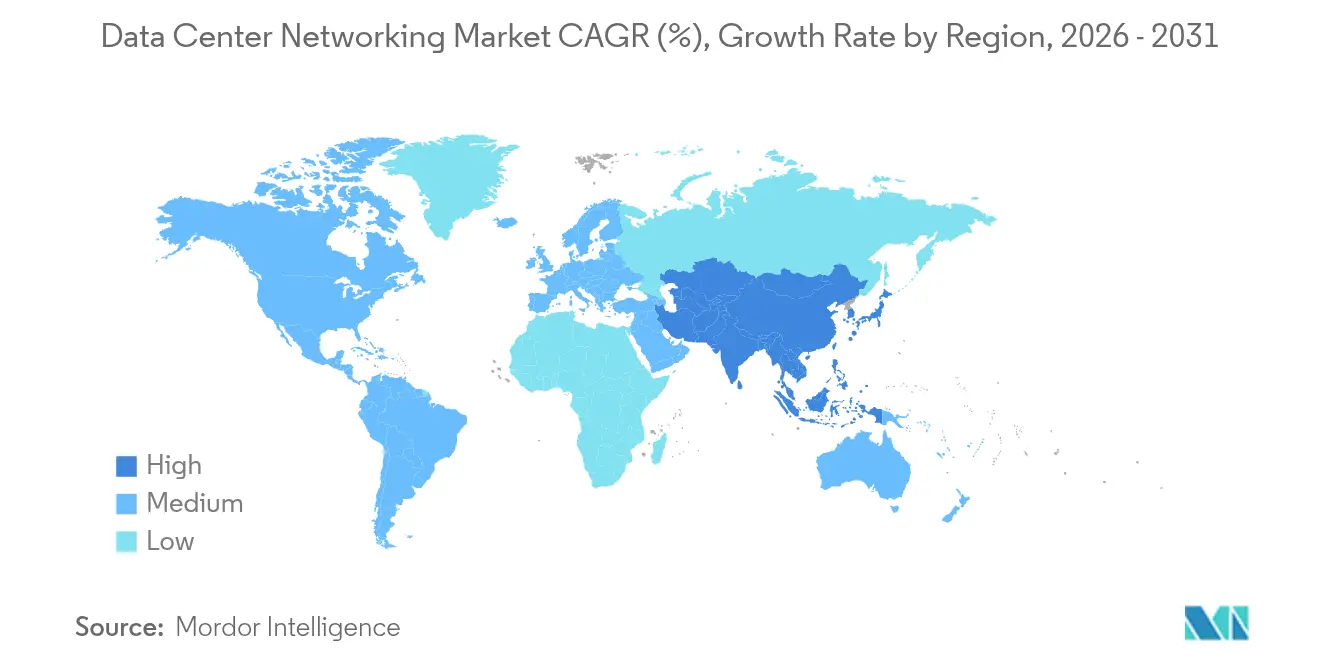

- Regionally, North America captured 26.05% of the 2025 data center networking market while Asia-Pacific is poised for the fastest 17.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Center Networking Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing cloud-first enterprise IT strategies | +3.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Surge in East-West traffic owing to AI/ML workloads | +4.1% | Global, led by Asia-Pacific hyperscale regions | Short term (≤ 2 years) |

| Edge data-center build-outs by telecom operators | +2.8% | Asia-Pacific core, spill-over to MEA and Latin America | Medium term (2-4 years) |

| 400 GbE port price erosion improves ROI | +1.9% | Global, early adoption in North America | Short term (≤ 2 years) |

| Adoption of lossless Ethernet for accelerated computing | +2.3% | North America and Asia-Pacific hyperscale markets | Medium term (2-4 years) |

| Hyperscalers' open-source network OS contributions | +1.5% | Global, concentrated in major cloud regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Cloud-First Enterprise IT Strategies

Enterprises replacing hub-and-spoke designs with micro-services generate unpredictable traffic bursts that demand software-defined overlays and realtime telemetry. Programmable switches, cloud-native firewalls, and zero-trust segmentation become mandatory as financial institutions expand cloud budgets. This driver sustains refresh cycles for 400 GbE leaf-spine fabrics and analytics engines that discover and remediate latency hotspots.

AI/ML East-West Traffic Surge

GPU clusters move gradients and parameters at volumes up to 100 times higher than legacy workloads, overwhelming conventional north-south architectures. RoCE-v2 with Priority Flow Control and Explicit Congestion Notification prevents packet loss during collective operations, while demand for 800 G and 1.6 T interfaces accelerates merchant-silicon innovation. [1]Alibaba HPN, "A Data Center Network for Large Language Model Training | Proceedings of the ACM SIGCOMM 2024 Conference," dl.acm.orgTier-2 clouds adopt Ethernet rather than proprietary transports to balance cost and interoperability.

Telecom-Led Edge Data-Center Build-Outs

Operators integrate carrier-grade timing with high-density Top-of-Rack switches to support 5G, IoT, and generative-AI inference at the network edge. Converged boxes with both BGP and VXLAN shorten deployment cycles in space-constrained shelters. Over 15 global telcos are now building AI-enabled micro sites that shift traffic away from regional cores.

400 GbE Port Price Erosion

Optics and switch ASIC costs for 400 GbE fell more than 35% between 2023 and 2025, giving mid-market enterprises economic headroom to leapfrog 100 G upgrades. The virtuous volume-cost loop enables hyperscalers to pilot 800 G links for forthcoming GPU generations while stimulating broader ecosystem adoption of QSFP-DD and OSFP transceivers.[2]Dell ,"64 x 400GbE: A Faster, Greener Data Center," dell.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-vendor interoperability challenges | -2.1% | Global, acute in enterprise environments | Medium term (2-4 years) |

| Rising network complexity and skill gaps | -1.8% | Global, concentrated in emerging markets | Long term (≥ 4 years) |

| Supply-chain risk for merchant silicon | -1.4% | Global, critical for APAC manufacturing | Short term (≤ 2 years) |

| Escalating data-center power density limits port upgrades | -2.3% | Global, severe in urban data centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Multi-Vendor Interoperability Issues

Proprietary protocol extensions impede seamless integration across switches, optics, and telemetry agents, forcing enterprises to invest in costly validation labs. [3]Verizon Communications, “Multi-Vendor Automation Lessons Learned,” verizon.com Delays in open-standard controller support extend migration timelines and create operational silos, particularly where AI clusters require deterministic latency guarantees across dissimilar fabrics.

Rising Network Complexity and Skill Gaps

Administrators must master lossless Ethernet semantics, GPU workload telemetry, and intent-based automation simultaneously. Certified talent pools remain scarce outside tier-one economies, driving demand for managed-service contracts and vendor-delivered automation. Knowledge shortages lengthen mean-time-to-repair and inflate operational budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Momentum Amid Complexity

Products retained 74.72% of data center networking market revenue in 2025, led by Ethernet switches that transitioned from 100 G to 400 G to satisfy AI workloads. Optical interconnects, storage fabrics, and application delivery controllers reinforced Product dominance but now face slowing unit growth as enterprises focus on architectural simplification. Vendors reported upticks in 51.2 Tbps chassis sales as GPU clusters expanded.

The Services segment is projected to grow at 17.7% CAGR as customers offload design, integration, and lifecycle management of lossless fabrics. Installation services for Priority Flow Control tuning, consulting on congestion metrics, and ongoing managed-fabric subscriptions fuel recurring revenue. Enterprises cite reduced mean-time-to-deploy by 38% after adopting turnkey managed operations, positioning Services as a critical enabler of AI business outcomes.

By End-User: Manufacturing Drives Edge Transformation

IT & Telecommunications captured 35.75% of the data center networking market in 2025 by virtue of hyperscale cloud, CDN, and telco investments that underpin digital-service delivery. Banking, media streaming, and e-commerce workloads dominate regional consumption across metro campuses.

Manufacturing & Industrial will advance at an 18.05% CAGR through 2031 as predictive-maintenance algorithms migrate from centralized clouds to factory-floor micro-data centers. Low-latency Ethernet fabrics link robotics, machine-vision cameras, and MES applications, cutting downtime and energy waste. Edge-native networking contracts have grown 2.4 times since 2023, underpinning sustained demand for compact, fanless 400 GbE leaf switches.

By Data-Center Type: Hyperscalers Lead AI Infrastructure

Colocation operators held 56.45% of 2025 revenue as enterprises pursued asset-light models but insisted on controlling their own layer-2 domains. Retrofit activity focused on liquid cooling loops and higher amperage feeds to accommodate racks exceeding 80 kW.

Hyperscaler and Cloud Service Provider campuses will rise at a 19.05% CAGR, accounting for the largest absolute addition to global optical backbones. AI clusters with 16,000+ GPUs require non-blocking Clos fabrics exceeding 2 Pbps, prompting system integrators to deploy fully integrated leaf-spine-superspine topologies pre-cabled at the factory. The result is an unprecedented pull-through effect for top-of-rack optics and 102.4 Tbps switching silicon.

By Bandwidth: Greater Than 100 GbE Segment Accelerates

Ports between 50 GbE and 100 GbE represented 38.15% of shipments in 2025 as enterprise refresh cycles caught up with hyperscale standards. However, the >100 GbE tier will grow 17.74% annually, driven by the data center networking market need for 400 G leafs and 800 G spines in AI clusters. In comparison, ≤10 GbE ports now concentrate in branch and management networks only.

The >100 GbE expansion correlates with merchant-silicon roadmaps offering 51.2 Tbps and 102.4 Tbps densities. Optoelectronic co-packaging and advanced PAM4 modulation further lower power per bit, partially offsetting rack-level thermal pressures. Early pilots of 1.6 T Ethernet are under evaluation by three hyperscalers for 2027 production clusters.

Geography Analysis

North America controlled 26.05% of 2025 revenue as the data center networking market scaled to support multi-billion-dollar hyperscale expansions. The United States dominates regional capex, while Canadian edge-cloud operators and Mexican near-shore campuses contribute incremental demand. Local equipment manufacturers benefit from favorable tax incentives and ultra-low carbon-intensity power grids.Asia-Pacific is the fastest-growing territory with a 17.55% CAGR through 2031, reflecting sovereign AI strategies that favor domestic processing. China’s Eastern-Data-Western-Compute backbone aligns eight desert-region hyperscale hubs with coastal interconnects, driving bulk transceiver procurement. India exceeded 950 MW installed IT load in 2025, triggering step-function demand for 400 GbE fabrics across both colocation and telco edge sites. Markets such as Indonesia and Vietnam reinforce the growth wave with supportive regulatory frameworks and regional subsea-cable investments.

Mordor Intelligence provides coverage of the data center networking market across other key regional markets, including Europe, Africa, North America, South America, Middle East, and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to Belgium, Nigeria, Canada, and Brazil incorporating local coverage and market participation, as required.

Competitive Landscape

Data center networking market competition is moderate but intensifying as AI optimizations shift value toward lossless fabrics and integrated telemetry. Arista Networks overtook Cisco in Q4 2023 switching revenue within hyperscale accounts by aligning its EOS operating system with AI congestion-control enhancements. NVIDIA capitalized on Spectrum-X to extend its GPU moat into Ethernet, targeting end-to-end AI platform ownership.

Cisco counters through Silicon One integration with NVIDIA’s platforms and by leveraging its enterprise installed base for cross-selling AI-ready fabrics. Juniper Networks’ impending acquisition by HPE signals a strategic move to fuse AI-native routing with edge-to-cloud stacks. Dell and Huawei compete on vertically-integrated racks that pre-stage copper-to-liquid cooling conversions. Start-ups such as Arrcus exploit cloud-neutral routing stacks to win Tier-2 cloud and colocation footprints where agility trumps vendor incumbency. Optical landscape dynamics include Nokia’s purchase of Infinera to create coherent-optics portfolios tuned for metro data-center-interconnect. The competitive frontier is now defined by co-packaged optics, adaptive routing for AI workloads, and cloud-native observability that unifies compute and network metrics.

Data Center Networking Industry Leaders

-

Cisco Systems Inc.

-

Arista Networks Inc.

-

Juniper Networks Inc.

-

Huawei Technologies Co. Ltd.

-

Dell Technologies (Dell EMC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: NVIDIA surpassed Cisco and Arista in datacenter Ethernet sales with its Spectrum-X platform, underscoring vertical AI-network integration ambitions.

- May 2025: Arista Networks posted record quarterly revenue above USD 2 billion and introduced Cluster Load Balancing plus CloudVision enhancements for AI telemetry.

- March 2025: Arista launched EOS Smart AI Suite delivering per-job congestion insights and fabric-wide load rebalancing.

- February 2025: Cisco and NVIDIA deepened partnership to co-design unified AI-ready fabrics blending Silicon One with Spectrum-X architectures.

Global Data Center Networking Market Report Scope

Data center networking refers to the set of technologies, protocols, and hardware used to connect physical and network-based devices and manage the network infrastructure, storage, and processing of applications and data. Data center networking is very critical for 100% uptime of data centers. In the current web-connected world, business workloads are executed on single computers, hence leading to the need for data center networking. Networks provide servers, clients, applications, and middleware with a standard plan to stage the execution of workloads and also to manage access to the data produced.

The global data center networking market is segmented by component type (product (ethernet switches, router, storage area network (SAN), application delivery controller (ADC), and other networking equipment), services (installation & integration, training & consulting, and support & maintenance)), end-user (IT & telecommunication, BFSI, government, media & entertainment, and other end-users) and region (North America, South America, Europe, Asia-Pacific, and Middle East and Africa)

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Products | Ethernet Switches |

| Routers | |

| Storage Area Network (SAN) | |

| Application Delivery Controllers (ADC) | |

| Network Security Appliances | |

| Software-Defined Networking (SDN) Controllers | |

| Optical Interconnects | |

| Services | Installation and Integration |

| Training and Consulting | |

| Support and Maintenance | |

| Managed Network Services |

| IT and Telecommunications |

| Banking, Financial Services and Insurance (BFSI) |

| Government and Defense |

| Media and Entertainment |

| Healthcare and Life Sciences |

| Manufacturing and Industrial |

| Other End-Users |

| Colocation |

| Hyperscalers/Cloud Service Providers |

| Edge/Micro Data Centers |

| Less than 10 GbE |

| 25-40 GbE |

| 50-100 GbE |

| Greater than 100 GbE |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Products | Ethernet Switches | |

| Routers | |||

| Storage Area Network (SAN) | |||

| Application Delivery Controllers (ADC) | |||

| Network Security Appliances | |||

| Software-Defined Networking (SDN) Controllers | |||

| Optical Interconnects | |||

| Services | Installation and Integration | ||

| Training and Consulting | |||

| Support and Maintenance | |||

| Managed Network Services | |||

| By End-User | IT and Telecommunications | ||

| Banking, Financial Services and Insurance (BFSI) | |||

| Government and Defense | |||

| Media and Entertainment | |||

| Healthcare and Life Sciences | |||

| Manufacturing and Industrial | |||

| Other End-Users | |||

| By Data-Center Type | Colocation | ||

| Hyperscalers/Cloud Service Providers | |||

| Edge/Micro Data Centers | |||

| By Bandwidth | Less than 10 GbE | ||

| 25-40 GbE | |||

| 50-100 GbE | |||

| Greater than 100 GbE | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the data center networking market?

The data center networking market size stands at USD 36.1 billion in 2026.

How fast is the data center networking market expected to grow?

Industry revenue is projected to rise at a 17.32% CAGR, reaching USD 80.21 billion by 2031.

Which region is growing the quickest?

Asia-Pacific is forecast to post the fastest 17.55% CAGR through 2031, buoyed by China’s Eastern-Data-Western-Compute program and India’s 950 MW capacity build-out.

Why are services outpacing product growth?

The complexity of AI-optimized fabrics is driving enterprises to outsource design, integration, and lifecycle management, pushing the Services segment to a 17.7% CAGR.

Page last updated on: